|

市場調查報告書

商品編碼

1937392

美國電子商務物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States E-commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

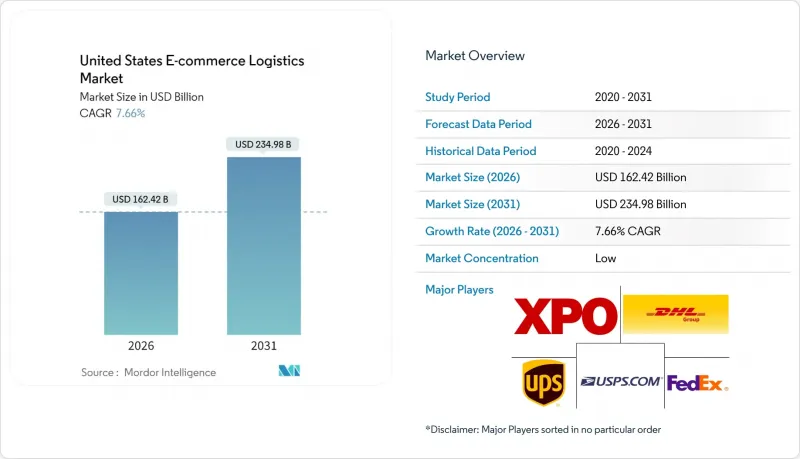

美國電子商務物流市場預計將從 2025 年的 1,508.6 億美元成長到 2026 年的 1,624.2 億美元,到 2031 年達到 2,349.8 億美元,2026 年至 2031 年的複合年成長率為 7.66%。

這種穩定擴張反映了數位商務從單純的便利選擇轉變為物流需求的主要成長引擎。消費者對即時送達的期望不斷提高、輕型小包裹數量的激增以及倉庫自動化的廣泛應用,正在共同重塑整個生態系統的成本結構和服務模式。監理政策的變化,例如取消對中國商品800美元最低限額關稅的優惠,已經促使國際經銷商在國內備貨,從而為履約網路帶來新的貨量。同時,勞動力短缺、都市區倉庫租金上漲以及超輕量訂單導致的小包裹盈利下降,正在擠壓利潤空間,並推動機器人技術和數據驅動的路線最佳化方面的創新。

美國電子商務物流市場趨勢與洞察

小規模B2C配送量的優勢

隨著直接面對消費者的銷售額超過企業對企業的貨運量,承運商正被迫調整原本為托盤運輸而設計的網路,以適應每天數百萬個輕型小包裹的運輸需求。都市區走廊的高密度配送促使演算法整合配送中心,從而減少路線里程並提高駕駛效率。大型企業不斷推動分類流程自動化,以滿足可追溯性要求並提高退貨率,而小型企業則在消費者安全文件的管理負擔上苦苦掙扎。因此,規模、資料整合和逆向物流能力能夠帶來永續的競爭優勢。

對當日達和隔日達的預期

消費者始終傾向於選擇承諾24小時送達的經銷商,這使得零售商能夠收取溢價,以彌補分散式庫存所需的資金投入。當日送達的可行性依賴於高訂單密度和先進的預測分析技術,這些技術可以將熱門商品投放到都市區的微型倉配中心。供應商利用人工智慧路線規劃引擎將多個目的地合併到一次配送中,從而降低最後一公里配送成本,即使客單價下降也能確保利潤率。隨著服務範圍擴展到第一線城市郊區,配送速度已成為網購消費者選擇品牌的三大重要因素之一。

供應鏈和勞動力問題

約33萬名卡車駕駛人離職率,加上倉庫員工流動率超過40%,導致運力緊張,薪資上漲。罷工、極端天氣和港口擁擠會迅速影響按時運行的小包裹運輸網路,造成額外費用和降低服務品質。雖然重複性工作的自動化和員工交叉培訓可以部分緩解風險,但人才保留仍然是一項結構性挑戰。

細分市場分析

截至2025年,運輸業在美國電子商務物流市場的佔有率將維持在65.40%,凸顯了覆蓋980萬公里公共道路的全國性小包裹網路的關鍵作用。儘管倉儲和履約業的複合年成長率將達到6.12%,在所有服務類別中位居榜首,但公路和最後一公里配送服務仍將是推動支出和成長的主要動力。自動路線最佳化、電動汽車車隊的引入以及整合API的可視化平台正在降低單位可變成本,同時將大多數都會地區的配送時間縮短至24小時以內。運輸活動的增加也推動了對套件組裝和客製化標籤等附加價值服務的需求,這些服務的價格溢價為5%至12%。

越來越多的托運人要求採用多模態解決方案,在單一管理合約中平衡成本、碳排放和速度目標。隨著美國電子商務物流市場持續吸收轉移至國內庫存的跨境物流流量,將倉儲能力與託管式專用車隊相結合的綜合服務供應商正在建立起穩固的市場地位。為遵守美國運輸部安全標準和各州新的排放法規,遠端資訊處理和預測性維護計畫正在推動應用,有助於確保車輛在需求高峰期的運轉率。

儘管到2025年B2C履約將佔總收入的72.30%,但C2C市場仍將以5.68%的複合年成長率持續成長,這反映了社交電商通路和P2P轉售應用程式的興起。 C2C寄售有獨特的服務需求,例如身分驗證、包裝指導和糾紛解決協助,這些都需要專業的第三方物流(3PL)解決方案。與付款閘道和買家保護計劃的端到端整合可以縮短從商品上架到交付給買家的周期,並提高市場流動性。

同時,大規模D2C品牌正深化外包夥伴關係,以提高產品推出的彈性。透過共用微型樞紐整合C2C和B2C貨量的混合型履約模式,能夠提供網路密度優勢。因此,美國電商物流市場對靈活的運力合約需求日益成長,這種合約允許在24小時內根據實際情況增加或減少運力和勞動力投入。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 小規模B2C配送量的優勢

- 對當日達和隔日達的預期

- 倉庫自動化和機器人技術的應用

- 中國國內庫存成長主要得益於監理改革的微量性調整。

- 零售媒體對履約數據的貨幣化

- 擴展暗店微型倉配網路

- 市場限制

- 供應鏈和勞動力中斷

- 都市區倉庫租金上漲

- 訂單量少導致小批量訂單盈利下降

- 人工智慧驅動的退貨詐騙日益增多

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 供需分析

- 行業的吸引力

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 逆向/退貨貨物流洞察

- 地緣政治事件如何影響供應鏈轉型

第5章 市場規模與成長預測

- 透過服務

- 運輸

- 路

- 鐵路運輸

- 航空郵件

- 海

- 倉儲和履約

- 附加價值服務(貼標籤、包裝、套件組裝)

- 運輸

- 按經營模式

- B2C

- B2B

- C2C

- 按目的地

- 國內的

- 跨境(國際)

- 按配送速度

- 當日送達(24小時內)

- 隔日送達(24-48小時)

- 標準配送(3-5個工作天)

- 其他(5天或以上)

- 按產品類別

- 食品/飲料

- 個人護理及家居用品

- 時尚與生活方式(配件、服裝、鞋履)

- 家具

- 家用電器和消費性電器產品

- 其他產品

- 按美國地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- United Parcel Service, Inc

- FedEx

- USPS

- XPO Logistics

- DHL

- DSV Solutions

- GEODIS

- Kuehne+Nagel

- CH Robinson

- CEVA Logistics

- Pitney Bowes

- OnTrac(formerly LaserShip)

- ShipBob

- ShipMonk

- Flexe

- Red Stag Fulfillment

- DSV Solutions

- Saddle Creek Logistics

- Rakuten Super Logistics

- Kenco Logistics Services

第7章 市場機會與未來展望

The United States E-commerce Logistics Market is expected to grow from USD 150.86 billion in 2025 to USD 162.42 billion in 2026 and is forecast to reach USD 234.98 billion by 2031 at 7.66% CAGR over 2026-2031.

Steady expansion reflects digital commerce's rise from a convenience option into the primary growth engine for logistics demand. Intensifying consumer expectations for instant delivery, a surge of lightweight parcel volumes, and widespread warehouse automation are together redefining cost structures and service models across the ecosystem. Regulatory shifts such as the end of the USD 800 de-minimis exemption for Chinese-origin goods are already prompting foreign sellers to hold inventory domestically, injecting fresh volume into fulfillment networks. Meanwhile, labor shortages, higher urban warehouse rents, and parcel-yield dilution from ultralight orders temper profit margins but accelerate innovation in robotics and data-driven route optimization.

United States E-commerce Logistics Market Trends and Insights

Dominance of B2C Parcel Volumes

Direct-to-consumer sales now outnumber business freight, forcing carriers to re-engineer networks built for pallets into systems tuned for millions of light parcels each day. High delivery density in metro corridors lets algorithms cluster stops, curbing route mileage and lifting driver productivity. Large players continue to automate sortation to meet traceability mandates and rising return flows, while smaller operators struggle with the administrative burden of consumer safety documentation. Scale, data integration, and reverse-logistics capability therefore confer durable competitive advantages.

Same-/Next-Day Delivery Expectations

Consumers consistently choose sellers promising shipment in 24 hours or less, letting retailers apply premium fees that offset the capital required for distributed inventory. Same-day viability hinges on high order density and advanced predictive analytics that stage popular SKUs inside urban micro-fulfillment nodes. Providers wield AI routing engines to combine multiple drops per run, slashing last-mile cost and protecting margins even when basket value dips. As coverage spreads to first-tier suburbs, delivery speed becomes a top-three brand selection criterion for online buyers.

Supply-Chain and Labor Disruptions

A shortage of around 330,000 truck drivers and warehouse turnover exceeding 40% keeps capacity tight and wages elevated. Strikes, extreme weather, or port congestion propagate swiftly through densely scheduled parcel networks, triggering surcharges and service deterioration. Automating repetitive tasks and cross-training crews provide partial risk mitigation, yet recruitment remains a structural challenge.

Other drivers and restraints analyzed in the detailed report include:

- Warehouse Automation and Robotics Adoption

- De-Minimis Reform Driving Chinese In-Market Stocking

- Escalating Urban Warehouse Rents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation maintained a 65.40% share of the United States e-commerce logistics market in 2025, underscoring the indispensable role of national parcel networks in covering 9.8 million km of public roads. Although warehousing and fulfillment are tracking a 6.12% CAGR the fastest among service categories linehaul and last-mile services carry the bulk of expenditure and growth visibility. Autonomous route optimization, electric-fleet rollouts, and API-integrated visibility platforms are lowering variable cost per package while shaving delivery windows to under 24 hours in most metro areas. Robust transportation activity also drives demand for in-line value-added services such as kitting and custom labeling, which fetch price premiums of 5-12%.

A growing share of shippers now demands multimodal solutions that reconcile cost, carbon, and speed targets within a single managed contract. As the United States e-commerce logistics market continues to absorb cross-border flows redirected into domestic stockholding, integrated service providers that couple warehousing capacity with controlled dedicated fleets own a defensible niche. Compliance with Department of Transportation safety standards and emerging state emissions rules is spurring telematics adoption and predictive maintenance scheduling, ensuring fleet uptime during surge events.

B2C fulfillment generated 72.30% of 2025 revenue; however, C2C marketplaces are on course for a 5.68% CAGR, reflecting the ascent of social-commerce channels and peer-to-peer resale apps. C2C consignments carry unique service needs, including identity verification, packaging guidance, and dispute resolution facilitation, prompting specialized 3PL solutions. End-to-end integrations with payment gateways and buyer-protection programs help shrink cycle times from seller listing to buyer delivery, improving marketplace liquidity.

Large direct-to-consumer brands are meanwhile deepening outsource partnerships to improve agility during new-product surges. Hybrid fulfillment models that pool C2C and B2C volume through shared micro-hubs deliver network density advantages. As a result, the United States e-commerce logistics market sees rising demand for flexible capacity contracts that ratchet space and labor commitments up or down on 24-hour notice.

The United States E-Commerce Logistics Market Report is Segmented by Service (Transportation, Warehousing & Fulfilment, and More), Business Model (B2C, B2B, C2C), Destination (Domestic, Cross-Border), Delivery Speed (Same-Day, Next-Day, Standard, Others), Product Category (Foods & Beverages, Personal & Household Care, Fashion & Lifestyle, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service, Inc

- FedEx

- USPS

- XPO Logistics

- DHL

- DSV Solutions

- GEODIS

- Kuehne + Nagel

- C.H. Robinson

- CEVA Logistics

- Pitney Bowes

- OnTrac (formerly LaserShip)

- ShipBob

- ShipMonk

- Flexe

- Red Stag Fulfillment

- DSV Solutions

- Saddle Creek Logistics

- Rakuten Super Logistics

- Kenco Logistics Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dominance of B2C parcel volumes

- 4.2.2 Same-/next-day delivery expectations

- 4.2.3 Warehouse automation and robotics adoption

- 4.2.4 De-minimis reform driving Chinese in-market stocking

- 4.2.5 Retail-media monetization of fulfilment data

- 4.2.6 Expansion of dark-store micro-fulfilment networks

- 4.3 Market Restraints

- 4.3.1 Supply-chain and labor disruptions

- 4.3.2 Escalating urban warehouse rents

- 4.3.3 Parcel-yield dilution from lightweight orders

- 4.3.4 AI-enabled returns fraud escalation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Demand and Supply Analysis

- 4.8 Industry Attractiveness

- 4.8.1 Porter's Five Forces

- 4.8.2 Threat of New Entrants

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Threat of Substitutes

- 4.8.6 Competitive Rivalry

- 4.9 Reverse / Return Logistics Insights

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing and Fulfilment

- 5.1.3 Value-Added Services (Labelling, Packaging, Kitting)

- 5.1.1 Transportation

- 5.2 By Business Model

- 5.2.1 B2C

- 5.2.2 B2B

- 5.2.3 C2C

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 Cross-border (international)

- 5.4 By Delivery Speed

- 5.4.1 Same-day (less than 24 h)

- 5.4.2 Next-day (24-48 h)

- 5.4.3 Standard (3-5 days)

- 5.4.4 Others (more than 5 days)

- 5.5 By Product Category

- 5.5.1 Foods and Beverages

- 5.5.2 Personal and Household Care

- 5.5.3 Fashion and Lifestyle (accessories, apparel, footwear)

- 5.5.4 Furniture

- 5.5.5 Consumer Electronics and Household Appliances

- 5.5.6 Other Products

- 5.6 By U.S. Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service, Inc

- 6.4.2 FedEx

- 6.4.3 USPS

- 6.4.4 XPO Logistics

- 6.4.5 DHL

- 6.4.6 DSV Solutions

- 6.4.7 GEODIS

- 6.4.8 Kuehne + Nagel

- 6.4.9 C.H. Robinson

- 6.4.10 CEVA Logistics

- 6.4.11 Pitney Bowes

- 6.4.12 OnTrac (formerly LaserShip)

- 6.4.13 ShipBob

- 6.4.14 ShipMonk

- 6.4.15 Flexe

- 6.4.16 Red Stag Fulfillment

- 6.4.17 DSV Solutions

- 6.4.18 Saddle Creek Logistics

- 6.4.19 Rakuten Super Logistics

- 6.4.20 Kenco Logistics Services

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

電子商務物流市場規模、佔有率和成長分析:按服務類型、模式、營運方式、產業和地區分類-2026-2033年產業預測

電子商務物流市場規模、佔有率和成長分析:按服務類型、模式、營運方式、產業和地區分類-2026-2033年產業預測 電子商務物流市場規模、佔有率、趨勢和預測:按產品類型、服務類型、業務領域和地區分類,2026-2034 年

電子商務物流市場規模、佔有率、趨勢和預測:按產品類型、服務類型、業務領域和地區分類,2026-2034 年 電子商務物流市場:依服務類型、供應商類型、營運模式、交付模式、經營模式、支付方式及最終用戶產業分類-2026-2032年全球市場預測

電子商務物流市場:依服務類型、供應商類型、營運模式、交付模式、經營模式、支付方式及最終用戶產業分類-2026-2032年全球市場預測 2026年全球跨境電子商務物流市場報告

2026年全球跨境電子商務物流市場報告 電子商務物流市場規模、市場佔有率和成長率;全球產業分析;按類型、應用和地區進行分析;以及未來預測(2026-2034 年)。2026年全球電子商務物流市場報告日本電子商務倉儲市場規模、佔有率、趨勢及預測(按產品類型、業務類型、組件和地區分類,2026-2034年)日本電子商務物流市場規模、佔有率、趨勢和預測:按服務、業務、目的地、產品和地區分類,2026-2034年

電子商務物流市場規模、市場佔有率和成長率;全球產業分析;按類型、應用和地區進行分析;以及未來預測(2026-2034 年)。2026年全球電子商務物流市場報告日本電子商務倉儲市場規模、佔有率、趨勢及預測(按產品類型、業務類型、組件和地區分類,2026-2034年)日本電子商務物流市場規模、佔有率、趨勢和預測:按服務、業務、目的地、產品和地區分類,2026-2034年 電子商務物流市場-全球產業規模、佔有率、趨勢、機會、預測:按營運區域、類型、服務類型、地區和競爭格局分類,2021-2031年

電子商務物流市場-全球產業規模、佔有率、趨勢、機會、預測:按營運區域、類型、服務類型、地區和競爭格局分類,2021-2031年 2026-2030年全球電子商務物流市場

2026-2030年全球電子商務物流市場