|

市場調查報告書

商品編碼

1939708

美國汽車服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Automotive Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

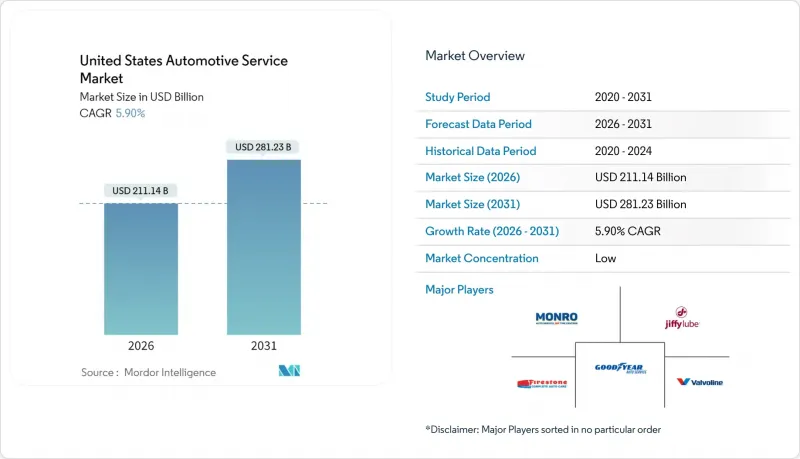

美國汽車服務市場預計到 2026 年價值將達到 2,111.4 億美元,高於 2025 年的 1993.8 億美元,預計到 2031 年將達到 2,812.3 億美元。

預計2026年至2031年年複合成長率(CAGR)為5.9%。

強勁的需求主要源自於美國車輛老化(平均車齡12.6年)、里程回收以及輕型商用車利用率的提高,這些因素共同推動了對汽車服務的需求。加速電氣化進程增加了維修的複雜性和單位成本,降低了定期保養的頻率,同時也促使服務提供者提昇技師技能並投資高壓工具。數位化預約平台、訂閱式保養套餐以及「維修權」立法的推出正在重塑競爭格局,而行動按需服務也越來越受到都市區消費者的青睞。這些因素共同推動了美國汽車服務市場的持續收入成長和營運轉型。

美國汽車服務市場趨勢與洞察

車齡超過12.6年

到2024年,車輛平均車齡將達到12.6年,這將帶來結構性利好,其中6-14年車齡的車輛將成為服務市場的主要用戶群。新車價格上漲至4.5萬美元以上,加上庫存短缺,導致車輛使用週期延長,更多車主選擇進行必要的保養而非更換。預計2021年至2024年間,混合動力汽車的註冊量將成長181%,為未來的電池更換收入奠定基礎。在2021年的經濟復甦期間,獨立維修店獲得了約45%的新增服務支出,顯示該細分市場的吸引力。高利率強化了消費者對車輛耐用性的關注,即使在經濟放緩時期,也能支撐穩定的零件更換需求。

新冠疫情里程恢復

根據美國聯邦公路管理局的數據,2024年2月全美公路行駛里程達到2,748億英里,年增1.4%,已完全恢復到疫情前水準。預計到2050年,長途貨車行駛里程將以每年1.1%的速度成長,而單體貨車運作預計將以每年1.9%的速度成長,這將進一步增加對商用車輛車隊維修的需求。行駛里程的增加加速了老舊車輛的磨損,從而推高了對煞車、輪胎和油液服務的需求。隨著疫情後駕駛需求的激增,每周行駛里程趨勢已成為衡量維修車間運作的關鍵指標。每加侖2.85美元的相對穩定的汽油價格支撐了人們的出行,而不斷成長的消費者信貸餘額也持續將新車購買預算轉向售後服務。

電動車的普及將減少定期維護的頻率。

電動車所需的機械油和皮帶更少,從而減少了定期檢查的頻率。然而,由於電池和電子系統的複雜性,電動車的平均維修成本比內燃機汽車高出約 50%。與動力傳動系統無關的維修工作,例如輪胎和擋風玻璃雨刷,仍將保持強勁勢頭,但到 2035 年,傳統的售後市場可能會萎縮。只有一小部分技術人員接受過完整的電動車培訓,這造成了技能缺口,有利於那些能夠投資高壓安全設備的大型連鎖店和經銷商集團。雖然到 2024 年,具備電動車維修能力的獨立維修店將佔據相當大的市場佔有率,但其中超過一半的維修店缺乏宣傳自身專業技術的行銷。

