|

市場調查報告書

商品編碼

1939724

美國冷藏運輸:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Refrigerated Trucking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

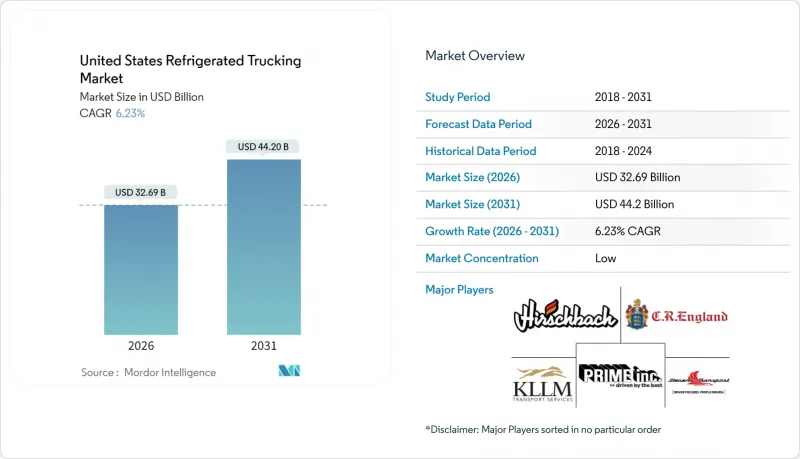

預計到 2026 年,美國冷藏卡車運輸市場規模將達到 326.9 億美元,較 2025 年的 307.7 億美元持續成長。

預計到 2031 年將達到 442 億美元,2026 年至 2031 年的複合年成長率為 6.23%。

這一成長是由多種因素共同推動的:消費者對全年生鮮食品的持續需求、超低溫藥品配送的擴張以及食品訂購的增加導致配送時間縮短。為了回應零排放法規,營運商正在升級車隊,採用電動運輸冷凍設備;基於人工智慧的配送路線最佳化平台則減少了空駛和食物浪費成本。雖然大型承運商之間的整合使得昂貴的技術投資得以規模化,但分散的區域專家網路對於確保最後一公里配送仍然至關重要。對現代化冷藏保管設施的同步投資是網路最佳化的基礎,尤其是在德克薩斯州、墨西哥灣沿岸和中西部農業帶等農業綜合企業走廊地區。

美國冷藏運輸市場趨勢與分析

FSMA實施促進冷藏車升級

《食品安全現代化法案》(FSMA) 第 204 條將於 2026 年 1 月全面生效,要求運輸商提交 FDA 指定食品的 24 小時追蹤記錄。各公司正在為其貨車配備物聯網感測器、基於區塊鏈的文件管理系統和 GPS 溫度探頭,從而將廢品率降低 30%,同時將準時交付率提高 25%。領先先行者已將合規性作為加值服務提供給藥品運輸商,因為藥品運輸商每次溫度超標都可能面臨高達 78,000 美元的召回成本。該法規將使可追溯性從成本中心轉變為競爭優勢,迫使落後的公司進行技術改造,否則將成為資金更雄厚的競爭對手的收購目標。

食品宅配的快速成長擴大了本地冷藏鏈的容量

預計到2025年,美國生鮮電商銷售額將達到1.24兆美元,其中「最後一公里」配送環節約佔物流成本的50%。零售商正投資超過10億美元,在人口密集的大都會區附近建造自動化冷藏中心。採用模組化冷凍面板的靈活溫控系統,使運輸商能夠在同一路線上混合運輸生鮮產品、乳製品和冷凍食品,避免交叉污染。創新的儲物櫃和攜帶式冷藏箱即使在終端消費者錯過送貨時間段的情況下也能保持產品質量,從而減少浪費並增強品牌忠誠度。這種對高頻次、小批量配送日益成長的需求,使得區域性專業公司在美國冷藏運輸市場,尤其是在紐約、洛杉磯和西雅圖地區,變得越發重要。

冷藏車駕駛人短缺導致人事費用上漲。

目前,冷藏運輸職位空缺總合已達24,043個,導致每週商機損失高達9,550萬美元。冷藏運輸需要溫度控制、危險品知識以及嚴格的配送時間表,因此與乾貨車運輸相比,合格的冷藏工人數量更為有限。冷藏倉庫的離職率加劇了員工對等待時間的不滿,進一步惡化了離職率。儘管美國聯邦汽車運輸安全管理局(FMCSA)的豁免條款允許卡車司機僱用沒有商業駕駛執照(CDL)的司機,但安全隱患仍然存在。提高薪資和提供技能提升計畫正逐漸成為美國冷藏運輸市場的強制性要求。

