|

市場調查報告書

商品編碼

1939662

中國電動車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)China Electric Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

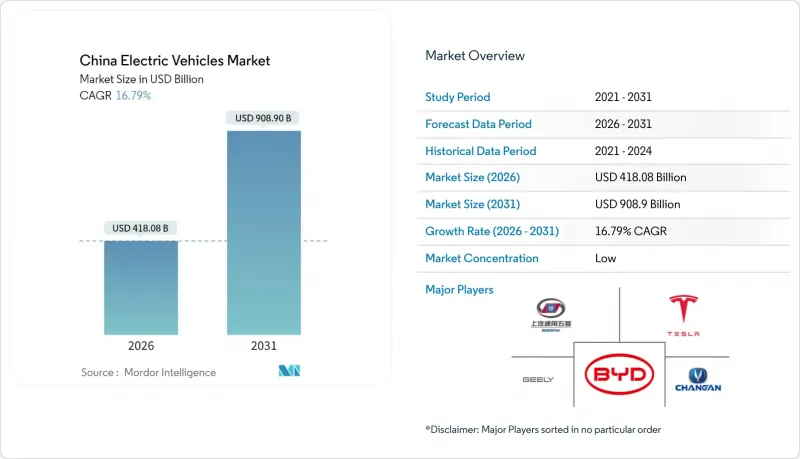

預計到 2026 年,中國電動車市場規模將達到 4,180.8 億美元,高於 2025 年的 3,579.8 億美元。

預計到 2031 年,該市場規模將達到 9,089 億美元,2026 年至 2031 年的複合年成長率為 16.79%。

電池成本趨於均等化、全國充電和換電基礎設施建設以及插電式混合動力汽車在二三線城市的強勁成長勢頭,是推動中國電動汽車銷量成長的主要因素。同時,為因應價格競爭導致的利潤率下滑,汽車製造商也正在加速推進電池化學領域的垂直整合和創新。隨著基礎設施投資的增加和磷酸鐵鋰電池成本的提升,中國電動車市場有望進一步滲透對價格敏感的農村市場。

中國電動車市場趨勢與展望

新能源汽車購置稅免稅政策延長至2027年

每輛車1,390美元至4,175美元的稅收減免將有助於緩解補貼結束後過渡期的困難,並保持入門車型的價格競爭力。二、三線城市的消費者對這些優惠政策反應熱烈,預計2024年新能源汽車銷售中有三分之一將同時享有稅收減免和以舊換新優惠。政策的可預測性也使汽車製造商能夠更好地規劃產能擴張和中期車型調整。這點在中檔跨界車領域尤其明顯,而中檔跨界車正是中國電動車銷售的主要驅動力。

建立全國快速充電和電池更換網路

過去幾年,公共充電樁數量激增,寧德時代和中石化已建成500座換電站,換電站換電週期僅兩分鐘。高速公路網路覆蓋率已達服務區的60%,但57%的充電樁仍集中在15個城市,西部省份仍有發展空間。這種雙軌制的基礎設施策略既滿足了通勤者的充電需求,也保障了車隊的運作,增強了市場對中國電動車市場的信心。

中央政府補貼逐步取消減緩了升級週期

隨著補貼政策於2022年12月結束,購車獎勵減少了1,670元至2,780元,讓中階轎車的價格更加敏感。汽車製造商透過提供折扣和區域性置換計劃來應對,但這延長了更換週期。隨著電池投入成本的下降,對直接補貼的依賴將會降低,預計中國電動車市場的自然更換節奏將逐漸恢復正常。

細分市場分析

到2025年,純電動車(BEV)將主導中國電動車市場,佔交車量的57.72%。同時,插電式混合動力汽車(PHEV)預計到2031年將以20.88%的複合年成長率成長,隨著基礎設施向內陸地區擴展,兩者之間的差距將逐漸縮小。在充電樁稀缺的地區,由於其雙燃料的柔軟性,插電式混合動力汽車正成為駕駛者首選的過渡技術。

純電動車成本的持續下降將使純電動車型對小型車和計程車車隊保持吸引力,而插電式混合動力車在家用SUV和鄉村轎車領域的成長正在推動動力傳動系統多樣化。汽車製造商正在使其架構多樣化,而固態電池專案則著眼於2030年後的高階純電動車市場浪潮。

