|

市場調查報告書

商品編碼

1982324

交通運輸用生質燃料的市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Transportation Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

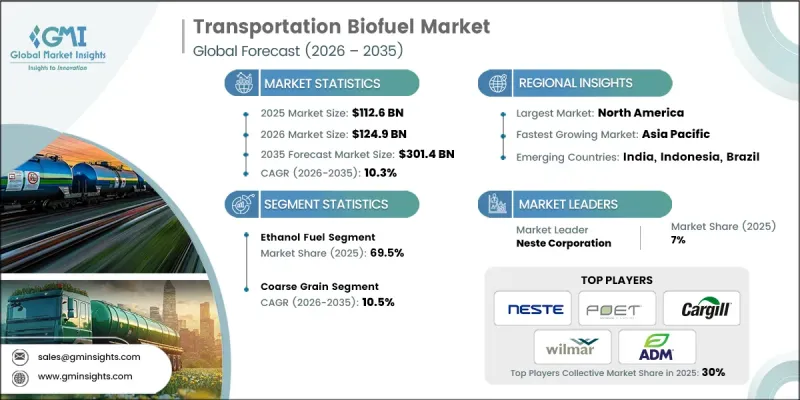

預計到 2025 年,全球運輸生質燃料市場價值將達到 1,126 億美元,並預計以 10.3% 的複合年成長率成長,到 2035 年達到 3,014 億美元。

主要市場的政策框架正從寬泛的可再生能源目標轉向具體的燃料強制性規定,將生質燃料納入交通運輸產業的長期脫碳策略。這種轉變在航空、道路運輸以及日益重要的海運領域尤其顯著,這些領域透過合格規則和永續性標準來界定哪些燃料需要遵守監管規定。隨著各國實施這些框架,專門的報告系統、註冊系統和預設值正在創造一個規則主導的環境,從而支持對先進生質燃料和可再生替代燃料的投資。由於液態能源的替代能源有限,永續航空燃料(SAF)已成為航空業成長的主要驅動力。關於最低混合要求和永續性標準的監管確定性正在推動煉油廠的改造、協同加工舉措和新計畫的開展。航空公司、機場和燃料供應商正在採用綜合採購、認證和預訂索賠(B&C)機制。隨著SAF從試驗計畫過渡到常規供應,長期供應協議、產能擴張和原料多樣化正在經核准的生產管道中加速推進。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1126億美元 |

| 預測金額 | 3014億美元 |

| 複合年成長率 | 10.3% |

預計到2025年,乙醇產業將佔據69.5%的市場佔有率,並在2035年之前以10.5%的複合年成長率成長。這一成長主要得益於農業政策、煉油廠整合以及交通運輸領域脫碳獎勵的協同效應,這些措施鼓勵降低碳辛烷值。各國政府持續擴大乙醇摻混義務和適用原料的範圍,汽車製造商正在檢驗其產品是否適用於高濃度混合燃料,而燃料零售商則在增加供應以降低推廣門檻。生產商正投資於製程最佳化、降低碳排放強度以及提升產品特定價值,以在不斷變化的碳計量框架下增強自身競爭力。

預計到2025年,粗粒穀物乙醇市佔率將達到37.8%,到2035年將以10.5%的複合年成長率成長。其地理分佈廣泛且儲量豐富的供應來源、成熟的轉化技術以及可預測的產品特定經濟效益,使粗粒穀物成為乙醇生態系統的核心組成部分。儘管輕型車輛的電氣化程度不斷提高,但由於粗粒穀物乙醇有助於提高辛烷值、具有廣泛的車輛相容性,並且有望成為未來生物中間體和電子燃料前體的生產平台,因此它在汽油市場中仍然扮演著重要的結構性角色。

