|

市場調查報告書

商品編碼

1939147

汽車冷卻液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Coolant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

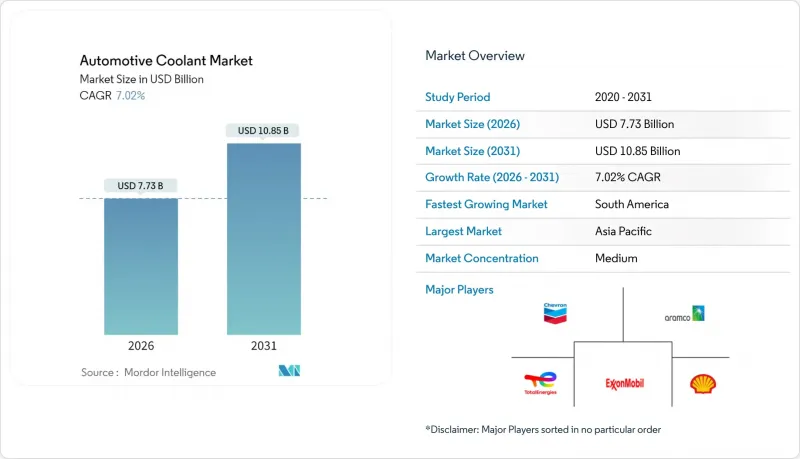

汽車冷卻液市場預計將從 2025 年的 72.2 億美元成長到 2026 年的 77.3 億美元,預計到 2031 年將達到 108.5 億美元,2026 年至 2031 年的複合年成長率為 7.02%。

電動車產量不斷成長、老舊內燃機車隊需要頻繁更換冷卻液,以及日益嚴格的溫度控管法規,共同推動了汽車冷卻液市場的穩定擴張。供應商受益於能夠延長換液週期的增值化學配方,而車隊營運商則可以透過更高品質的配方降低停機成本。電氣化正在重塑產品需求,推動低導電性和介電性冷卻液的大規模生產,從而在傳統的乙二醇基產品線之外創造新的收入來源。

全球汽車冷卻液市場趨勢與洞察

全球汽車保有量不斷成長,車隊卻日益老舊。

老化的車隊催生了持續的售後市場需求,因為與現代長效冷卻液相比,老舊車輛所需的冷卻液更換週期更短。全球汽車保有量的擴張,尤其是在新興市場,正在創造超過新車銷售成長的替換需求。在政府政策(例如生產關聯激勵計劃 (PLI) 和永久性機動車排放控制計劃 (PM E-DRIVE))的支持下,印度汽車售後市場預計將達到大規模的規模,足以支撐龐大的內燃機 (ICE) 車隊的運作。隨著北美和歐洲老化的車隊在關鍵保養週期中從傳統冷卻系統過渡到長效冷卻系統,這一趨勢將尤其有利於售後冷卻液供應商。重型商用車最能反映這一趨勢,車隊營運商擴大採用長效冷卻液,以在管理更多車輛的同時降低維護成本。

原始設備製造商推廣長效 OAT/HOAT 冷卻液

為了實現超過15萬英里的保養週期,汽車製造商正在將有機酸技術(OAT)和混合配方作為標準,這從根本上改變了冷卻液的需求模式,使其從基於用量轉向基於價值。通用汽車(GM)率先採用DexCool冷卻液,將使用壽命延長至15萬英里,而傳統冷卻液的使用壽命僅為3萬英里。這種轉變降低了車輛整個生命週期內的冷卻液總消耗量,同時提高了每單位冷卻液的價值和複雜性。歐洲汽車製造商,例如梅賽德斯-奔馳,正在為某些應用指定15年的保養週期,這催生了對具有更高穩定性和更強防腐蝕性能的優質冷卻液的需求。這種轉變給市場供應商帶來了挑戰:既需要儲備多種不同化學成分的冷卻液,又需要對維修技師進行相容性培訓,因為混合使用不相容的冷卻液會加速零件故障。

原料(乙二醇)價格波動

乙二醇價格波動直接影響冷卻液的生產成本,供應鏈中斷可能會擠壓冷卻液製造商的利潤空間,並限制價格敏感型細分市場的成長。全球乙二醇價格波動影響冷卻液製造商維持價格穩定的能力,對其拓展成本敏感型新興市場造成負面影響。環保生物基甘油替代品的高昂價格加劇了這項挑戰,限制了其在注重成本的售後市場的普及。為了降低進口依賴和外匯波動帶來的風險,供應鏈韌性變得日益重要,例如像Alteco這樣的製造商已在中國建立本地生產基地。原料短缺可能會加速產業整合,尤其是對於那些沒有垂直整合或長期供應協議的小型冷卻液製造商。

