|

市場調查報告書

商品編碼

1959637

2026 年至 2035 年授權汽車服務中心的市場機會、成長要素、產業趨勢分析與預測。Authorized Car Service Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

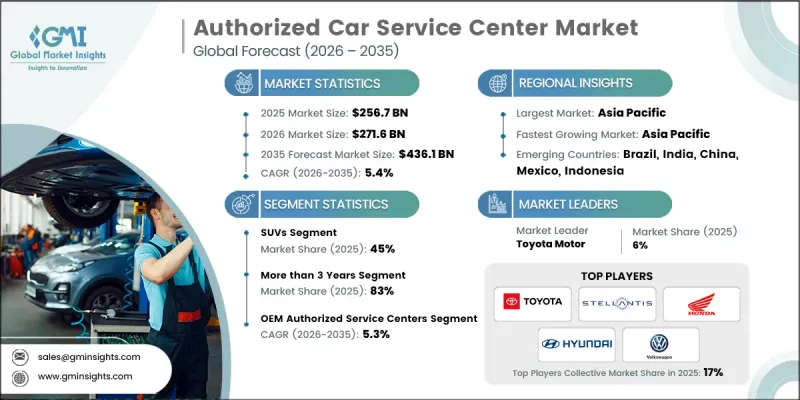

2025 年全球授權汽車服務中心市場價值為 2,567 億美元,預計到 2035 年將達到 4,361 億美元,年複合成長率為 5.4%。

授權服務中心在維護車輛安全、性能和耐用性方面發揮著至關重要的作用,它們提供原廠認證的保養、維修和升級服務。該市場涵蓋經銷商服務中心、多品牌授權研討會和專業維修連鎖機構,所有這些機構都提供有保障的維修、診斷解決方案和原廠配件。隨著車輛保有量的增加和使用週期的延長,車輛的複雜性也隨之增加,從而推動了對專業服務網路的需求。原廠製造商正日益重視授權服務中心,以提高客戶滿意度、維持車輛轉售價值並確保保固合規性。聯網汽車技術和遠端資訊處理技術的整合正在加速預測性維護的發展,並促進更頻繁、更主動的保養服務。數位化正在重塑整個產業,服務中心採用整合技術平台來簡化客戶服務、診斷、配件採購和服務管理,從根本上改變了整個產業的流程和投資策略。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2567億美元 |

| 預測金額 | 4361億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,SUV市佔率將達到45%,並在2035年之前以5.7%的複合年成長率成長。 SUV因其多功能性、高階定位以及能夠提高每次保養收入的複雜系統而備受青睞。維護這些車輛需要特別關注全輪驅動系統、大型煞車系統、複雜的懸吊診斷以及更頻繁的輪胎更換。

預計到2025年,OEM認證服務中心市佔率將達到57%,並在2035年之前以5.3%的複合年成長率成長。這些服務中心在製造商的獨家授權下運營,提供專用診斷工具、保固退款和OEM培訓。憑藉品牌信譽、原廠配件供應以及嚴格遵守製造商指南,它們比獨立服務供應商擁有明顯的競爭優勢。

預計到2025年,中國授權汽車服務中心市場規模將達到414億美元,並在2035年之前以5.9%的複合年成長率持續成長。這一成長主要得益於區域城市汽車保有量的成長、單車維修保養支出的增加以及豪華車對先進維修保養需求的不斷成長。線上預約、行動支付和聯網汽車診斷等數位化服務正逐漸成為業界標準。中國主要汽車製造商正透過授權服務中心、行動服務小組和換電站等方式創新服務模式,以提升服務的便利性和效率。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 車輛老化和車輛擁有周期延長

- 車輛日益複雜和技術整合不斷進步

- 里程數(VMT)增加

- 嚴格的排放氣體法規和安全標準

- 消費者對官方服務的偏好日益成長

- 擴大車輛保固計劃

- 產業潛在風險與挑戰

- 高昂的基礎設施和設備成本

- 熟練技術人員短缺及訓練成本

- 經濟不確定性和通貨膨脹的影響

- 供應鏈中斷和零件供應情況

- 市場機遇

- 電動車服務市場的崛起

- 數位轉型和線上服務預訂

- 訂閱式維護計劃

- 在新興市場拓展業務

- 車隊管理服務

- 二手車維修服務的成長

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國聯邦政府關於車輛安全標準、排放氣體標準和售後服務的法規。