細分市場分析

到2025年,乘用車將占美國汽車服務市場的68.74%,該細分市場車輛數量龐大,需要持續維護。隨著車輛平均車齡超過12年以及混合動力汽車日益普及,美國乘用車相關的汽車服務市場規模預計將穩定成長。受電子商務和最後一公里配送需求的推動,輕型商用車預計將以8.55%的複合年成長率成長至2031年,這將迫使維修店重新評估其產能規劃和零件庫存策略。

車隊營運商現在會簽訂預防性維護契約,以最大限度地減少停機時間,並便於預測煞車、輪胎和懸吊零件的訂購。特斯拉計劃在2024年開設70家新的服務中心,其中許多面積超過10萬平方公尺,以滿足乘用車和商用車領域日益成長的電動車需求。中型和重型卡車雖然銷量較小,但由於嚴格的運轉率要求和聯邦安全法規推動了對專業服務的需求,因此仍然是一個盈利的細分市場。

機械維修和保養仍將是美國汽車服務市場的核心,到 2025 年將維持 42.67% 的收入佔有率。在 ADAS(高級駕駛輔助系統)日益普及的推動下,電氣和電子相關工作預計到 2031 年將以 9.02% 的複合年成長率成長。

為了抓住這部分高利潤業務,汽車修理廠正在投資掃描工具、校準框架和靜態目標。複合材料車身結構使外部和結構維修更加穩定,但也更加複雜。快修連鎖店正在拓展業務範圍,涉足電池、輪胎和輕型維護等領域,以彌補電動車更長的換油週期,並維持客戶到店量。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 平均車齡超過12.6年的老舊車輛數量增加

- 感染疾病後的哩程恢復

- 拓展OEM品牌售後服務計劃

- 數位預訂系統和客戶關係管理平台的興起

- 訂閱維護套餐

- 州級維修權立法進展

- 市場限制

- 由於電動車的普及,常規維護頻率降低

- 工程師嚴重短缺推高了人事費用。

- 因通貨膨脹而推遲非必要維修。

- OEM車用資訊系統讓客戶留在經銷商處

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 買方和消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型卡車

- 按服務類型

- 機器維修保養

- 外觀和結構(車身/油漆/玻璃)

- 電氣和電子設備

- 快速保養(機油、潤滑油、濾清器)

- 透過裝置

- 胎

- 電池

- 座椅和內裝部件

- ADAS感測器和攝影機

- 透過服務管道

- 授權OEM經銷商

- 獨立綜合維修店

- 快速潤滑和輪胎防滑鏈

- 行動/按需服務

- 按美國人口普查區域分類

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Firestone Complete Auto Care

- Jiffy Lube International Inc.

- Meineke Car Care Centers

- Midas International

- Monro Inc.

- Safelite Group

- Walmart Auto Care Centers

- Pep Boys

- Valvoline Instant Oil Change

- Goodyear Auto Service

- NTB-National Tire & Battery

- Christian Brothers Automotive

- Take 5 Oil Change

- Express Oil Change & Tire Engineers

- Caliber Collision

- Gerber Collision & Glass

- Service King Collision

- Tesla Service Centers

- CarMax Auto Care

- AAA Car Care Centers

第7章 市場機會與未來展望

The United States automotive service market size in 2026 is estimated at USD 211.14 billion, growing from 2025 value of USD 199.38 billion with 2031 projections showing USD 281.23 billion, growing at 5.9% CAGR over 2026-2031.

Robust demand comes from an aging national vehicle fleet that averages 12.6 years, a rebound in vehicle miles traveled, and rising light commercial vehicle utilization that intensifies service requirements. Accelerating electrification lifts repair complexity and ticket values, even lowering routine maintenance frequency, prompting providers to invest in technician upskilling and high-voltage tooling. Digital booking platforms, subscription-based maintenance bundles, and right-to-repair legislation are reshaping competitive strategies, while mobile on-demand services gain traction among urban consumers. Collectively, these forces position the US automotive service market for sustained revenue growth and operational transformation

United States Automotive Service Market Trends and Insights

Aging Vehicle Parc Surpassing 12.6 Years

Average vehicle age reached 12.6 years in 2024, creating a structural tailwind as units between six and fourteen years now form the largest service cohort. High new-vehicle prices above USD 45,000 and constrained inventories have extended ownership cycles, pushing more owners toward essential maintenance rather than replacement. Hybrid registrations swelled 181% from 2021 to 2024, setting the stage for future battery replacement revenue. Independent repair specialists captured nearly 45% of incremental service spend during the 2021 rebound, evidencing the segment's appeal. High interest rates reinforce consumer emphasis on longevity, anchoring steady parts replacement demand even during economic slowdowns.

Post-COVID Rebound in Vehicle Miles Traveled

Federal Highway Administration data show national VMT climbing 1.4% year-over-year to 274.8 billion miles in February 2024, fully matching pre-pandemic baselines. Long-haul truck mileage is projected to expand 1.1% annually through 2050, while single-unit truck activity may grow 1.9% per year, reinforcing commercial fleet maintenance needs. Higher miles intensify wear across an aging vehicle mix, boosting brake, tire, and fluid service demand. As post-pandemic driving surges, weekly mileage trends emerge as a key indicator for workshop activity. Relatively stable gasoline at USD 2.85 per gallon supports sustained travel, and rising consumer credit balances continue to divert budgets from new-car purchases toward aftermarket services.

EV Adoption Lowers Routine Service Intensity

Electric vehicles require fewer mechanical fluids and belts, trimming routine visits, yet each repair averages almost 50% higher than on an internal-combustion model, mainly due to battery and electronic complexity. Powertrain-agnostic work, such as tires and wiper blades, remains resilient, but the conventional aftermarket could contract by 2035. Only some of technicians report substantial EV training, generating a skills gap that favors large chains and dealer groups capable of funding high-voltage safety infrastructure. Independent shops servicing BEVs claimed a significant share in 2024, yet over half lack dedicated marketing to showcase that capability.

Other drivers and restraints analyzed in the detailed report include:

- OEM-Branded After-Sales Program Expansion

- Digital Booking and CRM Platforms Proliferation

- OEM Telematics Locking Customers into Dealerships

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars accounted for 68.74% of the US automotive service market in 2025 as the segment's large installed base demanded consistent maintenance. The US automotive service market size linked to passenger cars is projected to grow steadily as the average age surpasses 12 years and hybrid penetration deepens. Light commercial vehicles, buoyed by e-commerce and last-mile delivery, are set to record the fastest 8.55% CAGR through 2031, reshaping shop capacity planning and parts inventory strategies.

Fleet operators now specify preventative maintenance contracts that minimize downtime, driving predictable parts ordering for brakes, tires, and suspension. Tesla opened seventy new service centers in 2024, many exceeding 100,000 square feet, to cater to rising EV volume across both passenger and commercial segments. Medium and heavy trucks, though smaller in count, remain lucrative due to stringent uptime requirements and federal safety regulations that drive specialized service demand.

Mechanical repair and maintenance retained a 42.67% revenue share in 2025, anchoring the US automotive service market. Electrical and electronics work is forecast to grow at a 9.02% CAGR as ADAS penetration rises by 2031.

Shops invest in scan tools, calibration frames, and static targets to capture this margin-rich business. Due to mixed-material body structures, exterior and structural repairs remain stable yet more complex. Quick-lube chains diversify into battery, tire, and light mechanical jobs to offset longer EV oil-change intervals, preserving customer frequency.

The United States Automotive Services Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Service Type (Mechanical Repair and Maintenance, and More), Equipment Type (Tires, Batteries, and More), Service Channel (OEM Dealerships, Independent General Repair Shops, and More), and by U. S. Census Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Firestone Complete Auto Care

- Jiffy Lube International Inc.

- Meineke Car Care Centers

- Midas International

- Monro Inc.

- Safelite Group

- Walmart Auto Care Centers

- Pep Boys

- Valvoline Instant Oil Change

- Goodyear Auto Service

- NTB - National Tire & Battery

- Christian Brothers Automotive

- Take 5 Oil Change

- Express Oil Change & Tire Engineers

- Caliber Collision

- Gerber Collision & Glass

- Service King Collision

- Tesla Service Centers

- CarMax Auto Care

- AAA Car Care Centers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Vehicle Parc Surpassing 12.6 Years

- 4.2.2 Post-COVID Rebound in Vehicle Miles Travelled

- 4.2.3 OEM-Branded After-Sales Program Expansion

- 4.2.4 Digital Booking and CRM Platforms Proliferation

- 4.2.5 Subscription-Based Maintenance Bundles

- 4.2.6 State-Level Right-To-Repair Legislation Momentum

- 4.3 Market Restraints

- 4.3.1 EV Adoption Lowers Routine Service Intensity

- 4.3.2 Acute Technician Shortage Inflates Labor Costs

- 4.3.3 Inflation-Driven Deferral of Discretionary Repairs

- 4.3.4 OEM Telematics Locking Customers into Dealerships

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium & Heavy Trucks

- 5.2 By Service Type

- 5.2.1 Mechanical Repair & Maintenance

- 5.2.2 Exterior & Structural (Body / Paint / Glass)

- 5.2.3 Electrical & Electronics

- 5.2.4 Quick Services (Oil, Fluids, Filters)

- 5.3 By Equipment Type

- 5.3.1 Tires

- 5.3.2 Batteries

- 5.3.3 Seats & Interiors

- 5.3.4 ADAS Sensors & Cameras

- 5.4 By Service Channel

- 5.4.1 OEM Dealerships

- 5.4.2 Independent General Repair Shops

- 5.4.3 Quick-Lube & Tire Chains

- 5.4.4 Mobile / On-Demand Services

- 5.5 By U.S. Census Region

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Firestone Complete Auto Care

- 6.4.2 Jiffy Lube International Inc.

- 6.4.3 Meineke Car Care Centers

- 6.4.4 Midas International

- 6.4.5 Monro Inc.

- 6.4.6 Safelite Group

- 6.4.7 Walmart Auto Care Centers

- 6.4.8 Pep Boys

- 6.4.9 Valvoline Instant Oil Change

- 6.4.10 Goodyear Auto Service

- 6.4.11 NTB - National Tire & Battery

- 6.4.12 Christian Brothers Automotive

- 6.4.13 Take 5 Oil Change

- 6.4.14 Express Oil Change & Tire Engineers

- 6.4.15 Caliber Collision

- 6.4.16 Gerber Collision & Glass

- 6.4.17 Service King Collision

- 6.4.18 Tesla Service Centers

- 6.4.19 CarMax Auto Care

- 6.4.20 AAA Car Care Centers

7 Market Opportunities & Future Outlook

2026年全球共乘市場報告

2026年全球共乘市場報告 汽車即服務市場:2026-2032年全球市場預測(依服務模式、車輛類型、燃料類型及客戶類型分類)汽車服務市場:2026-2032年全球市場預測(依服務類型、客戶群、價格範圍、車輛類型和銷售管道)2026年全球認證汽車服務中心市場報告全球捲簾鋼製服務門市場按操作方式、材料、門類型、應用、最終用途和配銷通路分類的預測(2026-2032年)

汽車即服務市場:2026-2032年全球市場預測(依服務模式、車輛類型、燃料類型及客戶類型分類)汽車服務市場:2026-2032年全球市場預測(依服務類型、客戶群、價格範圍、車輛類型和銷售管道)2026年全球認證汽車服務中心市場報告全球捲簾鋼製服務門市場按操作方式、材料、門類型、應用、最終用途和配銷通路分類的預測(2026-2032年) 2026 年至 2035 年授權汽車服務中心的市場機會、成長要素、產業趨勢分析與預測。按車輛類型、解決方案組件和部署模式分類的端到端汽車DMS平台市場,全球預測(2026-2032年)

2026 年至 2035 年授權汽車服務中心的市場機會、成長要素、產業趨勢分析與預測。按車輛類型、解決方案組件和部署模式分類的端到端汽車DMS平台市場,全球預測(2026-2032年) 車輛服務市場(按車輛、服務模式、類型、服務提供者、引擎、國家/地區分類)-全球產業分析、市場規模、市場佔有率及2025-2032年預測

車輛服務市場(按車輛、服務模式、類型、服務提供者、引擎、國家/地區分類)-全球產業分析、市場規模、市場佔有率及2025-2032年預測 全球授權汽車服務中心市場

全球授權汽車服務中心市場 2025-2029年全球汽車服務市場

2025-2029年全球汽車服務市場