細分市場分析

憑藉其卓越的性能和成熟的供應鏈,乙二醇將繼續保持市場領導地位,預計到2025年將佔據汽車冷卻液市場51.92%的佔有率。同時,甘油預計將成為成長最快的細分市場,到2031年複合年成長率將達到9.01%,這反映了環境永續性的迫切需求以及生物基化學技術的應用。乙二醇市場受益於成熟的生產基礎設施和成本優勢,尤其是在亞太地區的生產基地,規模經濟效應使其價格更具競爭力。

該領域的趨勢反映了整個行業的轉型,傳統化工行業的領導地位正受到永續性驅動的創新挑戰,這為擁有生物基技術的供應商創造了機會,而現有的乙二醇生產商除非致力於開發可再生替代品,否則將面臨市場佔有率被侵蝕的風險。

到2025年,乘用車仍將佔據汽車冷卻液市場45.52%的佔有率,這主要得益於電子商務的擴張和最後一公里配送電氣化帶來的特殊溫度控管需求。輕型商用車將成為成長最快的細分市場,到2031年複合年成長率將達到7.12%。雖然乘用車市場受益於大規模生產和標準化的冷卻液規格,但隨著長效冷卻液的推出,更換需求減少,其成長速度將會放緩。商用車應用需要高性能冷卻液,以應對更長的保養週期和嚴苛的駕駛條件。重型商用車市場正擴大採用OAT(氧亞甲基基)配方,以實現100萬英里(約160萬公里)的使用壽命。中型和重型商用車受益於車隊採購優勢和專業的維護保養方式,這些因素使得高階冷卻液配方優於傳統產品。

該領域的轉型反映了交通運輸電氣化的整體趨勢。由於電動車的整體擁有成本優勢,商用車隊正在主導電動車的普及,這也催生了對專用電池溫度控管冷卻劑的需求。美國環保署(EPA)要求在2032年大幅提高插電式電動車(PEV)的普及率,這將對中型貨車產生特別顯著的影響。亞馬遜和聯邦快遞等車隊採購商正在推動電動動力傳動系統的早期應用,而這些系統需要專門的溫度控管解決方案。

區域分析

到2025年,亞太地區將繼續保持其在汽車冷卻液市場的最大佔有率,佔全球市場佔有率的34.53%。這主要得益於中國嚴格的電動車溫度控管法規以及印度在政府製造業激勵政策支持下汽車生產的快速成長。中國的GB標準對電動車冷卻液的電導率有明確的限制,從而催生了對兼顧熱性能和電氣安全要求的專用配方的需求。在印度,在生產關聯激勵計劃(PLI)和PM E-DRIVE政策的支持下,汽車售後市場的成長推動了對傳統冷卻液和電動車專用冷卻液的持續需求,因為印度本土汽車製造商正在建立溫度控管供應鏈。日本和韓國正在為先進電動車技術的發展做出貢獻,這需要用於電池和電力電子設備冷卻的專用介電冷卻液。

南美洲正崛起為成長最快的地區,預計到2031年複合年成長率將達到6.67%。阿根廷和巴西的汽車一體化政策簡化了車輛認證和零件核准流程,同時擴大了商用車生產以滿足不斷成長的電子商務需求。該地區加速成長的原因在於,兩國簽署了相互核准協議,降低了冷卻液製造商向這兩個主要市場供貨的監管門檻,為區域營運創造了規模經濟效益。

北美和歐洲市場已趨於成熟,成長速度較為溫和,這主要得益於長效冷卻劑的普及降低了更換頻率,同時監管要求也推動了高階配方產品的升級。尤其值得一提的是,歐洲市場正面臨來自REACH和PFAS法規的轉型壓力,生物基冷媒替代品更受青睞。這為擁有永續化學技術的供應商創造了機會。北美車隊營運商正在加速採用長效冷卻劑以降低維護成本,雖然對售後市場銷售成長構成結構性阻力,但卻有利於OEM廠商的冷媒填充應用。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球汽車保有量不斷成長,車輛老化問題日益嚴重。

