|

市場調查報告書

商品編碼

1939048

中國中游油氣市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)China Oil And Gas Midstream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

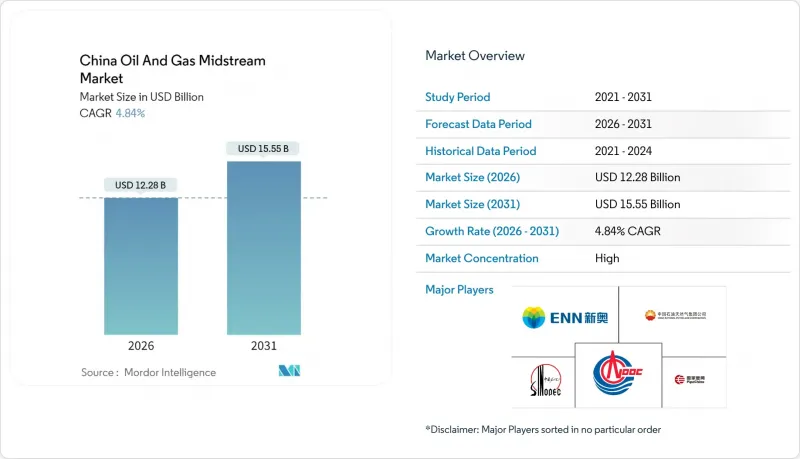

預計到 2026 年,中國中游油氣市場規模將達到 122.8 億美元,高於 2025 年的 117.1 億美元。

預計到 2031 年將達到 155.5 億美元,2026 年至 2031 年的複合年成長率為 4.84%。

市場成長的驅動力來自北京提出的能源安全和碳中和的雙重目標,這些目標優先考慮基礎設施韌性、供應多元化和可衡量的排放。工業和住宅用戶對天然氣需求的激增,加上國內產量的穩定,推動了對額外運輸、進口加工和儲存能力的需求。政策支持的管道里程擴張、LNG接收站的加速運作以及強制性戰略儲備目標,為承包商和設備供應商創造了持續的建設機會。數位化,特別是人工智慧驅動的監控系統,正在推動資產利用率的提高、營運成本的降低以及對環境法規更嚴格的遵守,從而進一步提升計劃的經濟效益。

中國油氣中游市場趨勢與洞察

延長國家天然氣管道

中國的「十四五」規劃旨在2025年將天然氣輸送管網擴展至12萬公里(比2020年增加25%)。該規劃的核心是東西向天然氣輸送系統。冗餘的主幹管道降低了地緣政治或技術動盪期間單點故障的風險,並加強了區域平衡。統一的管道所有權加快了互聯互通,實現了靈活的雙向輸送,並提高了運轉率。計劃於2024年運作的中俄東線將使天然氣供應來源多元化,並降低對海運的依賴。省際陸上協調工作較為複雜,但一旦獲得許可,集中規劃將縮短建設週期。這些計劃為專業承包商、高規格管道製造商和數位化監測解決方案提供者帶來了巨大的機會。

加速液化天然氣再氣化終端的建設。

預計到2024年,中國液化天然氣(LNG)再氣化能力將達到每年1.3億噸,另有4,000萬噸的產能正在興建中,中國已成為全球最活躍的LNG基礎建設國。為了緩解供應瓶頸,中國正在採用小規模、分佈更分散的設施。 2022年危機期間,大型接收站出現堵塞,供應瓶頸問題凸顯。沿海城市越來越重視浮體式再氣化裝置(FSRU),因為其部署速度快、資本支出柔軟性且對陸上土地的需求量小。舟山第三期接收站於2024年運作,憑藉其先進的蒸氣回收系統,甲烷排放減少了15%,樹立了國內新的標竿。 65%的平均運轉率既保證了策略儲備,也為機會性現貨採購留出了空間。這有助於進口多元化,並加強該領域的價格風險管理。

延長環境和土地使用許可程序

目前,環境評估需要18至36個月,穿越生態保護區的路線核准時間更長。在人口稠密的東部省份,土地採集費用平均為每公頃5萬美元,估價糾紛也屢見不鮮,往往導致計劃工期延長。因此,從規劃到運作的時間可能長達五至七年,增加了開發商的資金籌措風險,並降低了內部報酬率(IRR)。一個計劃於2024年推出的數位化一站式入口網站旨在縮短核准週期,但各機構的執行情況不盡相同。投資者目前會在預算中預留12至18個月的核准緩衝期,導致預算膨脹和收益延遲到帳。

