|

市場調查報告書

商品編碼

1934869

電信和網路管理中的基於代理的人工智慧:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Agentic AI In Telecommunications And Network Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

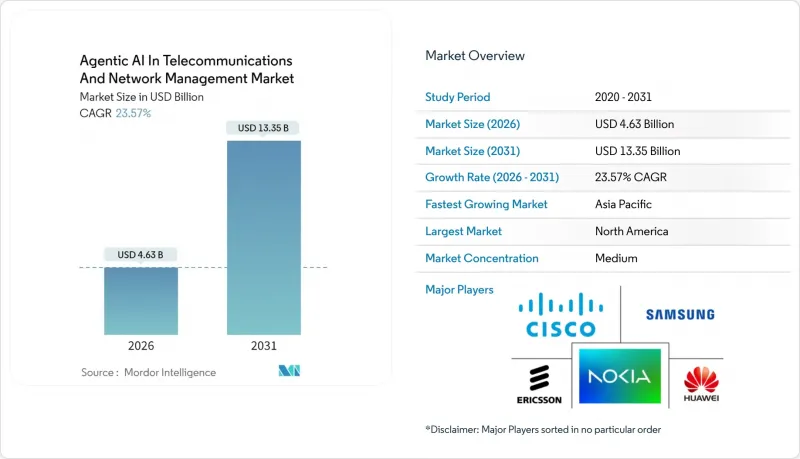

預計通訊和網路管理領域基於代理的人工智慧市場將從 2025 年的 37.5 億美元成長到 2026 年的 46.3 億美元,到 2031 年將達到 133.5 億美元,2026 年至 2031 年的複合年成長率為 23.57%。

隨著5G和新興的6G網路需要對數百萬個變數進行即時最佳化,而傳統的基於規則的系統無法應對,通訊業者正優先考慮自主編配。雖然雲端原生平台是早期採用的基礎,但為了降低推理延遲,邊緣運算和多接取邊緣運算(MEC)正在迅速發展。隨著攻擊者採用人工智慧,詐欺和安全管理尤其重要,迫使通訊業者在每一層都整合智慧異常檢測功能。網路設備供應商、超大規模資料中心業者和人工智慧專家組成多廠商聯盟,承諾提供開放介面和快速創新週期,競爭日益激烈。光纖和網路安全領域的策略併購預示著,未來整合連接和人工智慧安全將成為捍衛市場地位的必要前提。

全球基於代理的人工智慧市場趨勢及電信和網路管理洞察

5G/6G網路複雜性的增加推動了自主編配

天線數量、頻寬和服務等級要求的激增使得手動最佳化變得不切實際,迫使通訊業者嵌入能夠學習並持續執行網路意圖的自主代理。馬來西亞數位國民有限公司 (Digital Nasional Berhad) 在部署愛立信的基於意圖的平台六個月後,實現了 99.8% 的運轉率和 500% 的告警減少。 6G 研究表明,將非地面電波鏈路整合到地面電波小區中將使編配負擔翻倍,從而增強了其商業價值。諾基亞的模型顯示,自主網路每年可透過資本支出 (CAPEX)、營運支出 (OPEX) 和收入收益的組合,為通訊業者帶來 8 億美元的收益。這些經濟效益促使董事會迫切希望將概念驗證(PoC) 轉化為大規模運作部署。

資料流量的快速成長以及對預測性網路最佳化的需求

即時影片和人工智慧工作負載帶來的每小時流量高峰令傳統的規劃週期不堪重負。 Verizon部署的無線智慧控制器透過在流量高峰到來之前轉移容量,實現了15%的節能效果。通訊業者報告稱,與被動響應式方法相比,利用預測代理進行主動資源分配可將擁塞事件減少30%至50%。邊緣資料中心的情況更為嚴峻,因為那裡的推理負載是突發的且局部的。因此,預測最佳化已成為保障使用者體驗和企業服務等級協定 (SLA) 的必要手段。

通訊業者人工智慧舉措面臨的資料隱私和監管障礙

GDPR 和即將訂定的歐盟人工智慧法規迫使通訊業者增加多層可解釋性措施和嚴格的資料本地化控制,從而延長計劃週期。聯邦學習雖然能夠確保合規性,但可能會使計算成本增加三倍。跨境業者必須協調不同的框架,這會削弱規模經濟效益。這種不確定性導致部署方式趨於漸進,並促使營運商更加依賴超大規模資料中心業者的隱私工具包來確保審核準備就緒。

