|

市場調查報告書

商品編碼

1937425

亞太地區綠建築:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Asia-Pacific Green Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

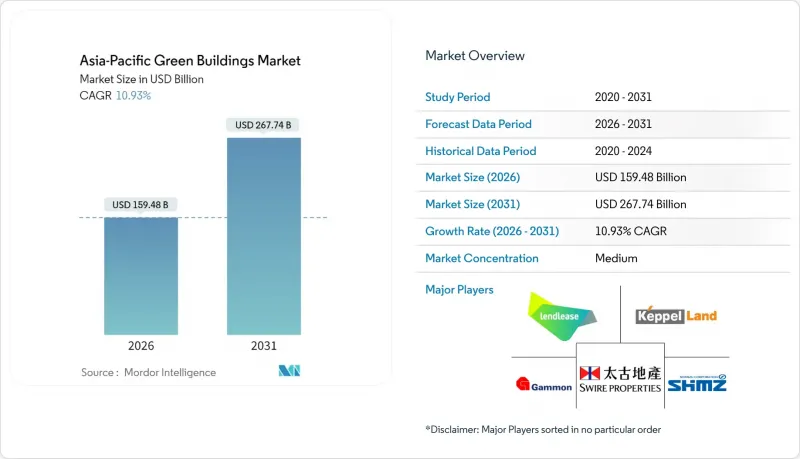

亞太地區綠建築市場在 2025 年的價值為 1,437.7 億美元,預計到 2031 年將達到 2,677.4 億美元,而 2026 年為 1,594.8 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 10.93%。

政策趨緊、企業持續推動淨零排放目標以及能源價格波動帶來的實際成本,正將綠色特性從附加的額外功能轉變為核心計劃要求。中國在規模方面保持主導,而印度13.02%的年複合成長率加速成長,凸顯了市場重心轉移到快速成長的南亞需求中心的趨勢。建築系統整合、智慧暖通空調系統的普及以及日趨成熟的綠色金融,正在支撐著強大的供應商體系,並緩解短期供應鏈摩擦的影響。由於認證障礙有利於現有企業,市場競爭強度適中,但數位化顛覆者正透過「性能即服務」模式重塑價值獲取方式。

亞太綠建築市場趨勢與洞察

日益嚴格的建築節能規範推動合規主導型成長

諸如中國的GB 55015-2021、日本修訂的《建築節能法》以及印度的2024年節能建築規範等強制性標準,正在擴大法規要求採用綠色技術的計劃範圍。開發人員現在在概念設計階段就引入效能建模,因為不符合標準可能會導致計劃核准延遲和轉售受限。因此,預製建築外牆板製造商和智慧空調系統供應商的訂單穩定成長,產能不斷擴大,單位成本壓力也隨之緩解。此外,中國地方政府正在補貼入住後的能源審核,支持從施工階段標準轉向使用中性能指標。這些協同效應正在建構一個相互促進的監管、檢驗和採購標準生態系統,加速亞太綠建築市場從自願採用階段走向規範化。

企業ESG政策轉變投資組合策略

凱德集團的淨零碳排放承諾和太古地產12億美元的永續發展掛鉤貸款,充分體現了資金籌措條款如今如何與可衡量的建築性能掛鉤。亞洲主要開發人員的負責人薪酬與科學碳目標舉措的里程碑掛鉤,脫碳目標也已納入企業管治。大型跨國公司正在利用標準化的建築評估模板,並將其推廣至本地供應鏈,迫使分包商提升自身能力,否則將面臨關閉的風險。在整個專案組合中採購高效能冷卻器和智慧感測器,可以享受批量折扣,降低小規模計劃的准入門檻。這些網路效應正在將亞太綠色建築產業的潛在市場遠遠擴展到旗艦計劃之外。

