|

市場調查報告書

商品編碼

1934824

歐洲家庭能源管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Europe Home Energy Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

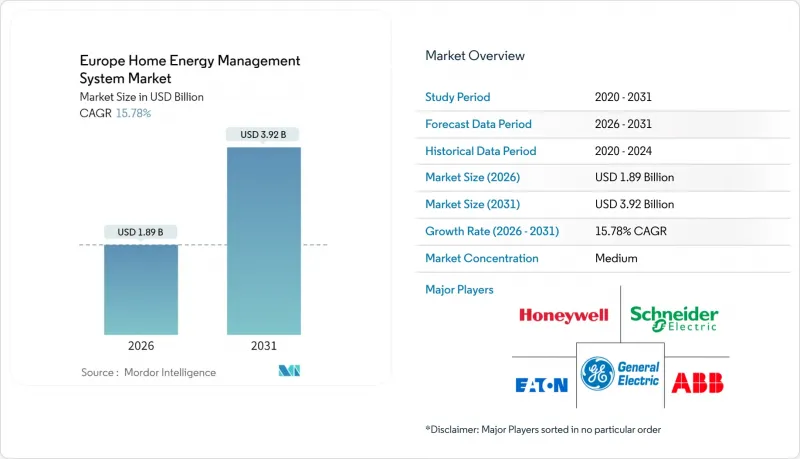

2025年歐洲家庭能源管理系統市值為16.3億美元,預計2031年將達到39.2億美元,高於2026年的18.9億美元。

預測期(2026-2031 年)的複合年成長率預計為 15.78%。

歐盟清潔能源一攬子計畫強制推廣智慧電錶,加上住宅用電價格持續上漲以及空間供暖和交通電氣化進程加速,共同為需求成長創造了有利環境。德國自2025年起強制在6000至10萬千瓦時用電量區間部署智慧電錶,西班牙全面實施動態收費系統,以及英國的分級需求柔軟性計劃,都體現了政策的廣泛一致性。基於物質而非執行緒的技術與人工智慧驅動的分析技術的融合,正在縮短投資回收期並簡化設備部署。如今,競爭策略強調建構生態系統夥伴關係,將能源、暖通空調、太陽能、電池和電動車充電控制整合起來,並透過統一的使用者介面進行管理。

歐洲家庭能源管理系統市場趨勢與洞察

歐盟清潔能源一攬子計畫強制推行智慧電錶。

2023年修訂的德國《計量營運法》設定了中期目標,即到2025年底再生能源滲透率達到20%,到2030年達到95%。隨著可再生能源滲透率的提高,電力系統營運商需要詳細的用電數據來進行靈活的負載調整。截至2024年9月,已安裝100萬台設備,是2023年之前安裝速度的三倍。然而,儘管歐洲標準化委員會(CEN)和歐洲電工標準化委員會(CENELEC)制定了最低網路安全規範,但成員國之間標準的差異仍然造成了市場碎片化的風險。

能源危機後家庭用電價格上漲

2024年底,歐洲住宅平均電費將達到每100度28.72歐元,較2019年上漲35%。德國住宅的平均電價將達到每100千瓦時39.43歐元,這進一步凸顯了需求面柔軟性的投資價值。浮動電價合約可在可再生能源使用高峰期降低34%的電費,但儘管強制性費率方案即將實施,家庭用戶對此的認知度僅為27%。

與傳統控制設備相比,初始硬體成本較高

一套完整的家庭能源管理系統(HEMS)平均安裝成本為1000歐元,遠高於價格在50-100歐元之間的恆溫器替代方案,阻礙了其在價格敏感地區的普及。訂閱模式雖然可以降低安裝成本,但每月10-20歐元的費用累積一筆不小的開支,令人擔憂其終身成本。由於零件短缺,預計到2024年半導體成本將上漲15-25%,這意味著即使太陽能板每年可節省400-500歐元,對於沒有安裝太陽能板的家庭來說,投資回收期也可能需要三年或更長時間。

細分市場分析

截至2025年,硬體將佔家庭能源管理系統市場的54.45%,凸顯了智慧電錶閘道和智慧控制器強制安裝對市場的影響。服務板塊22.90%的複合年成長率反映了市場對訂閱式最佳化服務日益成長的需求,而公用事業雲分析的普及也使需求更加多元化。服務套餐對預算有限的家庭極具吸引力,因為它們可以減少維護需求,並將資本支出轉化為營運支出。邊緣運算對於電壓調節和頻率響應等對延遲敏感的功能仍然至關重要。雖然供應商正在整合無線韌體更新以延長硬體壽命,但不同的訂閱等級透過更深入的分析、需量反應參與和點對點交易存取等功能來區分彼此。

智慧電錶強制安裝的持續推進將保持硬體收入的強勁成長。然而,到2031年,平台提供者將把持續服務定位為關鍵的收入促進因素,並將第三方設備部署支援和與保險公司關聯的安全診斷服務捆綁在一起。軟硬體的整合實現了即時雙向通訊,使Schneider Electric、ABB和Leglan等公司能夠利用現有的電力基礎設施交叉銷售其服務。在不斷擴大的住宅能源管理系統(HEMS)服務市場規模的推動下,家庭能源管理系統服務的市場規模預計將快速成長,這得益於不斷增加的住宅柔軟性監管獎勵。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟清潔能源一攬子計畫強制推行智慧電錶。

