|

市場調查報告書

商品編碼

1939155

南美洲聚對苯二甲酸乙二酯(PET):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Polyethylene Terephthalate (PET) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

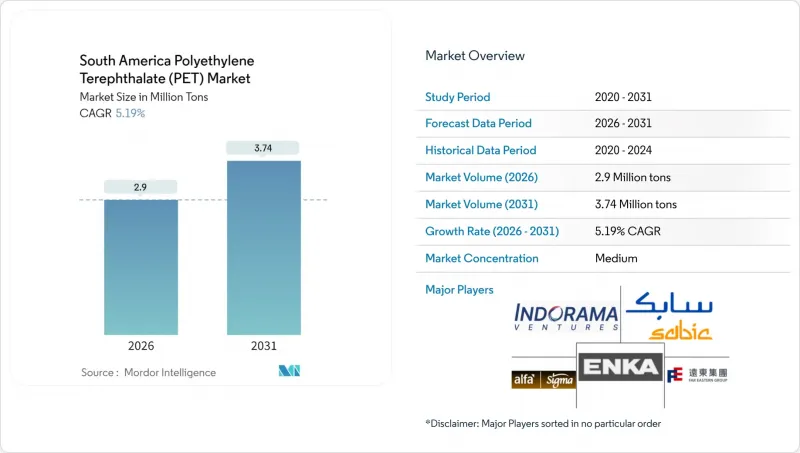

預計到 2026 年,南美洲聚對苯二甲酸乙二醇酯 (PET) 市場規模將達到 290 萬噸。

這意味著產量將從 2025 年的 276 萬噸增加到 2031 年的 374 萬噸,2026 年至 2031 年的年複合成長率(CAGR)為 5.19%。

這一成長軌跡凸顯了巴西向進口替代策略的果斷轉型、強制性再生材料含量法規以及大型消費品公司近岸外包措施如何共同支撐了區域PET需求。儘管桑托斯港和巴拉那瓜港的擁擠在短期內對進口物流構成瓶頸,但也促使加工商優先選擇能夠保證快速交貨的本地樹脂供應商,從而增強了國內投資勢頭。積極的產能擴張,例如可口可樂斥資70億雷亞爾擴建14條生產線,以及回收領域的公私合營,正在拓展供應管道,並降低與石油價格相關的原料價格波動風險。市場競爭依然適中,成熟的跨國公司利用垂直整合優勢,而新興回收企業則透過擴大回收網路和技術授權來提升市場佔有率。

南美聚對苯二甲酸乙二醇酯(PET)市場趨勢與分析

巴西強制使用再生寶特瓶的目標

國家固態廢棄物政策將於2026年起強制實施閉合迴路回收,要求飲料灌裝商對所有瓶子的回收和再加工進行認證。巴西預計2024年回收41萬噸PET,比2022年成長14%,但仍未達到監管要求。南方共同市場統一的食品級再生PET(rPET)標準允許生產商跨境運輸原料,從而降低運輸成本並提高等級一致性。供應鏈正將廢棄物視為戰略資產,並將收集路線從大都會圈擴展到瓶裝軟性飲料日益普及的農業地區。光學分類機和高黏度擠出系統的投資正在迅速成長,一些工廠已根據美國FDA的等效性審核獲得了食品接觸認證。隨著強制性逆向物流報告製度的實施,當地產業業者預計將在打包價格方面獲得更大的議價能力,從而在原油價格波動的情況下穩定原料成本。

餐飲場所飲料需求的成長推動了瓶裝PET的需求。

疫情後拉丁美洲的休閒需求激增,帶動了餐廳、體育場館和活動場所的客流量成長。 0.31升至0.51公升規格的高階寶特瓶需求持續攀升。可口可樂公司投資70億雷亞爾新建了14條運作線,其中許多專門用於生產可回收PET瓶,這種瓶子兼具耐用性和輕便性。百事公司在烏拉圭投資1億美元倉儲設施,利用自由貿易區的優勢,實現了24個出口市場的當週補貨,最大限度地縮短了庫存週轉時間。精釀啤酒廠和地區葡萄酒廠正在將戶外場所的玻璃瓶換成PET容器,每個托盤重量最多可減輕35%。不同設計的瓶身,例如顏色、紋理表面和智慧瓶蓋,可以支撐更高的價格,從而抵消樹脂成本的上漲。高腔吹塑成型機製造商的訂單已排至2026年,這顯示即使宏觀經濟成長放緩,市場需求依然強勁。