細分市場分析

2026年至2031年,終端產業將以8.16%的複合年成長率成長,超過管線產業(截至2025年,管線產業是中國中游油氣市場的主要組成部分,佔45.12%)。浮體式再氣化裝置(FSRU)的引入縮短了建設週期,最大限度地減少了對沿海地區的干擾,從而能夠快速響應需求波動。沿海地區政府正在快速建造小規模終端,以實現卸貨點的多元化,從而緩解擁塞並抑制區域價格飆升。管道仍然是整個系統的基礎,連接著西部資源和俄羅斯進口油氣與東部消費量大的省份。人工智慧增強的監控系統可將管道營運和維護成本降低15-20%,並提高安全標準的執行情況,使其成為進一步擴容的理想平台。雖然倉儲設施的規模最小,但在強制性20%戰略儲備政策的推動下,資本支出正轉向枯竭油田的再開發和鹽穴的開採。總體而言,這些綜合基礎設施投資兼顧了進口柔軟性和運輸可靠性,確保了透過多條路線實現天然氣供應的穩定性。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大國內天然氣管道總長度

- 加速液化天然氣再氣化終端的建設

- 工業和住宅部門強制推行煤改氣。

- 推出人工智慧驅動的管道健康分析

- 液化天然氣動力重型卡車運輸的快速成長正在催生小規模規模的液化天然氣需求。

- 戰略天然氣儲存能力要求

- 市場限制

- 冗長的環境與土地使用許可流程

- 商品價格波動導致資本投資成本增加

- 運輸瓶頸增加了液化天然氣停泊成本

- 沿海水資源壓力限制了新建LNG接收站。

- 供應鏈分析

- 監管環境

- 技術展望

- 已安裝管道容量分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過基礎設施

- 管道

- 終端

- 倉儲設施(地下和地上)

- 依產品類型

- 原油

- 天然氣

- 石油產品

- LNG

- 按服務類型

- 管道建置

- 管道維護和維修

- 倉儲及搬運服務

- 運輸/物流

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、聯盟、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- China National Petroleum Corporation(CNPC)

- PipeChina(China Oil & Gas Pipeline Network Corp.)

- China Petroleum & Chemical Corporation(Sinopec Group)

- China National Offshore Oil Corporation(CNOOC)

- PetroChina Pipeline Company

- China Petroleum Pipeline Engineering Co.(CPP)

- Kunlun Energy

- ENN Natural Gas

- Towngas China

- China Gas Holdings

- Guanghui Energy

- Beijing Gas Group

- Shenzhen Gas Corp.

- Guangdong Dapeng LNG Company

- Tian Lun Gas Group

- Xinxing Ductile Iron Pipes Co.

- COSCO Shipping Energy Transportation

- Yantai LNG Co.

- Shanghai Gas Group

- Zhejiang Energy Group

第7章 市場機會與未來展望

China Oil And Gas Midstream Market market size in 2026 is estimated at USD 12.28 billion, growing from 2025 value of USD 11.71 billion with 2031 projections showing USD 15.55 billion, growing at 4.84% CAGR over 2026-2031.

The market growth is driven by Beijing's twin goals of energy security and carbon neutrality, which together prioritize infrastructure resilience, diversified supply routes, and measurable reductions in emissions. Surging natural gas demand from industrial and residential users, combined with steady domestic production, intensifies the need for additional transmission, import handling, and storage capacity. Policy-backed pipeline mileage expansion, accelerated LNG terminal commissioning, and mandatory strategic reserve targets create a sustained construction pipeline for contractors and equipment suppliers. Digitalization-especially AI-enabled monitoring-enhances asset utilization, reduces operating costs, and facilitates stricter environmental compliance, thereby further improving project economics.

China Oil And Gas Midstream Market Trends and Insights

Expansion of National Gas-Pipeline Mileage

China's 14th Five-Year Plan raises the transmission grid target to 120,000 km by 2025-a 25% jump over 2020-anchored by the West-to-East system. Redundant trunk lines mitigate the risk of single-point failure during geopolitical or technical disruptions and enhance cross-regional balancing. PipeChina's unified ownership accelerates interconnections, allowing flexible, bidirectional flows that lift utilization rates. The commissioning of the China-Russia East Route in 2024 diversified supply and reduced reliance on seaborne trade. Although cross-provincial land coordination is complex, centralized planning compresses build times once permits are clear. These projects present sizable opportunities for specialist contractors, high-specification pipe manufacturers, and digital monitoring solution providers.

Accelerated Build-out of LNG Regasification Terminals

Regas capacity hit 130 million tpa in 2024, with 40 million tpa under construction, positioning the country as the world's most active LNG-infrastructure builder. Smaller, distributed facilities mitigate supply bottlenecks that were revealed during the 2022 crisis, when large terminals faced congestion. Coastal governments are increasingly favoring FSRUs due to their rapid deployment speed, flexibility in capital expenditure, and reduced demand for onshore land. The 2024-commissioned Zhoushan III terminal reduced methane emissions by 15% through advanced vapor-recovery systems, setting a new domestic benchmark. Average 65% utilization leaves headroom for opportunistic spot cargo buying while serving strategic stockpiles. The segment thereby underpins import diversification and strengthens price-risk management.