細分市場分析

預計加工食品領域將主導美國冷藏運輸市場,從 2026 年到 2031 年將以 7.02% 的複合年成長率成長。肉類、海鮮和家禽領域將在 2025 年占美國冷藏運輸市場的 21.42%,這表明該領域仍然依賴不間斷的低溫運輸。

如今,食材自煮包供應商和冷凍食品品牌需要SKU層級的溫度數據,這推動了對冷藏室和氣調包裝的投資。運輸公司和食品加工商正在合作建立預冷分揀流程,以減少碼頭入口處的環境溫度流入。醫療和藥品托運商正在利用為生技藥品開發的超低溫檢驗通道,而園藝產品出口商則透過美國農業部資助的回程傳輸運輸改進措施,延長運往中西部配送中心的漿果和綠葉蔬菜的保存期限。拖車內部的先進聚合物襯裡能夠實現乳製品溫度的快速變化,從而在不違反特定產品儲存規定的前提下,實現混合裝載的經濟效益。

2025 年,非貨櫃冷藏卡車憑藉專用硬體和路線柔軟性,在美國冷藏卡車運輸市場佔了 85.45% 的佔有率。隨著港口當局增加充電點,以及航運公司協調鐵路和公路交接以縮短門到門運輸時間,預計 2026 年至 2031 年貨櫃冷藏運輸量將以 6.41% 的複合年成長率成長。

位於休士頓冷港的這座佔地315,101平方英尺的設施以及位於海灣港耗資7300萬美元的擴建項目將創建新的多式聯運轉運點,從而縮短短途運輸距離並降低滯期費風險。嵌入冷藏集裝箱的物聯網感測器陣列將追蹤衝擊、濕度和位置訊息,幫助托運人檢驗海運、鐵路和公路運輸的品質。

預計到2025年,長途貨運將佔總收入的71.60%,並在2026年至2031年間以6.54%的複合年成長率快速成長,這主要得益於農產品、肉類和藥品跨境運輸量的增加。自動駕駛測試已在亞特蘭大和達拉斯之間完成了5萬英里無事故行駛,預示著一旦獲得監管部門批准,將能顯著降低成本。

長途柴油-電力混合動力汽車在嚴酷的沙漠環境中能夠延長車輛使用壽命,而預測性維護平台則會在運輸過程中通知終端壓縮機的磨損情況。雖然短程運輸路線正受益於電氣化,但電池密度限制和公路充電基礎設施的缺乏意味著長途柴油運輸預計到2030年仍將保持可行性,並將繼續支撐美國冷藏卡車運輸市場的大部分佔有率。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 經濟表現和公司概況

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲部門的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 公路貨運量趨勢

- 公路貨運價格趨勢

- 按交通方式分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- FSMA實施促進冷藏車升級

- 食品雜貨宅配的快速成長正在推動對區域低溫運輸產能的需求。

- 對需要超低溫(-20°C 或以下)運輸的特殊藥品的需求不斷成長

- 電氣化桁架受惠於州級零排放激勵計劃

- 利用人工智慧進行動態路線規劃有助於防止食物變質並最大限度地減少空駛里程。

- 農業出口走廊津貼(例如,墨西哥灣沿岸地區農產品補貼)旨在提高回程傳輸利用率

- 市場限制

- 合格冷凍車駕駛員短缺,給人事費用帶來了越來越大的壓力。

- 由於TRU排放法規日益嚴格,資本成本增加。

- 鋰離子電池防火安全標準的不確定性正在減緩電動儲能裝置的普及。

- 針對低溫運輸資訊處理系統的網路安全漏洞導致營運中斷

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 目的

- 園藝產品

- 乳製品

- 肉類、魚貝類和家禽

- 加工食品

- 醫療和藥品

- 其他用途

- 卡車裝載規範

- 整車運輸 (FTL)

- 小批量貨物(零擔)

- 貨櫃運輸

- 貨櫃運輸

- 非貨櫃運輸

- 距離

- 長途

- 短程交通

- 貨物類型

- 液體貨物

- 固態貨物

- 目的地

- 國內的

- 國際的

- 溫度類型

- 冷藏

- 冷凍

- 環境的

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- ATS(Anderson Trucking Service)

- Bay and Bay Transportation

- CR England

- Covenant Logistics Group, Inc.(Including Southern Refrigerated Transport)

- Decker Truck Line, Inc.