美國運輸生質燃料市場佔93%的佔有率,預計2025年市場規模將達到339億美元。這得益於健全的合規體系、成熟的供應鏈以及對全生命週期性能的重視。美國可再生燃料標準(RFS)透過信用市場、路線合格和年度標準為生產商和混合商提供支持,從而促進對纖維素乙醇、運輸沼氣、低碳乙醇和生物柴油的投資。聯邦和地方政府計畫正不斷完善永續性指標,推動製程效率提升、碳排放強度降低、熱能利用整合、碳捕獲能力建設以及原料多樣化。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

- 新機會與趨勢

- 數位化和物聯網整合

- 進入新興市場

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭性標竿分析

- 戰略儀錶板

- 創新與科技趨勢

第5章 市場規模及預測:依燃料類型分類,2022-2035年

- 生質柴油

- 乙醇

- 其他

第6章 市場規模及預測:依原料分類,2022-2035年

- 粗粒顆粒

- 糖料作物

- 植物油

- 其他

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 西班牙

- 英國

- 義大利

- 亞太地區

- 中國

- 印度

- 印尼

- 澳洲

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第8章:公司簡介

- ADM

- Borregaard

- BTG Bioliquids

- Cargill

- Chevron Corporation

- Clariant

- COFCO

- FutureFuel

- Inpasa

- Munzer Bioindustrie

- My Eco Energy

- Neste Corporation

- POET

- Praj Industries

- The Andersons

- TotalEnergies

- UPM

- Verbio

- Wilmar International

- Zilor

The Global Transportation Biofuel Market was valued at USD 112.6 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 301.4 billion by 2035.

Policy frameworks across key markets are evolving from broad renewable targets to precise fuel mandates that embed biofuels into long-term transport decarbonization strategies. This transition is evident across aviation, road transport, and increasingly maritime sectors, where eligibility rules and sustainability criteria define which fuels qualify for compliance. As nations implement these frameworks, professionalized reporting, registry systems, and default values create a rules-driven environment that supports investment in advanced biofuels and renewable drop-in fuels. Sustainable aviation fuel (SAF) is a major growth driver, given the limited alternatives to liquid energy in aviation. Regulatory certainty around minimum blending requirements and sustainability standards is encouraging refinery conversions, co-processing initiatives, and greenfield projects. Airlines, airports, and fuel suppliers are adopting integrated procurement, certification, and book-and-claim mechanisms. As SAF moves from pilot programs to routine supply, long-term offtake agreements, capacity expansion, and feedstock diversification are accelerating across approved production pathways.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $112.6 Billion |

| Forecast Value | $301.4 Billion |

| CAGR | 10.3% |

The ethanol segment held 69.5% share in 2025 and is expected to grow at a CAGR of 10.5% through 2035. Growth is driven by the convergence of agricultural policy, refinery integration, and transport decarbonization incentives rewarding low-carbon octane. Governments continue expanding blending mandates and eligible feedstocks, while automakers validate higher blend compatibility and fuel retailers increase availability, reducing adoption barriers. Producers are investing in process optimization, carbon intensity reduction, and coproduct valorization to enhance competitiveness under evolving carbon accounting frameworks.

The coarse grain segment accounted for 37.8% share in 2025 and is projected to grow at a CAGR of 10.5% by 2035. Its large, geographically diversified supply, mature conversion technologies, and predictable coproduct economics make coarse grains central to the ethanol ecosystem. Despite growing electrification in light-duty fleets, coarse-grain ethanol maintains a structural role in gasoline pools due to octane contribution, broad vehicle compatibility, and potential as a platform for future bio-intermediates and e-fuel precursors.

U.S. Transportation Biofuel Market held 93% share, generating USD 33.9 billion in 2025, driven by a robust compliance framework, mature supply chains, and focus on lifecycle performance. The U.S. Renewable Fuel Standard (RFS) underpins producer and blender behavior through credit markets, pathway eligibility, and annual standards, supporting investment in cellulosic ethanol, biogas for transport, and low-carbon ethanol and biodiesel. Federal and subnational programs increasingly refine sustainability measurement, promoting process efficiency, carbon intensity reduction, heat integration, carbon capture readiness, and feedstock diversification.

