|

市場調查報告書

商品編碼

1934806

輪胎輪胎邊緣圈鋼絲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Tire Bead Wire - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

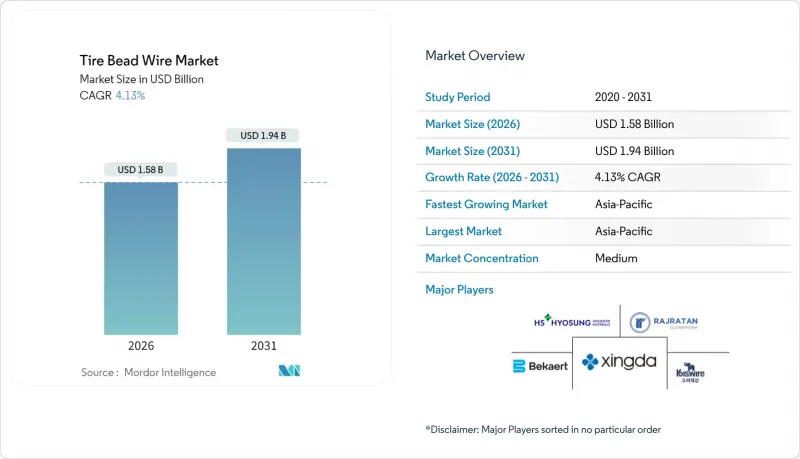

預計到 2025 年,輪胎輪胎邊緣鋼絲市場價值將達到 15.2 億美元,預計在預測期(2026-2031 年)內將以 4.13% 的複合年成長率成長,從 2026 年的 15.8 億美元成長到 2031 年的 19.4 億美元。

輪胎輪胎邊緣鋼絲市場正受益於一系列結構性利多因素,包括亞太地區大型汽車組裝廠的擴張、全球安全法規的加強(鼓勵使用更高等級的增強材料)以及負責電子商務運輸的商用車車隊加速更換。高抗張強度延展性的鋼絲能夠實現更窄的輪胎邊緣截面,從而降低輪圈打滑風險並減輕輪胎重量,進而提升主導價值。這項特性提高了乘用車和電動貨車的滾動效率。製造商不斷升級熔爐和拉絲生產線,以生產雜質含量極低的超純高碳鋼。同時,對光學檢測和雷射缺陷檢測的投資正在提升製程能力,並有助於滿足OEM輪胎製造商對長保固週期的要求。市場競爭格局依然複雜:大型垂直整合企業透過長期合約確保鋼材供應,而中型企業則透過從多個地區採購或混合廢鋼來規避價格波動風險。

全球輪胎輪胎邊緣鋼絲市場趨勢及洞察

全球汽車產量增加

全球汽車製造業的復甦帶動了對輪胎輪胎邊緣鋼絲的持續需求,促使輪胎製造商在2024年投資創紀錄的130億美元用於新工廠建設和產能擴張。墨西哥的輪胎產業是這項擴張的典型代表,Yokohama Rubber、中作和賽潤等公司投資超過10億美元用於新計畫,將產能提升至1億條以上。這些工廠策略性地位置於主要汽車市場附近,既降低了物流成本,也滿足了嚴格的供應鏈要求。柬埔寨也正在崛起為重要的製造地,預計到2025年,其輪胎製造投資將達到3.35億美元,使其成為全球輪胎供應鏈的重要參與者。產能的地理多元化為輪胎邊緣鋼絲供應商創造了多個需求中心,降低了集中風險,同時擴大了市場機會。

航空航太輪胎需求不斷成長

航太領域的強勁復甦催生了對高性能輪胎邊緣圈鋼絲的特殊需求。飛機輪胎在極端條件下運作,需要輪胎邊緣鋼絲具備卓越的抗張強度和抗疲勞性能。這些高標準要求推高了輪胎價格,並推動了整個輪胎產業的創新。美國聯邦航空管理局(FAA)針對飛機輪胎翻新和維修制定的嚴格維護標準(諮詢通告AC 145-4A)也進一步增加了對替換輪胎邊緣鋼絲組件的需求。不斷成長的軍事開支(預計2024年美國國防預算將達到約8,860億美元)進一步支撐了國防車輛和飛機專用輪胎的應用。這一細分領域的技術需求往往會催生創新,最終惠及商用輪胎,因此航太的需求也成為更廣泛市場發展的催化劑。

