|

市場調查報告書

商品編碼

1937353

空運貨代:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Air Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

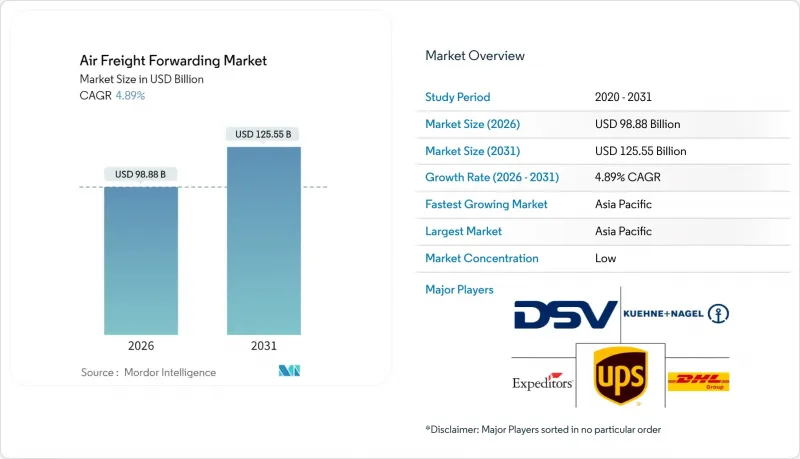

2025年航空貨運代理市場價值為942.7億美元,預計到2031年將達到1,255.5億美元,而2026年為988.8億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.89%。

成長要素包括強勁的跨境電子商務、對溫度敏感型藥品需求的激增以及正在進行的貨機改裝項目,這些項目正在填補貨艙運力的缺口。競爭格局的特點是旨在擴大規模的併購,其中DSV和Schenker的合併重塑了關鍵貿易航線的定價權和合約談判格局。數位化,包括即時貨物可視性工具,正在提高服務可靠性並實現溢價定價。同時,永續性和噴射機燃料價格使貨運代理商的利潤管理更加複雜,並促使他們進行策略性運力多元化。

全球空運代理市場趨勢與洞察

全球電子商務的快速成長

跨境電商目前佔亞洲空運貨運量的50%以上,縮短了旺季運輸時間,並增加了對貨運代理快遞運力的需求。預計到2025年,全球線上零售滲透率將達到24%,美國將達到26%,這將進一步強化對優先選擇空運而非海運的加急運輸解決方案的需求。美國計劃於2025年8月29日取消最低限額豁免,這將增加清關的複雜性,並促使托運人合併貨物以減輕合規負擔,從而導致國際小包裹運輸量增加。為此,貨運代理商正在將艙位包租合約重新分配給小小包裹密度高的航線,尤其是在亞洲和北美之間,並實施基於API的預訂系統以縮短報價週期。雖然這些趨勢增加了盈利波動性,但它們有利於那些能夠柔軟性調整網路運力以應對季節性需求高峰的營運商。

近岸外包與時間敏感型供應鏈

隨著企業將韌性置於成本最低採購之上,製造業的區域化正在北美地區催生新的運輸走廊。這導致美國區域機場(例如聖貝納迪諾國際機場和威爾明頓機場)在2024年和2025年的貨運量創下歷史新高。近岸外包趨勢正將貨物從擁擠的海岸門戶轉移到內陸設施,加速從卡車到飛機的轉運速度,提升高價值電子產品和汽車零件價值鏈的靈活性。蒂華納和鳳凰城-梅薩門戶機場等跨境樞紐表明,專用基礎設施如何加速墨西哥和美國之間的電子商務流通。分散式網路緩解了主要機場的航班時刻限制,並分散了地緣政治風險。貨運代理商正利用這些路線,為尋求更短補貨週期的客戶提供差異化的服務。

噴射機燃料價格波動

國際航空運輸協會(IATA)預測,2025年噴射機燃料平均價格為每桶87美元(2024年為每桶99美元),但燃油成本仍佔航空公司營運成本的26.4%,對貨運代理商的採購利潤造成壓力。永續航空燃油(SAF)的強制使用加劇了成本波動,因為SAF的交易價格遠高於煤油。儘管預計2025年產量將達到7.1326億加侖,但供應限制導致價格居高不下。貨運代理商透過與指數掛鉤的合約對沖風險,但中小托運人往往抵制燃油額外費用的上漲,從而擠壓了利潤空間。淨零排放強制要求迫使航空公司不計成本地採用SAF,將結構性價格風險納入航空貨運的經濟結構中。