與原油價格相關的原物料價格波動

PET利潤率與石腦油和對二甲苯價格掛鉤,而石腦油和對二甲苯價格又與原油基準價格的變動密切相關。巴西石油公司(Petrobras)計劃在2028年前投資167億美元升級煉油廠,但新的對二甲苯或PTA供應來源尚不明朗,這使得轉化企業面臨亞洲基準價格波動的風險。外匯波動也是重要因素,因為原料進口以美元計價,而國內銷售則以雷亞爾或披索結算。大規模一體化企業透過互換協議和多樣化的裂解裝置來對沖風險,而小型轉化企業主要依靠現貨交易,不得不承受近期成本飆升的影響。原料價格的頻繁重估使長期計劃的評估變得複雜,並延緩了新建PET和瓶坯工廠的建設。這種波動風險正在擴大信貸溢價,並提高尋求安裝固體反應器的中型回收企業的資金籌措成本。

細分市場分析

到2025年,包裝應用將佔南美聚對苯二甲酸乙二醇酯(PET)產量的98.58%,這印證了南美PET市場以包裝為中心的生態系統。該領域的結構性優勢源於成熟的飲料生產線、對PET阻隔性能的深入了解以及豐富的拉伸吹塑成型成型技術經驗。電氣和電子產業雖然規模較小,但預計將以7.15%的複合年成長率成長,這主要得益於家用電器組件和低壓連接器外殼等利用PET介電性能的應用。在汽車行業,燃料箱內襯和引擎室液體儲罐是關鍵應用,有助於製造商透過輕量化來滿足燃油經濟性標準。在建築業,PET片材用於照明和隔熱;而在工業和機械行業,PET用於精密導軌和泵組件。可口可樂在容迪亞伊試生產100%再生PET瓶坯,展現了其包裝產業永續性的開創性努力。同時,Sidel 的 Super Combi Line 使加工商能夠快速切換瓶子形狀,從而有助於保持生產線的運轉率。

未來幾年,可回收容器循環系統的擴展和更嚴格的瓶蓋固定法規預計將進一步鞏固PET在包裝應用領域的佔有率。同時,隨著拉丁美洲家用電器產量的成長,高利潤電子應用領域對樹脂的需求預計將會成長。阻燃等級的相互學習可望擴大PET在電子產品領域的應用,而汽車輕量化目標預示著燃料電池堆和電池組件等細分市場對PET的需求。從2026年到2031年,包裝仍將是PET的關鍵應用領域,而PET在各種終端用途的應用將有助於緩解飲料需求的週期性下滑。

南美聚對苯二甲酸乙二醇酯 (PET) 市場報告按終端用戶行業(汽車、建築、電氣電子、工業機械、包裝及其他終端用戶行業)、原料類型(原生 PET 和再生 PET)以及地區(阿根廷、巴西及南美其他地區)進行細分。市場預測以數量(噸)和價值(美元)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 巴西強制要求寶特瓶使用再生材料。

- 餐飲場所對飲料的需求不斷成長,帶動了對PET瓶的需求。

- 巴西提高聚合物進口稅後,促進進口替代

- 公私合營迅速擴大再生聚乙烯(rPET)產能

- 將快速消費品填充生產線近岸外包以降低供應鏈風險

- 市場限制

- 與原油價格相關的原物料價格波動

- 港口擁擠和海關罷工造成的物流瓶頸

- 南美洲的回收基礎建設利用率很低,不到15%。

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 進出口趨勢

- 價格趨勢

- 形態趨勢

- 回收利用概述

- 法律規範

- 終端用戶產業趨勢

- 航太(航太零件製造收入)

- 汽車(汽車生產)

- 建築與施工(新建建築占地面積)

- 電氣電子設備(電氣電子設備生產收入)

- 包裝(塑膠包裝量)

第5章 市場規模和成長預測(價值和數量)

- 按最終用戶行業分類

- 車

- 建築/施工

- 電氣和電子設備

- 工業和機械

- 包裝

- 其他終端用戶產業

- 依原料類型

- 處女寵物

- 回收PET

- 按國家/地區

- 阿根廷

- 巴西

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alfa SAB de CV

- ALPLA

- China Petroleum & Chemical Corporation

- ENKA Insaat ve Sanayi AS

- Far Eastern New Century Corporation

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- Reliance Industries Limited

- SABIC

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

The South America Polyethylene Terephthalate Market size in 2026 is estimated at 2.9 million tons, growing from 2025 value of 2.76 million tons with 2031 projections showing 3.74 million tons, growing at 5.19% CAGR over 2026-2031.

