|

市場調查報告書

商品編碼

2044112

歐洲聚對苯二甲酸乙二醇酯(PET):市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Europe Polyethylene Terephthalate (PET) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

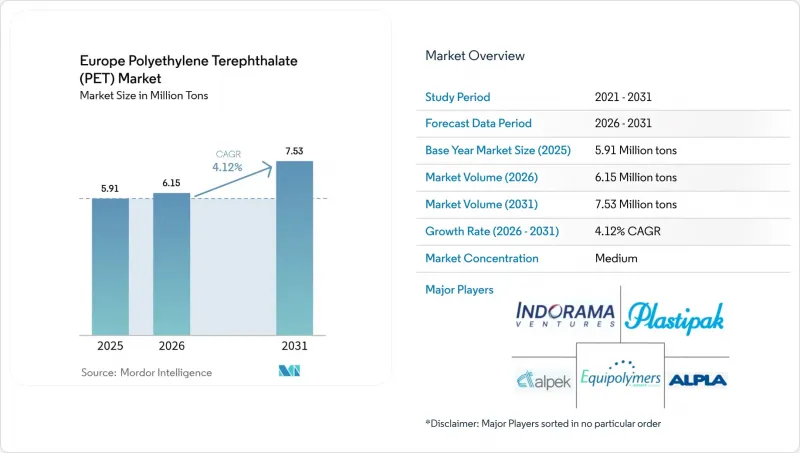

歐洲聚對苯二甲酸乙二醇酯(PET)市場預計將從2025年的591萬噸成長到2026年的615萬噸,到2031年達到753萬噸,2026年至2031年的複合年成長率為4.12%。

儘管原生樹脂仍佔據主導地位,但由於飲料瓶強制使用再生材料以及押金返還計畫的擴大,採購政策正在改變。這種轉變提高了對回收系統效率的需求。對機械和化學回收的投資分別於2024年和2025年開始運作,縮小了原生樹脂和再生PET(rPET)之間的價格差距。然而,生物再生塑膠的政策獎勵措施消除了剩餘的成本溢價。自2021年以來,能源價格上漲導致歐洲生產成本居高不下,而來自土耳其、埃及和越南的進口產品也給區域利潤率帶來了壓力。此外,全球飲料品牌的輕量化策略正在改變樹脂需求的趨勢。這些策略有利於精通精密成型的加工商,但同時也阻礙了包裝總產量的成長。

歐洲聚對苯二甲酸乙二醇酯(PET)市場趨勢與洞察

歐盟一次性塑膠指令規定飲料瓶中必須使用 25% 的再生 PET。

這項指令將再生材料的使用從單純的成本考量轉變為合規要求,品牌所有者現在面臨強制性要求。這項轉變迫使品牌所有者簽訂多年期收購協議,降低了現貨市場的流動性。此外,由於在歐盟以外加工的rPET在2027年之前無法用於實現合規目標,該指令給予歐盟回收商相當於關稅的優惠待遇。這項政策正在推動投資流向歐洲工廠。 2026年2月,Loop Industries策略性地選擇了BASF位於施瓦茨海德的工廠,凸顯了這項指令的影響。

擴大押金返還計畫可以提高PET包的品質和數量。

德國的高回收率使得回收的塑膠袋幾乎不受污染,從而實現了瓶對瓶的循環利用,最大限度地減少了再加工工序。愛爾蘭自實施押金制度以來,容器押金回收率一直非常高,凸顯了合理設定的押金金額對消費者選擇的影響。同時,英國將押金制度的實施推遲到2027年,仍然依賴對存在污染問題的家庭進行回收,這限制了食品級rPET的供應。

來自土耳其、埃及和越南的低成本PET進口正在給歐盟生產商的利潤率帶來壓力。

2025年,土耳其是歐盟最大的PET(聚對苯二甲酸乙二醇酯)外部供應商。由於來自越南和埃及的廉價進口產品擠壓了土耳其國內生產商的利潤空間,安卡拉政府啟動了一項保障措施調查。歐洲製造商面臨能源和原物料成本上漲的困境,被迫降低利潤率。這促使Indorama Ventures公司於2024年對其位於鹿特丹的工廠運作進行了審查。

