|

市場調查報告書

商品編碼

1939132

防水卷材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Waterproofing Membranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

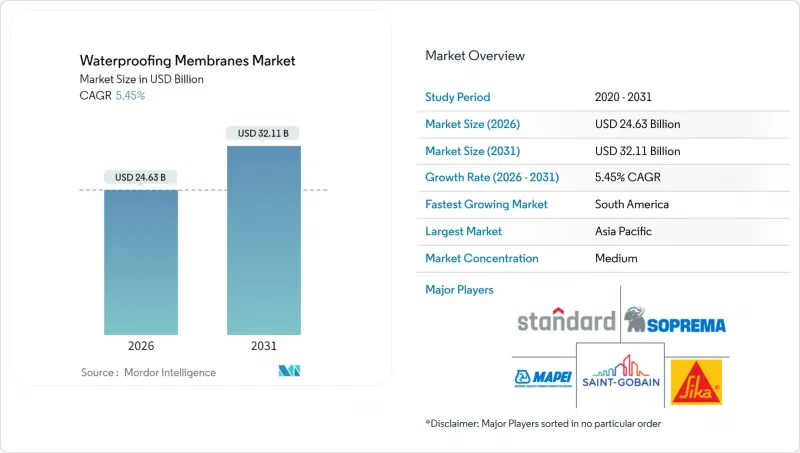

預計到 2026 年,防水膜市場規模將達到 246.3 億美元,高於 2025 年的 233.6 億美元。

預計到 2031 年將達到 321.1 億美元,2026 年至 2031 年的複合年成長率為 5.45%。

加速的都市化、日益嚴格的建築圍護結構節能規範以及基礎設施現代化項目推動了這一成長,這些因素將潛在需求轉化訂單住宅、商業和基礎設施等領域穩定的企劃為基礎。防水保護結構免受水的侵蝕,這是貫穿整個經濟週期的基本需求,因此產品替代的可能性有限。模組化建築、快速的城市發展以及綠色屋頂激勵措施正在改變防水應用格局,安裝人員越來越傾向於使用噴塗式液體系統,因為這種系統可以縮短安裝週期並緩解熟練勞動力短缺的問題。盈利取決於原料的及時避期保值、靈活的配送以及符合最新消防安全和能源性能法規的產品系列。

全球篷布市場趨勢與洞察

快速的都市化和基礎建設

在大都會圈,隨著地鐵網路、交通走廊和綜合用途大樓的擴張,城市人口不斷成長,採購模式也隨之改變。中國的都市化將在2024年達到66.2%,並計畫在2030年達到75%。印度的智慧城市計畫已累計280億美元用於城市基礎建設。這些計畫明確規定,隧道、地下室和裙樓等設施必須採用高品質、長壽命的防水膜,以防止連鎖失效,保障公共和經濟持續發展。由於地下結構需要多層防護,防水膜市場正受惠於單一計劃用量的增加。公私合營下的長期特許經營協議進一步刺激了市場需求,因為它鎖定了維護義務,並鼓勵業主選擇能夠最大限度降低全生命週期成本的耐用解決方案。

加強建築圍護結構的能源標準

能源性能法規將防水卷材視為保溫層內的功能層,模糊了氣密層、防潮層和防水層之間的界線。歐盟的《建築能源性能指令》要求新建築實現淨零能耗,鼓勵設計人員採用能同時控制水分和熱通量的整合式防水系統。在北美,ASHRAE 90.1-2022 標準規定連續氣密層為一項監管要求,這推動了對能夠與基材無縫過渡的液態防水卷材的需求。隨著法規的不斷完善,供應商正在利用高隔熱添加劑和反射顏料的附加價值來獲利,這些添加劑和顏料能夠將傳統的防水捲材轉變為多功能層,從而支撐其在維修和新建市場中的溢價。

瀝青價格波動

煉油廠減產和地緣政治衝擊導致2024年瀝青價格上漲23%,連續三次漲價對整體計劃預算造成了影響。改質瀝青卷材約佔全球消費量的40%,直接吸收原料價格的波動。對成本敏感的住宅屋頂維修承包商無法將額外成本轉嫁給住宅,導致工程延期,並選擇性地轉向熱塑性樹脂。儘管製造商透過長期供應合約和生物基因改質劑來規避成本,但風險敞口仍然是一個結構性挑戰,將在短期內抑制防水捲材市場的成長。

