|

市場調查報告書

商品編碼

1939045

生質燃料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Biofuels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

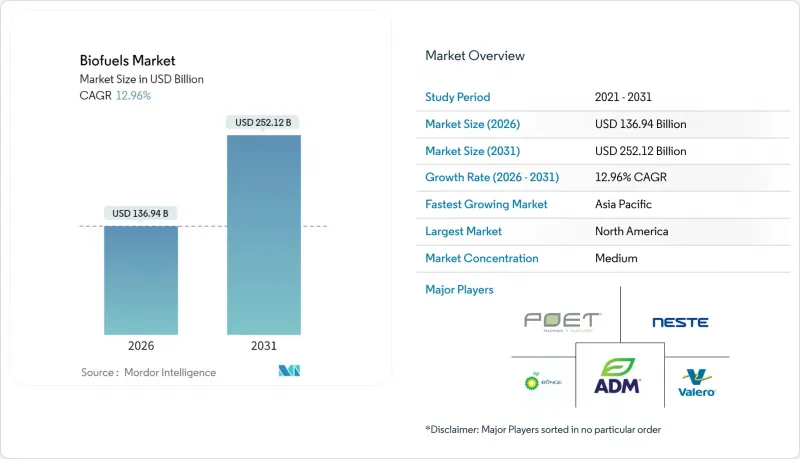

預計生質燃料市場規模將從 2025 年的 1,212.3 億美元成長到 2026 年的 1,369.4 億美元,到 2031 年將達到 2,521.2 億美元,2026 年至 2031 年的複合年成長率為 12.96%。

交通運輸領域(尤其是航空業)脫碳的壓力日益增大,加上大型石油公司的大規模投資,正在推動產能擴張,從而降低推廣應用的門檻。從第一代作物基燃料到廢棄物基和合成生物學解決方案的快速技術轉型,正在改善生命週期排放並降低原料風險。同時,北美政府的稅收優惠政策和亞洲的摻混規定,正在鼓勵簽訂長期承購協議,以穩定生產商的價格。主要企業宣布的43個煉油廠改造和新建設計劃預計到2030年將新增數百萬噸產能。這將加劇競爭,加速供應鏈重組,並縮小可再生和石化燃料之間的成本差距。

全球生質燃料市場趨勢及展望

加強亞洲和南美洲的混合運輸義務

亞洲和南美洲各國政府正在實施更高的生質柴油摻混比例,並調整原料分配和生產地點。光是印尼的B40計畫預計就能將生質柴油年消費量提高到1,315千萬公升,進而減少柴油進口,節省90億美元的外匯支出。印度正迅速推進2025年達到20%的乙醇摻混比例,同時鼓勵對蒸餾和物流設施的投資。菲律賓和泰國也正在推行類似的政策,而巴西則繼續維持其傳統的乙醇生產模式。這些政策有助於提高農村收入,降低原油進口成本,並透過建立可預測的需求來降低工廠擴張的風險。所有這些因素共同支撐著全球生質燃料市場的快速成長前景。

淨零排放購電協議推動北美對可再生柴油的需求

如今,各大物流和零售品牌均已簽訂多年採購協議,以確保獲得遠超監管最低標準的低碳燃料供應。 DHL集團與Neste公司合作,計劃到2030年每年採購30萬噸永續航空燃料(SAF)。加州低碳燃料標準(LCFS)允許參與企業兌換溫室氣體排放信用額度,其價值通常高於實際燃料價格,進一步改善長期經濟效益。這些企業承諾為生產商提供可預測的收入,並使其能夠獲得債務融資,用於在美國和加拿大各地建造新的加氫處理裝置。

原料價格(大豆、菜籽、廢棄食用油)的波動正在給生產商的利潤率帶來壓力。

預計到2024年,大豆油、廢食用油和牛油的價格波動幅度將達到40%至60%,這將擠壓煉油商的利潤空間,並使避險策略更加複雜。歐洲廢油進口中與詐欺相關的中斷推高了價格,同時也帶來了可追溯性的挑戰。生產商正透過多元化經營,轉向林業廢棄物和市政污泥等殘餘物來應對價格波動,但預處理過程需要資本投入且較為複雜。因此,短期盈利取決於原料來源組合的柔軟性以及強勁的信用市場,以抵消大宗商品價格波動的影響。

