|

市場調查報告書

商品編碼

1937256

非洲棉花:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Africa Cotton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

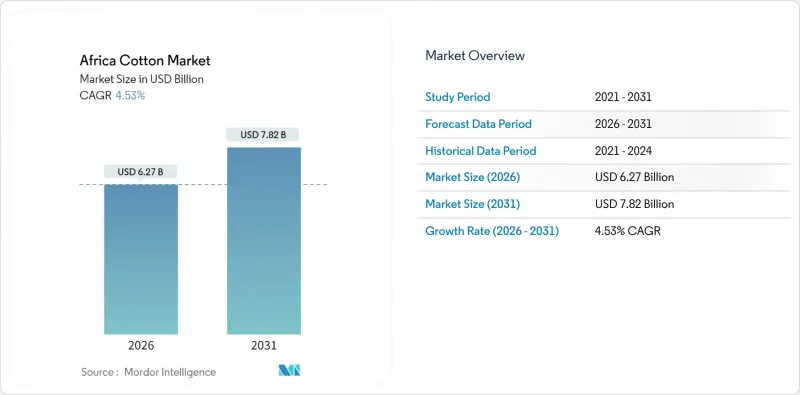

預計到 2026 年,非洲棉花市場價值將達到 62.7 億美元,高於 2025 年的 60 億美元。

預計到 2031 年將達到 78.2 億美元,2026 年至 2031 年的複合年成長率為 4.53%。

這項成長主要得益於薩赫勒地區灌溉網路的擴張、中國對西非棉花日益成長的需求,以及政府改善農民獲取水資源、農業投入品和數位化諮詢服務的政策。根據美國農業部海外農業局的數據,象牙海岸共和國和布吉納法索是非洲12個棉花生產國中最大的兩個國家,預計在研究期間產量將持續成長。根據聯合國糧食及農業組織(糧農組織)企業統計資料庫,馬利共和國2023年的棉花產量將超過68.5萬噸,創歷史新高。這些國家的大量棉花產量正在推動非洲棉花市場的成長。永續性認證透過可追溯性實現了溢價,而以影響力為導向的資金籌措則支持了小規模的現代化。儘管生產較為分散,但大型貿易業者正透過投資棉花加工廠和永續農業實踐來促進垂直整合。農村基礎設施不足、農業勞動力老化以及外匯限制阻礙了現代化進程。新技術和耐旱灌溉系統的引入為生產者提供了滿足品質要求的潛在改進空間。

非洲棉花市場趨勢與洞察

擴大棉花種植面積

隨著西非各國透過公共投資改善灌溉和倉儲基礎設施,擴大棉花種植面積,非洲棉花市場持續成長。伊斯蘭開發銀行集團成員國際伊斯蘭貿易融資公司(ITFC)已核准一項1.06億歐元(約11.194億日圓)的貸款,用於支持布吉納法索的棉花產業。該筆資金是根據與布吉納法索紡織協會(Sofitex)簽訂的「穆拉巴哈」(Murabaha)協議提供的。根據聯合國糧食及農業組織(FAO)預測,馬利共和國的棉花種植面積預計將從2022年的59萬公頃增加到2023年的71萬公頃。馬利共和國的尼日爾國家公司目前管理著7.4萬公頃農田,其中包括棉花種植區,並計劃將種植面積擴大3,300平方公里,顯示未來棉花供應潛力巨大。雖然耕地面積的擴大將增加農民的收入,但多邊組織正在努力實施氣候智慧型灌溉指南,以保護雨養農業系統免受氣候變遷的影響。耕地面積的永續擴張取決於氣候適應型水資源管理系統和獲得價格合理的農業投入品。

中國對西非棉花的需求日益成長

中國進口西非棉花出口的90%,透過維持長絨棉的溢價,支撐著非洲棉花市場的獲利成長。非洲棉花的高纖維強度符合中國紡織品生產的要求。這種依賴性使得非洲棉花生產商容易受到中國政策變化的影響,尤其是中國囤積採購行為的影響。為了保護收入免受市場波動的影響,非洲生產商必須在維持棉花高品質的同時,實現出口管道多元化。為了確保原料供應穩定,中國持續增加對非洲棉花整個價值鏈的投資,涵蓋從種植到服飾製造的各個環節。 「非洲製造棉花(CmiA)」等項目體現了中國對非洲棉花產業的承諾,並促進了非洲農民、紡織企業和中國市場之間的合作。

與全球同業其他公司相比,脫棉率較低

非洲棉花加工廠每噸棉花耗電78千瓦時,遠高於基準值。這降低了企業的競爭力,也減少了農民的利潤。引入自動化鋸輥可以在保持纖維長度的同時,將能耗降低50%。對喀麥隆的SODECOTON公司而言,棉花加工過程中產生的棉殼廢棄物蘊藏著巨大的未開發能源潛力,凸顯了上述挑戰。效率低下會增加加工成本,並影響纖維質量,因為過時的棉花技術會傷害棉纖維,降低其市場價值。這形成了一個惡性循環:盈利下降限制了對現代化設備的投資。