細分市場分析

預計到2025年,普通貨物將佔航空貨運收入的61.35%,其中電子產品、服裝和零件的貨運量將支撐航空貨運市場規模。由於價格競爭加劇和模式轉換方式選擇的增加,其成長率預計將保持溫和。特殊貨物及其他貨物板塊預計在2026年至2031年間以4.38%的複合年成長率成長,主要受對溫控藥品、危險品和高價值電子產品等高服務水準貨物的需求驅動。國際航空運輸協會(IATA)和國際民航組織(ICAO)的規定設置了准入壁壘,限制了新進入者的進入,從而支撐了該板塊可觀的利潤率。

貨機改裝為特殊貨物運輸提供了獨特的優勢,因為主甲板的便利通道和特定的裝載配置使得處理大型貨物比在腹艙更為輕鬆。 CRYOPDP(每年處理超過60萬件臨床試驗和生物製藥貨物)是特種貨物運輸能力策略投資的一個例證,該公司於2025年被DHL收購。儘管電子商務的蓬勃發展使普通貨物運輸保持了韌性,但隨著托運人將基礎服務商品化,利潤率持續下降。相較之下,特種貨物運輸則維持了定價權,使營運商免受燃油額外費用糾紛的影響,並有助於提升高服務供應商在空運代理市場的佔有率。

區域分析

亞太地區預計到2025年將佔全球收入的34.62%,並在2026年至2031年間以5.14%的複合年成長率成長,這主要得益於中國出口引擎的強勁成長、印度預計6-9%的貨運量成長以及區域內電子商務的擴張。印度寬體貨機的短缺為能夠快速部署運力的貨運代理商提供了成長機遇,而安克拉治等樞紐機場則有助於實現高效的跨太平洋運輸。

北美憑藉其完善的電子商務基礎設施以及與墨西哥和加拿大的近岸貿易,繼續佔據著較大的市場佔有率。為了滿足對時效性要求高的貨物運輸需求,區域門戶機場正在不斷擴建,例如聖貝納迪諾和威爾明頓等內陸機場正在分流原本經由洛杉磯和紐約運輸的貨物量。與歐洲相比,北美地區對環境法規的壓力較小,因此快遞服務仍有成長空間。

在歐洲,日益嚴格的環境法規正促使非緊急貨物轉向海運和鐵路運輸。然而,藥品和高價值電子產品仍然支撐著航空貨運需求,航空公司在航班時刻緊張的情況下,正透過合資企業最佳化運力。中東和非洲地區是連接亞洲、歐洲和非洲的樞紐。對資料中心和電子商務基礎設施的投資,加上優越的地理位置,正在推動IT設備和生鮮食品等專業貨物的運輸。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球電子商務的快速成長

- 近岸外包與時間敏感型供應鏈

- 溫控和高價值貨物的成長

- 透過貨物轉換釋放潛力

- 即時貨物可視性平台支援高級定價

- 二線機場的跨境電子商務樞紐

- 市場限制

- 噴射機燃料價格波動

- 模式轉換,並強調永續性。

- 主要貨運機場的航班時刻限制

- 數位轉送平台的網路安全風險

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按貨物類型

- 普通貨物

- 特殊貨物及其他

- 目的地

- 國際的

- 國內的

- 按最終用戶行業分類

- 電子商務與零售

- 製造業和汽車業

- 醫療保健和製藥

- 生鮮食品和農產品

- 高科技電子產品

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美洲

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain & Global Forwarding

- Kuehne+Nagel

- DSV

- UPS Supply Chain Solutions

- Expeditors International

- Nippon Express

- Hellmann Worldwide Logistics

- Kintetsu World Express

- CEVA Logistics

- GEODIS

- Sinotrans

- Yusen Logistics

- CH Robinson

- LX Pantos

- Rhenus Logistics

- Scan Global Logistics

- Kerry Logistics

- AWOT Global Logistics Group

- DACHSER

- Savino Del Bene

第7章 市場機會與未來展望

第8章附錄

The Air Freight Forwarding Market was valued at USD 94.27 billion in 2025 and estimated to grow from USD 98.88 billion in 2026 to reach USD 125.55 billion by 2031, at a CAGR of 4.89% during the forecast period (2026-2031).

Growth stems from resilient cross-border e-commerce, a surge in temperature-controlled pharmaceuticals, and sustained freighter-conversion programs that counteract belly-hold capacity shortages. Competitive activity is marked by scale-seeking mergers, with the DSV-Schenker combination reshaping pricing power and contract negotiations across major trade lanes. Digitalization, including real-time cargo-visibility tools, improves service reliability and enables premium pricing. At the same time, sustainability mandates and volatile jet-fuel costs complicate forwarders' margin management and prompt strategic capacity diversification.