鋼鐵和銅價格波動

經濟學人智庫 (EIU) 預測,2025 年和 2026 年工業原物料指數將雙雙上漲,推動橡膠價格升至每噸 2,643 美元。這將進一步推高鋼鐵原料成本。每當高碳鋼筋價格與能源關稅同步上漲時,由於生產商與輪胎製造商簽訂了為期六個月的合約以鎖定價格,輪胎邊緣利潤率就會下降。來自柬埔寨、越南、印度和泰國的低成本輪胎進口使得美國卡車輪胎價格在 2024 年全年保持穩定。這給國內線材製造商帶來了壓力,儘管鋼鐵成本上漲,他們卻無法將附加費轉嫁給消費者。匯率波動加劇了不不確定性。例如,人民幣突然貶值會使中國鋼筋出口價格下降,一夕之間重塑全球基準價格。為了生存,二手鋼供應商正在尋求金融避險和廢鋼混合最佳化,但這些策略都無法在價格突然飆升時完全保障息稅前利潤率。

細分市場分析

2025年,高抗張強度鋼絲桿佔輪胎輪胎邊緣鋼絲市場的56.63%,預計到2031年將以4.59%的複合年成長率成長,這主要得益於監管機構和車隊營運商對延長保固期的日益重視。製程創新至關重要:真空脫氣可降低氫孔隙率,而鈣注入則可控制硫化物形態,從而防止脆性斷裂。模擬研究表明,將TiN含量降低至0.003%以下(重量比)可使拉絲過程中的斷絲率降低24%,從而降低廢品率並提高交貨可靠性。

市場需求日益分散。乘用車輪胎製造商現在要求缺氣保用輪胎的抗張強度達到2500兆帕至3000兆帕,而電動車製造商則要求更精細的胎圈厚度,這就需要更純淨的微觀結構。航太輪胎產量較小,需要抗張強度為3400兆帕、在60%載重下抗裂紋擴展能力超過100萬次循環的鋼絲,這規格鮮有製造商能夠滿足。常規抗張強度等級的鋼絲在對成本敏感的細分市場(例如小型摩托車和農業機械)仍然有需求,但由於商品化帶來的競爭加劇,它們面臨著價格壓力。

輪胎輪胎邊緣鋼絲市場報告按等級(高抗張強度和普通鋼絲)、類型(子午線鋼絲和斜交鋼絲)、應用領域(乘用車輪胎、商用車輪胎、其他輪胎)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元以金額為準。

區域分析

預計到2025年,亞太地區將佔全球收入的40.02%,並在2031年之前以5.41%的複合年成長率加速成長,這主要得益於中國輪胎行業2024年前三季度24.28%的收入成長和1922萬條的產量成長。輪胎輪胎邊緣市場也受惠於印度政府的生產連結獎勵計畫計畫(PLI),該計畫對鋼鐵原料提供進口關稅退稅,進一步降低了新增產能的成本門檻。

儘管北美市場已趨於成熟,但其主要集中在高階電動車和航太產品線,這些領域對輪胎邊緣線材的潔淨度有著絕對的要求。安賽樂米塔爾位於阿拉巴馬州的工廠為馬達供應層壓鋼板和超高純度SWRH線材,不僅為位於阿肯色州的貝克特公司提供了在地採購原料,還降低了運輸風險。該公司於2024年投資新建了一座拉絲廠,並新增了38名員工。

在歐洲,德國和波蘭的輪胎生產保持穩定,主要由高階輪胎品牌營運。歐盟綠色交易的嚴格目標正迫使輪胎邊緣胎廠轉型使用可再生能源驅動的電弧爐和水性潤滑劑,以減少揮發性有機化合物(VOC)的排放。墨西哥和柬埔寨等新興地區正崛起為二級生產中心。預計到2026年後,墨西哥的輪胎產量將超過1億條,將使美國汽車製造商的輪胎供應來源更加多元化。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球汽車產量增加

- 航空航太輪胎需求不斷成長

- 子午線輪胎在開發中國家的快速普及

- 電動車專用低滾動阻力輪胎輪胎邊緣設計快速成長

- 高彈性模量混合輪胎邊緣增強材料的研發

- 市場限制

- 鋼鐵和銅價格波動

- 加強拉絲製程排放的環境法規

- 高碳鋼棒材供應集中風險

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按年級

- 高抗張強度

- 普通抗張強度

- 按類型

- 子午線輪胎

- 斜交輪胎

- 透過使用

- 乘用車輪胎

- 商用車輛輪胎

- 其他輪胎

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aarti Steel International Limited

- Arcelor Mittal

- Bekaert

- Daye Co., Ltd.