細分市場分析

永續航空燃料 (SAF) 的供應量雖然小規模,但正以 34.98% 的複合年成長率成長,這反映了航空公司即時的排放需求以及相關政策的支持。生質乙醇仍佔最大佔有率,這主要歸功於其在美國 E10 和巴西 E27 混合燃料中的廣泛應用。然而,加氫處理技術能夠聯產 SAF、可再生柴油和生物石腦油,這正推動資本朝向可直接替代現有管道生產的分子燃料轉移。

由於在寒冷氣候下與新型引擎系統有相容性問題,第二代生質柴油的成長已趨於平緩。與此同時,可再生柴油憑藉其更高的十六烷值和與化石柴油相媲美的基礎設施建設,市場佔有率正在擴大。生物丙烷等高附加價值產品進一步提升了計劃的經濟效益。因此,在其他產業需求的驅動下,全球生質燃料市場正轉向排碳權價值更高的燃料。

第一代生質燃料仍佔全球銷售額的67.62%,主要得益於巴西的甘蔗乙醇和美國的玉米乙醇。第一代生質燃料的全球市場規模預計將溫和成長,但隨著更先進技術的普及,其相對佔有率將會下降。第三代藻類生物燃料計劃目前年複合成長率達15.92%,這得益於基因工程和光生物反應器技術的進步,使得生產成本降低了兩位數。

近期大學研究表明,基因工程改造的微藻類可以將85%的廢油轉化為適用於加氫處理的脂質,從而有望減少土地利用問題。第二代纖維素生產設施,例如蘭扎捷航空的乙醇制永續航空燃料(SAF)工廠,最終實現了商業規模產能,並展現出更高的酵素效率。第四代合成生物學仍處於商業化前期階段,但已吸引創業投資資金,預計將實現直接利用捕獲的二氧化碳合成燃料。

生質燃料市場報告按燃料類型(生質乙醇、生質柴油、可再生柴油等)、世代(第一代、第三代等)、原料(糖料作物、澱粉作物、藻類等)、技術(發酵、酯交換、加氫處理等)、應用(道路運輸、航空、航運、發電和供熱)以及地區(北美、歐洲、亞太地區等)進行細分。

區域分析

預計到2025年,北美將佔全球生質燃料市場42.56%的佔有率,這主要得益於成熟的玉米乙醇工廠、大豆基可再生柴油的成長以及慷慨的稅額扣抵。到2025年,可再生柴油產能將加倍,達到52億加侖,而加州的低碳燃料標準(LCFS)將消耗掉幾乎全部的國內供應,從而形成穩定的價格底線。該地區政策的清晰性使生產商能夠快速資金籌措,而強大的糧食加工基礎設施則確保了原料的穩定供應。墨西哥近期延長了相關強制規定,加拿大也推出了無污染燃料法規,這些都將進一步提振該地區的需求。

在歐洲,《可再生能源指令III》設定了2030年可再生能源佔比達到42.5%的目標,並透過逐步淘汰棕櫚油作為原料來推動變革。德國將從2025年起禁止結轉上年度的溫室氣體排放排放權,迫使相關企業立即購買先進生質燃料。對中國生質柴油徵收反傾銷稅正在改變貿易路線,推高國產氫化植物油(HVO)的溢價,並鼓勵擴大本地產能。一系列複雜的政策組合正在推動技術創新,而原料供應的限制則將產量成長限制在適度水準。

亞太地區以16.78%的複合年成長率領先全球。印尼的B40強制性政策每年將吸收1,315千萬公升生質柴油,節省150億美元的外匯支出,同時提高小規模棕櫚油種植者的收入。印度計劃在2025年實現20%的乙醇混合燃料比例,將提振對穀物和糖蜜乙醇的需求,並為1000座壓縮沼氣廠創造市場。中國企業,例如BP投資嘉澳生物燃料公司規劃中的SAF生產線,顯示了其致力於航空業脫碳的決心。豐富的農業殘餘物、上行風險以及有利的財政獎勵,共同造就了亞洲在全球生質燃料市場中無可匹敵的成長引擎。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加強亞洲和南美洲交通運輸業的燃料摻混強制規定