Global Air Freight Forwarding Market Trends and Insights

Global E-commerce Boom

Cross-border e-commerce now represents more than 50% of Asia-originating air cargo volumes, compressing peak-season timelines and amplifying forwarder demand for express capacity. It is forecasted that global online retail penetration to reach 24% worldwide and 26% in the United States by 2025, reinforcing demand for fast transit solutions that favor air over ocean. The scheduled removal of the U.S. de minimis exemption on August 29, 2025, increases customs-clearance complexity and is expected to lift international parcel volumes as shippers consolidate shipments to reduce compliance burdens. Forwarders respond by reallocating block-space agreements toward lanes with high small-parcel density, particularly Asia-North America, while deploying API-based booking engines that shorten quotation cycles. These dynamics raise yield volatility yet reward operators that can flex network capacity to seasonal surges.

Near-shoring & Time-Critical Supply-Chains

Regionalization of manufacturing has spawned new North America-centric corridors as companies prioritize resilience over lowest-cost sourcing, pushing secondary U.S. airports such as San Bernardino International and Wilmington Air Park to record cargo growth in 2024 and 2025. Near-shoring dynamics shift volume away from congested coastal gateways toward inland facilities that offer faster truck-to-air transfers, enhancing supply-chain agility for high-value electronics and automotive components. Cross-border hubs in Tijuana and Phoenix-Mesa Gateway Airport illustrate how specialized infrastructure accelerates Mexico-U.S. e-commerce flows. Distributed networks mitigate slot constraints at tier-1 airports and disperse geopolitical risk. Forwarders leverage these routes to differentiate service offerings aimed at customers seeking shorter replenishment cycles.

Volatile Jet-Fuel Prices

IATA projects average jet-fuel at USD 87 per barrel in 2025 versus USD 99 in 2024, yet fuel still accounts for 26.4% of airline operating costs, putting pressure on forwarder procurement margins. Sustainable Aviation Fuel mandates elevate cost variability because SAF trades at a significant premium to kerosene. Production volumes are slated to reach 713.26 million gallons in 2025, but supply limitations keep prices elevated. Forwarders hedge exposure through index-linked contracts, yet smaller shippers often resist fuel-surcharge escalations, squeezing margins. Net-zero commitments press carriers to adopt SAF irrespective of cost, embedding structural price risk into air cargo economics.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Temperature-Controlled & High-Value Cargo

- Freighter Conversions Unlocking Latent Capacity

- Sustainability-Driven Modal Shift to Sea & Rail

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General cargo accounted for 61.35% of 2025 revenues, anchoring the air freight forwarding market size through volumes generated by electronics, apparel, and spare parts. Its growth rate remains modest as pricing competition intensifies and modal shift options proliferate. Special cargo and others are expected to climb at a 4.38% CAGR (2026-2031) because temperature-controlled pharmaceuticals, dangerous goods, and high-value electronics demand elevated service standards. This segment benefits from regulatory moats created by IATA and ICAO rules that limit new entrant penetration and underpin attractive yields.

Freighter conversions have disproportionate benefits for special cargo because main-deck access and specific load configurations accommodate outsized items better than belly holds. DHL's 2025 acquisition of CRYOPDP, which manages more than 600,000 clinical-trial and biopharma shipments annually, demonstrates strategic investment in special-cargo capacity. General cargo retains resilience from the e-commerce surge, but margin dilution persists as shippers commoditize basic services. Specialized cargo, by contrast, maintains pricing power that shields operators from fuel-surcharge debates, contributing positively to the air freight forwarding market share held by high-service providers.

The Air Freight Forwarding Market Report is Segmented by Cargo Type (General Cargo and Special Cargo & Others), Destination (International and Domestic), End-User Industry (E-Commerce & Retail, Manufacturing & Automotive, Healthcare & Pharmaceuticals, Perishables & Fresh Produce, and More), Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 34.62% of global revenues in 2025 and is projected to advance at a 5.14% CAGR (2026-2031), propelled by China's export engine, India's 6-9% projected cargo growth, and intra-regional e-commerce expansion. Wide-body freighter scarcity in India offers growth prospects for forwarders that can deploy capacity quickly, while hubs like Anchorage enable efficient trans-Pacific transfers.

North America maintains a significant share through embedded e-commerce infrastructure and near-shoring trade with Mexico and Canada. Regional gateways expand to accommodate time-critical flows, with San Bernardino and Wilmington illustrating how inland airports capture volumes that once funneled through Los Angeles or New York. Sustainability pressures are lower relative to Europe, granting growth runway for express freight services.

Europe faces tighter environmental regulations that nudge shippers toward sea or rail for non-urgent cargo. Still, pharmaceuticals and high-value electronics sustain air freight demand, and carriers leverage joint ventures to optimize capacity amid stringent slot allocations. The Middle East and Africa serve as connective hubs linking Asia, Europe, and Africa. Investments in data centers and e-commerce infrastructure, paired with the region's geographic advantage, foster specialized freight flows for IT equipment and perishables.

- DHL Supply Chain & Global Forwarding

- Kuehne + Nagel

- DSV

- UPS Supply Chain Solutions

- Expeditors International

- Nippon Express

- Hellmann Worldwide Logistics

- Kintetsu World Express

- CEVA Logistics

- GEODIS

- Sinotrans

- Yusen Logistics

- C.H. Robinson

- LX Pantos

- Rhenus Logistics

- Scan Global Logistics

- Kerry Logistics

- AWOT Global Logistics Group

- DACHSER

- Savino Del Bene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global e-commerce boom

- 4.2.2 Near-shoring & time-critical supply-chains

- 4.2.3 Growth in temperature-controlled & high-value cargo

- 4.2.4 Freighter conversions unlocking latent capacity

- 4.2.5 Real-time cargo-visibility platforms enabling premium pricing

- 4.2.6 Secondary-airport cross-border e-commerce hubs

- 4.3 Market Restraints

- 4.3.1 Volatile jet-fuel prices

- 4.3.2 Sustainability-driven modal shift to sea & rail

- 4.3.3 Slot constraints at tier-1 cargo airports

- 4.3.4 Cyber-security risks in digital forwarding platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Cargo Type

- 5.1.1 General Cargo

- 5.1.2 Special Cargo and Others

- 5.2 By Destination

- 5.2.1 International

- 5.2.2 Domestic

- 5.3 By End-user Industry

- 5.3.1 E-commerce & Retail

- 5.3.2 Manufacturing & Automotive

- 5.3.3 Healthcare & Pharmaceuticals

- 5.3.4 Perishables & Fresh Produce

- 5.3.5 High-Tech & Electronics

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain & Global Forwarding

- 6.4.2 Kuehne + Nagel

- 6.4.3 DSV

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 Expeditors International

- 6.4.6 Nippon Express

- 6.4.7 Hellmann Worldwide Logistics

- 6.4.8 Kintetsu World Express

- 6.4.9 CEVA Logistics

- 6.4.10 GEODIS

- 6.4.11 Sinotrans

- 6.4.12 Yusen Logistics

- 6.4.13 C.H. Robinson

- 6.4.14 LX Pantos

- 6.4.15 Rhenus Logistics

- 6.4.16 Scan Global Logistics

- 6.4.17 Kerry Logistics

- 6.4.18 AWOT Global Logistics Group

- 6.4.19 DACHSER

- 6.4.20 Savino Del Bene

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

8 Appendix

貨運代理市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。

貨運代理市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。 貨運代理市場:按運輸方式、客戶類型、服務、應用和地區分類的市場規模、佔有率和趨勢分析,以及細分市場預測(2026-2033 年)

貨運代理市場:按運輸方式、客戶類型、服務、應用和地區分類的市場規模、佔有率和趨勢分析,以及細分市場預測(2026-2033 年) 航空貨運代理市場報告:按類型、服務類型、最終用戶行業和地區分類(2026-2034 年)

航空貨運代理市場報告:按類型、服務類型、最終用戶行業和地區分類(2026-2034 年) 航空貨運代理市場:依服務類型、服務形式、貨運優先順序、貨運量、產品類型及最終用戶產業分類-2026-2032年全球市場預測

航空貨運代理市場:依服務類型、服務形式、貨運優先順序、貨運量、產品類型及最終用戶產業分類-2026-2032年全球市場預測 貨運市場:依運輸方式、服務類型、最終用戶產業及地區分類

貨運市場:依運輸方式、服務類型、最終用戶產業及地區分類 2026年全球國際貨運代理市場報告2026年全球貨運代理市場報告

2026年全球國際貨運代理市場報告2026年全球貨運代理市場報告 全球貨運市場規模、佔有率、趨勢和成長分析報告(2026-2034)貨運代理市場:依運輸方式、服務及區域分類

全球貨運市場規模、佔有率、趨勢和成長分析報告(2026-2034)貨運代理市場:依運輸方式、服務及區域分類 貨運代理市場-全球產業規模、佔有率、趨勢、機會及預測(依運輸方式、顧客類型、應用、地區及競爭格局分類,2021-2031年)

貨運代理市場-全球產業規模、佔有率、趨勢、機會及預測(依運輸方式、顧客類型、應用、地區及競爭格局分類,2021-2031年)