|

市場調查報告書

商品編碼

1939059

東南亞黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Southeast Asia Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

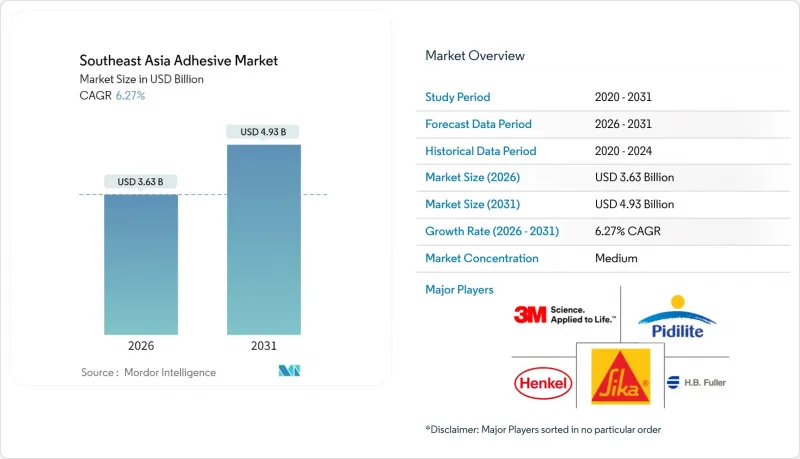

預計到 2026 年,東南亞黏合劑市場規模將達到 36.3 億美元。

這意味著從 2025 年的 34.2 億美元成長到 2031 年的 49.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.27%。

印尼和越南不斷成長的建築支出、泰國和印尼電動汽車電池投資的加速以及向低VOC水性化學品的轉變,都支撐著這一成長勢頭。外國直接投資在電子、鞋類和醫療耗材製造業的湧入,正在擴大區域基本客群,並促進樹脂和配方資產的下游在地化。越南的《化學品法》(65/2025/QH15)和新加坡的《國家環境局VOC法規》等法規結構正在重新定義技術選擇,並推動對符合循環經濟目標的水性、反應型和紫外光固化系統的需求。儘管石化原料價格波動對短期利潤率帶來壓力,但擁有穩定供應合約和垂直整合能力的生產商可以保障利潤,並投資於產能擴張,例如將西卡位於勿加泗的工廠的生產線規模擴大一倍。能夠將本地化生產、合規化學品和應用培訓相結合的黏合劑供應商,在贏得基礎設施、包裝和電動車供應鏈計劃的新訂單具有優勢。

東南亞黏合劑市場趨勢與洞察

印尼和越南的主導建設熱潮

印尼和越南龐大的政府預算正推動水泥、鋼材和工程板材等大型企劃投入創紀錄的用量,例如胡志明市的3號環城公路。黏合劑正在取代磁磚鋪設、隔熱材料、帷幕牆和模組化預製構件中的機械緊固件,從而縮短現場施工時間並提高氣密性。建築商傾向使用符合東協綠色建築VOC(揮發性有機化合物)限值50克/公升的水性丙烯酸和反應型聚氨酯產品。雅加達和胡志明市附近的預製構件工廠正在使用無需烘箱即可在炎熱潮濕的熱帶氣候下固化的雙組分環氧樹脂,從而能夠在24小時內交貨建築幕牆模組。

電子商務主導了軟性及永續包裝需求的成長

東南亞各地的線上零售商對使用黏合劑和水性黏合劑的瓦楞紙包裝袋、包裝袋和易撕標籤的需求日益成長。像艾利丹尼森的CleanFlake這樣的壓敏黏著劑產品在清洗過程中可以完全釋放,從而提高PET的回收率,並幫助品牌商達到東協循環經濟框架下的回收目標。使用漢高Technomelt Supra 115的瓦楞紙加工商每分鐘可封口多達120個瓦楞紙箱,節省了溶劑型膠合劑所需的能源。消費者願意為環保包裝支付更高的價格,這提高了獲得生物基或無溶劑生產線認證的加工商的利潤率。這些趨勢共同推動了東南亞黏合劑市場對永續等級產品的潛在需求成長。