高昂的資本成本溢價限制了次市場的採用。

在印尼,由於建築幕牆構件依賴進口且缺乏本地檢測設施,成本溢價高達30%。小型銀行因主要城市以外地區認證建築的轉售情況不佳,在其建築貸款中加入了高風險溢價。開發商為了確保預期收益,降低了建築規格,從而減少了對環境的影響並影響了市場估值。缺乏可靠的次市場數據迫使估值專家採用保守的估值假設,導致資金籌措持續面臨挑戰。這種情況很可能在短期內限制亞太地區綠建築市場在價格敏感型地區的滲透。

細分市場分析

預計到2025年,建築系統領域將佔亞太綠建築市場佔有率的40.85%,並在2031年之前以11.73%的複合年成長率持續成長。這一成長主要歸功於智慧暖通空調平台,該平台應用人工智慧演算法進行預測性維護和即時負載平衡,從而顯著降低能源消耗強度。供應商正在整合現場太陽能發電、電池儲能和需量反應功能,使建築物能夠作為靈活的電網參與者而非靜態的消費者發揮作用。外牆產品也緊跟著,建築圍護結構的創新兼顧了隔熱性和美觀性,適用於不同的氣候帶。室內產品則著重提升居住者的健康,例如採用低揮發性有機化合物(VOC)材料和晝夜節律照明,以符合後疫情時代人們對健康生活的期望。新興的「其他」類別,包括建築整合光伏(BIPV),凸顯了一系列創新材料的湧現,這些材料將繼續重塑亞太綠色建築市場。

整合平台透過將控制功能整合到統一的控制面板中,降低了試運行的複雜性。對於肩負日益成長的報告義務的設施管理團隊而言,這項特性越來越受到重視。標準化的數位雙胞胎支援遠端效能審核,從而提升了系統供應商的業務收益。隨著碳定價機制的日益普及,速率最佳化控制演算法已成為採購競標中的關鍵差異化因素,進一步增強了整合建築系統供應商的競爭優勢。儘管外牆和內牆產品保持成長勢頭,但其年成長率仍落後於領先的系統類別,而系統類別目前已成為亞太綠建築市場的核心收入驅動力。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察與動態

- 市場概覽

- 市場促進因素

- 加強建築節能規範、綠色標準及長期脫碳目標

- 企業環境、社會及公司治理/淨零排放目標推動投資組合整體評等上調

- 能源價格波動以及對降低生命週期營運成本的日益重視

- 擴大綠色金融(稅收優惠、綠色債券、永續發展掛鉤貸款)

- 支持市場對認證資產的偏好以及相關的租金和估值溢價

- 市場限制

- 次市場初始資本成本高,且投資回收期不確定性。

- 認證材料和技術方面的技能短缺和供需失衡

- 各司法管轄區法規碎片化、獎勵不統一、評估方法不一致。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 外飾商品

- 室內產品

- 建築系統

- 其他

- 最終用戶

- 住宅

- 公寓和住宅

- 別墅及獨戶房屋住宅

- 商業

- 辦公室

- 零售

- 後勤

- 公共利益組織

- 其他(工業地產、飯店地產等)

- 住宅

- 施工階段

- 新建工程

- 維修

- 按國家/地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Lendlease

- Keppel Land

- Shimizu Corporation

- Swire Properties

- Gammon Construction

- CapitaLand

- Sino Group

- WSP

- Obayashi Corporation

- Sun Hung Kai Properties

- Mitsubishi Estate

- Daiwa House

- China State Construction Eng. Corp.

- CSCEC Green Building

- SK Ecoplant

- LIXIL Group

- Kingspan Group

- Tata Projects

- Gensler

- GreenA Consultants

第7章 市場機會與未來展望

The Asia-Pacific Green Buildings Market was valued at USD 143.77 billion in 2025 and estimated to grow from USD 159.48 billion in 2026 to reach USD 267.74 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031).

Heightened policy stringency, sustained corporate net-zero pledges, and the tangible cost of energy volatility now position green specifications as baseline project requirements rather than premium add-ons. China retains scale leadership, while India's accelerating 13.02% CAGR underscores a geographic pivot toward fast-growing South Asian demand centers. Building systems integration, smart-HVAC adoption, and maturing green finance underpin robust supplier pipelines that dilute the impact of short-term supply chain friction. Competitive intensity remains moderate as certification hurdles favor incumbents, yet digital disruptors are reshaping value capture through performance-as-a-service models.

Asia-Pacific Green Buildings Market Trends and Insights

Strengthening Building-Energy Codes Drive Compliance-Led Growth

Mandatory codes such as China's GB 55015-2021, Japan's revised Building Energy Efficiency Act, and India's 2024 Energy Conservation Building Code enlarge the addressable pool of projects that must integrate green technologies by statute. Developers now incorporate performance modeling during concept design because non-compliance risks project approval delays, and resale limitations. Prefabricated facade makers and smart-HVAC suppliers consequently enjoy more stable order books, prompting capacity expansions that ease unit-cost pressures. Provincial authorities in China further subsidize post-occupancy energy audits, reinforcing the shift from construction-stage criteria to in-use performance metrics. The cumulative effect is a self-reinforcing ecosystem in which regulation, verification, and procurement standards accelerate the APAC Green Buildings market beyond voluntary adoption.

Corporate ESG Mandates Transform Portfolio Strategies

CapitaLand's net-zero carbon pledge and Swire Properties' USD 1.2 billion sustainability-linked loan exemplify how financing terms now hinge on measurable building performance. Executive compensation at leading Asian developers is tied to the Science Based Targets initiative milestones, embedding decarbonization goals in corporate governance. Large multinationals leverage standardized building assessment templates that cascade to local supply chains, forcing subcontractors to upgrade capabilities or face disqualification. Cross-portfolio procurement of high-efficiency chillers and smart sensors yields volume discounts, lowering adoption thresholds for smaller projects. The resulting network effects expand the APAC Green Buildings industry's serviceable obtainable market well beyond marquee flagship developments.

Capital Cost Premiums Constrain Secondary-Market Adoption

In Indonesia, cost premiums of up to 30% persist due to imported facade components and limited local testing facilities. Smaller banks price higher risk premiums into construction loans because resale benchmarks for certified buildings remain thin outside capital cities. Developers compromise on specification depth to preserve pro-forma returns, diluting environmental outcomes and market perception. Absent robust secondary-market data, valuation professionals default to conservative appraisal assumptions, perpetuating financing challenges. This dynamic tempers near-term APAC Green Buildings market penetration in price-sensitive locales.

Other drivers and restraints analyzed in the detailed report include:

- Energy Cost Volatility Accelerates Lifecycle Value Recognition

- Green Finance Mechanisms Enable Capital Formation

- Skills Gaps and Supply Chain Constraints Limit Execution Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Building Systems commanded 40.85% of the APAC Green Buildings market share in 2025, and the segment is expected to escalate at an 11.73% CAGR through 2031. This growth stems from intelligent HVAC platforms that apply artificial-intelligence algorithms for predictive maintenance and real-time load balancing, delivering measurable reductions in energy intensity. Suppliers integrate on-site solar, battery storage, and demand-response capabilities, enabling buildings to act as flexible grid participants rather than static consumers. Exterior Products follow in scale as building-envelope innovations combine thermal resistance with aesthetic versatility suited to diverse climatic zones. Interior Products advance occupant-wellness attributes, such as low-VOC materials and circadian lighting, aligning with post-pandemic health expectations. An emergent "Others" cluster, including building-integrated photovoltaics, underscores a pipeline of disruptive materials that will continue to reshape the APAC Green Buildings market.

Integrated platforms also lower commissioning complexity by consolidating controls under unified dashboards, a feature increasingly valued by facilities-management teams tasked with meeting escalating reporting obligations. Standardized digital twins facilitate remote performance auditing, strengthening post-handover service revenues for system vendors. As carbon-pricing schemes spread, tariff-optimized control algorithms become critical differentiators in procurement tenders, amplifying the competitive moat around integrated Building Systems providers. Although Exterior and Interior Products maintain momentum, their annual gains trail the flagship Systems category, which now represents the core revenue engine of the APAC Green Buildings market.

The Asia-Pacific Green Buildings Market Report is Segmented by Product Type (Exterior Products, Interior Products, Building Systems, Others), by End User (Residential - Apartments & Condominiums, Villas & Landed Houses; Commercial - Office, and More), by Construction Stage (New Construction, Renovation), and by Country (China, India, Japan, South Korea, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Lendlease

- Keppel Land

- Shimizu Corporation

- Swire Properties

- Gammon Construction

- CapitaLand

- Sino Group

- WSP

- Obayashi Corporation

- Sun Hung Kai Properties

- Mitsubishi Estate

- Daiwa House

- China State Construction Eng. Corp.

- CSCEC Green Building

- SK Ecoplant

- LIXIL Group

- Kingspan Group

- Tata Projects

- Gensler

- GreenA Consultants

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strengthening building-energy codes, green standards, and long-term decarbonization targets

- 4.2.2 Corporate ESG/net-zero commitments driving portfolio-wide upgrades

- 4.2.3 Energy price volatility and emphasis on lifecycle operating cost reductions

- 4.2.4 Expanding green finance (tax incentives, green bonds, sustainability-linked loans)

- 4.2.5 Market preference for certified assets, supporting rent and valuation premiums

- 4.3 Market Restraints

- 4.3.1 Higher upfront capital costs and uncertain payback in secondary markets

- 4.3.2 Skills shortages and uneven availability of certified materials/technologies

- 4.3.3 Fragmented regulations, split incentives, and inconsistent valuation practices across jurisdictions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Exterior Products

- 5.1.2 Interior Products

- 5.1.3 Building Systems

- 5.1.4 Others

- 5.2 By End User

- 5.2.1 Residential

- 5.2.1.1 Apartments & Condominiums

- 5.2.1.2 Villas & Landed Houses

- 5.2.2 Commercial

- 5.2.2.1 Office

- 5.2.2.2 Retail

- 5.2.2.3 Logistics

- 5.2.2.4 Institutional

- 5.2.2.5 Others (industrial real estate, hospitality real estate, etc.)

- 5.2.1 Residential

- 5.3 By Construction Stage

- 5.3.1 New Construction

- 5.3.2 Renovation

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Indonesia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lendlease

- 6.4.2 Keppel Land

- 6.4.3 Shimizu Corporation

- 6.4.4 Swire Properties

- 6.4.5 Gammon Construction

- 6.4.6 CapitaLand

- 6.4.7 Sino Group

- 6.4.8 WSP

- 6.4.9 Obayashi Corporation

- 6.4.10 Sun Hung Kai Properties

- 6.4.11 Mitsubishi Estate

- 6.4.12 Daiwa House

- 6.4.13 China State Construction Eng. Corp.

- 6.4.14 CSCEC Green Building

- 6.4.15 SK Ecoplant

- 6.4.16 LIXIL Group

- 6.4.17 Kingspan Group

- 6.4.18 Tata Projects

- 6.4.19 Gensler

- 6.4.20 GreenA Consultants

7 Market Opportunities & Future Outlook

綠色外牆市場:按類型、植被類型、應用和區域分類

綠色外牆市場:按類型、植被類型、應用和區域分類 2026年全球單戶住宅綠建築市場報告2026年全球多戶住宅綠建築市場報告2026年全球綠建築市場報告2026年全球非住宅綠建築市場報告2026年全球綠建築LEED諮詢市場報告

2026年全球單戶住宅綠建築市場報告2026年全球多戶住宅綠建築市場報告2026年全球綠建築市場報告2026年全球非住宅綠建築市場報告2026年全球綠建築LEED諮詢市場報告 簡易包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

簡易包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 綠色建築市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、應用、地區和競爭格局分類,2021-2031年

綠色建築市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、應用、地區和競爭格局分類,2021-2031年 綠建築市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

綠建築市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 客製化包裝市場(按包裝類型、材料、印刷技術和應用)—2025-2030 年全球預測

客製化包裝市場(按包裝類型、材料、印刷技術和應用)—2025-2030 年全球預測