細分市場分析

到2025年,解決方案和平台將佔總支出的59.65%,這主要得益於通訊業者對可直接整合到現有OSS/BSS系統中的承包功能的需求。由於客製化工作流程,服務預計將以26.99%的複合年成長率成長,超過電信和網路管理領域基於代理的人工智慧市場的整體成長速度。由於需要對現有(棕地)網路進行特定領域的調整,電信和網路管理服務領域基於代理的人工智慧市場規模預計將迅速擴張。整合通訊業者負責資料管道調優、領域模型開發和生命週期管治,而這些功能是許多營運商內部所缺乏的。他們還提供託管最佳化服務,以使人工智慧代理商能夠持續適應不斷變化的業務KPI。因此,專業服務收入將隨著人工智慧成熟階段的推進而同步成長,這將使服務提供者深度融入通訊業者運營,創造持續的收入來源,並提升整體市場知名度。

電信和網路管理領域的基於代理的人工智慧市場受益於平台供應商和服務合作夥伴之間的共生循環。隨著平台日趨成熟,它們會開放細粒度的API,從而促進第三方模組的開發。這形成了一個良性循環,推動了對整合和DevOps人才的需求。該循環加速了創新步伐,同時使營運商能夠保持精簡的內部團隊。因此,服務將縮小(但不會完全消除)與解決方案之間的收入差距,從而確保在2031年整個組件堆疊中實現均衡成長。

到2025年,雲端部署將維持57.62%的市場佔有率,這主要得益於超大規模資料中心業者提供的彈性運算資源,可用於訓練大型模型。然而,隨著自動駕駛汽車和工業自動化等需要毫秒響應時間的應用場景的興起,邊緣運算(MEC)實例預計將以26.02%的複合年成長率成長。一旦營運商在基地台台統一微型資料中心部署標準,電信和網路管理領域基於代理的人工智慧的邊緣市場佔有率預計將大幅提升。領先採用者報告稱,將推理處理保留在本地,可節省15%的能源並降低回程傳輸負載。雲端策略引擎負責協調學習過程,而決策迴路則在邊緣進行,從而支援混合拓撲結構。

尤其對於受嚴格主權法規約束的營運商而言,他們需要依賴國內部署的雲端平台來實現超大規模運營,同時確保合規性。這種雲端、邊緣和本地部署的混合模式增加了生命週期管理的複雜性,也編配提供了確保模型一致性的機會。成功的解決方案將抽象化位置的複雜性,並在不影響延遲或安全性的前提下,在整個聯合層提供統一的控制平面。

區域分析

預計到2025年,北美將維持38.34%的收入佔有率,這主要得益於5G的廣泛應用、充裕的創業投資以及鼓勵創新的明確監管政策。 Verizon和T-Mobile正與Google和英偉達合作,共同開發一款最佳化引擎,已將銷售轉換率提高了40%,並降低了能源成本。該地區在電信業的AI專利申請中佔據主導地位,這為本地供應商帶來了智慧財產權優勢,同時也有利於海外授權。政府資助計畫對區域邊緣雲端的津貼,進一步擴大了符合條件的站點範圍,並加快了部署速度。

亞太地區預計將成為成長最快的市場,到2031年複合年成長率將達到25.78%。在中國,政府主導的投資正在確保全國範圍內的5G覆蓋,並建立針對通訊業者需求的先進人工智慧研究實驗室。韓國一家大型通訊業者在2024年至2025年間向人工智慧Start-Ups投資超過2.1億美元,以確保獲得新興演算法的獨家使用權。印度智慧型手機的快速普及需要基於人工智慧的頻譜效率,以便在不購買頻寬的情況下服務人口密集的都市區。全球電信人工智慧聯盟等區域合作正在促進成熟框架的跨境應用,並縮短引進週期。

歐洲在支出方面排名第三,但在隱私權保護創新方面領先,這主要得益於GDPR合規性推動了聯邦學習技術的應用。通訊業者通常會在正式部署前對可解釋代理進行試點,雖然這會延長開發週期,但有助於建立信任。為了避免巨額資本支出,南美洲傾向於透過託管服務提供經濟高效的人工智慧解決方案,而中東和非洲則致力於利用人工智慧驅動的能源最佳化來抵消不斷上漲的電價。這些市場通常具有多樣化的進入路徑,確保全球供應商能夠根據區域限制調整其產品組合。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G/6G網路複雜性的增加推動了自主編配

