|

市場調查報告書

商品編碼

1940609

棒狀包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Stick Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

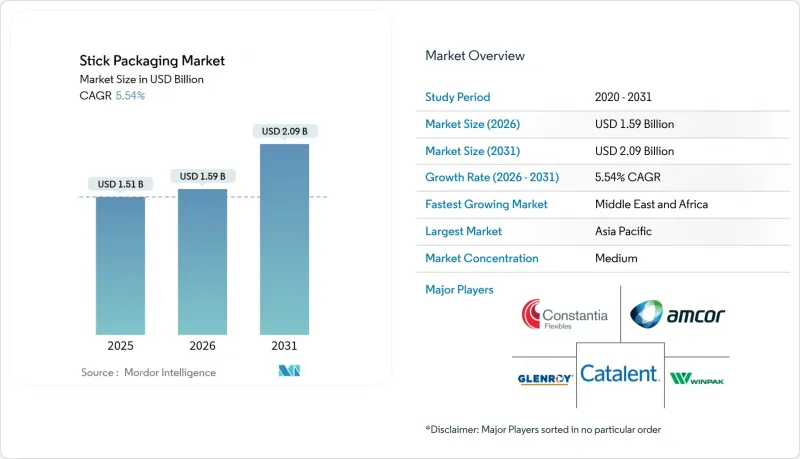

2025年,棒狀包裝市場價值為15.1億美元,預計到2031年將達到20.9億美元,高於2026年的15.9億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.54%。

這一前景得益於消費者對便捷單份包裝日益成長的需求、減少塑膠廢棄物的監管壓力不斷加大,以及柔軟性薄膜阻隔性能的持續提升。製造商正投資數位印刷機以滿足小批量個人化訂單的需求,品牌所有者也優先考慮份量控制的優勢,以順應健康意識的趨勢。樹脂價格的波動和鋁關稅的影響提升了輕質複合材料的相對吸引力。同時,為滿足電商物流效率目標,供應商正致力於開發能夠最佳化體積運輸成本的窄型緊湊包裝。主要加工商之間的整合加劇了其採購能力,加速了可回收單一材料結構的規模化生產。

全球棒狀包裝市場趨勢與洞察

便利性和行動消費的蓬勃發展

城市生活方式的興起和女性勞動參與率的提高,使得便攜性成為重要的購買考量因素,促使消費者選擇單份包裝。品牌商表示,以可放入口袋或健身包的纖薄小袋包裝銷售粉狀飲料、即溶咖啡和電解質飲料時,家庭用戶接受度顯著提升。速食連鎖店正將此概念延伸至調味品領域,從笨重的包裝袋轉向細長的條狀容器,從而減少高達35%的包裝材料。同時,電商食品平台也青睞條狀包裝的長方形形狀,可以最大限度地減少包裝空隙,並降低配送成本。便利性和配送效率的良性循環,為條狀包裝市場帶來了長期的良好需求。

對材料和重量減少的需求

原料成本上漲正促使人們更加重視薄壁複合材料的應用。預計到2025年初,瓦楞紙板價格將上漲70美元/噸,而美國對鋁箔徵收25%的進口關稅,進一步拉大了硬質和軟質基材之間的成本差距。與枕形袋相比,條狀包裝通常每克產品可節省30-40%的薄膜用量,有助於品牌商減輕樹脂價格波動的影響。供應商正抓住這一機遇,推出更薄的密封層(不會影響加工性能)和更高產量比率的聚乙烯基阻隔材料。這些變化共同增強了條狀包裝市場在通膨環境下的競爭力。

加強對一次性塑膠製品的監管

對某些一次性產品的禁令以及對再生樹脂含量低於30%的包裝課稅,增加了多層複合材料的合規成本。在英國,不合規包裝最高可被處以每噸200英鎊的罰款,這促使供應商要求提供經認證的再生樹脂含量證明。由於條狀包裝的材料用量低且薄膜寬度窄,再生樹脂的整合面臨挑戰,即使是微小的缺陷也會影響生產線速度。加工商必須加快物料平衡認證樹脂的合格,以確保提高產量。