- 原始設備製造商推廣長效 OAT/HOAT 冷卻液

- 新興市場汽車產量成長

- 高性能內燃機設計

- 電動車對介溫度控管液的需求

- 向生物基甘油冷卻劑的環境轉變

- 市場限制

- 原料(乙二醇)價格波動

- 延長換油週期會降低售後市場需求。

- 下一代電動車平台中的閉式冷卻迴路

- 基於毒性的乙二醇監管

- 價值/價值鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 依產品類型

- 乙二醇

- 丙二醇

- 甘油

- 其他

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 公車和長途客車

- 透過技術

- 無機添加劑技術(IAT)

- 有機添加劑技術(OAT)

- 混合有機酸技術(HOAT)

- 最終用戶

- OEM

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Dow Inc.

- Chevron Corporation

- ExxonMobil Corp.

- Shell plc

- TotalEnergies SE

- China Petroleum and Chemical Corp.(Sinopec)

- BP plc(Castrol)

- Saudi Aramco Group

- PETRONAS(Petroliam Nasional Berhad)

- Cummins Inc.

- Fuchs Petrolub SE

- Motul SA

- Old World Industries, LLC(PEAK)

- Recochem Corporation

- CCI Corporation

- Prestone Products Corporation

- Evans Cooling Systems Inc.

- AMSOIL Inc.

第7章 市場機會與未來展望

The automotive coolant market is expected to grow from USD 7.22 billion in 2025 to USD 7.73 billion in 2026 and is forecast to reach USD 10.85 billion by 2031 at 7.02% CAGR over 2026-2031.

Rising electric-vehicle production, aging internal-combustion fleets that require frequent fluid changes, and stricter thermal-management regulations all contribute to the steady expansion of the automotive coolant market. Suppliers gain from value-added chemistry that lengthens drain intervals, while fleet operators reduce downtime costs through premium formulations. Electrification reshapes product needs by pushing low-conductivity, dielectric coolants into volume production, creating a fresh revenue layer atop traditional ethylene-glycol lines.

Global Automotive Coolant Market Trends and Insights

Rising Global Vehicle Parc and Aging Fleet

Fleet aging dynamics create sustained aftermarket demand as older vehicles require more frequent coolant service intervals compared to modern extended-life formulations. The global vehicle parc expansion, particularly in emerging markets, generates replacement demand that outpaces the growth of new vehicle sales. India's automotive aftermarket is projected to reach a significant scale, driven by government policies such as PLI and PM E-DRIVE that incentivize domestic vehicle production while maintaining substantial ICE fleet operations. This trend particularly benefits aftermarket coolant suppliers as aging fleets in North America and Europe transition from conventional to long-life coolant systems during major service intervals. Heavy-duty commercial vehicles demonstrate this pattern most clearly, where fleet operators increasingly adopt extended-life coolants to reduce maintenance costs while managing larger vehicle populations.

OEM Push for Long-Life OAT/HOAT Coolants

Original equipment manufacturers are standardizing on organic acid technology and hybrid formulations to achieve service intervals exceeding 150,000 miles, fundamentally altering coolant demand patterns from volume-based to value-based consumption. General Motors' DexCool adoption established the template, with service life extending to 150,000 miles compared to conventional coolants' 30,000-mile intervals. This shift reduces total coolant volume consumption per vehicle over its lifetime while increasing per-unit coolant value and complexity. European OEMs, such as Mercedes-Benz, specify 15-year service intervals for certain applications, creating demand for premium coolant chemistries with enhanced stability and corrosion protection. The transition challenges aftermarket suppliers to stock multiple chemistry types while educating service technicians on compatibility requirements, as mixing incompatible coolant types accelerates component failures.

Raw-Material (Glycol) Price Volatility

Ethylene glycol price fluctuations directly impact coolant manufacturing costs, with supply chain disruptions creating margin pressure for coolant producers while potentially limiting market growth in price-sensitive segments. Global ethylene glycol pricing volatility affects coolant manufacturers' ability to maintain stable pricing, particularly impacting the penetration of emerging markets, where cost sensitivity remains high. The challenge intensifies as bio-based glycerin alternatives, while environmentally preferred, command premium pricing that limits adoption in cost-conscious aftermarket segments. Supply chain resilience becomes critical as manufacturers like Arteco establish local production facilities in China to mitigate risks associated with import dependency and currency fluctuations. Raw material constraints, particularly for smaller coolant manufacturers lacking vertical integration or long-term supply contracts, can accelerate industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Emerging-Market Vehicle Production

- Demand for Dielectric Thermal-Management Fluids in EVs

- Extended Drain Intervals Cutting Aftermarket Volume

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethylene glycol maintains its market leadership with a 51.92% of the automotive coolant market share in 2025, driven by its proven performance characteristics and established supply chains. Meanwhile, glycerin emerges as the fastest-growing segment, with a 9.01% CAGR through 2031, reflecting environmental sustainability mandates and the adoption of bio-based chemistry. The ethylene glycol segment benefits from mature manufacturing infrastructure and cost advantages, particularly in Asia-Pacific production hubs where scale economies support competitive pricing.

The segment dynamics reflect a broader industry transformation, where traditional chemistry leadership faces disruption from sustainability-driven innovation, creating opportunities for suppliers with bio-based capabilities while challenging established ethylene glycol producers to develop renewable alternatives or risk erosion of their market share.

Passenger cars maintain a 45.52% of the automotive coolant market share in 2025, as e-commerce expansion and last-mile delivery electrification create specialized thermal management requirements. Light commercial vehicles represent the fastest-growing segment, with a 7.12% CAGR through 2031. The passenger car segment benefits from volume production and standardized coolant specifications; however, growth moderates as extended-life coolants reduce the need for replacement. Commercial vehicle applications require higher-performance coolants that can support extended service intervals and severe-duty operation. The heavy-duty segments are increasingly adopting OAT formulations to achieve a 1,000,000-mile service life. Medium- and heavy-duty commercial vehicles benefit from the purchasing power of fleets and professional maintenance practices that favor premium coolant formulations over conventional alternatives.

The segment transformation reflects broader transportation electrification trends, where commercial fleets lead EV adoption due to total cost of ownership benefits, creating demand for specialized battery thermal management coolants. EPA regulations mandating substantial PEV penetration through 2032 particularly impact medium-duty delivery vehicles, where fleet purchasers like Amazon and FedEx drive early adoption of electric powertrains requiring dedicated thermal management solutions.

The Automotive Coolant Market Report is Segmented by Product Type (Ethylene Glycol, Propylene Glycol, Glycerin, Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Technology (IAT, OAT, HOAT), End User (OEM, and Aftermarket), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region maintains the largest regional market share, accounting for 34.53% of the automotive coolant market in 2025. This is driven by China's stringent EV thermal management regulations and India's rapid expansion of automotive production, which is supported by government manufacturing incentives. China's GB standards mandate specific electrical conductivity limits for EV coolants, creating demand for specialized formulations that balance thermal performance with electrical safety requirements. India's automotive aftermarket growth, supported by PLI and PM E-DRIVE policies, generates sustained demand for both conventional and EV-specific coolant formulations as domestic OEMs establish thermal management supply chains. Japan and South Korea contribute to advanced EV technology development, which requires specialized dielectric coolants for battery and power electronics cooling applications.

South America emerges as the fastest-growing region, with a 6.67% CAGR through 2031, benefiting from Argentina-Brazil automotive integration policies that streamline vehicle homologation and component approval processes, while expanding commercial vehicle production to meet growing e-commerce demand. The region's growth acceleration stems from mutual recognition agreements that reduce regulatory barriers for coolant suppliers serving both major markets, creating economies of scale for regional operations.

North America and Europe represent mature markets with moderate growth rates, as the adoption of extended-life coolants reduces replacement frequency, while regulatory requirements drive specification upgrades toward premium formulations. European markets are facing particular transformation pressure from REACH regulations and PFAS restrictions, which favor bio-based coolant alternatives, creating opportunities for suppliers with sustainable chemistry capabilities. North American fleet operators increasingly adopt extended-life coolants to reduce maintenance costs, creating structural headwinds for aftermarket volume growth while benefiting OEM fill applications.

- BASF SE

- Dow Inc.

- Chevron Corporation

- ExxonMobil Corp.

- Shell plc

- TotalEnergies SE

- China Petroleum and Chemical Corp. (Sinopec)

- BP plc (Castrol)

- Saudi Aramco Group

- PETRONAS (Petroliam Nasional Berhad)

- Cummins Inc.

- Fuchs Petrolub SE

- Motul S.A.