Lengthy Environmental & Land-Use Permitting Process

Environmental reviews now last 18-36 months, with extra delays where routes cross ecologically sensitive zones. Land acquisition in the densely populated eastern provinces averages USD 50,000 per hectare, often triggering valuation disputes that prolong project timelines. As a result, planning-to-operation spans stretch 5-7 years, raising financing risk and slicing IRRs for developers. Digital one-stop portals unveiled in 2024 aim to condense review cycles, yet agency adoption is uneven. Investors now incorporate 12-18 month permitting buffers into their schedules, which inflates budgets and delays revenue generation.

Other drivers and restraints analyzed in the detailed report include:

- Coal-to-Gas Switching Mandates in Industrial & Residential Sectors

- AI-Driven Pipeline-Health Analytics Adoption

- Capex Escalation Amid Commodity-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Terminals accounted for an 8.16% CAGR growth between 2026 and 2031, outpacing pipelines, which retained a dominant 45.12% 2025 share of the China oil and gas midstream market size. FSRU rollouts shorten build cycles and limit shoreline disruption, enabling rapid response to demand shifts. Coastal governments are fast-tracking the development of smaller terminals to diversify landing points, thereby reducing congestion and regional price spikes. Pipelines still underpin system integrity, linking western resources and Russian imports with high-consumption eastern provinces. AI-enhanced monitoring reduced pipeline O&M costs by 15-20% and improved safety compliance, enhancing the platform's attractiveness for further capacity expansion. Storage facilities, although the smallest, gain policy momentum from the 20% strategic reserve mandate, shifting capital expenditures toward depleted field re-engineering and salt-cavern leaching. Collectively, blended infrastructure investments strike a balance between import flexibility and transmission reliability, thereby securing multi-path gas flow resilience.

The China Oil and Gas Midstream Market Report is Segmented by Infrastructure (Pipelines, Terminals, and Storage Facilities), Product Type (Crude Oil, Natural Gas, Refined Products, and LNG), and Service Type (Pipeline Construction, Pipeline Maintenance and Repair, Storage and Handling Services, and Transportation and Logistics). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- China National Petroleum Corporation (CNPC)

- PipeChina (China Oil & Gas Pipeline Network Corp.)

- China Petroleum & Chemical Corporation (Sinopec Group)

- China National Offshore Oil Corporation (CNOOC)

- PetroChina Pipeline Company

- China Petroleum Pipeline Engineering Co. (CPP)

- Kunlun Energy

- ENN Natural Gas

- Towngas China

- China Gas Holdings

- Guanghui Energy

- Beijing Gas Group

- Shenzhen Gas Corp.

- Guangdong Dapeng LNG Company

- Tian Lun Gas Group

- Xinxing Ductile Iron Pipes Co.

- COSCO Shipping Energy Transportation

- Yantai LNG Co.

- Shanghai Gas Group

- Zhejiang Energy Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of national gas-pipeline mileage

- 4.2.2 Accelerated build-out of LNG regasification terminals

- 4.2.3 Coal-to-gas switching mandates in industrial & residential sectors

- 4.2.4 AI-driven pipeline-health analytics adoption

- 4.2.5 Boom in LNG-fueled heavy-duty trucking creating small-scale LNG demand

- 4.2.6 Strategic gas storage capacity mandates

- 4.3 Market Restraints

- 4.3.1 Lengthy environmental & land-use permitting process

- 4.3.2 Capex escalation amid commodity-price volatility

- 4.3.3 Shipping chokepoints inflating landed LNG costs

- 4.3.4 Coastal water-stress limits on new LNG terminals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Installed Pipeline Capacity Analysis

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Infrastructure

- 5.1.1 Pipelines

- 5.1.2 Terminals

- 5.1.3 Storage Facilities (Underground and Above-ground)

- 5.2 By Product Type

- 5.2.1 Crude Oil

- 5.2.2 Natural Gas

- 5.2.3 Refined Products

- 5.2.4 LNG

- 5.3 By Service Type

- 5.3.1 Pipeline Construction

- 5.3.2 Pipeline Maintenance and Repair

- 5.3.3 Storage and Handling Services

- 5.3.4 Transportation and Logistics

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 China National Petroleum Corporation (CNPC)

- 6.4.2 PipeChina (China Oil & Gas Pipeline Network Corp.)

- 6.4.3 China Petroleum & Chemical Corporation (Sinopec Group)

- 6.4.4 China National Offshore Oil Corporation (CNOOC)

- 6.4.5 PetroChina Pipeline Company

- 6.4.6 China Petroleum Pipeline Engineering Co. (CPP)

- 6.4.7 Kunlun Energy

- 6.4.8 ENN Natural Gas

- 6.4.9 Towngas China

- 6.4.10 China Gas Holdings

- 6.4.11 Guanghui Energy

- 6.4.12 Beijing Gas Group

- 6.4.13 Shenzhen Gas Corp.

- 6.4.14 Guangdong Dapeng LNG Company

- 6.4.15 Tian Lun Gas Group

- 6.4.16 Xinxing Ductile Iron Pipes Co.

- 6.4.17 COSCO Shipping Energy Transportation

- 6.4.18 Yantai LNG Co.

- 6.4.19 Shanghai Gas Group

- 6.4.20 Zhejiang Energy Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment