|

市場調查報告書

商品編碼

1939747

越南廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

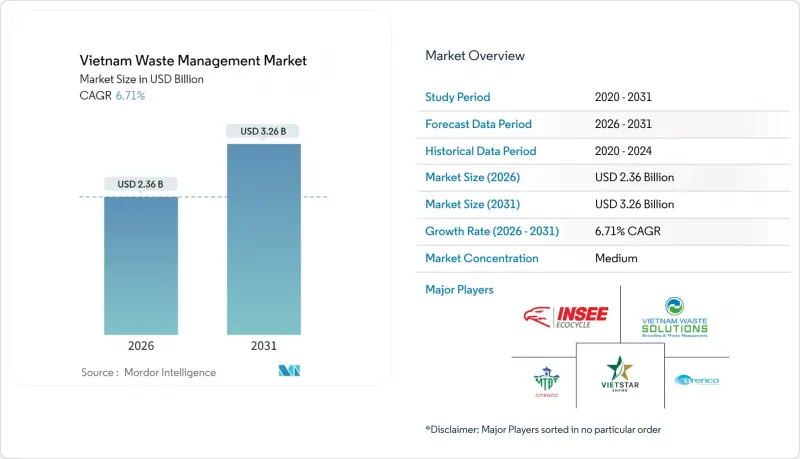

預計到 2026 年,越南廢棄物管理市場規模將達到 23.6 億美元。

這代表著從 2025 年的 22.1 億美元成長到 2031 年的 32.6 億美元,2026 年至 2031 年的複合年成長率為 6.71%。

加速的都市化、日益嚴格的環境法規以及國家循環經濟藍圖持續改變市場需求。同時,生產者延伸責任制(EPR)正引導製造商走向正規的回收管道。公共衛生宣傳活動和數位化路線最佳化工具正在提高胡志明市和河內的垃圾分類率,從而為高階處理創造了新的能力。不斷成長的外國直接投資正將廢棄物、聚酯回收和高純度堆肥技術引入當地市場。然而,計劃開發商必須應對諸多挑戰,例如土地徵用障礙、遍遠地區收集網路不足以及地方政府預算限制等,所有這些都會延緩基礎設施建設。

越南廢棄物管理市場趨勢及展望

國家循環經濟藍圖:目標是2030年達到85%的廢棄物收集率

根據越南2030年循環經濟行動計劃,越南的目標是實現都市區95%的廢棄物收集率和農村地區80%的垃圾收集率,並將掩埋率降低至50%以下。該策略將生質能和城市固體廢物與可再生能源目標相結合,為廢棄物發電企業提供政府認可的收入來源。農業部門每年產生9,361萬噸廢棄物,但只有52%被回收。現行法規要求到2025年有機肥料產量增加25%,到2030年所有註冊肥料中有機肥料的比例達到30%。這些目標將農村收入成長與排放目標相結合,為生物炭和堆肥計畫開放了農業用地市場。隨著收集目標的提高,越南的廢棄物管理市場對原料數量的了解日益清晰,區域加工中心的資金籌措。

加強和執行環境法規

越南現行的法律體制以第05/2025/ND-CP號法令、第611/QD-TTg號決定和第11/2025/QD-TTg號決定為核心,這三項法令均引入了更嚴格的生產者責任延伸(EPR)義務、區域處理區目標以及污染者回收規則。新體系提高了收入豁免門檻,正式認可了24家經認證的回收企業,並要求所有廢棄物事故受害者承擔全部修復費用。這些規則將加速市場整合,因為小規模業者難以獲得合規資金籌措,而大型綜合業者則可以利用規模經濟優勢。可預測的執法力度也降低了監管風險,並有助於大型處理設施獲得長期資金籌措。最終,這將創造一個更清晰、更合格投資的環境,從而支持越南廢棄物管理市場的中期擴張。