嚴格的揮發性有機化合物和危險化學品法規

為了應對新的VOC閾值法規,中型製造商現在必須對每條產品線進行大量投資,用於產品配方調整、安全測試和重新註冊。新加坡的排放報告要求增加了年度管理成本,迫使一些中小企業將生產外包或退出監管嚴格的行業。水基系統雖然可以解決VOC問題,但需要更長的乾燥週期,除非安裝除濕設備,否則會增加生產時間,這對注重成本的工廠來說是一個障礙。 APEC的協調促進了跨境貿易,但不同的過渡期造成了暫時的套利機會,並使供應鏈規劃變得複雜。

細分市場分析

在所有樹脂中,聚氨酯的成長速度最快,複合年成長率達到6.57%。這主要歸功於單面聚氨酯黏合劑的廣泛應用,可消除電動車電池和無溶劑鞋類生產線中的排放(VOC)排放。丙烯酸樹脂憑藉其成本和性能的平衡優勢,在軟包裝層壓材料和瓷磚砂漿領域仍佔據主導地位,市佔率高達31.18%。環氧樹脂則服務於電池組組裝等細分結構市場。 SikaPower-4720在室溫下固化後可達到25 MPa的拉伸強度。由於瓦克在亞洲新建的符合ISO 10993標準的矽樹脂生產線,醫療設備對矽膠樹脂的需求正持續成長。

對永續性的日益成長的需求推動了蓖麻油衍生生物基聚氨酯的研發,而BASF的丙烯酸丁酯供應協議則凸顯了原料安全的重要性。聚氨酯將鋁與碳纖維黏合,在東南亞黏合劑市場中扮演越來越重要的角色,幫助汽車製造商實現輕量化目標,降低車輛重量。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 印尼和越南的主導建設熱潮

- 電子商務推動了對靈活、永續包裝的需求激增

- 擴大拋棄式產品的生產

- 監理推動低VOC水性及反應性塗料體系的發展

- 在泰國和印尼投資電動車電池製造

- 市場限制

- 嚴格的揮發性有機化合物和危險化學品法規

- 石油化工原料價格波動劇烈

- 缺乏能夠操作先進化學技術的熟練工人

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 通過樹脂

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 矽酮

- 氰基丙烯酸酯

- VAE/EVA

- 其他樹脂

- 透過技術

- 水溶液

- 溶劑型

- 反應性

- 熱熔膠

- 紫外線固化型

- 按最終用戶行業分類

- 航太工業

- 車

- 建築/施工

- 鞋革業

- 衛生保健

- 包裝

- 木工和細木工

- 其他終端用戶產業

- 按地區

- 印尼

- 馬來西亞

- 菲律賓

- 新加坡

- 泰國

- 越南

- 東南亞及其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- ADB Sealant Co., Ltd

- Arkema

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- Dymax Corporation

- Franklin International

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- Mapei SpA

- Permabond LLC

- Pidilite Industries Ltd.

- Shin-Etsu Chemical Co., Ltd

- Sika AG

- Soudal NV

- Wacker Chemie AG

第7章 市場機會與未來展望

The Southeast Asia Adhesive Market size in 2026 is estimated at USD 3.63 billion, growing from 2025 value of USD 3.42 billion with 2031 projections showing USD 4.93 billion, growing at 6.27% CAGR over 2026-2031.

Rising construction outlays in Indonesia and Vietnam, accelerating EV-battery investments in Thailand and Indonesia, and the shift toward low-VOC waterborne chemistries collectively underpin this momentum. Foreign direct investment in electronics, footwear, and medical disposables manufacturing expands the regional customer base and stimulates the downstream localization of resin and formulation assets. Regulatory frameworks, such as Vietnam's Law on Chemicals (65/2025/QH15) and Singapore's NEA VOC limits, are redefining technology choices, steering demand toward water-borne, reactive, and UV-cured systems that align with circular economy goals. Price volatility in petrochemical feedstocks creates short-term margin pressure; however, producers with secured supply contracts or vertical integration can protect their earnings and invest in capacity expansions, such as Sika's Bekasi line doubling. Adhesive suppliers that combine localized production, compliant chemistries, and application training are best placed to capture new orders from infrastructure, packaging, and EV supply-chain projects.