到2025年,乘用車將佔中國電動車市場的87.60%,而輕型商用車的複合年成長率將達到18.20%。市政零排放配額、樞紐輻射式物流以及電池更換的經濟效益,使得電動輕型商用車成為可靠的車隊資產。

受消費者為追求更大車內空間而升級換代以及公車業者為響應地方政府低排放法規而更換柴油車輛的雙重推動,SUV市場呈現14.85%的複合年成長率。商用領域的廣泛應用也進一步推高了電池需求,使中國電動車市場規模超越了個人交通領域。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場促進因素

- 新能源汽車購置稅免稅政策延長至2027年

- 建立全國快速充電和電池更換網路

- 插電式混合動力車因其省油效果而備受推崇,在二、三線城市地區迅速普及。

- 地方政府電動貨車配額政策提振了對輕型商用電動車的需求。

- 透過V2G試點定價創造車網互動收入來源

- 使用磷酸鐵鋰電池實現與小型內燃機汽車的成本持平

- 市場限制

- 由於中央政府補貼逐步取消,升級週期放緩

- 碳酸鋰價格波動和出口限制

- 省級層級限制低運轉率公共充電樁的數量

- 新能源汽車品質問題日益增多(JD Power IQS調查),正在削弱客戶忠誠度。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 電池化學的發展趨勢

- 波特五力模型

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(以金額為準,2024-2030 年)

- 透過驅動系統

- 電池式電動車

- 插電式混合動力電動車

- 燃料電池電動車

- 按車輛類型

- 搭乘用車

- 掀背車

- 轎車

- SUV

- MPV

- 商用車輛

- 輕型商用車

- 巴士和長途汽車

- 中型和大型卡車

- 搭乘用車

- 電池化學

- LFP

- NCM/NMC

- NCA

- 其他

- 按價格範圍

- 不到1萬美元

- 10,000 美元至 20,000 美元

- 20,000美元至30,000美元

- 30,000 美元至 50,000 美元

- 超過5萬美元

第6章 競爭情勢

- 策略趨勢

- 市佔率分析

- 公司簡介

- BYD Company Ltd

- SAIC-GM-Wuling

- Tesla Inc.

- Geely Auto Group

- Changan Automobile

- Great Wall Motors

- BAIC Motor Corp.

- SAIC Motor Corp. Ltd.

- Dongfeng Motor Corp.

- FAW Group

- GAC Aion

- NIO Inc.

- Xpeng Motors

- Li Auto

- Leapmotor

- Hozon Auto(Neta)

- Zeekr Intelligent Tech.

- Seres Group

- Jiangling Motors Corp.

- JAC Motors

- Chery Automobile

第7章 市場機會與未來展望

The China Electric Vehicles Market size in 2026 is estimated at USD 418.08 billion, growing from 2025 value of USD 357.98 billion with 2031 projections showing USD 908.9 billion, growing at 16.79% CAGR over 2026-2031.

Battery cost parity, a nationwide charging and battery-swap build-out, and tier-2/3 city PHEV momentum reinforce volume expansion. Automakers are also accelerating vertical integration and battery chemistry innovation to secure falling margins amid price wars. Infrastructure investment and cost-competitive LFP batteries position the Chinese electric vehicle market for further penetration into price-sensitive rural segments.

China Electric Vehicles Market Trends and Insights

Extended NEV Purchase-Tax Exemptions to 2027

Tax-free status worth USD 1,390-4,175 per vehicle cushions the post-subsidy transition and keeps entry-level pricing competitive. Tier-2/3 customers react strongly to this saving, and one-third of 2024 NEV sales leveraged the exemption plus trade-in incentives. Predictable policy horizons let automakers schedule capacity ramps and mid-cycle refreshes, particularly for mid-market crossovers driving the volume of China's electric vehicles.

Nationwide Fast-Charging & Battery-Swap Corridor Build-Out

Public charging points rose drastically over the past few years, while CATL and Sinopec are placing 500 battery-swap stations capable of two-minute exchanges. Highway coverage now spans 60% of service areas, and 57% of chargers remain clustered within 15 cities, signalling headroom in western provinces. The twin-track infrastructure strategy addresses commuter top-up needs and fleet uptime demands, underpinning confidence in the Chinese electric vehicle market.