The growth curve highlights Brazil's decisive shift toward import substitution, mandatory recycled-content rules, and near-shoring moves by fast-moving consumer-goods majors that collectively anchor regional PET demand. Port congestion at Santos and Paranagua, while a short-term drag on inbound logistics, is nudging converters to favor local resin suppliers that can guarantee shorter lead times, thereby reinforcing domestic investment momentum. Active capacity expansion-such as Coca-Cola's BRL 7 billion, 14-line build-out-and public-private alliances in recycling are broadening supply options and cushioning volatility in crude-linked feedstock prices. Competitive intensity remains moderate; established multinationals leverage vertical integration, while emerging recyclers win share through collection-network outreach and technology licenses.

South America Polyethylene Terephthalate (PET) Market Trends and Insights

Brazil Mandatory Recycled-Content Targets for PET Bottles

The National Solid Waste Policy makes closed-loop recycling legally binding as of 2026, requiring beverage fillers to demonstrate that every bottle is collected and reprocessed. Brazil recycled 410,000 tons of PET in 2024, a 14% increase from 2022, yet volumes still fall short of compliance needs. Harmonized MERCOSUR food-grade rPET specifications enable producers to shuttle feedstock across borders, thereby trimming transport costs and enhancing grade uniformity. Supply chains now treat waste as a strategic asset, extending pickup routes from megacities to farming belts where bottled soft drink penetration is climbing. Investments in optical sorters and high-viscosity extrusion systems are scaling rapidly, with several facilities already boasting food-contact clearance under U.S. FDA equivalency audits. As reverse logistics reporting becomes enforceable, local players anticipate stronger bargaining power over bale pricing, thereby stabilizing input costs during crude price swings.

Growing On-Premise Beverage Demand Boosting Bottle-Grade PET

Latin America's post-pandemic leisure boom revives restaurant, stadium, and event traffic, lifting demand for premium PET bottles in the 0.31 L-0.51 L range. Coca-Cola has allocated BRL 7 billion to 14 new lines, many of which are dedicated to returnable PET, blending durability with lightweighting. PepsiCo's USD 100 million storage park in Uruguay enables same-week replenishment for 24 export markets, leveraging free-zone perks to minimize inventory holding days. Craft brewers and regional wineries are switching from glass to PET for open-air venues because weight reductions cut freight bills by up to 35% per pallet. Bottle-design differentiation-in colors, tactile finishes, and smart closures-supports higher shelf prices that absorb resin cost escalations. Equipment makers selling high-cavity blow-molders report order backlogs through late 2026, signaling sustained demand even if macroeconomic growth cools.

Crude-Oil-Linked Feedstock Price Volatility

PET margins fluctuate with shifts in naphtha and paraxylene prices, which follow changes in crude benchmarks. Petrobras plans USD 16.7 billion in refining upgrades through 2028, but fresh paraxylene or PTA streams remain unconfirmed, leaving converters exposed to Asian benchmark swings. Currency fluctuations add another layer because feedstock imports are clear in USD, while domestic sales settle in reals or pesos. Large integrated players hedge their exposures via swap arrangements and diversified cracker fleets, whereas small converters operate largely on a spot basis, absorbing immediate cost spikes. Frequent feedstock repricing complicates long-horizon project appraisals, thereby delaying the construction of green-field PET or preform plants. The volatility risk amplifies borrower-credit premiums, increasing finance costs for mid-tier recyclers seeking to incorporate solid-state reactors.

Other drivers and restraints analyzed in the detailed report include:

- Import-Substitution Push After Brazil Polymer Import-Tax Hike

- Rapid Expansion of rPET Capacity via Public-Private Partnerships

- Low South-American Recycling Infrastructure Utilization below 15%

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging applications accounted for 98.58% of the 2025 volume, confirming the South America Polyethylene Terephthalate market as a packaging-centric ecosystem. The segment's structural lead reflects entrenched beverage lines, familiarity with PET's barrier properties, and widespread stretch-blow expertise. Electrical and electronics, although small, are pacing at a 7.15% CAGR and benefit from consumer electronics assemblies and low-voltage connector housings that tap PET's dielectric performance. Automotive uptake centers on fuel-tank liners and under-hood fluid reservoirs, where weight saving helps manufacturers meet efficiency norms. Building and construction uses PET sheets for daylighting and insulation, while industrial and machinery firms select PET for precision guides and pump components. Coca-Cola's 100% rPET preform pilot at Jundiai showcases packaging's sustainability vanguard, whereas Sidel's Super Combi lines enable converters to quickly switch between bottle formats, thereby protecting line uptime.

In the years ahead, additional returnable loops and tethered-cap regulations will likely consolidate packaging's share, while higher-margin electrical applications may pull incremental resin volumes as Latin American appliance output increases. Cross-learning on flame-retardant grades could broaden PET's electronics footprint, while automotive lightweighting targets foreshadow niche demand in fuel-cell stacks and battery components. Over the 2026-2031 period, packaging remains the anchor, but diversified end-use adoption helps buffer cyclical dips in beverage demand.