細分市場分析

到2025年,塑膠產品板塊將佔總收入的63.42%,這主要得益於成本效益高的PE和PET結構,這些結構具有成熟的加工窗口。對薄壁共壓製產品和基於EVOH的氧氣阻隔材料的需求,幫助該板塊即使在監管審查下也保持了市場佔有率。然而,生質塑膠預計將以10.24%的複合年成長率成長,這是所有材料板塊中最高的成長率。弗勞恩霍夫研究所等生產商已經展示了80%生物基PLA共混物,其柔軟性與LDPE相當,突破了性能上的重大瓶頸。紙箔混合材料目前仍處於小眾市場,但由於其保存期限短,調味品領域的需求正在成長。

從價值角度來看,傳統基材至少在2028年之前仍將主導棒狀包裝市場規模,但隨著可追溯成分認證的實施,生物基薄膜將成為成長的主要來源,這將釋放企業在環境、社會和治理(ESG)方面的採購預算。領先的跨國飲料品牌正在就生物基聚乙烯(bio-PE)的多年採購協議進行談判,以確保在監管截止日期前獲得供應。同時,由於關稅政策的影響,金屬箔的成本不斷上漲,預計其應用範圍將僅限於需要99%或更高遮光率的高阻隔阻隔性藥品棒狀包裝。最終的結果將是一個漸進的重新平衡過程,而非突如其來的變革。

到2025年,粉狀產品將佔棒狀包裝市場57.35%的佔有率,這反映了其在即溶咖啡、膳食補充劑和運動營養混合物等領域的廣泛應用。粉末狀產品的高流動性使其能夠快速填充並實現可靠的密封性能,從而帶來優異的單位經濟效益。然而,由於採用具有更佳黏度控制的連續運動垂直灌裝封口(VFFS)平台,液體產品的複合年成長率預計將達到8.92%。正如Futamura公司利用水溶性薄膜製成的可堆肥小袋所展示的那樣,性能差距正在縮小,液體棒狀產品在旅行個人護理套裝中也變得越來越常見。

機能飲料品牌非常重視液體棒提供的10毫升至15毫升的精準分裝量,方便消費者根據需要取用膠原蛋白蛋白或電解質補充劑。在物流方面,液體棒包裝採用平板車運輸,而非笨重的寶特瓶,顯著降低了運輸成本和碳排放。隨著機械製造商不斷改進防滴漏噴嘴設計,預計到2031年,液體棒包裝市場規模將達到6.73億美元,雖然在絕對規模上落後於粉末包裝,但其相對成長率卻超過了粉末包裝。由於對剪切力的要求較高且缺乏自動化選項,顆粒狀和半固體填充物的成長速度預計將較為緩慢。

區域分析

預計到2025年,亞太地區將佔據35.44%的收入佔有率,其中中國和印度不斷壯大的中階將推動對分量控制飲料和營養補充劑的需求。都市區消費者更青睞小袋裝多包裝產品,這種包裝便於收納於空間有限的廚房,並能與基於應用程式的生鮮配送服務無縫銜接。本土品牌商正受益於垂直整合的薄膜擠出叢集,這些集群能夠縮短前置作業時間並降低最低訂購量。同時,政府鼓勵採用生物基聚合物的政策也開始影響材料的選擇,推動了甘蔗衍生聚乙烯的早期試驗。

北美是第二大區域貢獻者,這得益於其高階定位以及在醫藥和營養保健品應用領域不斷成長的滲透率。美國擁有眾多機械設備原始設備製造商 (OEM) 和合約包裝公司,形成了一個良性循環的生態系統,加速了新產品 (SKU) 的市場上市。然而,不斷上漲的運輸成本和波動的樹脂價格帶來了不利影響,迫使一些產能擴張計畫轉移到墨西哥等鄰近地區。

歐洲一直是永續性的標竿。即將推出的包裝和包裝廢棄物法規迫使加工商重新設計複合材料結構以提高其可回收性,該地區也因此成為單一材料PE/EVOH共混物的技術試驗場。中東和非洲地區雖然絕對規模仍小規模,但其複合年成長率高達6.66%。可支配收入的成長和餐飲服務業的快速發展推動了單份咖啡、果汁和香辛料包裝產品的應用,同時,區域各國政府正積極吸引外國直接投資(FDI)進入軟包裝製造業,以擺脫對石化行業的依賴。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 便利性和行動消費的蓬勃發展