- 加拿大 - 認證維護和電動車服務交付框架

- 歐洲

- 德國及歐盟車輛安全法規及國家服務標準

- 英國—關於脫歐後服務合規性和聯網汽車的指導意見

- 法國-車輛檢驗系統與電動車服務政策

- 義大利——智慧交通系統試點計畫和智慧服務法規

- 亞太地區

- 中國 - 工信部(工業和資訊化部)車輛服務義務和標準

- 印度—新興汽車服務與互聯互通法規

- 日本 - ITS 連線與認證服務政策

- 澳洲—技術中立的智慧交通系統政策

- LATAM

- 墨西哥 - NOM車輛安全標準

- 阿根廷 - 國家交通法 24.449

- 中東和非洲

- 南非共和國 - 道路交通法(1996 年)

- 沙烏地阿拉伯—交通運輸法律與2030願景交通運輸政策

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 數位服務預訂平台

- 人工智慧驅動的診斷系統

- 新興技術

- 預測性維護技術

- 電動車服務技術與基礎設施

- 當前技術趨勢

- 專利分析

- 價格分析

- 服務定價模式

- 人事費用趨勢

- 零件加價分析

- 競爭性定價策略

- 使用案例和成功案例

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 車輛車隊組成與車齡分析

- 全球車輛擁有量統計數據

- 車輛平均年齡趨勢

- 對服務需求的影響

- 單位經濟效益及服務中心盈利基準分析

- 電動車對傳統服務商業模式的影響

- 對標數位化客戶旅程與客戶體驗

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依車輛類型分類,2022-2035年

- 掀背車車

- SUV

- 轎車

第6章 市場估價與預測:依車型年份分類,2022-2035年

- 不到3年

- 3年或以上

第7章 市場估計與預測:依促進因素分類,2022-2035年

- 內燃機(ICE)

- HEV/PHEV

- 電動車(EV)

第8章 市場估算與預測:依服務業分類,2022-2035年

- 引擎

- 動力傳輸

- 煞車

- 暫停

- 電

- 身體

- 胎

- 腰帶和配件

- 其他

第9章 市場估算與預測:依服務供應商,2022-2035年

- OEM授權服務中心

- 多品牌服務中心

- 獨立維修店

第10章 市場估價與預測:依最終用途分類,2022-2035年

- 個人客戶

- 車隊營運商

- 企業客戶

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第12章:公司簡介

- 世界玩家

- 3M

- BMW

- Castrol

- Ford Motor

- General Motors

- Groupe Renault

- Honda Motor

- Hyundai Motor

- Mercedes-Benz

- Mobivia

- Robert Bosch

- Stellantis

- Suzuki Motor

- Toyota Motor

- Volkswagen

- 本地球員

- Automovill Technologies

- Carxpert Garage

- Lansdowne Automobile

- Mahindra First Choice

- Meineke Car Care Centers

- Mobil1 Car Care

- TVS Automobile Solutions

- 新興企業和技術供應商

- GoMechanic

- Wrench

- YourMechanic

The Global Authorized Car Service Center Market was valued at USD 256.7 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 436.1 billion by 2035.

Authorized service centers play a vital role in maintaining vehicle safety, performance, and longevity by offering OEM-certified maintenance, repairs, and upgrades. The market encompasses dealership service centers, multi-brand authorized workshops, and specialized maintenance chains, all providing warranty-backed repairs, diagnostic solutions, and genuine spare parts. As vehicle fleets grow and ownership cycles lengthen, vehicle complexity rises, driving demand for professional service networks. OEMs are increasingly focusing on authorized service centers to improve customer satisfaction, preserve resale value, and ensure warranty compliance. The integration of connected vehicle technologies and telematics has accelerated predictive maintenance, encouraging more frequent and proactive service visits. Digitalization is reshaping the sector, with service centers adopting integrated technology platforms to streamline customer interactions, diagnostics, parts sourcing, and service management, fundamentally transforming operational workflows and investment strategies across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $256.7 Billion |

| Forecast Value | $436.1 Billion |

| CAGR | 5.4% |

The SUV segment held a 45% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. SUVs are favored due to their versatility, premium positioning, and complex systems, which increase per-service revenue. Maintenance for these vehicles involves specialized attention to all-wheel-drive systems, larger brakes, complex suspension diagnostics, and more frequent tire replacements.

The OEM-authorized service centers segment held 57% share in 2025, with a 5.3% CAGR forecast through 2035. These centers operate under exclusive manufacturer authorization, offering proprietary diagnostics, warranty reimbursement, and OEM training. Their brand trust, access to genuine parts, and adherence to manufacturer guidelines give them a clear competitive advantage over independent service providers.

China Authorized Car Service Center Market reached USD 41.4 billion in 2025 and will grow at a CAGR of 5.9% through 2035. Growth is fueled by rising vehicle ownership in lower-tier cities, increasing service expenditure per vehicle, and higher demand for advanced maintenance in premium vehicles. Digital service adoption, including online booking, mobile payment, and connected vehicle diagnostics, is becoming standard. Leading Chinese OEMs are innovating service delivery through authorized centers, mobile units, and battery swap stations, enhancing convenience and efficiency.

Key players in the Global Authorized Car Service Center Market include Toyota Motor, Mercedes-Benz, Ford Motor, Honda Motor, Volkswagen, BMW, Stellantis, Hyundai Motor, Robert Bosch, and General Motors. Companies in the Authorized Car Service Center Market are strengthening their presence through multiple strategies, including expanding geographically into emerging markets, integrating digital platforms for booking, payment, and service tracking, and investing in mobile service solutions. They are forming partnerships with local operators to increase reach, leveraging data analytics to offer predictive maintenance, and improving customer experience with faster turnaround times. OEMs focus on enhancing brand loyalty by providing training, proprietary tools, and genuine parts to maintain service quality, while adopting flexible pricing and subscription-based maintenance plans to attract a broader customer base. Continuous innovation in diagnostics, connected vehicle services, and energy-efficient repairs further reinforces their competitive foothold.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Vehicles Age

- 2.2.4 Propulsion

- 2.2.5 Service

- 2.2.6 Service Providers

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aging vehicle fleet and extended ownership cycles

- 3.2.1.2 Rising vehicle complexity and technology integration

- 3.2.1.3 Increasing vehicle miles traveled (VMT)

- 3.2.1.4 Stringent emission and safety standards

- 3.2.1.5 Growing consumer preference for authorized services

- 3.2.1.6 Expansion of vehicle warranty programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure and equipment costs

- 3.2.2.2 Skilled technician shortage and training costs

- 3.2.2.3 Economic uncertainties and inflation impact

- 3.2.2.4 Supply chain disruptions and parts availability

- 3.2.3 Market opportunities

- 3.2.3.1 Electric vehicle service market emergence

- 3.2.3.2 Digital transformation and online service booking

- 3.2.3.3 Subscription-based maintenance programs

- 3.2.3.4 Expansion in emerging markets

- 3.2.3.5 Fleet management services

- 3.2.3.6 Used vehicle servicing growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal vehicle safety, emissions, and post-repair service regulations

- 3.4.1.2 Canada - Certified maintenance and EV servicing framework

- 3.4.2 Europe

- 3.4.2.1 Germany- EU vehicle safety regulations & national service standards

- 3.4.2.2 UK- Post-Brexit service compliance & connected vehicle guidance

- 3.4.2.3 France- National vehicle inspection & EV servicing policy

- 3.4.2.4 Italy- ITS pilots & smart-service regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT vehicle servicing mandates & standards

- 3.4.3.2 India- Emerging automotive service & connectivity regulations

- 3.4.3.3 Japan- ITS connect & certified service policies

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Digital service booking platforms

- 3.7.1.2 AI-powered diagnostic systems

- 3.7.2 Emerging technologies

- 3.7.2.1 Predictive maintenance technologies

- 3.7.2.2 EV service technologies & infrastructure

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Service pricing models

- 3.9.2 Labor cost trends

- 3.9.3 Parts markup analysis

- 3.9.4 Competitive pricing strategies

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Vehicle fleet demographics & age analysis

- 3.12.1 Global vehicle parc statistics

- 3.12.2 Average vehicle age trends

- 3.12.3 Impact on service demand

- 3.13 Unit Economics & Service Center Profitability Benchmarking

- 3.14 EV Impact on Authorized Service Business Models

- 3.15 Digital Customer Journey & Experience Benchmarking

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hatchbacks

- 5.3 SUVs

- 5.4 Sedan

Chapter 6 Market Estimates & Forecast, By Vehicles Age, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Less than 3 years

- 6.3 More than 3 years

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 ICE

- 7.3 HEV/PHEV

- 7.4 EVs

Chapter 8 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Engine

- 8.3 Transmission

- 8.4 Brakes

- 8.5 Suspension

- 8.6 Electrical

- 8.7 Body

- 8.8 Tire

- 8.9 Belts & accessories

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Service Providers, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEM authorized service centers

- 9.3 Multi-brand service centers

- 9.4 Independent garages

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Individual customers

- 10.3 Fleet operators

- 10.4 Corporate customers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 3M

- 12.1.2 BMW

- 12.1.3 Castrol

- 12.1.4 Ford Motor

- 12.1.5 General Motors

- 12.1.6 Groupe Renault

- 12.1.7 Honda Motor

- 12.1.8 Hyundai Motor

- 12.1.9 Mercedes-Benz

- 12.1.10 Mobivia

- 12.1.11 Robert Bosch

- 12.1.12 Stellantis

- 12.1.13 Suzuki Motor

- 12.1.14 Toyota Motor

- 12.1.15 Volkswagen

- 12.2 Regional Players

- 12.2.1 Automovill Technologies

- 12.2.2 Carxpert Garage

- 12.2.3 Lansdowne Automobile

- 12.2.4 Mahindra First Choice

- 12.2.5 Meineke Car Care Centers

- 12.2.6 Mobil1 Car Care

- 12.2.7 TVS Automobile Solutions

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 GoMechanic

- 12.3.2 Wrench

- 12.3.3 YourMechanic

汽車共乘市場:依預訂類型、車輛類型、應用程式和使用者類型分類-2026-2032年全球市場預測

汽車共乘市場:依預訂類型、車輛類型、應用程式和使用者類型分類-2026-2032年全球市場預測 2026年全球汽車品質服務市場報告2026年全球汽車服務市場報告2026年全球共乘市場報告汽車即服務市場:2026-2032年全球市場預測(依服務模式、車輛類型、燃料類型及客戶類型分類)汽車服務市場:2026-2032年全球市場預測(依服務類型、客戶群、價格範圍、車輛類型和銷售管道)2026年全球認證汽車服務中心市場報告

2026年全球汽車品質服務市場報告2026年全球汽車服務市場報告2026年全球共乘市場報告汽車即服務市場:2026-2032年全球市場預測(依服務模式、車輛類型、燃料類型及客戶類型分類)汽車服務市場:2026-2032年全球市場預測(依服務類型、客戶群、價格範圍、車輛類型和銷售管道)2026年全球認證汽車服務中心市場報告 全球汽車品質服務市場:市場規模、佔有率和趨勢分析(按車輛類型、檢測類型、應用、最終用途和地區分類),細分市場預測(2026-2033 年)全球捲簾鋼製服務門市場按操作方式、材料、門類型、應用、最終用途和配銷通路分類的預測(2026-2032年)

全球汽車品質服務市場:市場規模、佔有率和趨勢分析(按車輛類型、檢測類型、應用、最終用途和地區分類),細分市場預測(2026-2033 年)全球捲簾鋼製服務門市場按操作方式、材料、門類型、應用、最終用途和配銷通路分類的預測(2026-2032年) 美國汽車服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

美國汽車服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)