Southeast Asia Adhesive Market Trends and Insights

Infrastructure-Led Construction Boom in Indonesia and Vietnam

Significant government budgets in Indonesia and Vietnam channel record volumes of cement, steel, and engineered panels into megaprojects such as the Ho Chi Minh City Ring Road 3. Adhesives replace mechanical fasteners in tile setting, insulation, curtain wall, and modular precast elements, shortening on-site labor and improving airtightness. Contractors prefer water-borne acrylic and reactive polyurethane grades that comply with ASEAN Green Building VOC caps of 50 g/L. Prefabrication plants situated near Jakarta and Ho Chi Minh City utilize two-component epoxies that cure in humid tropical climates without the need for ovens, allowing for a 24-hour turnaround of facade modules.

E-Commerce-Driven Surge in Flexible and Sustainable Packaging

Online retail across Southeast Asia requires corrugate mailers, pouches, and easy-peel labels that rely on hot-melt and water-borne adhesives. Pressure-sensitive products, such as Avery Dennison's CleanFlake, enhance PET recycling rates by detaching cleanly during wash cycles, enabling brand owners to meet recycling targets under the ASEAN Circular Economy framework. Corrugate converters running Henkel Technomelt Supra 115 seal up to 120 cartons per minute, saving energy required by solvent types. Consumer willingness to pay a premium for eco-friendly packaging elevates margins for converters that certify bio-based or solvent-free lines. These trends collectively widen the addressable pool for sustainable grades within the Southeast Asia adhesive market.

Stringent VOC and Hazardous-Chemical Regulations

Mid-sized producers are now required to invest significantly per product line for reformulation, safety testing, and re-registration, all in response to new VOC threshold compliance mandates. Singapore's mandatory emissions reporting adds annual administrative expenses, prompting some SMEs to outsource production or exit high-compliance segments. Water-borne systems solve VOC challenges but extend drying cycles, increasing production time unless dehumidification is installed, a barrier for cost-sensitive workshops. Harmonization under APEC facilitates cross-border trade, but varying phase-in periods create temporary arbitrage, complicating supply chain planning.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hygiene and Medical Disposables Manufacturing

- Regulatory Push Toward Low-VOC Water-Borne and Reactive Systems

- Volatile Petrochemical Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane achieved a 6.57% CAGR, the fastest among resins, as EV batteries and solvent-free footwear lines specify single-sided PU adhesives that eliminate VOC emissions. Acrylic stayed dominant with a 31.18% share owing to its balanced cost and performance in flexible packaging laminates and tile-setting mortars. Epoxy addressed structural niches, such as battery-pack assembly. SikaPower-4720 reaches a tensile strength of 25 MPa while curing at room temperature. Silicone volumes in medical devices increased, supported by Wacker's new Asian capacity that meets ISO 10993 standards.

Intensifying sustainability pressure drives the development of bio-based polyurethanes derived from castor oil, while BASF's butyl-acrylate supply agreement highlights feedstock security priorities. Polyurethane's bonding of aluminum-to-carbon-fiber joints satisfies OEM lightweighting goals, enabling reduction in vehicle mass, thereby further expanding its role in the Southeast Asia adhesive market.

The Southeast Asia Adhesive Market Report is Segmented by Resin (Polyurethane, Epoxy, Acrylic, Silicone, Cyanoacrylate, and More), Technology (Water-Borne, Solvent-Borne, Reactive, Hot-Melt, and UV Cured), End-User Industry (Aerospace, Automotive, and More), and Geography (Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, and Rest of South-East Asia). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- ADB Sealant Co., Ltd

- Arkema

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- Dymax Corporation

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- Mapei S.p.A

- Permabond LLC

- Pidilite Industries Ltd.