- 對材料和重量減少的需求

- 軟包裝的永續性要求

- 藥物微劑量和兒童劑型

- 用於大量客製化包裝袋的數位印刷

- 電子商務中樣品包的普遍性

- 市場限制

- 加強對一次性塑膠製品的監管

- 多層薄膜的可回收性局限性

- 阻隔級單材料薄膜短缺

- 高黏度灌裝精度極限 > 15 道

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 激烈的競爭

- 關鍵績效指標(KPI)

第5章 市場規模與成長預測

- 材料

- 塑膠

- 紙

- 金屬箔

- 生質塑膠

- 按產品形式

- 粉末

- 顆粒

- 液體

- 半固體

- 按最終用戶行業分類

- 食品/飲料

- 即溶飲料

- 膳食補充劑粉

- 糖和甜味劑

- 製藥

- OTC

- Rx

- 化妝品和個人護理

- 工業和家用

- 食品/飲料

- 按包裝器材通道數

- 1至3號車道

- 第4至10號車道

- 第11至20泳道

- 20條或更多車道

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Constantia Flexibles Group GmbH

- Glenroy, Inc.

- Aranow Packaging Machinery SL

- Fres-Co System USA, Inc.

- Catalent, Inc.

- Winpak Ltd.

- Sonoco Products Company

- ePac Holdings, LLC

- GFR Pharma Ltd.

- Sonic Packaging Industries, Inc.

- Viking Masek Global Packaging Technologies sro

- Nichrome India Ltd.

- Unither Pharmaceuticals SAS

- Marchesini Group SpA

第7章 市場機會與未來展望

The stick packaging market was valued at USD 1.51 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 2.09 billion by 2031, at a CAGR of 5.54% during the forecast period (2026-2031).

Growing demand for convenient single-serve formats, mounting regulatory pressure to curb plastic waste, and continuous improvements in flexible-film barrier performance underpin this outlook. Producers are investing in digital presses to serve personalized short-run orders, while brand owners lean on portion-control benefits to align with wellness trends. Resin price volatility and aluminum tariffs are increasing the relative attractiveness of lightweight laminates. At the same time, the need to meet e-commerce fulfilment efficiency targets is pushing suppliers to favor narrow, compact packs that optimize volumetric shipping costs. Consolidation among top converters is boosting purchasing leverage and accelerating the scale-up of recyclable mono-material structures.

Global Stick Packaging Market Trends and Insights

Convenience & On-the-Go Consumption Boom

City-centric lifestyles and rising female workforce participation have made portability a prime purchase criterion, steering consumers toward single-dose packs. Brand owners report higher household penetration when powder beverages, instant coffee, or electrolyte mixes are sold in slim sachets that fit pockets and gym bags. Quick-service chains are extending this logic to condiments, replacing bulky pouches with narrow sticks that reduce pack material by as much as 35%. In parallel, e-commerce grocery platforms value the rectangular footprint of stick packs because it minimizes void space and shipping fees. The self-reinforcing cycle between lifestyle convenience and channel efficiency places the stick packaging market in a favorable long-run demand position.

Demand for Material & Weight Reduction

Input-cost inflation is sharpening the focus on downgauged laminates. Corrugated board prices rose USD 70 per ton in early 2025, and aluminum foil attracts 25% import tariffs in the United States, widening the cost delta between rigid and flexible substrates. Stick formats typically consume 30-40% less film area per gram of product than pillow pouches, allowing brand owners to limit exposure to resin price swings. Suppliers are capitalizing by introducing thinner sealant layers and higher-yield PE-based barriers that do not compromise machinability. Together, these shifts are reinforcing the stick packaging market's competitiveness in inflationary environments.

