|

市場調查報告書

商品編碼

1938994

滑石粉:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Talc - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

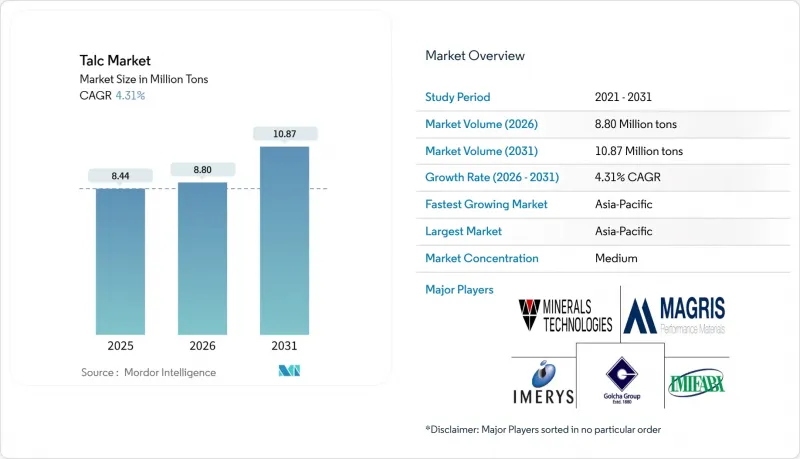

預計滑石粉市場將從 2025 年的 807 萬噸成長到 2026 年的 842 萬噸,到 2031 年將達到 1,039 萬噸,2026 年至 2031 年的複合年成長率為 4.29%。

電動車產量不斷成長、包裝永續性目標日益嚴格以及水性塗料的廣泛應用,正推動滑石粉市場穩步成長。含有高長寬比滑石粉的輕質聚丙烯複合材料正在取代玻璃纖維,應用於電動車內裝板和電池外殼。同時,食品飲料生產商也開始採用公認安全(GRAS)滑石粉作為天然加工助劑。伊梅里斯公司對其年產3.5萬噸蕪湖工廠的投資,體現了其對特定應用產品的專注。此外,透過礦石分選技術提高資源利用率,也幫助生產者應對日益嚴格的法規所帶來的成本壓力。

全球滑石市場趨勢及展望

電動車和電動出行對輕質聚合物的需求

汽車製造商正以滑石粉增強複合材料取代玻璃纖維增強聚丙烯,旨在透過降低成本和密度,在保持剛度的同時,實現15-25%的減重。滑石粉市場正受益於高長寬比)滑石粉,這種滑石粉可用於製造更薄、尺寸穩定的內裝板和電池機殼。伊梅里斯(Imerys)的HAR產品採用經過最佳化的片狀結構,可提高拉伸模量。電動車平台(包括需要保持負載容量的商用貨車)在全球的普及,正在擴大特殊滑石粉的需求量。中國和美國的零排放法規進一步推動了這一趨勢。因此,擁有混煉技術和聚丙烯配方專業知識的供應商正在滑石粉市場中獲得更高的利潤。

亞洲向水性建築塗料的轉變

中國和印度日益嚴格的低VOC法規正促使塗料製造商轉向水性塗料,而水性塗料需要滑石粉來控制黏度並提高遮蓋力。表面處理過的滑石粉可防止顏料懸浮和沈澱,保持光澤,同時為二氧化鈦提供了經濟高效的替代品。預計這些改質滑石粉將推動滑石粉市場價格上漲20-30%,儘管研磨和加工成本增加,但利潤率仍將提升。東南亞地區不斷加快的都市化和新房住宅量正在推動對中檔建築塗料的需求。在該地區設有工廠的跨國塗料製造商正與能夠可靠滿足分散規格要求的滑石粉供應商簽訂長期承購協議。

石棉相關訴訟的遺留問題

強生公司提案的80億至100億美元的和解方案凸顯了持續存在的責任風險,並繼續抑制了化妝品級滑石粉的需求。美國食品藥物管理局(FDA)新的強制性檢測規定增加了中小型加工商的合規成本。食品藥物管理局基於職業暴露將滑石粉重新歸類為“致癌性致癌物”,導致對其的審查力度加大。這些因素共同導致滑石粉市場分化為兩類供應商:一類是進行全面礦物學篩檢的供應商,另一類則被限制在工業細分市場。保險費持續上漲,進一步擠壓了利潤空間。