細分市場分析

從2026年到2031年,再生PET預計將以5.73%的複合年成長率超越原生PET,並在歐洲PET市場穩步擴大其佔有率。 2025年,Sterlinger公司的recoSTAR PET產品獲得歐洲食品安全局(EFSA)的核准,成功應對了更嚴格的物料平衡法規。這項策略措施不僅降低了合規門檻,也吸引了新的投資。原生PET目前佔據73.11%的市場佔有率(截至2025年),因其穩定的熔體流動特性而持續受到業界青睞。但化學回收技術的興起有望有效利用受污染的物料流,並實現供應來源多元化。

葡萄牙、法國和義大利近期擴建的設施主要集中在透明瓶的回收。與之形成對比的是,化學解聚合則致力於解決不透明塑膠和紡織廢棄物帶來的挑戰。為了支持這些創新方法,法國推出了生物再生廢棄物的現金獎勵政策,有效降低了營運成本。這項措施凸顯了雙重回收策略,並根據污染程度進行客製化。隨著監管日益嚴格,精通機械和化學製程的綜合性企業在採購和合規方面獲得了更大的柔軟性,從而增強了其在歐洲PET市場的競爭優勢。

《歐洲聚對苯二甲酸乙二醇酯(PET)市場報告》依原料種類(原生PET、再生PET)、終端用戶產業(包裝、汽車、建築、電氣電子、工業機械及其他終端用戶產業)及地區(法國、德國、義大利、俄羅斯、英國及其他歐洲國家)進行細分。市場預測以噸為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟一次性塑膠指令規定,飲料瓶中必須使用 25% 的再生 PET。

- 押金返還計劃 (DRS) 的擴大提高了 PET 包的品質和數量。

- 將酒精和乳類飲料的包裝從玻璃和金屬容器過渡到PET容器。

- 原生材料與再生PET之間的價格差異正在推動加工商進行替代。

- 擴大化學回收設施將確保食品級rPET的供應。

- 市場限制因素

- 來自土耳其、埃及和越南的低價PET進口產品正在給歐盟生產商的利潤率帶來壓力。

- 歐盟能源成本上漲正在削弱其競爭力。

- 非政府組織主導的塑膠減量宣傳活動正在推廣在飲料產業中使用鋁。

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 進出口趨勢

- 價格趨勢

- 形態趨勢

- 回收利用概述

- 法律規範

- EU

- 法國

- 德國

- 義大利

- 俄羅斯

- 英國

- 終端用戶領域的趨勢

- 航太(來自航太零件生產的銷售額)

- 汽車(汽車產量)

- 建築與施工(新建建築占地面積)

- 電氣和電子(電氣和電子產品生產產生的銷售收入)

- 包裝(塑膠包裝量)

第5章 市場規模與成長預測

- 原料類型

- 處女寵物

- 再生PET(rPET)

- 按最終用戶行業分類

- 包裝

- 車

- 建築/施工

- 電氣和電子

- 工業機械

- 其他終端用戶產業

- 按地區

- 法國

- 德國

- 義大利

- 俄羅斯

- 英國

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alpek SAB de CV

- ALPLA Group

- Equipolymers

- Indorama Ventures Public Company Limited

- JBF Industries Ltd

- Loop Industries

- NAN YA POLYESTER

- NEO GROUP, UAB

- NOVAPET, SA

- Plastipak Holdings, Inc.

- Polyplex

- SIBUR Holding PJSC

- Toray Industries Inc.

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The European Polyethylene Terephthalate Market size is expected to increase from 5.91 million tons in 2025 to 6.15 million tons in 2026 and reach 7.53 million tons by 2031, growing at a CAGR of 4.12% over 2026-2031.

Virgin resin remains dominant, but mandates for recycled content in beverage bottles and a broader deposit-return-scheme coverage are altering procurement decisions. This evolution heightens the demand's responsiveness to collection system efficiencies. Investments in mechanical and chemical recycling, which became operational in 2024 and 2025, have narrowed the price gap between virgin resin and recycled PET (rPET). However, policy incentives for biorecycled plastics have alleviated any remaining cost premium. Even as energy prices have kept European production costs high since 2021, imports from Turkey, Egypt, and Vietnam are squeezing regional margins. Additionally, global beverage brands' lightweighting strategies are changing the resin demand dynamics. These strategies benefit converters skilled in precision molding but simultaneously hinder overall packaging volume growth.