- FFE(Frozen Food Express)Transportation Services, Inc.(Owned by Duff Capital Investors)

- Freymiller, Inc.

- Hirschbach Motor Lines, Inc.

- J&R Schugel Trucking

- K&B Transportation

- KLLM Transport Services(Owned by Duff Capital Investors)

- Knight-Swift Transportation Holdings, Inc.(Including Swift Transportation Company)

- Leonards Express

- Marten Transport, Ltd.

- Penske Corporation, Inc.(Including Black Horse Carriers, Inc.)

- Prime, Inc.

- Roehl Transport, Inc.

- Ryder System, Inc.(Including Cardinal Logistics)

- Stevens Transport, Inc.

- TransAm Trucking, Inc.

- WEL Companies

第7章 市場機會與未來展望

The United States refrigerated trucking market size in 2026 is estimated at USD 32.69 billion, growing from 2025 value of USD 30.77 billion with 2031 projections showing USD 44.2 billion, growing at 6.23% CAGR over 2026-2031.

Growth stems from several converging forces: sustained consumer demand for year-round fresh food, expanding ultra-cold pharmaceutical distribution, and rising e-commerce grocery orders that shorten delivery windows. Operators are upgrading fleets with electric transport-refrigeration units to comply with zero-emission mandates, while artificial-intelligence routing platforms lower empty-mile ratios and spoilage costs. Consolidation among top carriers provides scale for expensive technology investments, yet a fragmented tail of regional specialists remains crucial for last-mile coverage. Parallel investment in modern cold-storage nodes underpins network optimization, especially in Texas, the Gulf Coast, and Midwest agribusiness corridors.

United States Refrigerated Trucking Market Trends and Insights

FSMA Enforcement Spurring Upgrades in Refrigerated Fleets

Section 204 of the Food Safety Modernization Act takes full effect in January 2026 and obliges carriers to furnish 24-hour traceability records for foods on the FDA's list. Fleets are outfitting vans with IoT sensors, blockchain-enabled documentation, and GPS temperature probes, cutting spoilage by 30% while lifting on-time performance by 25%. Early adopters market compliance as a premium service for pharma shippers, who face recall costs of USD 78,000 per incident when excursions occur. The regulation thereby transforms traceability from a cost center into a competitive differentiator, pushing laggards toward tech-enabled retrofits or acquisition by better-capitalized rivals.

Rapid Growth in Home-Delivered Groceries Increasing Regional Cold-Chain Capacity

E-commerce grocery receipts are set to total USD 1.24 trillion in 2025, with last-mile activity representing roughly 50% of logistics spend. Retailers are allocating more than USD 1 billion to automated cold-storage hubs positioned closer to dense urban clusters. Modular refrigeration panels enable flexible temperature zoning, letting carriers combine produce, dairy, and frozen SKUs on the same route without cross-contamination. Innovative lockers and portable cooling totes preserve integrity when end-consumers miss delivery windows, shrinking spoilage write-offs and reinforcing brand loyalty. Demand for high-frequency, low-volume drops thereby elevates regional specialists in the United States refrigerated trucking market, particularly around New York, Los Angeles, and Seattle.

Shortage of Reefer-Qualified Drivers is Putting Upward Pressure on Labor Costs

Vacancies total 24,043 seats, costing USD 95.5 million weekly in forgone revenue. Reefer duties demand temperature checks, hazmat familiarity, and tighter appointment windows, narrowing the qualified labor pool relative to dry-van work. Cold-warehouse turnover elevates wait-time frustrations, worsening attrition. Although FMCSA exemptions let carriers seat commercial-learner-permit holders without CDL escorts, safety concerns remain. Enhanced compensation and upskilling programs are becoming table stakes across the United States refrigerated trucking market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Specialty Pharmaceuticals Requiring Ultra-Cold Transport Lanes

- AI-Powered Dynamic Routing Helps Reduce Spoilage and Minimize Empty Miles

- Stricter TRU Emissions Regulations are Increasing Capital Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Processed Food Products are expected to expand at a 7.02% CAGR (2026-2031), outstripping all other verticals in the United States refrigerated trucking market. Meats, Fish, and Poultry maintained a 21.42% United States refrigerated trucking market share in 2025, signifying continued reliance on uninterrupted cold-chain links.