細分市場分析

到2025年,碳酸滑石將佔據滑石市場61.92%的佔有率,成為該細分市場的主要驅動力。這主要得益於印度和中國豐富的碳酸蘊藏量,以及適合高通量通用級滑石的加工成本結構。儘管綠泥石的供應有限,但由於其熱穩定性,綠泥石的複合年成長率仍高達4.76%,使其適用於汽車引擎室零件和電子產品。利用機械化學活化技術的供應商可以根據客戶規格調整表面能和粒度比例,使來自獲利能力較低的礦床的碳酸鹽礦石也能在中端應用領域佔有一席之地。此外,投資噴射磨機技術將粗粒原料轉化為亞2微米粉末(高光澤塗料的必要原料)也至關重要。

對超細和微層狀滑石形態的持續研究和開發正在模糊傳統礦床類型之間的界限,有可能使碳酸鹽礦在某些應用中取代綠泥石礦。然而,關於殘餘礦物含量的監管阻力使得富含綠泥石的滑石礦對要求低雜質的原始設備製造商(OEM)更具吸引力。因此,滑石市場呈現雙軌發展趨勢:成本主導的碳酸鹽礦主導著大批量應用,而價值主導的綠泥石礦則在高階細分市場中佔據越來越大的佔有率。

本滑石市場報告按礦床類型(碳酸鹽滑石和亞氯酸鹽滑石)、終端用戶行業(塑膠和橡膠、油漆和塗料、陶瓷、紙漿和造紙、個人護理和化妝品、食品和飲料以及其他行業)和地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行分析。市場預測以公噸為單位。

區域分析

預計到2025年,亞太地區將佔全球滑石粉市場規模的53.10%,並在2031年之前以5.18%的複合年成長率成長。這主要得益於印度在全球滑石粉產量中佔比高達25%,以及連接中國加工商和下游塑膠出口商的完善供應鏈。中國、日本和韓國的電動車製造需要超細滑石粉母粒,從而確保了對高長寬比滑石粉的本地需求。同時,儘管監管趨勢傾向於低揮發性有機化合物(VOC)配方,但東南亞的建築熱潮仍然推高了塗料級滑石粉的需求。

北美具有重要的戰略意義,OEM廠商的輕量化措施推動了優質滑石粉的消費。然而,消費者對化妝品中滑石粉的謹慎態度,以及新礦開採面臨環境核准障礙,預計將限制市場成長,使其僅為個位數。天氣相關的供應中斷凸顯了風險,下游買家正在將採購來源分散到多個地區,以確保滑石粉市場的穩定供應。

在歐洲,針對結晶質二氧化矽的更嚴格法規以及擬議的REACH法規修訂預計將增加檢測成本,並修訂工業用戶的採購標準。德國和法國的買家已經開始要求進行ESG(環境、社會和管治)審核,預計這將增加對低碳供應來源的需求。儘管南美、中東和非洲的建築和消費品生產正在成長,但分散的物流和本地加工能力的不足仍然是限制區域市場擴張的因素。瞄準這些地區的投資者通常會與現有的歐洲或亞洲加工商成立合資企業,以確保技術訣竅。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車和電動出行對輕質聚合物的需求

- 亞洲向水性建築塗料的轉變

- 食品級滑石粉在膠基和肉類塗層的應用

- 利用人工智慧技術進行礦石分選,提高礦石回收率。

- 用於符合ESG目標採購的低碳滑石粉

- 市場限制

- 與石棉相關的訴訟的法律遺留問題

- 生物基填充材替代滑石粉用於高檔紙張

- 芬蘭罷工後,歐洲高品位礦石短缺

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按礦床類型

- 滑石和碳酸鹽

- 滑石綠泥石

- 按最終用戶行業分類

- 塑膠和橡膠

- 油漆和塗料

- 陶瓷

- 紙漿和造紙

- 個人護理及化妝品

- 食品/飲料

- 其他行業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AKJ MinChem

- ANAND TALC

- Chanda Minerals

- CIMBAR PERFORMANCE MINERALS

- euroMinerals GmbH

- Golcha Group

- Hayashi-Kasei

- Imerys

- IMI Fabi SpA

- LITHOS Industrial Minerals GmbH

- Magris Performance Materials

- Minerals Technologies Inc.

- Nippon Talc Co., Ltd.

- Sibelco

第7章 市場機會與未來展望

The Talc market is expected to grow from 8.07 million tons in 2025 to 8.42 million tons in 2026 and is forecast to reach 10.39 million tons by 2031 at 4.29% CAGR over 2026-2031.

Rising electric-vehicle production, stricter packaging sustainability targets, and a broad shift to water-based coatings keep the talc market on a steady upward path. Lightweight polypropylene compounds containing high-aspect-ratio talc grades are replacing glass fiber in electric vehicle (EV) interior panels and battery housings, while food and beverage firms are adopting Generally Recognized as Safe (GRAS)-certified talc as a natural processing aid. Investments such as Imerys' 35,000 tpa Wuhu plant underline the emphasis on application-specific products. Simultaneously, ore-sorting technology is lifting resource utilization, helping producers offset cost pressures tied to tightening regulatory frameworks.

Global Talc Market Trends and Insights

Light-weighting Demand from EV and E-mobility Polymers

Automakers are targeting 15-25% weight cuts by substituting glass-fiber polypropylene with talc-reinforced compounds that preserve stiffness while trimming cost and density. The talc market benefits because high-aspect-ratio grades support thinner, dimensionally stable interior panels and battery enclosures. Imerys' HAR products emphasize engineered plate-like morphologies optimized for tensile modulus improvement. Global EV platform proliferation, including commercial vans that demand payload retention, extends the addressable tonnage for specialty talc grades. Government zero-emission mandates in China and the U.S. further anchor this momentum. Suppliers with compounding knowledge and polypropylene formulation expertise thus capture premium margins in the talc market.

Shift to Water-based Architectural Paints in Asia

Stricter low-VOC rules in China and India push formulators toward water-borne coatings that need talc for viscosity control and hiding power. Surface-treated talc prevents pigment flooding and sedimentation, enabling cost-effective substitution for titanium dioxide while keeping gloss intact. The talc market sees 20-30% price uplifts for these modified grades, creating margin headroom despite higher grinding and treatment expenses. Urbanization across Southeast Asia is swelling new housing starts, expanding demand for mid-tier architectural paints. Multinational paint companies with regional plants are securing long-term offtake agreements with talc suppliers that can meet dispersion specifications reliably.

Litigation Legacy of Asbestos-related Claims

Johnson & Johnson's proposed USD 8-10 billion settlement underscores persistent liability overhang and keeps cosmetic-grade demand subdued. The FDA has outlined new mandatory testing rules, escalating compliance costs for smaller processors. The WHO's reclassification of talc to "probably carcinogenic" based on occupational exposure intensifies scrutiny. Collectively, these factors split the talc market between suppliers with full-spectrum mineralogical screening and those relegated to industrial niches. Insurance premiums continue to climb, further narrowing margins.

Other drivers and restraints analyzed in the detailed report include:

- Food-grade Talc Uptake in Gum Base and Meat Coatings

- AI-enabled Ore-sorting Boosting Ore Recovery Rates

- Bio-based Fillers Replacing Talc in Premium Papers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Talc carbonate led the segment with 61.92% of the Talc market size in 2025, benefiting from abundant reserves in India and China and a processing cost structure that favors high-throughput commodity grades. Talc chlorite, though less available, is gaining traction at a 4.76% CAGR because its thermal stability suits under-hood automotive and electronics parts. Suppliers exploiting mechanochemical activation now tailor surface energy and particle aspect ratio to user specifications, enabling carbonate ore from marginal deposits to compete in mid-range applications. Investment in jet-mill fine grinding is equally pivotal, turning coarse feedstock into sub-2 µm powders critical for high-gloss coatings.

Continued R&D on ultrafine, micro-lamellar morphologies blurs traditional boundaries between deposit types, letting carbonate mines displace chlorite grades in some roles. Yet, regulatory headwinds related to residue mineral content make chlorite-rich ore attractive for OEMs demanding low impurities. The talc market, therefore, tracks a dual trajectory: cost-driven carbonate volumes dominate mass applications, while value-driven chlorite captures incremental share in premium niches.

The Talc Market Report is Segmented by Deposit Type (Talc Carbonate and Talc Chlorite), End-User Industry (Plastics and Rubber, Paints and Coatings, Ceramics, Pulp and Paper, Personal Care and Cosmetics, Food and Beverage, and Other Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 53.10% of the Talc market size in 2025 and is projected to grow at a 5.18% CAGR through 2031, supported by India's 25% global production share and integrated supply chains linking Chinese processors to downstream plastics exporters. Domestic EV manufacturing in China, Japan, and South Korea requires ultrafine talc masterbatches, ensuring local offtake for high-aspect-ratio grades. Simultaneously, booming construction in Southeast Asia increases paint-grade demand despite regulatory moves toward low-VOC (Volatile Organic Compound) formulations.

North America remains strategically important, with original equipment manufacturer (OEM) lightweighting initiatives sustaining premium-grade consumption. Nonetheless, cautious consumer sentiment around talc cosmetics and environmental approval hurdles for new mines hold growth to mid-single digits. Weather-induced disruptions highlight supply risks, prompting downstream buyers to diversify procurement across multiple regions to stabilize talc market access.

Europe's stricter crystalline silica protocols and pending REACH revisions will likely raise testing costs and reshape purchasing criteria for industrial users. Buyers in Germany and France already request Environmental, Social, and Governance (ESG) audits, boosting prospects for low-carbon supply streams. South America and the Middle East & Africa show rising construction and consumer-goods output, yet fragmented logistics and limited local processing still constrain regional talc market scalability. Investors targeting these regions often form joint ventures with established European or Asian processors to lock in technological know-how.

- AKJ MinChem

- ANAND TALC

- Chanda Minerals

- CIMBAR PERFORMANCE MINERALS

- euroMinerals GmbH

- Golcha Group

- Hayashi-Kasei

- Imerys

- IMI Fabi SpA

- LITHOS Industrial Minerals GmbH

- Magris Performance Materials

- Minerals Technologies Inc.

- Nippon Talc Co., Ltd.

- Sibelco

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Light-weighting Demand from EV and E-mobility Polymers

- 4.2.2 Shift to Water-based Architectural Paints in Asia

- 4.2.3 Food-grade Talc Uptake in Gum Base and Meat Coatings

- 4.2.4 AI-enabled Ore-sorting Boosting Ore Recovery Rates

- 4.2.5 Low-carbon talc Grades for ESG-scoped Procurement

- 4.3 Market Restraints

- 4.3.1 Litigation Legacy of Asbestos-related Claims

- 4.3.2 Bio-based Fillers Replacing Talc in Premium Papers

- 4.3.3 High-purity Ore Shortages in Europe Post-Finnish Strike

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Deposit Type

- 5.1.1 Talc Carbonate

- 5.1.2 Talc Chlorite

- 5.2 By End-user Industry

- 5.2.1 Plastics and Rubber

- 5.2.2 Paints and Coatings

- 5.2.3 Ceramics

- 5.2.4 Pulp and Paper

- 5.2.5 Personal Care and Cosmetics

- 5.2.6 Food and Beverage

- 5.2.7 Other Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AKJ MinChem

- 6.4.2 ANAND TALC

- 6.4.3 Chanda Minerals

- 6.4.4 CIMBAR PERFORMANCE MINERALS

- 6.4.5 euroMinerals GmbH

- 6.4.6 Golcha Group

- 6.4.7 Hayashi-Kasei

- 6.4.8 Imerys

- 6.4.9 IMI Fabi SpA

- 6.4.10 LITHOS Industrial Minerals GmbH

- 6.4.11 Magris Performance Materials

- 6.4.12 Minerals Technologies Inc.

- 6.4.13 Nippon Talc Co., Ltd.

- 6.4.14 Sibelco

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球滑石粉市場

全球滑石粉市場 葉蠟石市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地區和競爭格局分類,2021-2031年

葉蠟石市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地區和競爭格局分類,2021-2031年 滑石市場預測至2034年—按類型、礦床類型、應用和地區分類的全球分析

滑石市場預測至2034年—按類型、礦床類型、應用和地區分類的全球分析 滑石粉市場:依形態、等級、純度、應用及通路分類-2026-2032年全球市場預測

滑石粉市場:依形態、等級、純度、應用及通路分類-2026-2032年全球市場預測 滑石市場報告:礦床類型、形態、終端用途產業及地區分類,2026-2034年

滑石市場報告:礦床類型、形態、終端用途產業及地區分類,2026-2034年 2026-2034年全球葉蠟石市場規模、佔有率、趨勢和成長分析報告日本滑石市場規模、佔有率、趨勢和預測:按礦床類型、形態、最終用途行業和地區分類,2026-2034年

2026-2034年全球葉蠟石市場規模、佔有率、趨勢和成長分析報告日本滑石市場規模、佔有率、趨勢和預測:按礦床類型、形態、最終用途行業和地區分類,2026-2034年 2026年全球滑石市場報告超細滑石粉市場按等級、終端用途行業、應用和通路- 全球預測 2026-2032

2026年全球滑石市場報告超細滑石粉市場按等級、終端用途行業、應用和通路- 全球預測 2026-2032 葉蠟石:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

葉蠟石:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)