掩埋容量限制和土地徵用障礙

位於得農省的達拉普垃圾掩埋場等運作掩埋已超出設計容量,而道尼艾掩埋等替代計劃則因土地徵用問題而停滯不前,預計竣工時間將推遲至2025年底。胡志明市目前已有四座垃圾處理廠,佔地1,670公頃,但由於缺乏先前協議規定的緩衝區,擴建受到限制。垃圾焚化發電發電廠需要更大的場地和特殊的規劃用途,這進一步增加了核准流程的複雜性,延長了工期。城市周邊地區的土地稀缺性推高了土地成本,迫使營運商轉向高密度和垂直化技術,而這些技術需要更大的初始投資和更先進的技術能力。

細分市場分析

到2025年,住宅廢棄物將佔越南廢棄物管理市場佔有率的55.12%,這主要得益於城市人口的快速成長,導致廢棄物沿著可預測的高密度路線產生。這使得市政營運商能夠最佳化垃圾收集時間並統一垃圾桶規格,從而降低每個家庭的成本,並騰出資金用於升級處理設施。雖然越南的商業廢棄物管理市場目前規模小規模,但預計到2031年將以7.92%的複合年成長率成長,這主要得益於二線城市購物中心、物流樞紐和住宿設施的興起。商業客戶也開始接受利潤豐厚的廢棄物加值服務套餐,例如週末收集和安全碎紙服務。

工業廢棄物、醫療和廢棄物廢棄物剩餘佔有率,各領域均發展出專門的收入來源。危險廢棄物處理公司因溶劑和污泥處理而獲得認證溢價,北江省的醫院必須遵守第33/2025/QD-UBND號決定規定的嚴格廢棄物分類規則。橡膠生產商已開始將污水污泥轉化為有機肥料,展現了農業領域增值回收的潛力。儘管在政策壓力不斷增加的情況下,這些細分領域將會擴張,但住宅廢棄物仍將是越南整體廢棄物管理市場中車輛運轉率的基礎。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加強環境法規和更嚴格的執法

- 提高公眾健康意識及開展城市清潔宣傳活動

- 國家循環經濟藍圖的目標是到2030年達到85%的廢棄物回收率。

- 外國主導的廢棄物發電計劃技術轉讓

- 將生產者延伸責任制(EPR)擴展到包裝和電子產品領域

- 市場限制

- 掩埋容量限制和土地徵用障礙

- 地方廢棄物基礎建設發展面臨的資金限制

- 地方政府收款系統的碎片化

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值,單位:十億美元)

- 按來源

- 住宅

- 商業設施(零售商店、辦公室等)

- 產業

- 醫療(健康和醫藥)

- 建築和拆除廢棄物

- 其他(公共設施、農業廢棄物等)

- 按服務類型

- 收集、運輸、分類和分離

- 處理/處置

- 掩埋場

- 回收和資源回收

- 焚燒和廢棄物發電

- 其他(化學處理、堆肥等)

- 其他(諮詢、審核、訓練等)

- 依廢物類型

- 都市固態廢棄物

- 工業用危險廢棄物

- 電子廢棄物

- 塑膠廢棄物

- 醫療廢棄物

- 建築和廢棄物廢棄物

- 農業廢棄物

- 其他特殊廢棄物(放射性廢棄物等)

- 按地區

- 胡志明市

- 河內

- 峴港

- 其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CITENCO

- URENCO(Urban Environment Company Hanoi)

- INSEE Ecocycle

- Vietnam Waste Solutions

- Vietstar Environment

- Tetra Tech Coffey Vietnam

- Thuan Thanh Environment JSC

- Sonadezi Services JSC

- DUYTAN Plastic Recycling

- Green Environment Production Services Trade Co. Ltd

- Vietnam Australia Environment JSC

- SGS Vietnam

- Tan Phat Tai Co. Ltd

- An Phat Holdings(AnEco)

- Ha Noi Urban Environment Co. Ltd

- Bac Ninh Clean & Environment JSC

- TKV Waste Treatment Centre

- Holcim Vietnam Geocycle

- Indovin Power(Waste-to-Energy)

- Green Growth Asia Corp.

第7章 市場機會與未來展望

Vietnam Waste Management Market size in 2026 is estimated at USD 2.36 billion, growing from 2025 value of USD 2.21 billion with 2031 projections showing USD 3.26 billion, growing at 6.71% CAGR over 2026-2031.

Accelerating urbanization, tighter environmental laws, and a national circular-economy roadmap continue to reshape demand, while extended-producer-responsibility (EPR) rules nudge manufacturers toward formal recycling channels. Public-health campaigns and digital route-optimization tools are raising source-separation rates in Ho Chi Minh City and Hanoi, creating new volumes for advanced treatment. Rising foreign direct investment is bringing waste-to-energy, polyester-to-polyester recycling, and high-purity composting technologies to provincial markets. At the same time, project developers must work around land-acquisition hurdles, rural collection gaps, and constrained provincial budgets, all of which slow down infrastructure roll-outs.

Vietnam Waste Management Market Trends and Insights

National Circular-Economy Roadmap Targeting 85% Waste Collection by 2030

Under the 2030 circular-economy action plan, Vietnam aims for 95% urban and 80% rural waste collection, while cutting landfill use below 50%. The strategy also links biomass and municipal waste to renewable-energy targets, giving waste-to-energy developers a government-endorsed revenue story. Agriculture generates 93.61 million tons of waste annually, yet just 52% is reused; regulations now call for a 25% jump in organic-fertilizer output by 2025 and a 30% organic share of all registered fertilizers by 2030. These targets integrate rural income growth with emissions goals, opening farmland markets for biochar and compost initiatives. As collection targets rise, the Vietnam waste management market gains visibility on feedstock volumes, improving bankability for regional treatment hubs.

Tightening Environmental Legislation & Enforcement

Vietnam's legal framework now revolves around Decree 05/2025/ND-CP, Decision 611/QD-TTg, and Decision 11/2025/QD-TTg, each introducing stricter EPR obligations, regional treatment-zone targets, and polluter-pays recovery rules. The new regime lifts revenue-exemption thresholds, formalizes 24 certified recyclers, and assigns full restoration costs to parties causing waste incidents. These rules accelerate market consolidation because smaller operators struggle to finance compliance upgrades, while integrated players monetize economies of scale. Predictable enforcement also reduces regulatory risk, unlocking long-tenor funding for large treatment plants. The net effect is a clearer, more investable backdrop that underpins the Vietnam waste management market's medium-term expansion.

Limited Landfill Capacity & Land-Acquisition Hurdles

Sites such as Dak R'lap in Dak Nong are operating beyond design limits because replacement projects like Dao Nghia remain stalled over land clearance, pushing completion to late 2025. In Ho Chi Minh City, four treatment complexes already span 1,670 ha, yet buffers mandated in earlier agreements are missing, constraining expansion. Waste-to-energy developers need larger footprints and special zoning, adding another layer of approvals that extends timelines. Scarcity of peri-urban land raises acquisition costs, forcing operators to pivot toward high-density or vertical technologies that demand larger upfront capital and more technical skill.

Other drivers and restraints analyzed in the detailed report include:

- Foreign-Investor-Led Technology Transfer in Waste-to-Energy Projects

- Rising Public-Health Awareness & Urban Cleanliness Campaigns

- Capital Constraints for Provincial Waste-Infrastructure Upgrades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential streams held 55.12% of the Vietnam waste management market share in 2025, underpinned by an expanding urban population that generated predictable, route-dense tonnage. As a result, municipal operators have optimized pick-up times and standardized bins, bringing down per-household costs and freeing capital for treatment upgrades. The Vietnam waste management market size for commercial waste is much smaller today, yet it is forecast to rise at an 7.92% CAGR through 2031 as shopping centers, logistics hubs, and hospitality venues multiply across Tier-2 cities. Commercial clients also accept premium service packages, such as weekend pick-up and secure shredding, that carry higher margins.

Industrial, medical, and construction waste together account for the remaining share, yet each niche opens specialized revenue streams. Hazardous-waste contractors earn certification premiums to handle solvents and sludge, while hospitals in Bac Giang must conform to Decision 33/2025/QD-UBND's strict segregation rules. Rubber producers have begun converting wastewater sludge into organic fertilizer, signaling agricultural up-cycling potential. With policy pressure mounting, these sub-segments will scale, but residential tonnage will continue to anchor fleet utilization across the Vietnam waste management market.