- 淨零排放購電協議(PPA)推動了北美地區可再生柴油的需求。

- 歐盟和美國《通貨膨脹控制法案》中的永續航空燃料(SAF)稅收優惠

- 歐盟逐步淘汰棕櫚油基原料,推動對藻類和廢油的投資。

- 生物石腦油在石油化學原料脫碳領域的興起

- 市場限制

- 原料價格(大豆、菜籽、廢棄食用油)的波動正在給生產商的利潤率帶來壓力。

- 印度和印尼農業殘餘物收集的基礎設施瓶頸

- 歐洲間接土地利用變化(ILUC)的永續性上限

- 在遠距航空領域,與可直接取代的電子燃料競爭

- 供應鏈分析

- 監管和技術趨勢

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模和成長預測(價值和數量)

- 按燃料類型

- 生質乙醇

- 生質柴油(FAME)

- 可再生柴油/氫化植物油

- 永續航空燃料(SAF)

- 生物石腦油和其他可直接取代的生質燃料

- 按世代

- 第一代(醣類和澱粉)

- 第二代(纖維素基)

- 第三代(藻類基)

- 第四代(合成生物學/光生物學)

- 按原料

- 糖料作物(甘蔗、甜菜)

- 澱粉作物(玉米、小麥、木薯)

- 油籽(大豆、油菜籽、棕櫚)

- 廢棄食用油和動物脂肪

- 木質纖維素農業殘渣

- 藻類

- 透過技術

- 發酵

- 酯交換反應

- 加氫處理(HVO/SAF)

- 氣化和費托合成

- 熱解與重整

- 按最終用途

- 道路運輸

- 航空

- 船運

- 發電和供熱

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 丹麥

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 印尼

- 日本

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Abengoa Bioenergy SA

- Archer Daniels Midland Co.

- BP plc

- Cargill Inc.

- Chevron Renewable Energy Group Inc.

- Cosan SA/Raizen

- Eni SpA(Eni Sustainable Mobility)

- Gevo Inc.

- Green Plains Inc.

- LanzaTech Global Inc.

- Neste Oyj

- POET LLC

- Petrobras

- Shell plc

- TotalEnergies SE

- Valero Energy Corp.(Diamond Green Diesel)

- Verbio Vereinigte BioEnergie AG

- Wilmar International Ltd.

- Aemetis Inc.

- Amyris Inc.

- Clariant AG

- Enerkem Inc.

- Pacific Ethanol(Alto Ingredients)

- Orsted A/S(Power-to-X Bio-methanol)

- Pacific Biodiesel Technologies

第7章 市場機會與未來展望

The Biofuels market is expected to grow from USD 121.23 billion in 2025 to USD 136.94 billion in 2026 and is forecast to reach USD 252.12 billion by 2031 at 12.96% CAGR over 2026-2031.

Growing decarbonization mandates in transportation, especially aviation, and scaled investments from oil majors are driving capacity additions that ease adoption barriers. Rapid shifts in technology from first-generation crop-based fuels toward waste-derived and synthetic biology solutions are improving life-cycle emissions and reducing feedstock risk. At the same time, government tax credits in North America and blending mandates in Asia are prompting long-term offtake contracts that stabilize prices for producers. Competitive intensity is rising because 43 refinery conversion and greenfield projects announced by leading petroleum companies will add multimillion-ton capacity before 2030, reshaping supply chains and narrowing cost gaps between renewable and fossil fuels.