Europe Polyethylene Terephthalate (PET) Market Trends and Insights

EU Single-Use Plastics Directive Mandates 25% rPET in Beverage Bottles

Brand owners now face a mandate, as the directive transforms recycled content from a cost consideration into a compliance requirement. This shift compels them to secure multi-year offtake contracts, which reduces spot-market liquidity. Furthermore, until 2027, the directive provides a tariff-equivalent advantage for EU recyclers, as rPET processed outside the EU does not contribute to compliance targets. This policy channels investments into European facilities. In February 2026, Loop Industries strategically selected BASF's Schwarzheide site, highlighting the directive's impact.

Deposit-Return-Scheme Expansion Boosts PET Bale Quality and Volumes

Germany's high return rate ensures bales remain largely uncontaminated, facilitating direct bottle-to-bottle recycling with minimal reprocessing. In its inaugural operational year, Ireland's impressive container deposit figures underscore the impact of well-calibrated deposit values on consumer choices. On the other hand, the United Kingdom's postponement to 2027 keeps it dependent on curbside streams, which face contamination issues, restricting the supply of food-grade rPET.

Low-Cost PET Imports from Turkey, Egypt, and Vietnam Squeeze EU Producer Margins

In 2025, Turkey was the largest external supplier of PET to the European Union. The government in Ankara initiated a safeguard investigation when its domestic producers experienced margin compression due to cheaper shipments from Vietnam and Egypt. European manufacturers, who faced higher energy and feedstock-related costs, saw their profit margins narrow. This prompted Indorama Ventures to conduct a review of its Rotterdam site operations in 2024.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Shift from Glass or Metal to PET in Alcoholic and Dairy Drinks

- Virgin-versus-rPET Price Spread Incentivizes Converter Substitution

- Elevated EU Energy Costs Erode Competitiveness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

From 2026 to 2031, recycled PET is set to outpace its virgin counterpart, growing at a projected CAGR of 5.73% and steadily expanding its foothold in the European PET market. In 2025, Starlinger's recoSTAR PET art, having secured EFSA approval, adeptly navigated tighter mass-balance regulations. This strategic move not only alleviated compliance hurdles but also drew in fresh investments. While virgin grades, commanding 73.11% of the market (in 2025), remain favored by industries prioritizing consistent melt-flow properties, the ascent of chemical recycling promises to tap into contaminated material streams, diversifying the supply.

Recent mechanical expansions in Portugal, France, and Italy are focusing on clear-bottle loops. In contrast, chemical depolymerization is tackling challenges from opaque and textile waste. To bolster these innovative methods, France has rolled out a cash bonus for biorecycled plastics, effectively mitigating their operational expenses. This initiative highlights a dual recycled-content strategy, customized for different contamination levels. As regulations become more stringent, integrated players proficient in both mechanical and chemical processes gain enhanced sourcing and compliance flexibility, strengthening their competitive edge in the European PET arena.

The Europe Polyethylene Terephthalate (PET) Market Report is Segmented by Source Type (Virgin PET, Recycled PET), End-User Industry (Packaging, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, and Other End-User Industries), and Geography (France, Germany, Italy, Russia, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Alpek S.A.B. de C.V.

- ALPLA Group

- Equipolymers

- Indorama Ventures Public Company Limited

- JBF Industries Ltd

- Loop Industries

- NAN YA POLYESTER

- NEO GROUP, UAB

- NOVAPET, S.A.

- Plastipak Holdings, Inc.

