|

市場調查報告書

商品編碼

1939753

南美洲廢棄物管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)South American Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

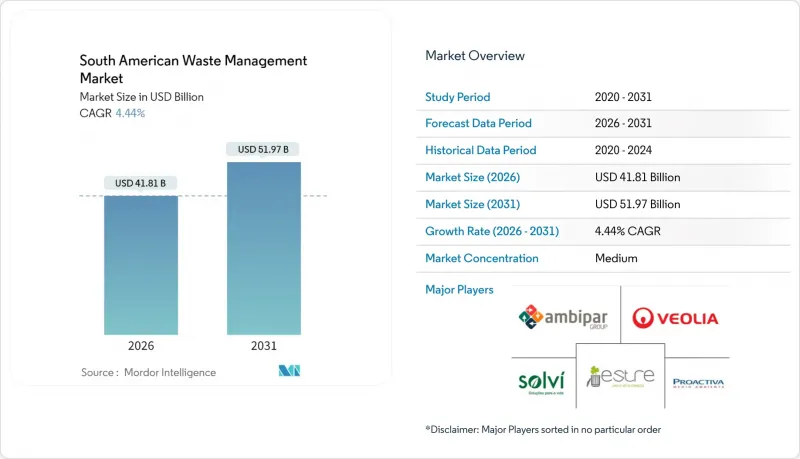

預計南美洲廢棄物管理市場將從 2025 年的 400.3 億美元成長到 2026 年的 418.1 億美元,到 2031 年將達到 519.7 億美元,2026 年至 2031 年的複合年成長率為 4.44%。

人口成長、快速都市化以及日益嚴格的監管(尤其是巴西於2024年6月宣布的《國家循環經濟戰略》)支撐了市場需求前景,而綠色債券的流入正在加速廢棄物發電(WtE)和高回收利用率資產的部署。隨著地方政府提高掩埋稅,生產商面臨強制性回收目標,傳統的垃圾處理模式正穩步向資源回收平台轉變。

南美洲廢棄物管理市場趨勢與洞察

快速的都市化正在推高城市垃圾的產生量。

南美城市正以數十年來最快的速度擴張,巴西的都市區每年產生超過8,300萬噸都市廢棄物。目前,只有4-5%的廢棄物得到正規收集,凸顯了巨大的處理能力缺口,也為收集和處理於一體的綜合平台創造了極具吸引力的市場。哥倫比亞的麥德林等城市正在試驗將非正式收集合作社納入市政服務合約的模式,這表明社會包容性和規模效益可以兼得。雖然農村城市的人口集中增加了物流的複雜性,但也帶來了路線密度優勢,降低了每噸垃圾的收整合本。市政領導人越來越意識到,僅靠新建掩埋無法處理日益成長的垃圾量,這進一步凸顯了建立以回收和能源回收為核心的多流系統的重要性。

巴西和智利的循環經濟法律

監理改革正在推動結構性變革。巴西國家循環經濟戰略要求生產商優先考慮產品重新設計和再利用,鼓勵企業投資建造高產能分類線和先進的材料回收設施。智利第20.920號法律將生產商責任擴展至包裝、電子產品和電池,並制定了可強制執行的回收目標,這些目標將從2023年開始分階段實施。這些法規為能夠證明其符合審核的材料回收指標的企業創造了競爭優勢。光學分類機、生物消化器和廢棄物衍生燃料(RDF)系統的設備供應商報告稱,與這些強制性要求相關的競標有所增加。從長遠來看,這些立法有望抑制原料進口,並將工業需求轉向本地回收材料。

非正規廢棄物收集者的主導地位

在巴西,約90%的回收物由非正規回收商收集,但他們的營運不受法律規範。聖保羅州一項旨在規範合作社的計劃,到2017年僅有不到1%的路邊回收商參與其中,凸顯了社會、經濟和物流方面的障礙。雖然高效收集高價值可回收物可以減少掩埋的需求,但缺乏協調的分類會降低材料質量,並使正規承包商的路線規劃更加複雜。一項在巴西25個城市開展的綜合計畫表明,透過提供培訓和設備,由回收商主導的分類中心可以將收整合本降低至每噸35美元(而傳統的挨家挨戶收集模式的成本為每噸195.3美元)。然而,專案的成功取決於穩定的市政資金和透明的收入分配。

細分市場分析

到2025年,住宅廢棄物將佔南美廢棄物管理市場的56.02%,成為垃圾收集業者路線規劃和資金配置決策的基礎。住宅垃圾不僅數量龐大,而且成分複雜,涵蓋有機物到軟質塑膠等多種物質,因此需要先進的分類和運輸能力。儘管主要城市的垃圾收集覆蓋率超過90%,但資源回收率仍低於10%,這表明在進行先進的上門分類和計量型計畫方面仍有很大的提升空間。住宅廢棄物的龐大規模為提供物聯網垃圾收集容器和卡車調度最佳化分析平台的技術供應商提供了極具吸引力的市場。能夠實現稱重資料自動化的營運商可以提高計費準確性,並為垃圾焚化發電(WtE)投資者提供所需的原料供應保障。

商業廢棄物正以6.22%的複合年成長率成長,預計到2031年將成為成長最快的廢棄物來源,這主要得益於波哥大、聖地牙哥和利馬零售業和旅館業的擴張。更嚴格的職業健康法規促使購物中心和酒店與許可機構簽訂合約。品牌擁有者的ESG(環境、社會和治理)目標刺激了對閉合迴路包裝方案的需求。在工業廢棄物領域,巴西優先考慮戰略材料國內再加工的進口法規提高了審查力度,迫使工廠尋找本地回收合作夥伴。一種「前端整合」的趨勢正在興起,飲料品牌在其工廠安裝包裝機,並將壓縮PET直接出售給回收商,從而減少了仲介業者環節。建築廢棄物仍然是服務最不足的領域,但哥倫比亞和秘魯不斷上漲的廢棄物處理稅正在獎勵破碎和回收企業的發展。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速的都市化導致需要處理的城市垃圾數量不斷增加。

- 巴西和智利的循環經濟立法

- 安地斯國家擴大掩埋稅制度

- 用於廢棄物發電廠的綠色債券資金籌措激增

- 礦業零廢棄物指令

- 市場限制

- 非正規廢棄物收集者的主導地位

- 地方政府預算缺口

- 跨境危險廢棄物貿易

- 電網互聯程度有限,削弱了廢棄物發電(WtE)的經濟效益。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 物流基礎設施洞察

- Start-Ups策略與創業融資

第5章 市場規模及成長預測(價值,單位:十億美元)

- 按來源

- 住宅

- 商業設施(零售商店、辦公室等)

- 產業

- 醫療(健康和醫藥)

- 建築和廢棄物廢棄物

- 其他(引擎廢棄物、農業廢棄物等)

- 按服務類型

- 收集、運輸、分類和分離

- 處理/處置

- 掩埋處置

- 回收和資源回收

- 焚燒和廢棄物發電

- 其他(化學處理、堆肥等)

- 其他(諮詢、審核、訓練等)

- 依廢物類型

- 都市固態廢棄物

- 工業用危險廢棄物

- 電子廢棄物

- 塑膠廢棄物

- 醫療廢棄物

- 建築和拆除廢棄物

- 農業廢棄物

- 其他特殊廢棄物(放射性廢棄物等)

- 按地區

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Veolia Latin America

- Estre Ambiental

- Grupo Solvi

- Ambipar

- Proactiva Medio Ambiente

- Waste Management Inc.

- Republic Services Inc.

- Casella Waste Systems

- Covanta Holding Corporation

- Inciner8 Ltd

- SWM Colombia

- Capitao Ambiental

- Entorno Sustentable

- Syngas do Brasil

- Usina Verde

- Bioelektra

- Estaciones Ecologicas

- Solvi Essencis

- Reciclar SA

- TRASHCo Peru

第7章 市場機會與未來展望

The South American Waste Management Market is expected to grow from USD 40.03 billion in 2025 to USD 41.81 billion in 2026 and is forecast to reach USD 51.97 billion by 2031 at 4.44% CAGR over 2026-2031.

Population growth, rapid urbanization, and tightening regulations, especially Brazil's National Circular Economy Strategy of June 2024, anchor the demand outlook, while green-bond inflows are accelerating the deployment of waste-to-energy (WtE) and advanced recycling assets. Regional governments are raising landfill taxes, and producers face mandatory collection targets, driving a measured pivot from linear disposal models to resource-recovery platforms.

South American Waste Management Market Trends and Insights

Rapid Urbanization Boosting MSW Volumes

South America's cities are expanding at their fastest pace in decades, with Brazil's urban centers generating more than 83 million tons of municipal solid waste annually. Only 4-5% of this material presently undergoes formal recovery, which underscores the sizable capacity gap and opens attractive niches for integrated collection-to-treatment platforms. Colombian hubs such as Medellin are piloting models that fold informal picker cooperatives into municipal service contracts, proving that social inclusion and scale efficiencies can coexist. The concentration of population in secondary cities compounds the logistical complexity, yet also yields route-density advantages that can lower per-ton collection costs. Municipal leaders increasingly accept that new landfills alone cannot absorb climbing waste volumes, reinforcing the case for multi-stream systems anchored by recycling and energy recovery assets.

Circular-Economy Legislation in Brazil & Chile

Regulatory reform is driving structural change. Brazil's National Circular Economy Strategy obliges producers to redesign products and prioritize reuse, compelling operators to invest in high-throughput sorting lines and advanced material-recycling facilities. Chile's Law 20.920 extends producer responsibility to packaging, electronics, and batteries, with enforceable collection targets that began phasing in during 2023. These rules tilt the competitive field toward players that can back up compliance claims with auditable resource-recovery metrics. Equipment suppliers of optical sorters, biodigesters, and refuse-derived-fuel (RDF) systems report increasing tenders tied to these mandates. Over the long haul, the legislation is expected to curb raw-material imports, channeling industrial demand toward locally recovered feedstock.

Dominance of Informal Waste Pickers

Informal recyclers recover nearly 90% of Brazil's recycled materials, yet operate outside tax and safety frameworks. Attempts to formalize cooperatives in Sao Paulo captured fewer than 1% of street pickers by 2017, revealing the scale of social, economic, and logistical hurdles. While their efficiency in collecting high-value recyclables relieves landfill demand, uncoordinated sorting can degrade material quality and complicate route planning for formal contractors. Integration programs in 25 Brazilian municipalities show that with training and equipment, picker-led sorting centers can cut collection costs to USD 35 per ton versus USD 195.3 for conventional curbside models. Success, however, hinges on steady municipal funding and transparent revenue-sharing.

Other drivers and restraints analyzed in the detailed report include:

- Rising Landfill-Tax Regimes Across Andean Nations

- Surge in Green-Bond Financing for WtE Plants

- Municipal Budget Shortfalls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential waste streams captured 56.02% of the South American waste management market share in 2025, anchoring route planning and capital-allocation decisions for collectors. Household refuse is not only voluminous but also compositionally diverse, ranging from organics to flexible plastics, which demands sophisticated sorting and transfer capacity. Collection coverage in large cities tops 90%, yet material recovery remains below 10%, signaling room for advanced curbside segregation and pay-as-you-throw pilots. The residential stream's sheer scale is a magnet for technology vendors offering IoT-enabled collection bins and analytics platforms that optimize truck dispatch. Operators that automate weigh-ticket data improve billing accuracy and unlock feedstock assurances sought by WtE financiers.

Commercial waste is advancing at a 6.22% CAGR, emerging as the fastest-growing source through 2031 on the back of retail and hospitality expansion across Bogota, Santiago, and Lima. Stricter occupational health rules push malls and hotels to contract licensed handlers, while brand-owner ESG targets stimulate demand for closed-loop packaging programs. Industrial waste streams face rising scrutiny as Brazil's import-control decree prioritizes domestic reprocessing of strategic materials, nudging factories to secure local recovery partners. A forward integration trend is observable where beverage brands install on-site balers and sell compacted PET directly to recyclers, squeezing out intermediaries. Construction debris remains the least served, yet rising disposal taxes in Colombia and Peru present incentives for crushing and reuse businesses.

The South American Waste Management Market Report is Segmented by Source (Residential, Commercial, Industrial, and More), by Service Type (Collection, Transportation, Sorting & Segregation, and More), by Waste Type (Municipal Solid, Industrial Hazardous Waste, E-Waste, and More), and Geography (Brazil, Argentina, Chile, Colombia, Peru, and the Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Veolia Latin America

- Estre Ambiental

- Grupo Solvi

- Ambipar

- Proactiva Medio Ambiente

- Waste Management Inc.

- Republic Services Inc.

- Casella Waste Systems

- Covanta Holding Corporation

- Inciner8 Ltd

- SWM Colombia

- Capitao Ambiental

- Entorno Sustentable

- Syngas do Brasil

- Usina Verde

- Bioelektra

- Estaciones Ecologicas

- Solvi Essencis

- Reciclar S.A.

- TRASHCo Peru

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation boosting MSW volumes

- 4.2.2 Circular-economy legislation in Brazil & Chile

- 4.2.3 Rising landfill-tax regimes across Andean nations

- 4.2.4 Surge in green-bond financing for WtE plants

- 4.2.5 Mining-sector zero-waste mandates

- 4.3 Market Restraints

- 4.3.1 Dominance of informal waste pickers

- 4.3.2 Municipal budget shortfalls

- 4.3.3 Cross-border hazardous-waste trafficking

- 4.3.4 Limited grid interconnection hurting WtE economics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Logistics Infrastructure Insights

- 4.9 Startup Strategies & Venture Funding

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Veolia Latin America

- 6.4.2 Estre Ambiental

- 6.4.3 Grupo Solvi

- 6.4.4 Ambipar

- 6.4.5 Proactiva Medio Ambiente

- 6.4.6 Waste Management Inc.

- 6.4.7 Republic Services Inc.

- 6.4.8 Casella Waste Systems

- 6.4.9 Covanta Holding Corporation

- 6.4.10 Inciner8 Ltd

- 6.4.11 SWM Colombia

- 6.4.12 Capitao Ambiental

- 6.4.13 Entorno Sustentable

- 6.4.14 Syngas do Brasil

- 6.4.15 Usina Verde

- 6.4.16 Bioelektra

- 6.4.17 Estaciones Ecologicas

- 6.4.18 Solvi Essencis

- 6.4.19 Reciclar S.A.

- 6.4.20 TRASHCo Peru

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球多氟烷基物質(PFAS)廢棄物管理市場報告2026年全球廢棄物管理與回收服務市場報告2026年全球紡織廢棄物管理市場報告2026年全球廢棄物管理軟體市場報告2026年全球放射性廢棄物管理系統市場報告2026年全球水務和廢棄物管理諮詢服務市場報告

2026年全球多氟烷基物質(PFAS)廢棄物管理市場報告2026年全球廢棄物管理與回收服務市場報告2026年全球紡織廢棄物管理市場報告2026年全球廢棄物管理軟體市場報告2026年全球放射性廢棄物管理系統市場報告2026年全球水務和廢棄物管理諮詢服務市場報告 全球廢棄物管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球廢棄物管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 廢棄物管理市場分析及預測(至2035年):按類型、產品、服務、技術、應用、材料類型、製程及最終用戶分類

廢棄物管理市場分析及預測(至2035年):按類型、產品、服務、技術、應用、材料類型、製程及最終用戶分類 新加坡廢棄物管理市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)越南廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

新加坡廢棄物管理市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)越南廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)