Global Biofuels Market Trends and Insights

Transport-sector blend mandates intensifying in Asia & South America

Asian and South American governments are implementing higher blending requirements, which are reshaping feedstock allocation and production footprints. Indonesia's B40 program alone lifts biodiesel consumption to 13.15 million kiloliters annually, cutting diesel imports and saving USD 9 billion in foreign exchange. India is fast-tracking its move to 20% ethanol blending by 2025, which drives parallel investment in distillation and logistics assets. Similar policies in the Philippines and Thailand add regional momentum, while Brazil keeps its long-standing ethanol platform. These mandates support rural incomes, curb crude import bills, and establish predictable demand that de-risks plant expansions. Together, they underpin the steep growth outlook for the global biofuels market.

Net-zero-aligned corporate PPAs driving renewable diesel demand in North America

Major logistics and retail brands now sign multiyear purchase agreements that guarantee low-carbon fuel supply beyond regulatory minimums. DHL Group intends to source 300,000 tons of SAF annually by 2030 under a partnership with Neste . California's Low Carbon Fuel Standard enables participating firms to monetize greenhouse-gas credits, which are often valued above the physical fuel price, thereby further sweetening long-term economics. These corporate commitments provide producers with clearer revenue visibility, enabling them to secure debt financing for new hydrotreatment units across the United States and Canada.

Volatile Feedstock Prices (Soy, Rapeseed, UCO) Squeezing Producer Margins

Soybean oil, used cooking oil, and tallow prices swung 40-60% during 2024, eroding margins and complicating hedge strategies for refiners. Fraud-related disruptions in European waste-oil imports inflated prices while creating challenges to traceability. Producers are countering volatility by diversifying into residues such as forestry waste and municipal sludges, although preprocessing adds capital cost and complexity. Near-term profitability, therefore, depends on agile feedstock portfolios and robust credit markets that offset commodity swings.

Other drivers and restraints analyzed in the detailed report include:

- SAF tax incentives in the EU & U.S. Inflation Reduction Act

- Palm feedstock phase-out prompting algae & waste-oil investment in Europe

- Infrastructure bottlenecks in collecting agri-residues in India & Indonesia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sustainable aviation fuel volumes scale from a small base at a 34.98% CAGR, reflecting airlines' need for immediate emissions cuts and supportive mandates. Bioethanol retains the lion's share because it is entrenched in U.S. E10 and Brazilian E27 blends. Yet hydrotreatment's ability to co-produce SAF, renewable diesel, and bio-naphtha is shifting capital toward drop-in molecules that fit existing pipelines.

Second-generation biodiesel is plateauing because of compatibility issues with newer engine systems in cold climates. In contrast, renewable diesel gains market share thanks to its superior cetane numbers and parity with fossil diesel in terms of infrastructure. High-value co-products such as bio-propane further enhance project economics. The global biofuels market is therefore shifting toward fuels with cross-sector appeal and higher carbon credit valuation.

First-generation fuels still account for 67.62% of sales, driven primarily by sugarcane ethanol in Brazil and corn ethanol in the United States. The global biofuels market size for first-generation pathways is expected to rise modestly; however, the relative share will decline as advanced options scale. Third-generation algae projects now demonstrate 15.92% CAGR after genetics and photobioreactor advances cut production costs by double digits.

Recent university studies show that engineered microalgae can convert 85% of waste oil into lipids suitable for hydrotreatment, thereby reducing land-use concerns. Second-generation cellulosic facilities, such as LanzaJet's ethanol-to-SAF plant, are finally hitting commercial throughput and proving enzyme efficiency gains. Fourth-generation synthetic biology remains pre-commercial but attracts venture funding because it promises direct fuel synthesis from captured CO2.

The Biofuels Market Report is Segmented by Fuel Type (Bioethanol, Biodiesel, Renewable Diesel, and More), Generation (First-Generation, Third-Generation, and More), Feedstock (Sugar Crops, Starch Crops, Algae, and More), Technology (Fermentation, Trans-Esterification, Hydrotreatmen, and More), End-Use (Road Transport, Aviation, Marine, and Power Generation and Heating), and Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America is expected to control 42.56% of the global biofuels market in 2025, driven by mature corn ethanol plants, the growth of soybean oil-based renewable diesel, and generous tax credits. Installed renewable diesel capacity doubles to 5.2 billion gallons by 2025, and California's LCFS consumes nearly the entire domestic pool, creating a stable price floor. The region's policy clarity enables producers to secure financing quickly, while robust grain handling infrastructure ensures a stable feedstock flow. Mexico's recent mandate extensions and Canada's clean fuel regulations further enlarge regional demand.