The Vietnam Waste Management Market Report is Segmented by Source (Residential, Commercial, Industrial, and More), by Service Type (Collection/Transportation/Sorting, and More), by Waste Type (Municipal Solid Waste, Industrial Hazardous Waste, E-Waste, Plastic Waste, Biomedical Waste, and More), and by Geography (Ho Chi Minh City, Hanoi, Da Nang, Rest of Vietnam). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- CITENCO

- URENCO (Urban Environment Company Hanoi)

- INSEE Ecocycle

- Vietnam Waste Solutions

- Vietstar Environment

- Tetra Tech Coffey Vietnam

- Thuan Thanh Environment JSC

- Sonadezi Services JSC

- DUYTAN Plastic Recycling

- Green Environment Production Services Trade Co. Ltd

- Vietnam Australia Environment JSC

- SGS Vietnam

- Tan Phat Tai Co. Ltd

- An Phat Holdings (AnEco)

- Ha Noi Urban Environment Co. Ltd

- Bac Ninh Clean & Environment JSC

- TKV Waste Treatment Centre

- Holcim Vietnam Geocycle

- Indovin Power (Waste-to-Energy)

- Green Growth Asia Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening environmental legislation & enforcement

- 4.2.2 Rising public health awareness & urban cleanliness campaigns

- 4.2.3 National circular-economy roadmap targeting 85 % waste collection by 2030

- 4.2.4 Foreign-investor led technology transfer in waste-to-energy projects

- 4.2.5 Extended Producer Responsibility (EPR) expansion to packaging & electronics

- 4.3 Market Restraints

- 4.3.1 Limited landfill capacity & land-acquisition hurdles

- 4.3.2 Capital constraints for provincial waste-infrastructure upgrades

- 4.3.3 Fragmented collection system in rural communes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Geography

- 5.4.1 Ho Chi Minh City

- 5.4.2 Hanoi

- 5.4.3 Da Nang

- 5.4.4 Rest of Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 CITENCO

- 6.4.2 URENCO (Urban Environment Company Hanoi)

- 6.4.3 INSEE Ecocycle

- 6.4.4 Vietnam Waste Solutions

- 6.4.5 Vietstar Environment

- 6.4.6 Tetra Tech Coffey Vietnam

- 6.4.7 Thuan Thanh Environment JSC

- 6.4.8 Sonadezi Services JSC

- 6.4.9 DUYTAN Plastic Recycling

- 6.4.10 Green Environment Production Services Trade Co. Ltd

- 6.4.11 Vietnam Australia Environment JSC

- 6.4.12 SGS Vietnam

- 6.4.13 Tan Phat Tai Co. Ltd

- 6.4.14 An Phat Holdings (AnEco)

- 6.4.15 Ha Noi Urban Environment Co. Ltd

- 6.4.16 Bac Ninh Clean & Environment JSC

- 6.4.17 TKV Waste Treatment Centre

- 6.4.18 Holcim Vietnam Geocycle

- 6.4.19 Indovin Power (Waste-to-Energy)

- 6.4.20 Green Growth Asia Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球多氟烷基物質(PFAS)廢棄物管理市場報告2026年全球廢棄物管理與回收服務市場報告2026年全球紡織廢棄物管理市場報告2026年全球廢棄物管理軟體市場報告2026年全球放射性廢棄物管理系統市場報告2026年全球水務和廢棄物管理諮詢服務市場報告

2026年全球多氟烷基物質(PFAS)廢棄物管理市場報告2026年全球廢棄物管理與回收服務市場報告2026年全球紡織廢棄物管理市場報告2026年全球廢棄物管理軟體市場報告2026年全球放射性廢棄物管理系統市場報告2026年全球水務和廢棄物管理諮詢服務市場報告 全球廢棄物管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球廢棄物管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 廢棄物管理市場分析及預測(至2035年):按類型、產品、服務、技術、應用、材料類型、製程及最終用戶分類

廢棄物管理市場分析及預測(至2035年):按類型、產品、服務、技術、應用、材料類型、製程及最終用戶分類 南美洲廢棄物管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)新加坡廢棄物管理市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

南美洲廢棄物管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)新加坡廢棄物管理市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)