Key players in the Global Transportation Biofuel Market include Neste Corporation, POET, ADM, Praj Industries, Borregaard, FutureFuel, My Eco Energy, Wilmar International, Clariant, TotalEnergies, BTG Bioliquids, Chevron Corporation, Cargill, UPM, Inpasa, Verbio, The Andersons, Munzer Bioindustrie, COFCO, and Zilor. Companies in the Global Transportation Biofuel Market are employing multiple strategies to solidify their market position. They are investing in R&D to optimize conversion efficiency, reduce carbon intensity, and expand eligible feedstocks. Strategic partnerships with OEMs, fuel distributors, and aviation stakeholders enhance market access and long-term offtake agreements. Firms are also modernizing production infrastructure, adopting co-processing and integrated refinery approaches, and expanding geographically to capture emerging demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Feedstock trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive benchmarking

- 4.4 Strategic dashboard

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million, Mtoe)

- 5.1 Key trends

- 5.2 Biodiesel

- 5.3 Ethanol

- 5.4 Others

Chapter 6 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million, Mtoe)

- 6.1 Key trends

- 6.2 Coarse grain

- 6.3 Sugar crop

- 6.4 Vegetable oil

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Mtoe)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ADM

- 8.2 Borregaard

- 8.3 BTG Bioliquids

- 8.4 Cargill

- 8.5 Chevron Corporation

- 8.6 Clariant

- 8.7 COFCO

- 8.8 FutureFuel

- 8.9 Inpasa

- 8.10 Munzer Bioindustrie

- 8.11 My Eco Energy

- 8.12 Neste Corporation

- 8.13 POET

- 8.14 Praj Industries

- 8.15 The Andersons

- 8.16 TotalEnergies

- 8.17 UPM

- 8.18 Verbio

- 8.19 Wilmar International

- 8.20 Zilor

2034年農業生質燃料市場預測:按燃料類型、原料、技術、應用、最終用戶和地區分類的全球分析

2034年農業生質燃料市場預測:按燃料類型、原料、技術、應用、最終用戶和地區分類的全球分析 生質燃料市場:2026-2032年全球市場預測(依生質燃料類型、原料類型、生產流程、形態、混合比例、最終用途及通路分類)

生質燃料市場:2026-2032年全球市場預測(依生質燃料類型、原料類型、生產流程、形態、混合比例、最終用途及通路分類) 2026年全球燃油品質分析儀市場報告生物合成燃料市場預測至2034年—按燃料類型、原料、技術、應用、最終用戶和地區分類的全球分析

2026年全球燃油品質分析儀市場報告生物合成燃料市場預測至2034年—按燃料類型、原料、技術、應用、最終用戶和地區分類的全球分析 生質燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按形態、應用、原料、區域和競爭格局分類,2021-2031年生質燃料生產市場:預測(至2034年)-按生質燃料類型、生產流程、原料、形態、最終用戶和地區分類的全球分析

生質燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按形態、應用、原料、區域和競爭格局分類,2021-2031年生質燃料生產市場:預測(至2034年)-按生質燃料類型、生產流程、原料、形態、最終用戶和地區分類的全球分析 生質燃料市場:依原料類型、燃料類型、應用、生產技術、終端用戶產業及地區分類乳化燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、分銷管道、應用和最終用戶分類)乙醇生質燃料市場:依原料、應用和地區分類

生質燃料市場:依原料類型、燃料類型、應用、生產技術、終端用戶產業及地區分類乳化燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、分銷管道、應用和最終用戶分類)乙醇生質燃料市場:依原料、應用和地區分類 燃油品質感測器-全球市場佔有率和排名、總銷售量和需求預測(2026-2032 年)

燃油品質感測器-全球市場佔有率和排名、總銷售量和需求預測(2026-2032 年)