Europe is transforming as the Renewable Energy Directive III sets a 42.5% renewable energy target by 2030 and phases out the use of palm oil feedstocks. Germany banned carry-over of prior-year greenhouse-gas certificates starting in 2025, forcing obligated parties to purchase more advanced biofuels immediately. Anti-dumping duties on Chinese biodiesel reroute trade and raise premiums for domestic HVO, encouraging local capacity additions. The complex policy mix fosters technological innovation while keeping volume growth moderate due to feedstock constraints.

Asia-Pacific posts the highest regional CAGR at 16.78%. Indonesia's B40 mandate absorbs 13.15 million kiloliters of biodiesel annually and saves USD 15 billion in foreign exchange, while supporting the incomes of smallholder palm farmers . India's march toward 20% ethanol by 2025 boosts demand for grain and molasses ethanol and seeds the market for 1,000 compressed-biogas plants. China's joint ventures, such as BP's stake in Jiaao's upcoming SAF line, signal intent to decarbonize aviation. Ample agricultural residues, rising oil-price exposure, and supportive fiscal incentives combine to make Asia an unrivaled growth engine for the global biofuels market.

- Abengoa Bioenergy SA

- Archer Daniels Midland Co.

- BP p.l.c.

- Cargill Inc.

- Chevron Renewable Energy Group Inc.

- Cosan S.A. / Raizen

- Eni S.p.A. (Eni Sustainable Mobility)

- Gevo Inc.

- Green Plains Inc.

- LanzaTech Global Inc.

- Neste Oyj

- POET LLC

- Petrobras

- Shell p.l.c.

- TotalEnergies SE

- Valero Energy Corp. (Diamond Green Diesel)

- Verbio Vereinigte BioEnergie AG

- Wilmar International Ltd.

- Aemetis Inc.

- Amyris Inc.

- Clariant AG

- Enerkem Inc.

- Pacific Ethanol (Alto Ingredients)

- Orsted A/S (Power-to-X Bio-methanol)

- Pacific Biodiesel Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transport-sector Blend Mandates Intensifying in Asia & South America

- 4.2.2 Net-Zero-Aligned Corporate PPAs Driving Renewable Diesel Demand in North America

- 4.2.3 SAF (Sustainable Aviation Fuel) Tax Incentives in the EU & U.S. Inflation Reduction Act

- 4.2.4 Phasing-Out of Palm-based Feedstocks Prompting Algae & Waste-Oil Investments in EU

- 4.2.5 Emergence of Bio-naphtha for Petro-Chem Feedstock Decarbonisation

- 4.3 Market Restraints

- 4.3.1 Volatile Feedstock Prices (Soy, Rapeseed, UCO) Squeezing Producer Margins

- 4.3.2 Infrastructure Bottlenecks in Collecting Agri-Residues in India & Indonesia

- 4.3.3 Indirect Land-Use-Change (ILUC) Sustainability Caps in Europe

- 4.3.4 Competition from Drop-in e-Fuels in Long-haul Aviation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Fuel Type

- 5.1.1 Bioethanol

- 5.1.2 Biodiesel (FAME)

- 5.1.3 Renewable Diesel / HVO

- 5.1.4 Sustainable Aviation Fuel (SAF)

- 5.1.5 Bio-naphtha and Other Drop-in Biofuels

- 5.2 By Generation

- 5.2.1 First-Generation (Sugar & Starch)

- 5.2.2 Second-Generation (Cellulosic)

- 5.2.3 Third-Generation (Algae-based)

- 5.2.4 Fourth-Generation (Synthetic Biology/Photobiological)

- 5.3 By Feedstock

- 5.3.1 Sugar Crops (Sugarcane, Sugar Beet)