Meal-kit providers and frozen entree brands now demand SKU-level temperature data, spurring investments in reefer compartmentalization and controlled-atmosphere packaging. Carrier collaboration with food processors yields pre-cool staging protocols that cut ambient ingress at dock doors. Healthcare and pharmaceutical shippers leverage ultra-cold validation lanes created for biologics, while horticultural exporters benefit from USDA-funded backhaul upgrades, extending shelf life for berries and leafy greens en route to Midwest distribution hubs. Advanced polymer linings inside trailers allow rapid temperature swings for dairy products, enabling mixed-load economics without violating product-specific storage rules.

Non-containerized reefers kept an 85.45% United States refrigerated trucking market share in 2025, owing to specialized hardware and lane flexibility. Containerized refrigerated flows are expected to grow at a 6.41% CAGR (2026-2031) as port authorities expand plug-in points, and carriers sync rail and truck hand-offs to shrink door-to-door transit times.

Houston ColdPort's 315,101 ft2 facility and Port Gulfport's USD 73 million expansion create new intermodal staging nodes that shorten drayage distance and slash demurrage risk. IoT-sensor arrays embedded in reefer containers track shock, humidity, and location, helping shippers validate integrity across marine-rail-road segments.

Long haul freight claims 71.60% of the revenue share in 2025 and is expected to grow the fastest at 6.54% CAGR (2026-2031) as cross-country produce, meat, and pharma volumes escalate. Autonomous pilots amassed 50,000 miles without accident on the Atlanta-Dallas lane, foreshadowing cost reductions once regulatory green lights emerge.

Extended-range diesel-electric hybrids prolong asset life in harsh desert corridors, while predictive maintenance platforms alert terminals to compressor wear mid-route. Short-haul lanes enjoy electrification gains, but battery-density constraints and sparse highway charging keep long-haul diesel viable through 2030, underpinning the bulk of the United States refrigerated trucking market.

The United States Refrigerated Trucking Market Report is Segmented by Application (Processed Food Products and More), Truckload Specification (Full-Truck-Load (FTL) and More), Containerization (Containerized and More), Distance (Long Haul and More), Goods Configuration (Fluid Goods and More), Destination (Domestic and International), and Temperature Type (Chilled and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ATS (Anderson Trucking Service)

- Bay and Bay Transportation

- C.R. England

- Covenant Logistics Group, Inc. (Including Southern Refrigerated Transport)

- Decker Truck Line, Inc.

- FFE (Frozen Food Express) Transportation Services, Inc. (Owned by Duff Capital Investors)

- Freymiller, Inc.

- Hirschbach Motor Lines, Inc.

- J&R Schugel Trucking

- K&B Transportation

- KLLM Transport Services (Owned by Duff Capital Investors)

- Knight-Swift Transportation Holdings, Inc. (Including Swift Transportation Company)

- Leonards Express

- Marten Transport, Ltd.

- Penske Corporation, Inc. (Including Black Horse Carriers, Inc.)

- Prime, Inc.

- Roehl Transport, Inc.

- Ryder System, Inc. (Including Cardinal Logistics)

- Stevens Transport, Inc.

- TransAm Trucking, Inc.

- WEL Companies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Economic Performance and Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport and Storage Sector GDP

- 4.7 Logistics Performance

- 4.8 Length of Roads

- 4.9 Export Trends

- 4.10 Import Trends

- 4.11 Fuel Pricing Trends

- 4.12 Trucking Operational Costs

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain and Distribution Channel Analysis

- 4.19 Market Drivers

- 4.19.1 FSMA Enforcement Spurring Upgrades in Refrigerated Fleets

- 4.19.2 Rapid Growth in Home-Delivered Groceries Increasing Demand for Regional Cold Chain Capacity

- 4.19.3 Rising Demand for Specialty Pharmaceuticals Requiring Ultra-Cold (Below -20°C) Transport Lanes

- 4.19.4 Electrified TRUs Benefiting from State-Level Zero-Emission Incentive Programs

- 4.19.5 AI-Powered Dynamic Routing Helping Reduce Spoilage and Minimize Empty Miles

- 4.19.6 Agricultural Export Corridor Grants (e.g., Gulf Coast Produce) Improving Back-Haul Utilization

- 4.20 Market Restraints

- 4.20.1 Shortage of Reefer-Qualified Drivers Putting Upward Pressure on Labor Costs

- 4.20.2 Stricter TRU Emissions Regulations Increasing Capital Costs

- 4.20.3 Uncertainty over Lithium-Ion Battery Fire Codes Slowing Adoption of Electric TRUs

- 4.20.4 Cybersecurity Breaches Targeting Cold Chain Telematics Disrupting Operations

- 4.21 Technology Innovations in the Market

- 4.22 Porter's Five Forces Analysis

- 4.22.1 Threat of New Entrants

- 4.22.2 Bargaining Power of Buyers

- 4.22.3 Bargaining Power of Suppliers

- 4.22.4 Threat of Substitutes

- 4.22.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Application

- 5.1.1 Horticultural Products

- 5.1.2 Dairy Products

- 5.1.3 Meats, Fish, and Poultry

- 5.1.4 Processed Food Products

- 5.1.5 Healthcare and Pharmaceutical

- 5.1.6 Other Applications

- 5.2 Truckload Specification

- 5.2.1 Full-Truck-Load (FTL)

- 5.2.2 Less than-Truck-Load (LTL)

- 5.3 Containerization

- 5.3.1 Containerized

- 5.3.2 Non-Containerized

- 5.4 Distance

- 5.4.1 Long Haul

- 5.4.2 Short Haul

- 5.5 Goods Configuration

- 5.5.1 Fluid Goods

- 5.5.2 Solid Goods

- 5.6 Destination

- 5.6.1 Domestic

- 5.6.2 International

- 5.7 Temperature Type

- 5.7.1 Chilled

- 5.7.2 Frozen

- 5.7.3 Ambient

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ATS (Anderson Trucking Service)

- 6.4.2 Bay and Bay Transportation

- 6.4.3 C.R. England

- 6.4.4 Covenant Logistics Group, Inc. (Including Southern Refrigerated Transport)

- 6.4.5 Decker Truck Line, Inc.

- 6.4.6 FFE (Frozen Food Express) Transportation Services, Inc. (Owned by Duff Capital Investors)

- 6.4.7 Freymiller, Inc.

- 6.4.8 Hirschbach Motor Lines, Inc.

- 6.4.9 J&R Schugel Trucking

- 6.4.10 K&B Transportation

- 6.4.11 KLLM Transport Services (Owned by Duff Capital Investors)

- 6.4.12 Knight-Swift Transportation Holdings, Inc. (Including Swift Transportation Company)

- 6.4.13 Leonards Express

- 6.4.14 Marten Transport, Ltd.

- 6.4.15 Penske Corporation, Inc. (Including Black Horse Carriers, Inc.)

- 6.4.16 Prime, Inc.

- 6.4.17 Roehl Transport, Inc.

- 6.4.18 Ryder System, Inc. (Including Cardinal Logistics)

- 6.4.19 Stevens Transport, Inc.

- 6.4.20 TransAm Trucking, Inc.

- 6.4.21 WEL Companies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

冷藏拖車市場 - 全球預測,2026-2032年冷藏車市場:2026-2032年全球市場預測(依車輛類型、動力來源、溫度、隔熱材料及應用分類)

冷藏拖車市場 - 全球預測,2026-2032年冷藏車市場:2026-2032年全球市場預測(依車輛類型、動力來源、溫度、隔熱材料及應用分類) 冷藏拖車市場:依產品類型、最終用途產業和地區分類-市場規模、佔有率、前景和機會分析,2025-2032年

冷藏拖車市場:依產品類型、最終用途產業和地區分類-市場規模、佔有率、前景和機會分析,2025-2032年 2026年全球冷藏拖車市場報告2026年全球冷藏貨物運輸市場報告

2026年全球冷藏拖車市場報告2026年全球冷藏貨物運輸市場報告 冷藏車市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、有效載荷、應用、地區和競爭格局分類,2021-2031年)

冷藏車市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、有效載荷、應用、地區和競爭格局分類,2021-2031年) 日本冷藏車市場規模、佔有率、趨勢及預測(按類型、噸位、應用及地區分類),2026-2034年

日本冷藏車市場規模、佔有率、趨勢及預測(按類型、噸位、應用及地區分類),2026-2034年 冷藏拖車市場規模、佔有率和成長分析(按拖車類型、軸型、動力來源、最終用途產業和地區分類)-2026-2033年產業預測

冷藏拖車市場規模、佔有率和成長分析(按拖車類型、軸型、動力來源、最終用途產業和地區分類)-2026-2033年產業預測 全球冷藏拖車市場冷藏拖車市場-全球產業規模、佔有率、趨勢、機會和預測(按溫度、應用、最終用途、地區和競爭細分,2020-2030 年)

全球冷藏拖車市場冷藏拖車市場-全球產業規模、佔有率、趨勢、機會和預測(按溫度、應用、最終用途、地區和競爭細分,2020-2030 年)