- Shin-Etsu Chemical Co., Ltd

- Sika AG

- Soudal NV

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure-led construction boom in Indonesia and Vietnam

- 4.2.2 E-commerce-driven surge in flexible and sustainable packaging

- 4.2.3 Expansion of hygiene and medical disposables manufacturing

- 4.2.4 Regulatory push toward low-VOC water-borne and reactive systems

- 4.2.5 EV-battery manufacturing investments in Thailand and Indonesia

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and hazardous-chemical regulations

- 4.3.2 Volatile petrochemical feedstock prices

- 4.3.3 Shortage of skilled applicators for advanced chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Reactive

- 5.2.4 Hot-Melt

- 5.2.5 UV Cured

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Building and Construction

- 5.3.4 Footwear and Leather

- 5.3.5 Healthcare

- 5.3.6 Packaging

- 5.3.7 Woodworking and Joinery

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Philippines

- 5.4.4 Singapore

- 5.4.5 Thailand

- 5.4.6 Vietnam

- 5.4.7 Rest of South-East Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 ADB Sealant Co., Ltd

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 Avery Dennison Corporation

- 6.4.6 Beardow Adams

- 6.4.7 Dow

- 6.4.8 DuPont

- 6.4.9 Dymax Corporation

- 6.4.10 Franklin International

- 6.4.11 H.B. Fuller Company

- 6.4.12 Henkel AG & Co. KGaA

- 6.4.13 Huntsman International LLC

- 6.4.14 ITW Performance Polymers

- 6.4.15 Jowat SE

- 6.4.16 Mapei S.p.A

- 6.4.17 Permabond LLC

- 6.4.18 Pidilite Industries Ltd.

- 6.4.19 Shin-Etsu Chemical Co., Ltd

- 6.4.20 Sika AG

- 6.4.21 Soudal NV

- 6.4.22 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測 2026年全球磁磚黏合劑市場報告

2026年全球磁磚黏合劑市場報告 混凝土黏合劑市場:按產品類型、形式、應用和最終用途產業分類-2026-2032年全球市場預測

混凝土黏合劑市場:按產品類型、形式、應用和最終用途產業分類-2026-2032年全球市場預測 無塵室黏合墊市場規模、佔有率和成長分析:按材料、黏合劑類型、產品設計、最終用途產業和地區分類-2026-2033年產業預測黏合劑市場:2026-2032年全球市場預測(黏合劑產品形態、化學性質、黏合技術和最終用途產業分類)紡織黏合劑市場:黏合劑類型、形態、功能、織物類型、最終用戶和分銷管道分類-全球預測,2026-2032年黏合劑機器類型、聚合物類型、速度、黏度、應用、最終用途產業和銷售管道,全球預測,2026-2032年有機熱連接件市場:依產品類型、應用、終端用戶產業及通路分類,全球預測(2026-2032年)橡皮筋黏合劑市場按類型、形式、分銷管道、應用和最終用戶分類,全球預測(2026-2032年)橡膠基材黏合劑市場按配方技術、樹脂類型、基材類型、最終用途產業和應用分類-全球預測,2026-2032年

無塵室黏合墊市場規模、佔有率和成長分析:按材料、黏合劑類型、產品設計、最終用途產業和地區分類-2026-2033年產業預測黏合劑市場:2026-2032年全球市場預測(黏合劑產品形態、化學性質、黏合技術和最終用途產業分類)紡織黏合劑市場:黏合劑類型、形態、功能、織物類型、最終用戶和分銷管道分類-全球預測,2026-2032年黏合劑機器類型、聚合物類型、速度、黏度、應用、最終用途產業和銷售管道,全球預測,2026-2032年有機熱連接件市場:依產品類型、應用、終端用戶產業及通路分類,全球預測(2026-2032年)橡皮筋黏合劑市場按類型、形式、分銷管道、應用和最終用戶分類,全球預測(2026-2032年)橡膠基材黏合劑市場按配方技術、樹脂類型、基材類型、最終用途產業和應用分類-全球預測,2026-2032年