- Polyplex

- SIBUR Holding PJSC

- Toray Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Single-Use Plastics Directive mandates 25% rPET in beverage bottles

- 4.2.2 Deposit-Return-Scheme (DRS) expansion boosts PET bale quality and volumes

- 4.2.3 Lightweighting shift from glass/metal to PET in alcoholic and dairy drinks

- 4.2.4 Virgin-vs-rPET price spread incentivises converter substitution

- 4.2.5 Chemical-recycling build-out secures food-grade rPET supply

- 4.3 Market Restraints

- 4.3.1 Low-cost PET imports (TR, EG, VN) squeeze EU producer margins

- 4.3.2 Elevated EU energy costs erode competitiveness

- 4.3.3 NGO anti-plastic campaigns drive aluminium substitution in beverages

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Import and Export Trends

- 4.7 Price Trends

- 4.8 Form Trends

- 4.9 Recycling Overview

- 4.10 Regulatory Framework

- 4.10.1 EU

- 4.10.2 France

- 4.10.3 Germany

- 4.10.4 Italy

- 4.10.5 Russia

- 4.10.6 United Kingdom

- 4.11 End-use Sector Trends

- 4.11.1 Aerospace (Aerospace Component Production Revenue)

- 4.11.2 Automotive (Automobile Production)

- 4.11.3 Building and Construction (New Construction Floor Area)

- 4.11.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.11.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source Type

- 5.1.1 Virgin PET

- 5.1.2 Recycled PET (rPET)

- 5.2 By End-User Industry

- 5.2.1 Packaging

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 United Kingdom

- 5.3.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Alpek S.A.B. de C.V.

- 6.4.2 ALPLA Group

- 6.4.3 Equipolymers

- 6.4.4 Indorama Ventures Public Company Limited

- 6.4.5 JBF Industries Ltd

- 6.4.6 Loop Industries

- 6.4.7 NAN YA POLYESTER

- 6.4.8 NEO GROUP, UAB

- 6.4.9 NOVAPET, S.A.

- 6.4.10 Plastipak Holdings, Inc.

- 6.4.11 Polyplex

- 6.4.12 SIBUR Holding PJSC

- 6.4.13 Toray Industries Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

聚對苯二甲酸乙二醇酯樹脂市場報告:趨勢、預測與競爭分析(至2035年)

聚對苯二甲酸乙二醇酯樹脂市場報告:趨勢、預測與競爭分析(至2035年) 聚對苯二甲酸乙二醇酯(PET)纖維市場規模、佔有率、趨勢和預測:按原料、纖維類型、形態、應用和地區分類,2026-2034年

聚對苯二甲酸乙二醇酯(PET)纖維市場規模、佔有率、趨勢和預測:按原料、纖維類型、形態、應用和地區分類,2026-2034年 聚對苯二甲酸乙二醇酯(PET)市場:依產品種類、應用及地區分類

聚對苯二甲酸乙二醇酯(PET)市場:依產品種類、應用及地區分類 再生聚對苯二甲酸乙二醇酯市場:2026-2032年全球市場預測(依原料種類、形態、等級、製造流程、顏色及應用分類)

再生聚對苯二甲酸乙二醇酯市場:2026-2032年全球市場預測(依原料種類、形態、等級、製造流程、顏色及應用分類) 聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034)。

聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034)。 2026年全球聚對苯二甲酸乙二醇酯(PET)杯市場報告全球聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球聚對苯二甲酸乙二醇酯(PET)杯市場報告全球聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 聚對苯二甲酸乙二醇酯(PET)杯市場規模、佔有率和成長分析:按杯子設計與應用、原料、製造技術、最終用途和地區分類-2026-2033年產業預測

聚對苯二甲酸乙二醇酯(PET)杯市場規模、佔有率和成長分析:按杯子設計與應用、原料、製造技術、最終用途和地區分類-2026-2033年產業預測 全球雙向拉伸聚對苯二甲酸乙二醇酯(BOPET)薄膜市場分析:按厚度、應用、終端用戶產業和預測(2018-2034 年)生物基聚對苯二甲酸丙二醇酯(BioPTT)市場:市場規模-按地區、應用和預測至2034年

全球雙向拉伸聚對苯二甲酸乙二醇酯(BOPET)薄膜市場分析:按厚度、應用、終端用戶產業和預測(2018-2034 年)生物基聚對苯二甲酸丙二醇酯(BioPTT)市場:市場規模-按地區、應用和預測至2034年