- Old World Industries, LLC (PEAK)

- Recochem Corporation

- CCI Corporation

- Prestone Products Corporation

- Evans Cooling Systems Inc.

- AMSOIL Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Vehicle Parc And Aging Fleet

- 4.2.2 OEM Push For Long-Life OAT/HOAT Coolants

- 4.2.3 Growth Of Emerging-Market Vehicle Production

- 4.2.4 Adoption Of High-Performance ICE Designs

- 4.2.5 Demand For Dielectric Thermal-Management Fluids In EVs

- 4.2.6 Environmental Shift Toward Bio-Based Glycerin Coolants

- 4.3 Market Restraints

- 4.3.1 Raw Material (Glycol) Price Volatility

- 4.3.2 Extended Drain Intervals Cutting Aftermarket Volume

- 4.3.3 Sealed Cooling Loops in Next-Gen EV Platforms

- 4.3.4 Toxicity-Driven Ethylene-Glycol Restrictions

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Ethylene Glycol

- 5.1.2 Propylene Glycol

- 5.1.3 Glycerin

- 5.1.4 Others

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Bus and Coaches

- 5.3 By Technology

- 5.3.1 Inorganic Additive Technology (IAT)

- 5.3.2 Organic Additive Technology (OAT)

- 5.3.3 Hybrid Organic Acid Technology (HOAT)

- 5.4 By End User

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Dow Inc.

- 6.4.3 Chevron Corporation

- 6.4.4 ExxonMobil Corp.

- 6.4.5 Shell plc

- 6.4.6 TotalEnergies SE

- 6.4.7 China Petroleum and Chemical Corp. (Sinopec)

- 6.4.8 BP plc (Castrol)

- 6.4.9 Saudi Aramco Group

- 6.4.10 PETRONAS (Petroliam Nasional Berhad)

- 6.4.11 Cummins Inc.

- 6.4.12 Fuchs Petrolub SE

- 6.4.13 Motul S.A.

- 6.4.14 Old World Industries, LLC (PEAK)

- 6.4.15 Recochem Corporation

- 6.4.16 CCI Corporation

- 6.4.17 Prestone Products Corporation

- 6.4.18 Evans Cooling Systems Inc.

- 6.4.19 AMSOIL Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

電動冷卻液幫浦市場-全球市場預測(2026-2032年)汽車冷卻液市場:依技術、冷卻液形態、基礎油、車輛類型、最終用戶和通路分類-2026-2032年全球市場預測

電動冷卻液幫浦市場-全球市場預測(2026-2032年)汽車冷卻液市場:依技術、冷卻液形態、基礎油、車輛類型、最終用戶和通路分類-2026-2032年全球市場預測 汽車冷卻液市場規模、佔有率和成長分析:按化學成分、抑制劑技術類型、產品形式、車輛驅動系統、車輛類型和地區分類-2026-2033年產業預測

汽車冷卻液市場規模、佔有率和成長分析:按化學成分、抑制劑技術類型、產品形式、車輛驅動系統、車輛類型和地區分類-2026-2033年產業預測 汽車冷卻液市場報告:按產品、類型、應用、最終用戶和地區分類(2026-2034 年)

汽車冷卻液市場報告:按產品、類型、應用、最終用戶和地區分類(2026-2034 年) 電動冷卻液幫浦市場規模、佔有率、成長率、全球產業分析、區域分析及未來預測(2026-2034)

電動冷卻液幫浦市場規模、佔有率、成長率、全球產業分析、區域分析及未來預測(2026-2034) 電動冷卻液幫浦市場:按類型、車輛類型、應用、推進類型、技術和地區分類

電動冷卻液幫浦市場:按類型、車輛類型、應用、推進類型、技術和地區分類 2034年農業海水淡化市場預測-全球分析(按來源、技術、系統類型、工廠容量、能源來源、灌溉方式、分配模式、應用、最終用戶和地區分類)

2034年農業海水淡化市場預測-全球分析(按來源、技術、系統類型、工廠容量、能源來源、灌溉方式、分配模式、應用、最終用戶和地區分類) 2026年全球電動冷卻液幫浦市場報告全球汽車冷卻液市場:趨勢、技術發展、電動車整合及展望全球汽車冷卻液和潤滑油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球電動冷卻液幫浦市場報告全球汽車冷卻液市場:趨勢、技術發展、電動車整合及展望全球汽車冷卻液和潤滑油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)