|

市場調查報告書

商品編碼

1822642

防水膜市場機會、成長動力、產業趨勢分析及2025-2034年預測Waterproofing Membrane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

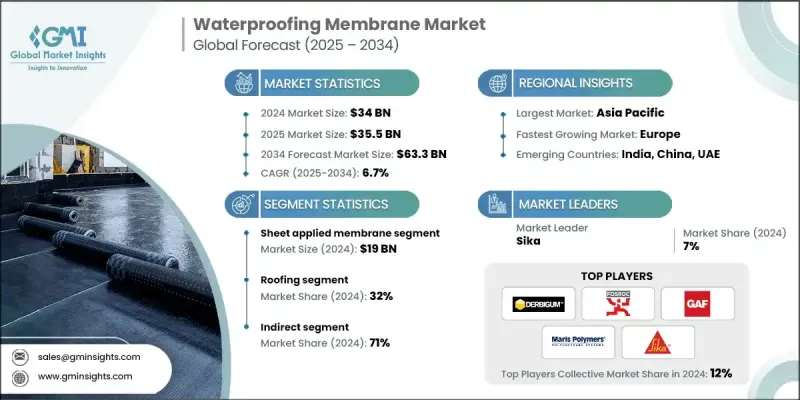

根據 Global Market Insights Inc. 發布的報告,全球防水膜市場規模預計在 2024 年為 340 億美元,預計將從 2025 年的 355 億美元成長到 2034 年的 633 億美元,複合年成長率為 6.7%。

在亞洲、拉丁美洲和非洲部分地區,快速城鎮化地區的建築活動激增,這推動了防水膜的需求。隨著政府和私營部門對基礎設施、住房、商業建築和工業設施的大力投資,人們越來越重視結構的長期耐久性和防潮性能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 340億美元 |

| 預測值 | 633億美元 |

| 複合年成長率 | 6.7% |

片狀應用膜獲得牽引力

片狀防水卷材市場在2024年佔據了顯著的市場佔有率,這得益於其可靠性和易於安裝的特點。這類卷材通常由改質瀝青或熱塑性塑膠製成,厚度均勻,且具有優異的抗滲水性,因此在商業和住宅建築中廣受歡迎。建築業主和承包商青睞這類卷材,因為它具有可預測的性能、耐用性以及與各種基材的兼容性。

屋頂材料應用日益普及

2024年,受新建築和屋頂更換專案的推動,屋頂市場佔據了相當大的佔有率。屋頂暴露在惡劣的天氣條件下,因此堅固的防水措施對於防止漏水和結構損壞至關重要。綠色屋頂和涼爽屋頂解決方案的採用也增加了對結合防水和隔熱功能的先進薄膜技術的需求。

間接銷售需求不斷成長

預計間接防水領域在2025年至2034年期間將以可觀的複合年成長率成長,主要受惠於隧道、橋樑和地下結構等應用。這些應用需要高度專業的防水膜來承受極端壓力和環境壓力。該領域的特點是需要具有優異機械強度、耐化學性和長壽命的防水膜。城市基礎設施項目和公共交通網路的成長顯著推動了這一需求。

區域洞察

亞太地區將崛起為利潤豐厚的地區

受中國、印度和東南亞等國家大規模城鎮化和大型基礎建設項目的推動,到2034年,亞太地區防水膜市場將創造可觀的收入。政府在經濟適用房、商業綜合體和交通基礎設施的支出不斷增加,對高性能防水解決方案的需求也隨之激增。該地區氣候多樣,從熱帶潮濕氣候到極端季風氣候,更凸顯了對能夠適應各種環境條件的多功能防水膜的需求。

防水膜市場的主要參與者有 Pidilite Industries、陶氏、Danrae Group、Kemper System、Asian Paints、Fosroc、Derbigum International、Bauder、BASF、Sika、Xypex Chemical、Maris Polymers、Alchimica Building Chemicals、Koster Bauchemie 和 GAF Materials。

防水膜市場中的企業正在採取多種策略來鞏固其市場地位。產品創新仍然是重中之重,企業正在投入研發資金,開發能夠減少揮發性有機化合物 (VOC) 排放並增強耐用性的環保防水膜。與建築公司和分銷商建立策略合作夥伴關係,可以擴大市場覆蓋範圍並加快產品普及速度。此外,企業正專注於在地化生產,以降低成本並提高亞太等關鍵地區的供應鏈效率。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 快速城市化和基礎設施發展

- 永續性和綠建築趨勢

- 產業陷阱與挑戰

- 原物料價格波動

- 嚴格的環境法規

- 機會

- 新興經濟體的擴張

- 綠屋頂與永續建築

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 液體塗膜

- 聚氨酯

- 丙烯酸纖維

- 瀝青

- 水泥基

- 其他(矽膠等)

- 片狀膜

- PVC

- 三元乙丙橡膠

- 磷酸酯酶

- 其他(丁腈橡膠等)

第6章:市場估計與預測:依原料,2021 - 2034 年

- 主要趨勢

- 瀝青

- 聚合物

- 橡皮

- 其他

第7章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 屋頂

- 地下室和地基

- 牆壁和外牆

- 垃圾掩埋場和隧道

- 其他(陽台等)

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 住宅

- 商業的

- 工業的

- 基礎設施

第9章:市場估計與預測:按配銷通路,2021 - 2034

- 主要趨勢

- 直銷

- 間接銷售

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Alchimica Building Chemicals

- Asian Paints

- BASF

- Bauder

- Danrae Group

- Derbigum International

- Dow

- Fosroc

- GAF Materials

- Kemper System

- Koster Bauchemie

- Maris Polymers

- Pidilite Industries

- Sika

- Xypex Chemical

The global waterproofing membrane market was estimated at USD 34 billion in 2024 and is expected to grow from USD 35.5 billion in 2025 to USD 63.3 billion by 2034, at a CAGR of 6.7%, according to the report published by Global Market Insights Inc.

The global surge in construction activity in rapidly urbanizing regions across Asia, Latin America, and parts of Africa is boosting demand for waterproofing membranes. As governments and private sectors invest heavily in infrastructure, housing, commercial buildings, and industrial facilities, there is a growing emphasis on long-term structural durability and moisture protection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34 Billion |

| Forecast Value | $63.3 Billion |

| CAGR | 6.7% |

Sheet Applied Membrane to Gain Traction

The sheet-applied membrane segment held a notable share in 2024, driven by its reliability and ease of installation. These membranes, often made from modified bitumen or thermoplastics, provide consistent thickness and excellent resistance to water infiltration, making them popular in commercial and residential construction. Building owners and contractors favor this segment because it offers predictable performance, durability, and compatibility with various substrates.

Rising Adoption in Roofing

The roofing segment generated a significant share in 2024, fueled by new construction and roof replacement projects. Roofs are exposed to harsh weather conditions, making robust waterproofing essential to prevent leaks and structural damage. The adoption of green roofs and cool roofing solutions has also increased the need for advanced membrane technologies that combine waterproofing with thermal insulation.

Growing Demand in Indirect Sales

The indirect segment is expected to grow at a decent CAGR during 2025-2034, driven by applications such as tunnels, bridges, and underground structures. They require highly specialized waterproofing membranes to withstand extreme pressure and environmental stress. This segment is characterized by the need for membranes with superior mechanical strength, chemical resistance, and longevity. Growth in urban infrastructure projects and public transportation networks is significantly boosting the demand.

Regional Insights

Asia Pacific to Emerge as a Lucrative Region

Asia Pacific waterproofing membrane market will generate substantial revenues by 2034, driven by extensive urbanization and large-scale infrastructure projects in countries like China, India, and Southeast Asia. Increased government spending on affordable housing, commercial complexes, and transportation infrastructure is creating substantial demand for high-performance waterproofing solutions. The region's diverse climate, ranging from tropical humidity to extreme monsoons, emphasizes the need for versatile membranes capable of adapting to varying environmental conditions.

Major players in the waterproofing membrane market are Pidilite Industries, Dow, Danrae Group, Kemper System, Asian Paints, Fosroc, Derbigum International, Bauder, BASF, Sika, Xypex Chemical, Maris Polymers, Alchimica Building Chemicals, Koster Bauchemie, and GAF Materials.

Companies in the waterproofing membrane market are adopting several strategies to strengthen their market foothold. Product innovation remains a top priority, with firms investing in research to develop eco-friendly membranes that reduce VOC emissions and enhance durability. Strategic partnerships with construction firms and distributors enable wider market reach and faster adoption. Additionally, companies are focusing on localized manufacturing to reduce costs and improve supply chain efficiency in key regions like Asia Pacific.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Raw material

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization & infrastructure development

- 3.2.1.2 Sustainability & green building trends

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Strict environmental regulations

- 3.2.3 Opportunities

- 3.2.3.1 Expansion in emerging economies

- 3.2.3.2 Green roofing and sustainable construction

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade Statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 ($Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid-applied membrane

- 5.2.1 Polyurethane

- 5.2.2 Acrylic

- 5.2.3 Bituminous

- 5.2.4 Cementitious

- 5.2.5 Others (silicone etc.)

- 5.3 Sheet membrane

- 5.3.1 PVC

- 5.3.2 EPDM

- 5.3.3 TPO

- 5.3.4 Others (nitrile rubber etc.)

Chapter 6 Market Estimates & Forecast, By Raw Material, 2021 - 2034 ($Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Bitumen

- 6.3 Polymers

- 6.4 Rubber

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Roofing

- 7.3 Basement & foundation

- 7.4 Walls & facades

- 7.5 Landfills & tunnels

- 7.6 Others (balconies etc.)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.5 Infrastructure

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alchimica Building Chemicals

- 11.2 Asian Paints

- 11.3 BASF

- 11.4 Bauder

- 11.5 Danrae Group

- 11.6 Derbigum International

- 11.7 Dow

- 11.8 Fosroc

- 11.9 GAF Materials

- 11.10 Kemper System

- 11.11 Koster Bauchemie

- 11.12 Maris Polymers

- 11.13 Pidilite Industries

- 11.14 Sika

- 11.15 Xypex Chemical

防水膜市場:依技術、應用、終端用戶和通路分類-2026-2032年全球市場預測

防水膜市場:依技術、應用、終端用戶和通路分類-2026-2032年全球市場預測 2026年全球防水卷材市場報告綠色屋頂防水膜市場:按膜類型、材料、安裝方法、厚度範圍、應用和最終用戶分類-全球預測,2026-2032年

2026年全球防水卷材市場報告綠色屋頂防水膜市場:按膜類型、材料、安裝方法、厚度範圍、應用和最終用戶分類-全球預測,2026-2032年 防水卷材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

防水卷材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 防水膜市場-全球產業規模、佔有率、趨勢、機會、預測:按材料、類型、應用、地區和競爭格局分類,2021-2031年

防水膜市場-全球產業規模、佔有率、趨勢、機會、預測:按材料、類型、應用、地區和競爭格局分類,2021-2031年 全球地下防水卷材市場:市場規模、份額、成長率、產業分析、類型、應用和地區因素及未來預測(2026-2034)

全球地下防水卷材市場:市場規模、份額、成長率、產業分析、類型、應用和地區因素及未來預測(2026-2034) 防水材料市場規模、佔有率、成長分析(按原料、類型、技術、用途、價格分佈、銷售管道、應用、最終用戶產業和地區分類)-2026-2033年產業預測

防水材料市場規模、佔有率、成長分析(按原料、類型、技術、用途、價格分佈、銷售管道、應用、最終用戶產業和地區分類)-2026-2033年產業預測 全球防水布市場全球防水膜市場規模(依材料類型、最終用戶、區域範圍、預測)

全球防水布市場全球防水膜市場規模(依材料類型、最終用戶、區域範圍、預測) 2032 年地下防水膜市場預測:按產品、材料、安裝類型、應用、最終用戶和地區進行的全球分析

2032 年地下防水膜市場預測:按產品、材料、安裝類型、應用、最終用戶和地區進行的全球分析