- 能源危機後,居民電費飆升

- 住宅電氣化需要負載平衡(熱泵和電動車充電器)

- 公共產業主導的需求需量反應激勵計劃

- 人工智慧驅動的直升機緊急醫療服務應用程式將投資回收期縮短至三年以內

- 零售能源領域「彈性交易」帶來的產消者收入來源

- 市場限制

- 與傳統控制系統相比,初始硬體成本較高

- 設備標準分散(Zigbee、Thread、Matter 等)

- 關於分散式消費者載入資料的網路隱私問題

- 歐盟國家延遲引進浮動關稅制度

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 依產品類型

- 照明控制系統

- 自我監控系統和服務

- 可程式設計的恆溫器

- 高級中央控制設備

- 智慧暖通空調控制器

- 透過技術

- Zigbee

- Wi-Fi

- 網際網路

- Z-Wave

- 其他

- 按國家/地區

- 英國

- 德國

- 法國

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric

- Eaton Corporation

- ABB Group

- General Electric

- Honeywell International

- tado GmbH

- Netatmo

- Legrand Group

- EnergyHub

- Johnson Controls

- OVO Energy

- E.ON Group

- tado GmbH

- Sonnen GmbH

- Netatmo

- Hive(Home Serve)

- Devolo AG

- Legrand Group

- Thermondo

- Deutsche Telekom(Magenta SmartHome)

第7章 市場機會與未來展望

The Europe Home Energy Management System Market was valued at USD 1.63 billion in 2025 and estimated to grow from USD 1.89 billion in 2026 to reach USD 3.92 billion by 2031, at a CAGR of 15.78% during the forecast period (2026-2031).

Mandatory smart meter deployments under the EU Clean Energy Package intersect with sustained residential electricity price inflation and accelerated electrification of space heating and mobility, creating a fertile demand environment. Germany's regulatory mandate for smart meters in the 6,000-100,000 kWh consumption bracket starting 2025, Spain's fully rolled-out dynamic tariff framework, and the United Kingdom's scaled demand-flexibility programs together illustrate widespread policy alignment. Technology convergence around Matter-over-Thread and artificial-intelligence-enabled analytics lowers payback periods and simplifies device onboarding. Competitive strategies now favor ecosystem partnerships that integrate energy, HVAC, solar, battery, and electric-vehicle-charging controls behind unified user interfaces.

Europe Home Energy Management System Market Trends and Insights

Mandatory smart-meter roll-outs under EU Clean Energy Package

Revisions to Germany's Messstellenbetriebsgesetz in 2023 set interim smart-meter milestones of 20% by end-2025, moving toward 95% coverage by 2030. Grid operators require granular consumption data to coordinate flexible loads amid rising renewable penetration. One million units had been installed by September 2024, triple the pre-2023 pace. Variability across member-state standards, however, risks market fragmentation even as CEN-CENELEC develops minimum cybersecurity specifications.

Soaring household electricity prices post-energy crisis

Average European residential tariffs rested at EUR 28.72 per 100 kWh in late 2024, 35% above 2019 levels. German households faced EUR 39.43 per 100 kWh, buttressing investment cases for demand-side flexibility. Dynamic contracts enable 34% bill savings during high-renewable periods, yet household awareness stands at 27% despite upcoming mandatory tariff offerings.

High upfront hardware cost vs. traditional controls

Comprehensive HEMS installations average EUR 1,000, dwarfing EUR 50-100 thermostat alternatives, discouraging adoption in price-sensitive regions. Subscription models cut entry costs but accumulate EUR 10-20 monthly fees, raising lifetime expense concerns. Component shortages raised semiconductor costs 15-25% in 2024, stretching payback times to beyond three years for non-solar homes, even when savings reach EUR 400-500 annually for solar-equipped households.

Other drivers and restraints analyzed in the detailed report include:

- Residential electrification needing load orchestration

- Utility-led demand-response incentive programmes

- Fragmented device standards creating interoperability challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 54.45% of the home energy management system market in 2025, underscoring the impact of mandatory smart meter gateways and intelligent controllers. Utility cloud analytics are now diverging demand, and the services segment's 22.90% CAGR reflects rising appetite for subscription-based optimization. Services bundles offload maintenance requirements and shift capital expenditure into operating expenditure, attracting budget-constrained households. Edge-based processing remains critical for latency-sensitive functions such as voltage regulation and frequency response. Vendors integrate over-the-air firmware updates that prolong hardware lifespan, yet subscription tiers differentiate on analytics depth, demand-response participation, and peer-to-peer trading access.

Continued smart-meter mandates ensure hardware revenue resilience. Nevertheless, platform providers position recurring services as the primary revenue driver by 2031, bundling third-party device onboarding and insurer-linked safety diagnostics. Hardware-software convergence empowers real-time bidirectional communication, and Schneider Electric, ABB, and Legrand leverage their installed electrical backbones to cross-sell services. The home energy management system market size for services is projected to expand rapidly, supported by growing regulatory incentives for residential flexibility.

The Europe Home Energy Management System Market Report is Segmented by Component (Hardware, Software, and Services), Product Type (Lighting Controls, Self-Monitoring Systems and Services, Programmable Communicating Thermostats, Advanced Central Controllers, Intelligent HVAC Controller, and More), Technology (Z-Wave, Zigbee, Wi-Fi, Internet, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Schneider Electric

- Eaton Corporation

- ABB Group

- General Electric

- Honeywell International

- tado GmbH

- Netatmo

- Legrand Group

- EnergyHub

- Johnson Controls

- OVO Energy

- E.ON Group

- tado GmbH

- Sonnen GmbH

- Netatmo

- Hive (Home Serve)

- Devolo AG

- Legrand Group

- Thermondo

- Deutsche Telekom (Magenta SmartHome)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory smart-meter roll-outs under EU Clean Energy Package

- 4.2.2 Soaring household electricity prices post-energy crisis

- 4.2.3 Residential electrification (heat pumps and EV chargers) needing load orchestration

- 4.2.4 Utility-led demand-response incentive programmes

- 4.2.5 AI-enabled HEMS apps lowering payback to <3 yrs

- 4.2.6 Retail-energy "Flexibility Trading" revenue streams for prosumers (under-reported)

- 4.3 Market Restraints

- 4.3.1 High upfront hardware cost vs. traditional controls

- 4.3.2 Fragmented device standards (Zigbee, Thread, Matter, etc.)

- 4.3.3 Consumer cyber-privacy concerns on granular load data

- 4.3.4 Slow roll-out of dynamic tariffs in several EU states (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Product Type

- 5.2.1 Lighting Controls

- 5.2.2 Self-Monitoring Systems and Services

- 5.2.3 Programmable Communicating Thermostats

- 5.2.4 Advanced Central Controllers

- 5.2.5 Intelligent HVAC Controllers

- 5.3 By Technology

- 5.3.1 Zigbee

- 5.3.2 Wi-Fi

- 5.3.3 Internet

- 5.3.4 Z-Wave

- 5.3.5 Others

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric

- 6.4.2 Eaton Corporation

- 6.4.3 ABB Group

- 6.4.4 General Electric

- 6.4.5 Honeywell International

- 6.4.6 tado GmbH

- 6.4.7 Netatmo

- 6.4.8 Legrand Group

- 6.4.9 EnergyHub

- 6.4.10 Johnson Controls

- 6.4.11 OVO Energy

- 6.4.12 E.ON Group

- 6.4.13 tado GmbH

- 6.4.14 Sonnen GmbH

- 6.4.15 Netatmo

- 6.4.16 Hive (Home Serve)

- 6.4.17 Devolo AG

- 6.4.18 Legrand Group

- 6.4.19 Thermondo

- 6.4.20 Deutsche Telekom (Magenta SmartHome)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2034年智慧家居能源基礎設施整合市場預測-按產品類型、組件、服務模式、部署方式、應用領域、最終用戶和地區分類的全球分析

2034年智慧家居能源基礎設施整合市場預測-按產品類型、組件、服務模式、部署方式、應用領域、最終用戶和地區分類的全球分析 家庭能源管理系統市場分析:按產品類型、通訊技術、系統類型和地區分類(2026-2034 年)

家庭能源管理系統市場分析:按產品類型、通訊技術、系統類型和地區分類(2026-2034 年) 家庭能源管理系統市場:按組件、產品類型、通訊技術、最終用戶和應用分類-2026-2032年全球市場預測

家庭能源管理系統市場:按組件、產品類型、通訊技術、最終用戶和應用分類-2026-2032年全球市場預測 住宅自動馬達啟動器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、解決方案分類智慧家庭能源管理系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能及安裝類型分類

住宅自動馬達啟動器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、解決方案分類智慧家庭能源管理系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能及安裝類型分類 全球家庭能源管理系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球家庭能源管理系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 智慧家庭能源管理設備市場-全球產業規模、佔有率、趨勢、機會、預測:按組件、通訊技術、地區和競爭對手分類,2021-2031年

智慧家庭能源管理設備市場-全球產業規模、佔有率、趨勢、機會、預測:按組件、通訊技術、地區和競爭對手分類,2021-2031年 家庭能源管理系統市場規模、佔有率和成長分析(按組件、技術、應用、最終用戶和地區分類)—2026-2033年產業預測

家庭能源管理系統市場規模、佔有率和成長分析(按組件、技術、應用、最終用戶和地區分類)—2026-2033年產業預測 區域能源服務市場按服務類型、能源來源、技術、最終用戶和地區分類2032 年家庭能源管理市場預測:按組件、負載、技術、應用、最終用戶和地區進行的全球分析

區域能源服務市場按服務類型、能源來源、技術、最終用戶和地區分類2032 年家庭能源管理市場預測:按組件、負載、技術、應用、最終用戶和地區進行的全球分析