Phase-Out of Central Subsidies Slowing Upgrade Cycles

The December 2022 subsidy sunset trimmed purchase incentives by RMB 1,670-2,780, elevating price sensitivity in mid-market sedans. Automakers countered with rebates and regional trade-in schemes, yet replacement intervals lengthened. As battery input costs drop, reliance on direct subsidies is expected to fade, restoring natural replacement rhythms within the Chinese electric vehicle market.

Other drivers and restraints analyzed in the detailed report include:

- PHEV Surge in Tier-2/3 Cities on Fuel-Savings Appeal

- Municipal E-Freight Quotas Boosting Electric LCV Demand

- Lithium-Carbonate Price & Export-Control Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery electric vehicles led 2025 deliveries with a 57.72% share, anchoring the China electric vehicle market size for that year. Plug-in hybrids, however, are forecast to post a 20.88% CAGR to 2031, narrowing the gap as infrastructure diffuses inland. Dual-fuel flexibility makes PHEVs the preferred bridge tech for drivers facing sparse chargers.

Continued BEV cost erosion keeps fully electric models appealing in subcompacts and taxi fleets, yet PHEV growth in family SUVs and rural sedans diversifies the powertrain mix. Manufacturers, therefore, hedge across architectures, while solid-state programs target the post-2030 premium BEV wave.

Passenger cars captured 87.60% of China's electric vehicle market share in 2025, but light commercial vans are rising on an 18.20% CAGR trajectory. Municipal zero-emission quotas, hub-and-spoke logistics, and battery-swap economics make electric LCVs a reliable fleet asset.

SUVs show 14.85% CAGR as consumers trade up for cabin space, and bus operators refresh diesel fleets under local low-emission mandates. Commercial adoption reinforces battery demand curves and broadens China's electric vehicle market size beyond private mobility.

The China Electric Vehicle Market Report is Segmented by Drivetrain Type (Battery Electric Vehicles, Plug-In Hybrid Electric Vehicles, and More), Vehicle Type (Passenger Cars [Hatchback and More] and Commercial Vehicles [Light Commercial Vehicles and More]), Battery Chemistry (LFP, NCM/NMC, and More), and Price Band (Less Than USD 10, 000 and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- BYD Company Ltd

- SAIC-GM-Wuling

- Tesla Inc.

- Geely Auto Group

- Changan Automobile

- Great Wall Motors

- BAIC Motor Corp.

- SAIC Motor Corp. Ltd.

- Dongfeng Motor Corp.

- FAW Group

- GAC Aion

- NIO Inc.

- Xpeng Motors

- Li Auto

- Leapmotor

- Hozon Auto (Neta)

- Zeekr Intelligent Tech.

- Seres Group

- Jiangling Motors Corp.

- JAC Motors

- Chery Automobile

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Extended NEV Purchase-Tax Exemptions to 2027

- 4.1.2 Nationwide Fast-Charging & Battery-Swap Corridor Build-Out

- 4.1.3 PHEV Surge in Tier-2/3 Cities on Fuel-Savings Appeal

- 4.1.4 Municipal E-Freight Quotas Boosting Electric LCV Demand

- 4.1.5 V2G Pilot Tariffs Enabling Vehicle-Grid Revenue Streams

- 4.1.6 LFP-Driven Cost Parity With Sub-Compact ICE Cars

- 4.2 Market Restraints

- 4.2.1 Phase-Out of Central Subsidies Slowing Upgrade Cycles

- 4.2.2 Lithium-Carbonate Price & Export-Control Volatility

- 4.2.3 Provincial Caps on Low-Utilisation Public Chargers

- 4.2.4 Rising NEV Quality Issues (JD Power IQS) Denting Loyalty

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Battery-Chemistry Trends

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, 2024-2030)