- 資料流量的快速成長以及對預測性網路最佳化的需求

- 為降低客戶流失率,對客戶分析的需求日益成長

- 通訊業者資本支出轉向人工智慧驅動的開放式無線存取網和虛擬無線存取網部署

- 通訊業者主權人工智慧資料中心的崛起

- 在自主現場服務運作中引入基於代理的人工智慧

- 市場限制

- 通訊業者人工智慧舉措面臨的資料隱私和監管障礙

- 通訊業者嚴重缺乏人工智慧人才

- 網路邊緣推理能耗飆升

- 使用專有AI原生網路協定棧的供應商鎖定風險

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按組件

- 解決方案/平台

- 服務

- 透過部署模式

- 雲

- 本地部署

- Edge/MEC

- 透過使用

- 客戶分析

- 網路最佳化與編配

- 詐欺和安全控制

- 虛擬助理和客戶體驗自動化

- 預測性維護

- 其他用途

- 透過網路域

- 核心網路

- 無線接取網路(RAN)

- 運輸/回程傳輸

- OSS/BSS

- 借助人工智慧技術

- 機器學習

- 自然語言處理

- 深度學習

- 人工智慧世代

- 強化學習

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- ZTE Corporation

- NEC Corporation

- Mavenir Systems, Inc.

- Parallel Wireless, Inc.

- Airspan Networks Holdings Inc.

- Rakuten Symphony Singapore Pte. Ltd.

- Amdocs Limited

- Netcracker Technology Corporation

- Ribbon Communications Inc.

- Casa Systems, Inc.

- Radisys Corporation

- Ciena Corporation

- VIAVI Solutions Inc.

- EXFO Inc.

- TEOCO Corporation

- Subex Limited

- Intracom SA Telecom Solutions

- MATRIXX Software, Inc.

- Sandvine Corporation

- DeepSig, Inc.

第7章 市場機會與未來趨勢

- 閒置頻段與未滿足需求評估

The Agentic AI in Telecommunications and Network Management market is expected to grow from USD 3.75 billion in 2025 to USD 4.63 billion in 2026 and is forecast to reach USD 13.35 billion by 2031 at 23.57% CAGR over 2026-2031.

Operators are prioritizing autonomous orchestration because 5G and emerging 6G networks require real-time optimization across millions of variables that conventional rule-based systems cannot manage. Cloud-native platforms anchor early deployments, yet rapid migration toward edge and multi-access edge computing (MEC) is underway to shave inference latency. Fraud and security management is enjoying outsized attention as adversaries adopt AI, pushing operators to embed intelligent anomaly detection at every layer. Competitive intensity is rising as network equipment makers, hyperscalers, and AI specialists form multi-vendor coalitions that promise open interfaces and faster innovation cycles. Strategic mergers in fibre and cybersecurity hint at a future where integrated connectivity and AI security become table stakes for defending market positions.

Global Agentic AI In Telecommunications And Network Management Market Trends and Insights

Rising 5G/6G Network Complexity Driving Autonomous Orchestration

Escalating antenna counts, spectrum bands, and service-level requirements make manual optimisation unworkable, prompting operators to embed autonomous agents that learn network intent and enforce it continuously. Digital Nasional Berhad achieved 99.8% uptime and a 500% alarm reduction within six months of adopting Ericsson's intent-based platform. Research for 6G suggests the orchestration burden will multiply as non-terrestrial links join terrestrial cells, reinforcing the business case. Nokia's modelling shows autonomous networks can unlock USD 800 million in annual operator benefits through combined CAPEX, OPEX, and revenue effects. Those economics drive board-level urgency to convert proof-of-concepts into production deployments at scale.

Surging Data Traffic and Need for Predictive Network Optimisation

Hourly traffic spikes fuelled by live video and AI workloads now overwhelm conventional planning cycles. Verizon's deployment of radio-intelligent controllers delivers 15% energy savings by shifting capacity ahead of surges. Operators report 30-50% reductions in congestion events when predictive agents pre-allocate resources versus reactive steps. Edge data centres intensify the challenge because inference loads appear suddenly and locally. Consequently, predictive optimisation is no longer optional for safeguarding user experience and enterprise SLA commitments.

Data-Privacy and Regulatory Hurdles for Telco AI Initiatives

GDPR and impending EU AI Act rules force operators to add explainability layers and strict data-localisation controls that stretch project timelines. Federated learning offers compliance but can triple compute costs. Cross-border operators must juggle divergent frameworks that undercut scale economies. The uncertainty prompts phased deployments and higher dependence on privacy-preserving toolkits from hyperscalers that guarantee audit readiness.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Churn-Reducing Customer Analytics

- Operator CAPEX Shift Toward AI-Powered Open RAN and vRAN Roll-outs

- Acute Shortage of Telecom-Grade AI Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions and platforms accounted for 59.65% of 2025 spending as operators sought turnkey functionality that plugs into existing OSS/BSS. Services are projected to expand at a 26.99% CAGR, outpacing the overall Agentic AI in Telecommunications and Network Management market due to customisation workstreams. The Agentic AI in Telecommunications and Network Management market size for services is forecast to widen quickly as brownfield networks require domain-specific tuning. Integration specialists orchestrate data pipelines, develop domain models, and handle lifecycle governance, functions that many operators lack in-house. They also deliver managed optimisation that continuously aligns AI agents with shifting business KPIs. Professional services revenue, therefore, rises in tandem with AI maturity phases, embedding providers deep within operator operations and creating annuity streams that lift overall market visibility.

The Agentic AI in Telecommunications and Network Management market benefits from a symbiotic cycle between platform vendors and service partners. As platforms mature, they expose granular APIs that foster third-party modules, which in turn spur demand for integration and DevOps talent. This virtuous loop accelerates innovation velocity while allowing operators to maintain lean internal teams. Consequently, services will narrow but not erase the revenue gap with solutions, ensuring balanced growth across the component stack through 2031.

Cloud deployments retained a 57.62% share in 2025 because hyperscalers supply elastic compute for training massive models. However, MEC instances are set to post a 26.02% CAGR as use cases, such as autonomous vehicles and industrial automation, demand single-digit millisecond responses. The Agentic AI in Telecommunications and Network Management market share for edge is expected to rise sharply once operators standardise micro-data-centre footprints across base-station sites. Early adopters cite 15% energy savings and reduced backhaul when inference stays local. Policy engines in the cloud still coordinate learning, yet decision loops shrink at the edge, reinforcing a hybrid topography.

Notably, operators with stringent sovereignty rules rely on on-premises clouds inside national borders, preserving compliance while retaining hyperscale-like operations. This blend of cloud, edge, and on-premises outposts complicates lifecycle management, creating room for orchestration vendors that guarantee model consistency. Winning solutions will abstract location complexity, providing a single control plane across federation layers without compromising latency or security.

Agentic AI in Telecommunications and Network Management Market Report is Segmented by Component (Solutions/Platforms and Services), Deployment Mode (Cloud and More), Application (Customer Analytics and More), Network Domain (Core Network, Radio Access Network, and More), AI Technology (Machine Learning, Natural Language Processing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.34% revenue share in 2025 owing to pervasive 5G, deep venture capital, and clear regulatory signals that reward experimentation. Verizon and T-Mobile partner with Google and NVIDIA to co-create optimisation engines that have already lifted sales conversions by 40% and trimmed energy bills. The region also commands the lion's share of AI patent filings in telecoms, giving local vendors an intellectual-property edge that travels well when licensing abroad. Government funding programmes that subsidise rural edge clouds further expand addressable sites, accelerating rollout velocity.

Asia-Pacific is projected to post a 25.78% CAGR to 2031, making it the fastest-expanding theatre. China's state-backed investments guarantee nationwide 5G coverage and seed advanced AI research labs that dovetail with operator needs. South Korea's leading telcos invested over USD 210 million in AI start-ups during 2024-2025 to secure exclusive access to emerging algorithms. India, propelled by surging smartphone adoption, demands AI-based spectral efficiency to serve dense urban clusters without exhaustive spectrum purchases. Regional collaborations, such as the Global Telco AI Alliance, spread proven frameworks across borders, compressing deployment cycles.

Europe ranks third in spending but first in privacy-preserving innovation as GDPR compliance drives adoption of federated learning. Operators often pilot explainable agents before turning them loose in production, lengthening timelines yet fostering trust. South America favours cost-efficient AI delivered via managed services to sidestep capex spikes, while the Middle East and Africa pursue AI-enabled energy optimisation to offset high power costs. Collectively, these markets demonstrate diverse entry paths, ensuring global suppliers tailor portfolios to local constraints.

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- ZTE Corporation

- NEC Corporation

- Mavenir Systems, Inc.

- Parallel Wireless, Inc.

- Airspan Networks Holdings Inc.

- Rakuten Symphony Singapore Pte. Ltd.

- Amdocs Limited

- Netcracker Technology Corporation

- Ribbon Communications Inc.

- Casa Systems, Inc.

- Radisys Corporation

- Ciena Corporation

- VIAVI Solutions Inc.

- EXFO Inc.

- TEOCO Corporation

- Subex Limited

- Intracom S.A. Telecom Solutions

- MATRIXX Software, Inc.

- Sandvine Corporation

- DeepSig, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising 5G/6G network complexity driving autonomous orchestration

- 4.2.2 Surging data traffic and need for predictive network optimisation

- 4.2.3 Growing demand for churn-reducing customer analytics

- 4.2.4 Operator CAPEX shift toward AI-powered Open RAN and vRAN roll-outs

- 4.2.5 Emergence of sovereign AI data-centres operated by telcos

- 4.2.6 Adoption of agentic AI for autonomous field-service operations

- 4.3 Market Restraints

- 4.3.1 Data-privacy and regulatory hurdles for telco AI initiatives

- 4.3.2 Acute shortage of telecom-grade AI talent

- 4.3.3 Escalating inference energy costs at network edge

- 4.3.4 Vendor lock-in risk in proprietary AI-native network stacks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions/Platforms

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Edge/MEC

- 5.3 By Application

- 5.3.1 Customer Analytics

- 5.3.2 Network Optimisation and Orchestration

- 5.3.3 Fraud and Security Management

- 5.3.4 Virtual Assistants and CX Automation

- 5.3.5 Predictive Maintenance

- 5.3.6 Other Applications

- 5.4 By Network Domain

- 5.4.1 Core Network

- 5.4.2 Radio Access Network (RAN)

- 5.4.3 Transport/Backhaul

- 5.4.4 OSS/BSS

- 5.5 By AI Technology

- 5.5.1 Machine Learning

- 5.5.2 Natural Language Processing

- 5.5.3 Deep Learning

- 5.5.4 Generative AI

- 5.5.5 Reinforcement Learning

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Telefonaktiebolaget LM Ericsson

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Nokia Corporation

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Juniper Networks, Inc.

- 6.4.7 ZTE Corporation

- 6.4.8 NEC Corporation

- 6.4.9 Mavenir Systems, Inc.

- 6.4.10 Parallel Wireless, Inc.

- 6.4.11 Airspan Networks Holdings Inc.

- 6.4.12 Rakuten Symphony Singapore Pte. Ltd.

- 6.4.13 Amdocs Limited

- 6.4.14 Netcracker Technology Corporation

- 6.4.15 Ribbon Communications Inc.

- 6.4.16 Casa Systems, Inc.

- 6.4.17 Radisys Corporation

- 6.4.18 Ciena Corporation

- 6.4.19 VIAVI Solutions Inc.

- 6.4.20 EXFO Inc.

- 6.4.21 TEOCO Corporation

- 6.4.22 Subex Limited

- 6.4.23 Intracom S.A. Telecom Solutions

- 6.4.24 MATRIXX Software, Inc.

- 6.4.25 Sandvine Corporation

- 6.4.26 DeepSig, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

AMD公司:GPU、APU、DPU和AI網卡的全球部署狀況

AMD公司:GPU、APU、DPU和AI網卡的全球部署狀況 2026年全球通訊領域生成式人工智慧市場報告2026年全球人工智慧(AI)光纖網路控制器市場報告2026年全球通訊產業人工智慧市場報告

2026年全球通訊領域生成式人工智慧市場報告2026年全球人工智慧(AI)光纖網路控制器市場報告2026年全球通訊產業人工智慧市場報告 2026-2034年通訊產業人工智慧(AI)全球市場規模、佔有率、趨勢和成長分析報告人工智慧驅動的通訊產業:拉丁美洲,2024-2030 年

2026-2034年通訊產業人工智慧(AI)全球市場規模、佔有率、趨勢和成長分析報告人工智慧驅動的通訊產業:拉丁美洲,2024-2030 年 電信人工智慧市場平台市場,全球預測至2032年:按組件、平台類型、主要用例、組織類型、技術、最終用戶和地區分類

電信人工智慧市場平台市場,全球預測至2032年:按組件、平台類型、主要用例、組織類型、技術、最終用戶和地區分類 人工智慧原生電信業者的崛起正在重塑電信經濟格局:26 個人工智慧案例研究展現電信營運與獲利模式

人工智慧原生電信業者的崛起正在重塑電信經濟格局:26 個人工智慧案例研究展現電信營運與獲利模式 2026-2030年全球通訊業人工智慧(AI)市場

2026-2030年全球通訊業人工智慧(AI)市場 人工智慧輸入市場按產品類型、技術、輸入方式、分銷管道、應用和最終用戶產業分類-2026-2032年全球預測

人工智慧輸入市場按產品類型、技術、輸入方式、分銷管道、應用和最終用戶產業分類-2026-2032年全球預測