Single-Use-Plastic Regulation Tightening

Bans on certain single-use articles and taxes on packaging containing less than 30% recycled resin are raising compliance costs for multi-layer laminates. Financial penalties in the United Kingdom can reach GBP 200 per ton for non-conforming packs, prompting retailers to pressure suppliers for verified PCR content. Although stick formats use less material, their narrow gauge complicates PCR incorporation because small film defects can impair line speeds. Converters must therefore accelerate the qualification of mass-balance certified resins to safeguard volume growth.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Mandates for Flexible Packs

- Pharma Micro-Dosing & Pediatric Formats

- Limited Recyclability of Multi-Layer Films

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The plastics family accounted for 63.42% of 2025 revenue, underpinned by cost-effective PE and PET structures that offer well-established processing windows. Demand for downgauged coextrusions and EVOH-based oxygen barriers helped the segment preserve share despite regulatory scrutiny. However, bioplastics are projecting a 10.24% CAGR, the fastest across the material spectrum. Producers such as Fraunhofer Institute have demonstrated PLA blends with 80% bio-based content that replicate LDPE flexibility, clearing a significant performance hurdle. Paper-foil hybrids remain niche but are gaining traction in condiment channels that tolerate shorter shelf life.

In value terms, traditional substrates will continue to dominate the stick packaging market size until at least 2028, yet the incremental gains will concentrate in bio-based films as traceable feedstock certification unlocks ESG procurement budgets. Early movers among multinational beverage brands are negotiating multi-year offtake contracts for bio-PE to secure volumes ahead of regulatory deadlines. Meanwhile, metal foils face cost inflation from tariff regimes, limiting their use to high-barrier pharmaceutical sticks that demand >99% light protection. The net result is a gradual rebalancing rather than a sudden disruption.

Powder applications retained 57.35% of the stick packaging market in 2025, reflecting entrenched usage in instant coffee, dietary supplements, and sports nutrition mixes. Their free-flowing nature enables high-speed filling and reliable seal integrity, supporting attractive unit economics. That said, liquids are on track for a brisk 8.92% CAGR, supported by continuous-motion vertical form-fill-seal (VFFS) platforms equipped with improved viscosity control. Futamura's demonstration of compostable film for aqueous sachets illustrates how performance gaps are narrowing, making liquid sticks a more common sight in personal-care travel kits.

Functional beverage brands value the precise 10 ml to 15 ml dose that liquid sticks deliver, enabling consumers to mix collagen shots or electrolyte boosters on demand. From a logistics standpoint, packs ship as flat carts rather than bulky PET bottles, slashing freight costs and carbon intensity. As machinery OEMs refine nozzle design to prevent drips, the stick packaging market size for liquids is expected to reach USD 673 million by 2031, outpacing powders in relative expansion though not absolute scale. Granular and semi-solid fillings will grow more moderately, held back by higher shearing requirements and fewer automated equipment options.

The Stick Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foils, Bioplastics), Product Form (Powders, Granules, Liquids, Semi-Solids), End-User Industry (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Industrial & Household), Packaging-Machinery Lane Count (1-3 Lanes, 4-10 Lanes, 11-20 Lanes, Greater Than 20 Lanes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded a 35.44% revenue share in 2025, anchored by China's and India's expanding middle-class appetites for portion-controlled beverages and nutraceuticals. Urban consumers gravitate toward sachet multipacks that fit small kitchens and integrate seamlessly with app-based grocery delivery. Local brand owners benefit from vertically integrated film extrusion clusters, which shorten lead times and lower minimum order quantities. Meanwhile, government initiatives that encourage bio-based polymer adoption are beginning to influence material selection, fostering early experimentation with sugarcane-sourced PE.

North America ranks as the second-largest regional contributor, supported by premium positioning and greater penetration of pharmaceutical and nutraceutical applications. The United States also hosts a deep roster of machinery OEMs and contract packers, reinforcing a virtuous ecosystem that accelerates time-to-market for new SKUs. However, elevated freight costs and resin volatility create headwinds, pushing some capacity expansion plans toward nearshore sites in Mexico.

Europe remains the rule-setter on sustainability. The forthcoming Packaging and Packaging Waste Regulation is compelling converters to redesign laminate structures for recyclability, making the region a technology test bed for mono-material PE/EVOH blends. Middle East & Africa, while still small in absolute dollars, is on pace for a 6.66% CAGR. Rising disposable incomes and rapid food-service expansion support single-serve coffee, juice, and spice applications, while regional governments court FDI into flexible-pack manufacturing to diversify away from hydrocarbons.

- Amcor plc

- Constantia Flexibles Group GmbH

- Glenroy, Inc.

- Aranow Packaging Machinery S.L.

- Fres-Co System USA, Inc.

- Catalent, Inc.

- Winpak Ltd.

- Sonoco Products Company

- ePac Holdings, LLC

- GFR Pharma Ltd.

- Sonic Packaging Industries, Inc.

- Viking Masek Global Packaging Technologies s.r.o.

- Nichrome India Ltd.

- Unither Pharmaceuticals SAS

- Marchesini Group S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience and on-the-go consumption boom

- 4.2.2 Demand for material and weight reduction

- 4.2.3 Sustainability mandates for flexible packs

- 4.2.4 Pharma micro-dosing and pediatric formats

- 4.2.5 Digital printing for mass-customised sachets

- 4.2.6 E-commerce sample sachet proliferation

- 4.3 Market Restraints

- 4.3.1 Single-use-plastic regulation tightening

- 4.3.2 Limited recyclability of multi-layer films

- 4.3.3 Barrier-grade mono-material film shortage

- 4.3.4 High-viscosity fill accuracy limits >15 lanes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Key Performance Indicators (KPIs)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.2 Paper

- 5.1.3 Metal Foils

- 5.1.4 Bioplastics

- 5.2 By Product Form

- 5.2.1 Powders

- 5.2.2 Granules

- 5.2.3 Liquids

- 5.2.4 Semi-solids

- 5.3 By End-user Industry

- 5.3.1 Food and Beverages

- 5.3.1.1 Instant Beverages

- 5.3.1.2 Nutraceutical Powders

- 5.3.1.3 Sugar and Sweeteners

- 5.3.2 Pharmaceuticals

- 5.3.2.1 OTC

- 5.3.2.2 Rx

- 5.3.3 Cosmetics and Personal Care

- 5.3.4 Industrial and Household

- 5.3.1 Food and Beverages

- 5.4 By Packaging-Machinery Lane Count

- 5.4.1 1-3 Lanes

- 5.4.2 4-10 Lanes

- 5.4.3 11-20 Lanes

- 5.4.4 Greater than 20 Lanes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Amcor plc

- 6.4.2 Constantia Flexibles Group GmbH

- 6.4.3 Glenroy, Inc.

- 6.4.4 Aranow Packaging Machinery S.L.

- 6.4.5 Fres-Co System USA, Inc.

- 6.4.6 Catalent, Inc.

- 6.4.7 Winpak Ltd.

- 6.4.8 Sonoco Products Company

- 6.4.9 ePac Holdings, LLC

- 6.4.10 GFR Pharma Ltd.

- 6.4.11 Sonic Packaging Industries, Inc.

- 6.4.12 Viking Masek Global Packaging Technologies s.r.o.

- 6.4.13 Nichrome India Ltd.

- 6.4.14 Unither Pharmaceuticals SAS

- 6.4.15 Marchesini Group S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

棒狀包裝市場:按材料、產品類型、應用、分銷管道和地區分類

棒狀包裝市場:按材料、產品類型、應用、分銷管道和地區分類 棒狀包裝市場:依產品類型、材料類型、產品形式、包裝尺寸、封口方式及最終用途分類-全球預測,2026-2032年

棒狀包裝市場:依產品類型、材料類型、產品形式、包裝尺寸、封口方式及最終用途分類-全球預測,2026-2032年 條狀包裝市場報告:按材料、填充類型、容量、應用和地區分類(2026-2034 年)

條狀包裝市場報告:按材料、填充類型、容量、應用和地區分類(2026-2034 年) 全球條狀包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)楝樹棒市場:依產品類型、應用程式、最終用戶、通路和地區分類。

全球條狀包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)楝樹棒市場:依產品類型、應用程式、最終用戶、通路和地區分類。 條狀包裝市場規模、佔有率及成長分析(按材料、終端用途產業及地區分類)-2026-2033年產業預測

條狀包裝市場規模、佔有率及成長分析(按材料、終端用途產業及地區分類)-2026-2033年產業預測 棒狀包裝市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2025-2033 年)

棒狀包裝市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2025-2033 年) 北美棒狀包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)糖包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

北美棒狀包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)糖包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 棒包裝市場機會、成長動力、產業趨勢分析及 2024 年至 2032 年預測

棒包裝市場機會、成長動力、產業趨勢分析及 2024 年至 2032 年預測