- 5.1 By Drivetrain Type

- 5.1.1 Battery Electric Vehicles

- 5.1.2 Plug-in Hybrid Electric Vehicles

- 5.1.3 Fuel-cell Electric Vehicles

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.1.1 Hatchback

- 5.2.1.2 Sedan

- 5.2.1.3 SUV

- 5.2.1.4 MPV

- 5.2.2 Commercial Vehicles

- 5.2.2.1 Light Commercial Vehicles

- 5.2.2.2 Buses & Coaches

- 5.2.2.3 Medium & Heavy Trucks

- 5.2.1 Passenger Cars

- 5.3 By Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCM/NMC

- 5.3.3 NCA

- 5.3.4 Others

- 5.4 By Price Band

- 5.4.1 Less than USD 10,000

- 5.4.2 USD 10,000 - 20,000

- 5.4.3 USD 20,000 - 30,000

- 5.4.4 USD 30,000 - 50,000

- 5.4.5 Over USD 50,000

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 BYD Company Ltd

- 6.3.2 SAIC-GM-Wuling

- 6.3.3 Tesla Inc.

- 6.3.4 Geely Auto Group

- 6.3.5 Changan Automobile

- 6.3.6 Great Wall Motors

- 6.3.7 BAIC Motor Corp.

- 6.3.8 SAIC Motor Corp. Ltd.

- 6.3.9 Dongfeng Motor Corp.

- 6.3.10 FAW Group

- 6.3.11 GAC Aion

- 6.3.12 NIO Inc.

- 6.3.13 Xpeng Motors

- 6.3.14 Li Auto

- 6.3.15 Leapmotor

- 6.3.16 Hozon Auto (Neta)

- 6.3.17 Zeekr Intelligent Tech.

- 6.3.18 Seres Group

- 6.3.19 Jiangling Motors Corp.

- 6.3.20 JAC Motors

- 6.3.21 Chery Automobile

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

電動車虛擬原型製作市場:按組件、技術、部署模式、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測

電動車虛擬原型製作市場:按組件、技術、部署模式、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測 2026年全球V2B(車輛到建築)電力市場報告

2026年全球V2B(車輛到建築)電力市場報告 全電動多用途貨車市場規模、佔有率和成長分析:按產能、應用、終端用戶產業、地區和產業預測,2026-2033年

全電動多用途貨車市場規模、佔有率和成長分析:按產能、應用、終端用戶產業、地區和產業預測,2026-2033年 長續航里程電動車市場規模、佔有率和成長分析:按車輛類型、電池類型、充電基礎設施、續航里程、消費群體、動力系統、功率輸出和地區分類-2026-2033年產業預測

長續航里程電動車市場規模、佔有率和成長分析:按車輛類型、電池類型、充電基礎設施、續航里程、消費群體、動力系統、功率輸出和地區分類-2026-2033年產業預測 800V電動車架構市場規模、佔有率和成長分析:按車輛、架構、充電方式、組件、應用和地區分類-2026-2033年產業預測

800V電動車架構市場規模、佔有率和成長分析:按車輛、架構、充電方式、組件、應用和地區分類-2026-2033年產業預測 電動車售後市場規模、佔有率和成長分析:按零件類型、車輛類型、服務類型、動力系統、銷售管道、最終用戶、地區和產業預測,2026-2033年

電動車售後市場規模、佔有率和成長分析:按零件類型、車輛類型、服務類型、動力系統、銷售管道、最終用戶、地區和產業預測,2026-2033年 電動車(零能耗汽車)市場規模、佔有率和成長分析:按車輛類型、電源管理方法、充電基礎設施、電池技術、最終用戶和地區分類-產業預測(2026-2033 年)

電動車(零能耗汽車)市場規模、佔有率和成長分析:按車輛類型、電源管理方法、充電基礎設施、電池技術、最終用戶和地區分類-產業預測(2026-2033 年) 2026-2030年全球電動車市場

2026-2030年全球電動車市場 歐洲電動車市場:依動力類型(純電動車 (BEV)、燃料電池電動車 (FCEV)、插電式混合動力車 (PHEV)、混合動力車 (HEV))、功率輸出(100kW 以下、100kW-250kW)、應用(個人用途、商業用途)和地區劃分 - 全球預測至 2036 年

歐洲電動車市場:依動力類型(純電動車 (BEV)、燃料電池電動車 (FCEV)、插電式混合動力車 (PHEV)、混合動力車 (HEV))、功率輸出(100kW 以下、100kW-250kW)、應用(個人用途、商業用途)和地區劃分 - 全球預測至 2036 年 東協電動車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東協電動車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)