細分市場分析

非洲棉花市場報告按地區分類(布吉納法索、馬利共和國、貝南、象牙海岸共和國、喀麥隆、蘇丹、奈及利亞、埃及等)。研究包括產量分析(數量)、消費量分析(價值和數量)、出口量分析(價值和數量)、進口量分析(價值和數量)以及價格趨勢分析。市場預測以價值(美元)和數量(公噸)表示。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大棉花種植面積

- 中國市場對西非棉花的需求不斷成長

- 擴大灌溉走廊

- 引進基因改造棉種子

- 數位化傳播平台

- 來自注重ESG品牌的可追溯性溢價

- 市場限制

- 與其他全球競爭對手相比,脫粒率較低

- 小規模人口老化

- 低度開發的農村物流

- 由於外匯短缺,進口原料受到限制

- 價值/供應鏈分析

- 監管環境

- 技術展望

- PESTEL 分析

第5章 市場規模和成長預測(價值和數量)

- 按地區分類(生產分析、消費分析(數量和價值)、進口分析(數量和價值)、出口分析(數量和價值)、價格趨勢分析)

- 布吉納法索

- 馬利共和國

- 貝南

- 象牙海岸共和國

- 喀麥隆

- 蘇丹

- 奈及利亞

- 埃及

- 辛巴威

- 摩洛哥

- 迦納

- 南非

第6章 競爭情勢

- 相關利益者名單

- Olam International Limited

- Louis Dreyfus Company BV

- Cargill, Incorporated

- Plexus Cotton Limited(RCMA Group)

- Paul Reinhart AG

- Compagnie Malienne pour le Developpement des Textiles SA

- Societe Burkinabe des Fibres Textiles(SOFITEX)

- Ivoire Coton SA

- Societe de Developpement du Coton(SODECOTON)

- Devcot SA

- West African Cotton Company Limited(WACOT)

- Branson Commodities

- ETG Commodities(ETC Group)

- Cotton Company of Zimbabwe Limited(COTTCO)

- Alliance Ginneries Limited

第7章 市場機會與未來展望

Africa cotton market size in 2026 is estimated at USD 6.27 billion, growing from 2025 value of USD 6.0 billion with 2031 projections showing USD 7.82 billion, growing at 4.53% CAGR over 2026-2031.

The growth stems from expanded irrigation networks in the Sahel region, increased Chinese demand for West African cotton, and government policies improving farmers' access to water, agricultural inputs, and digital advisory services. According to the USDA's Foreign Agricultural Service, among the twelve cotton-producing nations in Africa, Cote d'Ivoire and Burkina Faso are the largest producers, with production projected to increase during the study period. Mali achieved its highest cotton production of over 685,000 metric tons in 2023, as reported by the Food and Agriculture Organization Corporate Statistical Database. The significant production volumes from these countries drive growth in the African cotton market. Sustainability certifications enable premium pricing through traceability, while impact-focused financing supports smallholder farm modernization. Despite fragmented production, major traders are pursuing vertical integration, investing in ginning facilities and sustainable farming practices. Inadequate rural infrastructure, an aging agricultural workforce, and foreign exchange limitations constrain modernization efforts. The adoption of new technologies and drought-resistant irrigation systems offers potential improvements for producers who meet quality requirements.

Africa Cotton Market Trends and Insights

Rising Area Under Cotton Cultivation

The African cotton market is expanding as West African producers increase planted areas through public investments in irrigation and storage infrastructure. The International Islamic Trade Finance Corporation (ITFC), a member of the Islamic Development Bank Group, has approved a €106 million ($119.4 million) financing facility for Burkina Faso to support its cotton industry. The funding was granted under a 'Mourabaha' agreement with the Burkinabe Society of Textile Fibers (Sofitex). According to the Food and Agriculture Organization, Mali's cotton cultivation area increased from 590,000 hectares in 2022 to 710,000 hectares in 2023. Mali's Office du Niger currently manages 74,000 hectares of agricultural land, including cotton farming, and plans to expand by 3,300 square kilometers, indicating significant future supply potential. While these expansions increase farmer revenues, they expose rain-fed systems to climate variability, leading multilateral agencies to implement climate-smart irrigation guidelines. The sustained growth in planted area depends on climate-resilient water management systems and access to affordable agricultural inputs.

Growing Chinese Demand for West-African Lint

China imports 90% of West African cotton exports, maintaining price premiums for long-staple lint and supporting revenue growth in the African cotton market. The high fiber strength of African cotton meets Chinese textile manufacturing requirements. This dependency makes producers vulnerable to Chinese policy changes, particularly in reserve buying practices. African producers need to diversify their export channels while maintaining premium quality to protect their income from market fluctuations. China continues to expand its investments across the African cotton value chain, from cultivation to garment manufacturing, to ensure a consistent raw material supply. Programs such as Cotton made in Africa (CmiA) demonstrate China's commitment to African cotton and facilitate connections between African farmers, textile companies, and the Chinese market.

Low Ginning Out-Turn Ratios vs. Global Peers

African cotton gins consume 78 kWh per metric ton, significantly exceeding benchmark levels, which reduces competitiveness and decreases farmer margins. Automated saw cylinders can reduce energy consumption by 50% while maintaining fiber length integrity. In Cameroon, SODECOTON's operations demonstrate these challenges, as cotton shell waste from processing contains substantial untapped energy potential. The efficiency gap increases processing costs and affects fiber quality, as outdated ginning technology can damage cotton fibers and lower their market value. This creates a cycle where reduced profitability constrains investment in modern equipment.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Irrigation Corridors

- Adoption of Genetically Modified Cotton Seeds

- Aging Smallholder Farmer Base

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Africa Cotton Market Report is Segmented by Geography (Burkina Faso, Mali, Benin, Cote D'Ivoire, Cameroon, Sudan, Nigeria, Egypt, and More). The Study Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Market Overview

- Market Drivers

- Market Restraints

- Value / Supply-Chain Analysis

- Regulatory Landscape

- Technological Outlook

- PESTLE Analysis

- List of Stakeholders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Area Under Cotton Cultivation

- 4.2.2 Growing Chinese Demand for West-African Lint

- 4.2.3 Expansion of Irrigation Corridors

- 4.2.4 Adoption of Genetically Modified Cotton Seeds

- 4.2.5 Digitized Extension Platforms

- 4.2.6 Traceability Premiums from ESG-Oriented Brands

- 4.3 Market Restraints

- 4.3.1 Low Ginning Out-Turn Ratios vs. Global Peers

- 4.3.2 Aging Smallholder Farmer Base

- 4.3.3 Under-Developed Rural Logistics

- 4.3.4 Foreign Exchange Shortages Restricting Input Imports

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 PESTLE Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- 5.1.1 Burkina Faso

- 5.1.2 Mali

- 5.1.3 Benin

- 5.1.4 Cote d'Ivoire

- 5.1.5 Cameroon

- 5.1.6 Sudan

- 5.1.7 Nigeria

- 5.1.8 Egypt

- 5.1.9 Zimbabwe

- 5.1.10 Morocco

- 5.1.11 Ghana

- 5.1.12 South Africa

6 Competitive Landscape

- 6.1 List of Stakeholders

- 6.1.1 Olam International Limited

- 6.1.2 Louis Dreyfus Company B.V.

- 6.1.3 Cargill, Incorporated

- 6.1.4 Plexus Cotton Limited (RCMA Group)

- 6.1.5 Paul Reinhart AG

- 6.1.6 Compagnie Malienne pour le Developpement des Textiles SA

- 6.1.7 Societe Burkinabe des Fibres Textiles (SOFITEX)

- 6.1.8 Ivoire Coton SA

- 6.1.9 Societe de Developpement du Coton (SODECOTON)

- 6.1.10 Devcot SA

- 6.1.11 West African Cotton Company Limited (WACOT)

- 6.1.12 Branson Commodities

- 6.1.13 ETG Commodities (ETC Group)

- 6.1.14 Cotton Company of Zimbabwe Limited (COTTCO)

- 6.1.15 Alliance Ginneries Limited

7 Market Opportunities and Future Outlook

2026-2030年全球棉花市場

2026-2030年全球棉花市場 棉漿市場:依產品類型、形態、加工方法、等級、應用和銷售管道分類-2026-2032年全球預測

棉漿市場:依產品類型、形態、加工方法、等級、應用和銷售管道分類-2026-2032年全球預測 日本有機棉市場規模、佔有率、趨勢和預測:按類型、品質類型、應用和地區分類,2026-2034年100%有機棉衛生棉條市場:依產品類型、吸收量、包裝類型、年齡層、價格範圍、皮膚刺激性和通路分類-2026-2032年全球預測硝化精棉市場按類型、原料、純度等級、終端用戶產業及通路分類-2026年至2032年全球預測精棉纖維素醚市場:依纖維素醚類型、等級、生產流程、應用和分銷管道分類-2026年至2032年全球預測精煉棉市場按類型、技術、等級、應用、最終用戶和通路分類-2026-2032年全球預測

日本有機棉市場規模、佔有率、趨勢和預測:按類型、品質類型、應用和地區分類,2026-2034年100%有機棉衛生棉條市場:依產品類型、吸收量、包裝類型、年齡層、價格範圍、皮膚刺激性和通路分類-2026-2032年全球預測硝化精棉市場按類型、原料、純度等級、終端用戶產業及通路分類-2026年至2032年全球預測精棉纖維素醚市場:依纖維素醚類型、等級、生產流程、應用和分銷管道分類-2026年至2032年全球預測精煉棉市場按類型、技術、等級、應用、最終用戶和通路分類-2026-2032年全球預測 全球棉花市場-2025年至2030年預測

全球棉花市場-2025年至2030年預測 棉纖維市場:依纖維等級、應用和地區分類

棉纖維市場:依纖維等級、應用和地區分類 棉花:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

棉花:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)