- HBT RUBBER INDUSTRIAL CO.,LTD

- HS HYOSUNG ADVANCED MATERIALS

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Kiswire Ltd.

- Rajratan Global Wire Limited

- Shandong Xinhao Tire Materials Co., Ltd.

- Shanghai Metal Corporation

- SNTAI INDUSTRIAL GROUP LTD.

- TIANJIN BLADDER TECHNOLOGY CO.,LTD

- WireCo

第7章 市場機會與未來展望

The Tire Bead Wire Market was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 1.94 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031).

The tire bead wire market enjoys a structural tailwind from Asia-Pacific's large-scale vehicle assembly plants, stricter global safety regulations that favor premium reinforcement materials, and an accelerating replacement cycle among commercial fleets that carry e-commerce traffic. High-tensile grades with enhanced ductility dominate value because they reduce rim-slip risk and permit narrower bead sections that save tire weight, an attribute that boosts rolling efficiency for passenger cars and electric vans alike. Manufacturers continue upgrading furnaces and wire-drawing lines to produce ultraclean high-carbon steel that minimizes inclusions; concurrent investments in optical inspection and laser flaw detection improve process capability and support the longer warranty cycles expected by original-equipment tire makers. Competitive dynamics remain mixed: vertically integrated giants secure raw-steel rod under long-term contracts, while mid-tier firms hedge volatility through multi-regional sourcing and scrap-steel blending.

Global Tire Bead Wire Market Trends and Insights

Rising Global Vehicle Production

Global automotive production recovery has created sustained demand for tire bead wire, with tire manufacturers investing a record USD 13 billion in new factories and capacity expansions during 2024. Mexico's tire industry exemplifies this expansion, with production capacity expected to exceed 100 million tires as companies like Yokohama, Zhongce, and Sailun allocate over USD 1 billion for new projects. The strategic positioning of these facilities near major automotive markets reduces logistics costs while meeting stringent supply chain requirements. Cambodia has emerged as another significant manufacturing hub, attracting USD 335 million in tire manufacturing investments during 2025, positioning the country as a key player in the global tire supply chain. This geographic diversification of production capacity creates multiple demand centers for bead wire suppliers, reducing concentration risks while expanding market opportunities.

Expanding Demand from Aviation and Aerospace Tyres

The aerospace sector's robust recovery has generated specialized demand for high-performance bead wire applications. Aircraft tires operate under extreme conditions requiring bead wire with exceptional tensile strength and fatigue resistance, specifications that command premium pricing and drive technological advancement across the broader tire industry. The FAA's stringent maintenance standards for aircraft tire retreading and repair create additional demand for replacement bead wire components, as outlined in Advisory Circular AC 145-4A. Military spending increases, with the U.S. defense budget projected at approximately USD 886 billion for 2024, further support specialized tire applications in defense vehicles and aircraft. This niche segment's technical requirements often pioneer innovations that eventually cascade into commercial tire applications, making aerospace demand a catalyst for broader market advancement.

Volatile Steel and Copper Prices

The Economist Intelligence Unit expects industrial raw-material indices to rise in both 2025 and 2026, sending rubber to USD 2,643 per tonne and pushing ferrous feedstock costs upward. Bead-wire margins shrink whenever high-carbon rod moves in tandem with energy tariffs because producers fix prices under six-month tire-maker contracts. Imports of low-priced tires from Cambodia, Vietnam, India, and Thailand kept U.S. truck-tire prices level during 2024 even as steel costs advanced, creating a squeeze for domestic wire-drawers who cannot pass through surcharges. Currency swings layer on additional unpredictability; a sudden yuan depreciation, for instance, cheapens Chinese rod exports and resets global reference prices overnight. To survive, tier-two vendors engage in financial hedging and scrap-mix optimization, but neither fully shields EBIT margins during sharp spikes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Penetration of Radial Tyres in Developing Economies

- