|

市場調查報告書

商品編碼

1937428

越南電動車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

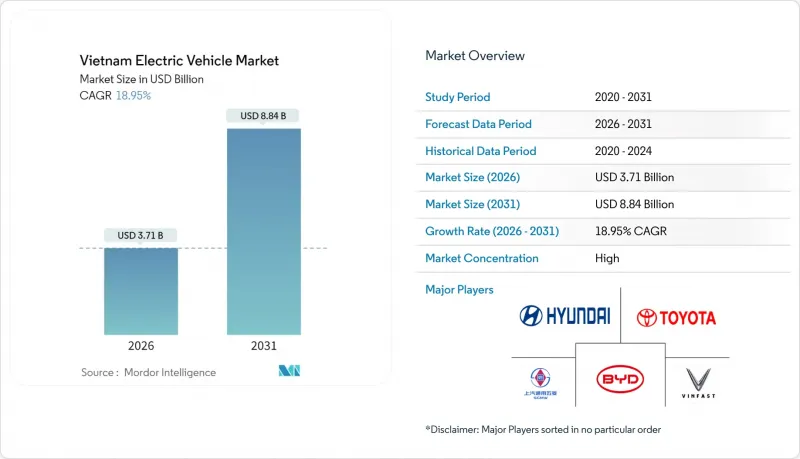

預計到 2026 年,越南電動車市場規模將達到 37.1 億美元,高於 2025 年的 31.2 億美元。

預計到 2031 年,該市場規模將達到 88.4 億美元,2026 年至 2031 年的複合年成長率為 18.95%。

政府設定的2030年都市區電動車普及率達到50%、2050年達到淨零排放的明確目標,推動了市場需求。 VinFast的本土化策略、外資OEM廠商的建廠計畫以及優惠的電價政策,共同降低了電動車的整體擁有成本,加速了其普及。摩托車電動化的快速推進提升了消費者的環保意識,共用充電基礎設施也正在向汽車市場擴展。同時,電池組價格的下降使得磷酸鐵鋰電池技術在對成本較為敏感的細分市場中成為主流。由於VinFast的市場主導地位抑制了價格戰,市場競爭格局相對平靜。但隨著中國品牌和全球大眾市場OEM廠商攜具有成本競爭力的車型進入市場,整個生態系統正朝著車型多元化和價格下降的方向發展。

越南電動車市場趨勢與洞察

擴大國內生產

VinFast的目標是到2026年達到80%的國產化率,到2027年年產量達到50萬輛,到2030年達到100萬輛。這項擴張將降低零件成本並減外匯風險。奇瑞和吉利的協同努力鞏固了越南作為區域組裝中心的地位,但先進的電子元件和電池管理系統仍然依賴進口。 VinFast的銷售保障合約為本地供應商提供了需求可見性,從而鼓勵新的資本投資並加速在地化進程。

政府激勵措施和稅收優惠

此獎勵方案將免除電動車的註冊費至2027年2月,並對東協地區生產的電動車維持零進口關稅,使每輛車的購置成本降低超過1億越南盾。優惠的充電費用(2204越南盾/千瓦時)進一步降低了電動車的總擁有成本。此外,地方政府還採取了其他措施,例如為胡志明市提案的40萬輛摩托車改裝計畫提供稅收減免和低利率貸款,這些措施凸顯了多層次的政策協調。 2027年後的持續性取決於能否實現成本平價,這使得市場面臨財政政策連續性的風險。

公共充電基礎設施不足

雖然主要城市的公車系統覆蓋全面,但遍遠地區的公車密度迅速下降,限制了城際出行和200公里以下路段以外的公車路線發展。 V-Green計畫撥款4.04億美元用於興建更多公車站,但由於前置作業時間較長,短期內仍將面臨瓶頸問題。高峰用電月份電網壓力日益加劇,促使政府下令優先保障電力供應的韌性。

細分市場分析

2025年,乘用車將佔越南汽車市場總規模的67.65%,其中公車市場成長最快,大規模年成長率將達33.11%。在地方政府政策競標下,越南電動公車市場預計將在2025年至2028年間翻倍。雖然目前私人用戶佔據了大部分市場佔有率,但商業用戶將成為推動市場成長的主要力量。胡志明市計劃在37條線路上引入電動公車,河內計劃在市中心實現公車100%電動化,這些舉措都帶來了巨大且可預測的需求。

商業用戶將率先採用者新一代電池技術和快速充電解決方案,因為更高的車隊利用率意味著更高的整體擁有成本優勢。同時,二輪車仍將受到城鄉通勤者需求的推動,這透過提升充電站的經濟效益,間接促進了四輪車的普及。在預測期內,儘管乘用車銷量成長,但其市場佔有率預計將溫和下降,因為巴士和廂型車將在政策主導,在公共交通和最後一公里物流領域獲得更大的佔有率。

截至2025年,電池式電動車(BEV)在越南電動車市場佔有70.82%的佔有率,超過了混合動力汽車和插電混合動力汽車。隨著政府推行動力傳動系統轉型跨越式發展策略,純電動車的銷售量預計將以27.85%的複合年成長率成長,進一步鞏固其市場主導地位。混合動力汽車在需要續航里程柔軟性的郊區通勤者中佔有一席之地,但與純電動車的稅收不平等限制了其成長。由於基礎設施不足,燃料電池汽車仍處於試驗階段。

VinFast 專注於純電動車的產品策略正在塑造消費者的認知,而全國範圍內的充電補貼政策也進一步強化了純電動車的形象。儘管外國製造商可能會推出插電式混合動力汽車來緩解里程焦慮,但政策方向仍然傾向於將純電動車視為主流。同時,電池技術的進步正在縮短充電時間,消除了過去混合動力汽車價格溢價所面臨的實際限制。整體而言,越南電動車產業正堅持直接向純電動車轉型,避免了已開發市場逐步轉向混合動力汽車的趨勢。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大國內生產規模(VinFast 和進口車)

- 政府補助和稅收優惠

- 日益增強的環保意識和淨零排放目標

- 對電動摩托車生態系統的連鎖反應

- 電池組價格下降

- 優惠電動車充電收費系統

- 市場限制

- 公共充電基礎設施不足

- 相對於平均收入而言,購車的初始成本較高

- 中階機型有限

- 尖峰時段電力系統容量限制

- 價值/價值鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 電動車充電基礎設施建設

第5章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 按車輛類型

- 搭乘用車

- 商用車輛

- 摩托車

- 公車

- 透過推進力

- 電池式電動車(BEV)

- 插電式混合動力電動車(PHEV)

- 混合動力電動車(HEV)

- 燃料電池電動車(FCEV)

- 按里程

- 不到200公里

- 200~400km

- 超過400公里

- 依電池類型

- LFP

- NMC/NCA

- 其他

- 最終用戶

- 個人所有

- 商用車輛/叫車服務

- 政府和公共交通

- 按地區

- 越南北部

- 越南中部

- 越南南部

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- VinFast Motor Ltd.

- Hyundai Motor Corporation

- Toyota Motor Corporation

- BYD Auto Co. Ltd

- SAIC-GM-Wuling Automobile Co., Ltd.

- Tesla Inc.

- Mercedes-Benz Group AG

- Kia Corporation

- Nissan Motor Co. Ltd

- Honda Motor Co. Ltd

- MG Motor(China)

- Chery Automobile Co.

- Great Wall Motor(Haval)

- Volvo Car AB

- Selex Motors(VN)

- Dat Bike(VN)

- Foxconn EV Charging(VN)

- VinES Battery(VN)

- ABB Vietnam(Chargers)

- Delta Electronics(VN)

第7章 市場機會與未來展望

The Vietnam electric vehicle market size in 2026 is estimated at USD 3.71 billion, growing from 2025 value of USD 3.12 billion with 2031 projections showing USD 8.84 billion, growing at 18.95% CAGR over 2026-2031.

Demand is propelled by firm government targets that mandate 50% EV penetration in urban areas by 2030 and net-zero emissions by 2050. VinFast's localization drive, foreign OEM factory commitments, and preferential electricity tariffs collectively reduce the total cost of ownership, amplifying adoption. Rapid two-wheeler electrification creates consumer familiarity and shared charging infrastructure that spills over to four-wheelers, while falling battery pack prices allow LFP technology to dominate value-conscious segments. Competition remains moderate because VinFast's dominance deters price wars, yet Chinese brands and global mass-market OEMs are entering with cost-competitive models, nudging the ecosystem toward wider model variety and lower pricing.

Vietnam Electric Vehicle Market Trends and Insights

Domestic Manufacturing Scale-up

VinFast aims for 80% domestic content by 2026, with a goal to produce 500,000 vehicles by 2027 and reach 1 million vehicles annually by 2030, a scale that compresses component costs and mitigates exchange-rate exposure. Complementary commitments from Chery and Geely reinforce Vietnam's standing as a regional assembly hub, yet sophisticated electronics and battery management systems remain import-reliant. Guaranteed offtake contracts from VinFast give local suppliers demand visibility, prompting new capital investment that accelerates localisation.

Government Incentives and Tax Rebates

The incentive package waives registration fees for EVs until February 2027 and keeps import duties at zero on ASEAN-built cars, trimming purchase prices by more than VND 100 million per unit. Preferential charging tariffs of 2,204 VND/kWh further tilt the total cost of ownership in favor of electric models. Provincial add-ons, such as Ho Chi Minh City's proposed tax holidays and soft loans for its 400,000-unit motorcycle conversion program, underscore multi-tier policy coordination. Continuity beyond 2027 depends on reaching cost parity, exposing the market to fiscal-policy rollover risk.

Sparse Public Charging Infrastructure

Although dense in tier-one cities, the network thins rapidly in rural corridors, restricting inter-city travel and segment growth beyond sub-200 km models. V-Green has earmarked USD 404 million to deploy additional stations, yet lead times mean near-term bottlenecks persist. Grid stress surfaces during high-demand months, prompting government directives that prioritize power supply resilience.

Other drivers and restraints analyzed in the detailed report include:

- Rising Environmental Awareness and Net-zero Targets

- Electric Two-wheeler Ecosystem Spill-over

- High Up-front Vehicle Cost vs Average Income

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars contributed 67.65% of overall revenue in 2025, while buses registered the quickest expansion at a 33.11% CAGR. The Vietnam electric vehicle market size for buses is projected to double between 2025 and 2028 as provincial mandates trigger large tender volumes. Private car buyers account for much of today's stock, yet commercial fleets tip the growth curve; Ho Chi Minh City's 37-route electric bus roll-out and Hanoi's 100% core-area bus electrification agenda inject predictable bulk demand.

Intense fleet utilisation magnifies total-cost benefits, making commercial buyers early adopters of newer battery chemistries and fast-charging solutions. Conversely, two-wheelers retain vitality through rural-urban commuter demand, indirectly bolstering charging-hub economics that benefit four-wheeler deployment. Over the forecast horizon, passenger-car share will erode modestly even as volumes rise, because buses and vans gain policy-driven ground in public transit and last-mile logistics.

Battery electric vehicles captured 70.82% of the Vietnam electric vehicle market share in 2025, eclipsing hybrid and plug-in alternatives. That dominance deepens as BEV volumes compound at 27.85% CAGR, propelled by a government strategy that leapfrogs transitional powertrains. Hybrids hold niche appeal for peri-urban commuters needing range flexibility, but a lack of tax parity with BEVs caps growth. Fuel-cell vehicles remain experimental due to infrastructure voids.

VinFast's single-minded BEV product map shapes consumer perception, while nationwide charging subsidies reinforce the pure-electric narrative. Foreign OEMs may inject plug-in variants to hedge range anxiety, yet policy signals keep BEVs on the mainstream trajectory. In tandem, battery advancements shorten charging times, shaving practical limitations that once justified hybrid premiums. Altogether, the Vietnam electric vehicle industry stays on a direct-to-BEV path, avoiding the incremental hybrid detour seen in developed markets.

The Vietnamese Electric Vehicle Market Report is Segmented by Vehicle Type (Passenger Cars, Commercial Vehicles, and More), Propulsion (Battery Electric Vehicles, Plug-In Hybrid Electric Vehicles, and More), Driving Range (Below 200 Km, 200 To 400 Km, and More), Battery Type (Private Ownership, and More), and Region (Northern Vietnam, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- VinFast Motor Ltd.

- Hyundai Motor Corporation

- Toyota Motor Corporation

- BYD Auto Co. Ltd

- SAIC-GM-Wuling Automobile Co., Ltd.

- Tesla Inc.

- Mercedes-Benz Group AG

- Kia Corporation

- Nissan Motor Co. Ltd

- Honda Motor Co. Ltd

- MG Motor (China)

- Chery Automobile Co.

- Great Wall Motor (Haval)

- Volvo Car AB

- Selex Motors (VN)

- Dat Bike (VN)

- Foxconn EV Charging (VN)

- VinES Battery (VN)

- ABB Vietnam (Chargers)

- Delta Electronics (VN)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Domestic manufacturing scale-up (VinFast and imports)

- 4.2.2 Government incentives and tax rebates

- 4.2.3 Rising environmental awareness and net-zero targets

- 4.2.4 Electric two-wheeler ecosystem spill-over

- 4.2.5 Falling battery pack prices

- 4.2.6 Preferential EV-charging tariff structure

- 4.3 Market Restraints

- 4.3.1 Sparse public charging infrastructure

- 4.3.2 High up-front vehicle cost vs average income

- 4.3.3 Limited mid-range model availability

- 4.3.4 Grid capacity constraints at peak hours

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 EV Charging Infrastructure Development

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.1.3 Two-Wheelers

- 5.1.4 Buses

- 5.2 By Propulsion

- 5.2.1 Battery Electric Vehicles (BEV)

- 5.2.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 5.2.3 Hybrid Electric Vehicles (HEV)

- 5.2.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.3 By Driving Range

- 5.3.1 Below 200 km

- 5.3.2 200 to 400 km

- 5.3.3 Above 400 km

- 5.4 By Battery Type

- 5.4.1 LFP

- 5.4.2 NMC/NCA

- 5.4.3 Others

- 5.5 By End User

- 5.5.1 Private Ownership

- 5.5.2 Commercial Fleet/Ride-Hailing

- 5.5.3 Government and Public Transport

- 5.6 By Region

- 5.6.1 Northern Vietnam

- 5.6.2 Central Vietnam

- 5.6.3 Southern Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 VinFast Motor Ltd.

- 6.4.2 Hyundai Motor Corporation

- 6.4.3 Toyota Motor Corporation

- 6.4.4 BYD Auto Co. Ltd

- 6.4.5 SAIC-GM-Wuling Automobile Co., Ltd.

- 6.4.6 Tesla Inc.

- 6.4.7 Mercedes-Benz Group AG

- 6.4.8 Kia Corporation

- 6.4.9 Nissan Motor Co. Ltd

- 6.4.10 Honda Motor Co. Ltd

- 6.4.11 MG Motor (China)

- 6.4.12 Chery Automobile Co.

- 6.4.13 Great Wall Motor (Haval)

- 6.4.14 Volvo Car AB

- 6.4.15 Selex Motors (VN)

- 6.4.16 Dat Bike (VN)

- 6.4.17 Foxconn EV Charging (VN)

- 6.4.18 VinES Battery (VN)

- 6.4.19 ABB Vietnam (Chargers)

- 6.4.20 Delta Electronics (VN)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

電動車虛擬原型製作市場:按組件、技術、部署模式、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測

電動車虛擬原型製作市場:按組件、技術、部署模式、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測 2026年全球V2B(車輛到建築)電力市場報告

2026年全球V2B(車輛到建築)電力市場報告 全電動多用途貨車市場規模、佔有率和成長分析:按產能、應用、終端用戶產業、地區和產業預測,2026-2033年

全電動多用途貨車市場規模、佔有率和成長分析:按產能、應用、終端用戶產業、地區和產業預測,2026-2033年 長續航里程電動車市場規模、佔有率和成長分析:按車輛類型、電池類型、充電基礎設施、續航里程、消費群體、動力系統、功率輸出和地區分類-2026-2033年產業預測

長續航里程電動車市場規模、佔有率和成長分析:按車輛類型、電池類型、充電基礎設施、續航里程、消費群體、動力系統、功率輸出和地區分類-2026-2033年產業預測 800V電動車架構市場規模、佔有率和成長分析:按車輛、架構、充電方式、組件、應用和地區分類-2026-2033年產業預測

800V電動車架構市場規模、佔有率和成長分析:按車輛、架構、充電方式、組件、應用和地區分類-2026-2033年產業預測 電動車售後市場規模、佔有率和成長分析:按零件類型、車輛類型、服務類型、動力系統、銷售管道、最終用戶、地區和產業預測,2026-2033年

電動車售後市場規模、佔有率和成長分析:按零件類型、車輛類型、服務類型、動力系統、銷售管道、最終用戶、地區和產業預測,2026-2033年 電動車(零能耗汽車)市場規模、佔有率和成長分析:按車輛類型、電源管理方法、充電基礎設施、電池技術、最終用戶和地區分類-產業預測(2026-2033 年)

電動車(零能耗汽車)市場規模、佔有率和成長分析:按車輛類型、電源管理方法、充電基礎設施、電池技術、最終用戶和地區分類-產業預測(2026-2033 年) 2026-2030年全球電動車市場

2026-2030年全球電動車市場 歐洲電動車市場:依動力類型(純電動車 (BEV)、燃料電池電動車 (FCEV)、插電式混合動力車 (PHEV)、混合動力車 (HEV))、功率輸出(100kW 以下、100kW-250kW)、應用(個人用途、商業用途)和地區劃分 - 全球預測至 2036 年

歐洲電動車市場:依動力類型(純電動車 (BEV)、燃料電池電動車 (FCEV)、插電式混合動力車 (PHEV)、混合動力車 (HEV))、功率輸出(100kW 以下、100kW-250kW)、應用(個人用途、商業用途)和地區劃分 - 全球預測至 2036 年 中國電動車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

中國電動車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)