- 5.3.2 Starch Crops (Corn, Wheat, Cassava)

- 5.3.3 Oilseeds (Soy, Rapeseed, Palm)

- 5.3.4 Used Cooking Oil and Animal Fat

- 5.3.5 Lignocellulosic Agri-Residues

- 5.3.6 Algae

- 5.4 By Technology

- 5.4.1 Fermentation

- 5.4.2 Trans-esterification

- 5.4.3 Hydrotreatment (HVO/SAF)

- 5.4.4 Gasification and FT-Synthesis

- 5.4.5 Pyrolysis and Upgrading

- 5.5 By End-use Sector

- 5.5.1 Road Transport

- 5.5.2 Aviation

- 5.5.3 Marine

- 5.5.4 Power Generation and Heating

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Denmark

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Indonesia

- 5.6.3.4 Japan

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Abengoa Bioenergy SA

- 6.4.2 Archer Daniels Midland Co.

- 6.4.3 BP p.l.c.

- 6.4.4 Cargill Inc.

- 6.4.5 Chevron Renewable Energy Group Inc.

- 6.4.6 Cosan S.A. / Raizen

- 6.4.7 Eni S.p.A. (Eni Sustainable Mobility)

- 6.4.8 Gevo Inc.

- 6.4.9 Green Plains Inc.

- 6.4.10 LanzaTech Global Inc.

- 6.4.11 Neste Oyj

- 6.4.12 POET LLC

- 6.4.13 Petrobras

- 6.4.14 Shell p.l.c.

- 6.4.15 TotalEnergies SE

- 6.4.16 Valero Energy Corp. (Diamond Green Diesel)

- 6.4.17 Verbio Vereinigte BioEnergie AG

- 6.4.18 Wilmar International Ltd.

- 6.4.19 Aemetis Inc.

- 6.4.20 Amyris Inc.

- 6.4.21 Clariant AG

- 6.4.22 Enerkem Inc.

- 6.4.23 Pacific Ethanol (Alto Ingredients)

- 6.4.24 Orsted A/S (Power-to-X Bio-methanol)

- 6.4.25 Pacific Biodiesel Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Next-Gen Electro-Bio-Refineries Integrating Green H2

生質燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按形態、應用、原料、區域和競爭格局分類,2021-2031年

生質燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按形態、應用、原料、區域和競爭格局分類,2021-2031年 生質燃料生產市場:預測(至2034年)-按生質燃料類型、生產流程、原料、形態、最終用戶和地區分類的全球分析

生質燃料生產市場:預測(至2034年)-按生質燃料類型、生產流程、原料、形態、最終用戶和地區分類的全球分析 生質燃料市場:2026-2032年全球市場預測(依生質燃料類型、製造流程、形態、原料類型、應用、最終用途及通路分類)

生質燃料市場:2026-2032年全球市場預測(依生質燃料類型、製造流程、形態、原料類型、應用、最終用途及通路分類) 生質燃料市場:依原料類型、燃料類型、應用、生產技術、終端用戶產業及地區分類乳化燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、分銷管道、應用和最終用戶分類)

生質燃料市場:依原料類型、燃料類型、應用、生產技術、終端用戶產業及地區分類乳化燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、分銷管道、應用和最終用戶分類) 單細胞油市場規模、佔有率、成長及全球產業分析:按類型和應用、區域洞察及2026-2034年預測

單細胞油市場規模、佔有率、成長及全球產業分析:按類型和應用、區域洞察及2026-2034年預測 燃油品質感測器-全球市場佔有率和排名、總銷售量和需求預測(2026-2032 年)

燃油品質感測器-全球市場佔有率和排名、總銷售量和需求預測(2026-2032 年) 2026年全球生質燃料催化劑市場研究報告

2026年全球生質燃料催化劑市場研究報告 交通運輸用生質燃料的市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。全球交通運輸用生質燃料市場:規模、佔有率、趨勢和成長分析報告(2026-2034年)

交通運輸用生質燃料的市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。全球交通運輸用生質燃料市場:規模、佔有率、趨勢和成長分析報告(2026-2034年)