The South America Polyethylene Terephthalate (PET) Market Report is Segmented by End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-User Industries), Source Type (Virgin PET and Recycled PET), and Geography (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

List of Companies Covered in this Report:

- Alfa S.A.B. de C.V.

- ALPLA

- China Petroleum & Chemical Corporation

- ENKA Insaat ve Sanayi A.S.

- Far Eastern New Century Corporation

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- Reliance Industries Limited

- SABIC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brazil mandatory recycled content targets for PET bottles

- 4.2.2 Growing on-premise beverage demand boosting bottle-grade PET

- 4.2.3 Import-substitution push after Brazil polymer import-tax hike

- 4.2.4 Rapid expansion of rPET capacity via public-private partnerships

- 4.2.5 Near-shoring of FMCG bottling lines to mitigate supply-chain risks

- 4.3 Market Restraints

- 4.3.1 Crude-oil-linked feedstock price volatility

- 4.3.2 Port-congestion and customs-strike logistics bottlenecks

- 4.3.3 Low South-American recycling infrastructure utilisation below 15%

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import And Export Trends

- 4.7 Price Trends

- 4.8 Form Trends

- 4.9 Recycling Overview

- 4.10 Regulatory Framework

- 4.11 End-use Sector Trends

- 4.11.1 Aerospace (Aerospace Component Production Revenue)

- 4.11.2 Automotive (Automobile Production)

- 4.11.3 Building and Construction (New Construction Floor Area)

- 4.11.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.11.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By End-User Industry

- 5.1.1 Automotive

- 5.1.2 Building and Construction

- 5.1.3 Electrical and Electronics

- 5.1.4 Industrial and Machinery

- 5.1.5 Packaging

- 5.1.6 Other End-user Industries

- 5.2 By Source Type

- 5.2.1 Virgin PET

- 5.2.2 Recycled PET

- 5.3 By Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 ALPLA

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 ENKA Insaat ve Sanayi A.S.

- 6.4.5 Far Eastern New Century Corporation

- 6.4.6 Formosa Plastics Group

- 6.4.7 Indorama Ventures Public Company Limited

- 6.4.8 Reliance Industries Limited

- 6.4.9 SABIC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

聚對苯二甲酸乙二醇酯(PET)纖維市場規模、佔有率、趨勢和預測:按原料、纖維類型、形態、應用和地區分類,2026-2034年

聚對苯二甲酸乙二醇酯(PET)纖維市場規模、佔有率、趨勢和預測:按原料、纖維類型、形態、應用和地區分類,2026-2034年 再生聚對苯二甲酸乙二醇酯市場:2026-2032年全球市場預測(依原料種類、形態、等級、製造流程、顏色及應用分類)

再生聚對苯二甲酸乙二醇酯市場:2026-2032年全球市場預測(依原料種類、形態、等級、製造流程、顏色及應用分類) 聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034)。

聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034)。 2026年全球聚對苯二甲酸乙二醇酯(PET)杯市場報告全球聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球聚對苯二甲酸乙二醇酯(PET)杯市場報告全球聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 聚對苯二甲酸乙二醇酯(PET)杯市場規模、佔有率和成長分析:按杯子設計與應用、原料、製造技術、最終用途和地區分類-2026-2033年產業預測

聚對苯二甲酸乙二醇酯(PET)杯市場規模、佔有率和成長分析:按杯子設計與應用、原料、製造技術、最終用途和地區分類-2026-2033年產業預測 歐洲聚對苯二甲酸乙二醇酯(PET):市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲聚對苯二甲酸乙二醇酯(PET):市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 全球雙向拉伸聚對苯二甲酸乙二醇酯(BOPET)薄膜市場分析:按厚度、應用、終端用戶產業和預測(2018-2034 年)生物基聚對苯二甲酸丙二醇酯(BioPTT)市場:市場規模-按地區、應用和預測至2034年

全球雙向拉伸聚對苯二甲酸乙二醇酯(BOPET)薄膜市場分析:按厚度、應用、終端用戶產業和預測(2018-2034 年)生物基聚對苯二甲酸丙二醇酯(BioPTT)市場:市場規模-按地區、應用和預測至2034年 聚對苯二甲酸乙二醇酯市場分析及預測(至2035年):類型、產品類型、應用、形態、材料類型、製程、最終用戶、功能、安裝類型

聚對苯二甲酸乙二醇酯市場分析及預測(至2035年):類型、產品類型、應用、形態、材料類型、製程、最終用戶、功能、安裝類型