細分市場分析

到2025年,冷塗式防水卷材將佔據防水卷材市場最大的佔有率(33.92%),這主要得益於其能夠在拐角、穿孔和複雜的建築幕牆構件周圍形成無縫屏障。全黏合片材系統的市場佔有率較小,但預計到2031年將以7.38%的複合年成長率成長,因為建築師看重其尺寸穩定性和卓越的A級防火性能。熱塗式防水卷材系統在需要耐高溫的工業環境中仍被應用。同時,儘管銷售量有所下降,但攤舖式防水卷材仍能滿足對成本敏感的屋頂維修的需求。

冷浸防水捲材市場的擴張主要得益於模組化生產線的快速應用,在這些生產線中,速度和品質穩定性至關重要。供應商正將自修復複合材料融入聚氨酯和PMMA基體中,以減少維護返工並延長保固期。同時,全黏合PVC和TPO捲材也越來越受到資料中心建置者的青睞,他們需要低鹵素、阻燃的組件來滿足關鍵任務型安裝的需求。產品組合趨勢正轉向混合型產品,將噴塗基層與預製面層結合,充分發揮兩種技術的優勢。

區域分析

到2025年,亞太地區將佔全球收入的36.08%,這主要得益於中國的「一帶一路」計劃和印度城市軌道交通的快速發展。中印兩國的地鐵建設規劃和智慧城市建設舉措,持續推動膜材供應鏈的訂單。日本和韓國將繼續保持對抗震加固和建築維修的需求,而印尼、越南和泰國則將因工業園區和物流中心的興起而實現兩位數成長。

北美和歐洲是成熟且技術先進的市場。在美國,修訂後的ASHRAE 90.1-2022標準預計將推動對氣密膜的採購。加拿大的基礎設施改善計畫優先考慮地方政府用水和污水處理設施,因此增加了對耐化學腐蝕液體塗覆系統的採購。歐洲的需求集中在強制推行綠屋頂上,柏林和維也納都強制要求在大型平屋頂上安裝植被。膜材市場正在積極響應,推出兼具抗根紮性能和抗穿刺性能的新型配方,以確保與植被結構的兼容性。

預計到2031年,南美洲將引領成長,年複合成長率將達到5.94%,主要得益於巴西一項價值150億美元的排水和防洪項目以及阿根廷布宜諾斯艾利斯的商業重建。儘管匯率波動和資金籌措缺口造成了暫時的挫折,但計劃儲備依然充足。供應商正在建造本地混合工廠,以對沖外匯風險並降低運輸成本。中東和非洲地區預計將溫和成長,因為經濟多元化政策將為社會住宅、旅遊業和公共產業大型企劃提供資金籌措。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速的都市化和不斷擴大的基礎設施建設

- 更嚴格的建築圍護結構能源標準

- 擴大推廣綠屋頂的措施

- 都市區地鐵和隧道建設的快速擴張

- 自修復奈米複合膜的出現

- 模組化建築中液態塗覆膜的強勁轉型

- 市場限制

- 瀝青價格波動

- 熟練安裝人員短缺

- 某些防水卷材的防火等級A級相容性限制

- 價值鏈分析

- 監管環境

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 低溫液體應用

- 高溫液體應用

- 全黏性片材

- 鬆散鋪墊

- 按最終用途

- 商業的

- 工業和公共設施

- 基礎設施

- 住宅

- 按地區

- 亞太地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 韓國

- 泰國

- 越南

- 亞太其他地區

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 歐洲

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲地區

- 南美洲

- 阿根廷

- 巴西

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Ardex Group

- Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

- HOLCIM

- Hongyuan Waterproof Technology Group Co., Ltd.

- Johns Manville

- Keshun Waterproof Technology Co., Ltd.

- Kingspan Group

- MAPEI SpA

- Minerals Technologies Inc.

- RPM International Inc.

- Saint-Gobain

- Sika AG

- SOPREMA Group

- Standard Industries Inc.

- Thermax Limited

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略問題

Waterproofing Membranes Market size in 2026 is estimated at USD 24.63 billion, growing from 2025 value of USD 23.36 billion with 2031 projections showing USD 32.11 billion, growing at 5.45% CAGR over 2026-2031.

This growth is anchored in accelerating urbanization, stringent building-envelope energy codes, and infrastructure modernization programs that convert pent-up demand into steady, project-backed orders across residential, commercial, and infrastructure sites. Product substitution is limited because waterproofing protects structural assets from water ingress, a fundamental requirement that remains constant throughout economic cycles. Modular construction, rapid metro development, and green-roof incentives are reshaping the application mix, while contractors increasingly favor spray-applied liquid systems that shorten installation cycles and mitigate skilled-installer shortages. Profitability hinges on timely raw material hedging, agile distribution, and product portfolios that meet emerging fire safety and energy performance mandates.

Global Waterproofing Membranes Market Trends and Insights

Rapid Urbanization and Infrastructure Build-out

Urban population growth is reshaping procurement patterns as megacities extend their underground networks, transit corridors, and mixed-use towers. China's urbanization rate reached 66.2% in 2024, with a national target of 75% by 2030, and India's Smart Cities Mission has earmarked USD 28 billion for urban infrastructure upgrades. These programs specify premium, long-service-life membranes for tunnels, basements, and podium decks to prevent cascading failures that would otherwise threaten public safety and economic continuity. The waterproofing membranes market benefits from the fact that below-grade structures require multiple layers of protection, driving higher volumes per project. Long concession tenures in public-private partnerships further reinforce demand by locking in maintenance obligations and encouraging owners to choose durable solutions that minimize life-cycle cost.

Tightening Building-Envelope Energy Codes

Energy-performance regulations now treat waterproofing membranes as functional layers within the thermal envelope, blurring the lines between air, vapor, and water barriers. The European Union's Energy Performance of Buildings Directive mandates near-zero-energy new construction, pushing designers to specify integrated membrane systems that control moisture and heat flow simultaneously. In North America, ASHRAE 90.1-2022 lists continuous air barriers as a prescriptive requirement, prompting demand for liquid membranes that create seamless transitions across substrates. As codes evolve, suppliers monetize higher R-value additives and reflective pigments that transform traditional waterproofing into multifunctional layers, supporting premium pricing in both retrofit and new-build markets.

Bitumen Price Volatility

Refinery curtailments and geopolitical shocks lifted bitumen prices by 23% in 2024, prompting three consecutive list-price increases that rippled across project budgets. Modified-bitumen sheets comprise roughly 40% of global consumption and absorb raw-material shocks directly. Contractors in cost-sensitive residential reroofing struggle to pass surcharges to homeowners, causing postponements and selective specification switches to thermoplastics. Manufacturers are hedging through long-term supply contracts and bio-based modifiers, but exposure remains a structural risk that dampens the waterproofing membranes market growth in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Green-Roof Incentives

- Rapid Urban Metro and Tunnel Build-outs

- Skilled-Installer Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cold-liquid-applied membranes held the largest share at 33.92% of the waterproofing membranes market in 2025, thanks to their ability to form seamless barriers around angles, penetrations, and complex facade elements. Fully adhered sheet systems trail but register a 7.38% CAGR through 2031 as architects value their dimensional stability and superior Class A fire performance. Hot liquid systems persist in industrial settings where process temperatures demand thermal resistance, whereas loose-laid sheets continue to cater to cost-sensitive reroofing despite eroding volumes.

The waterproofing membranes market size for cold liquid-applied products is driven by the rapid adoption in modular manufacturing lines that prioritize speed and uniform quality. Suppliers integrate self-healing nano-composites into polyurethane and PMMA matrices, reducing maintenance callbacks and supporting longer warranties. Meanwhile, fully adhered PVC and TPO sheets attract data center builders who require low-halogen, flame-retardant assemblies for mission-critical installations. The product mix is trending toward hybrids that combine spray-applied base layers with prefabricated cap sheets, capitalizing on the respective strengths of each technology.

The Global Waterproofing Membranes Market Report is Segmented by Product Type (Cold Liquid Applied, Hot Liquid Applied, Fully Adhered Sheet, and Loose-Laid Sheet), End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific recorded a 36.08% share of global revenue in 2025, propelled by China's Belt and Road projects and India's surge in urban rail. China and India's metro pipeline and Smart Cities Mission funnel continuous orders into membrane supply chains. Japan and South Korea sustain demand through seismic retrofitting and building rehabilitation, while Indonesia, Vietnam, and Thailand post double-digit growth as industrial parks and logistics hubs proliferate.

North America and Europe represent mature but technologically advanced markets. In the United States, the upgraded ASHRAE 90.1-2022 standards are expected to stimulate spending on membranes that integrate air-barrier functionality. Canada's infrastructure improvement plan prioritizes municipal water and wastewater facilities, increasing procurement of chemically resistant liquid-applied systems. European demand centers on green-roof mandates, with Berlin and Vienna mandating vegetation on expansive flat roofs. The waterproofing membranes market responds by introducing root-resistant formulations that combine elongation with puncture resistance, ensuring compatibility with vegetated assemblies.

South America leads regional growth with a 5.94% CAGR forecast through 2031, guided by Brazil's USD 15 billion drainage and flood-control program and Argentina's commercial redevelopment in Buenos Aires. Currency volatility and financing gaps create intermittent pauses, but project backlogs remain healthy. Suppliers build local blending plants to hedge currency risk and slash freight costs. The Middle East and Africa follow with gradual gains as economic diversification funds public housing, tourism, and utility megaprojects.

- Ardex Group

- Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

- HOLCIM

- Hongyuan Waterproof Technology Group Co., Ltd.

- Johns Manville

- Keshun Waterproof Technology Co., Ltd.

- Kingspan Group

- MAPEI S.p.A.

- Minerals Technologies Inc.

- RPM International Inc.

- Saint-Gobain

- Sika AG

- SOPREMA Group

- Standard Industries Inc.

- Thermax Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation and infrastructure build-out

- 4.2.2 Tightening building-envelope energy-codes

- 4.2.3 Expansion of green-roof incentives

- 4.2.4 Rapid urban metro and tunnel build-outs

- 4.2.5 Emergence of self-healing nano-composite membranes

- 4.2.6 Robust shift towards liquid-applied membranes in modular construction

- 4.3 Market Restraints

- 4.3.1 Bitumen price volatility

- 4.3.2 Skilled-installer shortages

- 4.3.3 Fire-class-A compliance limits for some membranes

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Cold Liquid Applied

- 5.1.2 Hot Liquid Applied

- 5.1.3 Fully Adhered Sheet

- 5.1.4 Loose-Laid Sheet

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 South Korea

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 Canada

- 5.3.2.2 Mexico

- 5.3.2.3 United States

- 5.3.3 Europe

- 5.3.3.1 France

- 5.3.3.2 Germany

- 5.3.3.3 Italy

- 5.3.3.4 Russia

- 5.3.3.5 Spain

- 5.3.3.6 United Kingdom

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Argentina

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Ardex Group

- 6.4.2 Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

- 6.4.3 HOLCIM

- 6.4.4 Hongyuan Waterproof Technology Group Co., Ltd.

- 6.4.5 Johns Manville

- 6.4.6 Keshun Waterproof Technology Co., Ltd.

- 6.4.7 Kingspan Group

- 6.4.8 MAPEI S.p.A.

- 6.4.9 Minerals Technologies Inc.

- 6.4.10 RPM International Inc.

- 6.4.11 Saint-Gobain

- 6.4.12 Sika AG

- 6.4.13 SOPREMA Group

- 6.4.14 Standard Industries Inc.

- 6.4.15 Thermax Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOS

2026年全球防水卷材市場報告

2026年全球防水卷材市場報告 綠色屋頂防水膜市場:按膜類型、材料、安裝方法、厚度範圍、應用和最終用戶分類-全球預測,2026-2032年

綠色屋頂防水膜市場:按膜類型、材料、安裝方法、厚度範圍、應用和最終用戶分類-全球預測,2026-2032年 防水膜市場-全球產業規模、佔有率、趨勢、機會、預測:按材料、類型、應用、地區和競爭格局分類,2021-2031年

防水膜市場-全球產業規模、佔有率、趨勢、機會、預測:按材料、類型、應用、地區和競爭格局分類,2021-2031年 全球地下防水卷材市場:市場規模、份額、成長率、產業分析、類型、應用和地區因素及未來預測(2026-2034)

全球地下防水卷材市場:市場規模、份額、成長率、產業分析、類型、應用和地區因素及未來預測(2026-2034) 防水材料市場規模、佔有率、成長分析(按原料、類型、技術、用途、價格分佈、銷售管道、應用、最終用戶產業和地區分類)-2026-2033年產業預測

防水材料市場規模、佔有率、成長分析(按原料、類型、技術、用途、價格分佈、銷售管道、應用、最終用戶產業和地區分類)-2026-2033年產業預測 防水膜市場機會、成長動力、產業趨勢分析及2025-2034年預測

防水膜市場機會、成長動力、產業趨勢分析及2025-2034年預測 全球防水布市場全球防水膜市場規模(依材料類型、最終用戶、區域範圍、預測)

全球防水布市場全球防水膜市場規模(依材料類型、最終用戶、區域範圍、預測) 2032 年地下防水膜市場預測:按產品、材料、安裝類型、應用、最終用戶和地區進行的全球分析綠色水處理化學品市場按類型、形式、應用和最終用途行業分類 - 2025-2030 年全球預測

2032 年地下防水膜市場預測:按產品、材料、安裝類型、應用、最終用戶和地區進行的全球分析綠色水處理化學品市場按類型、形式、應用和最終用途行業分類 - 2025-2030 年全球預測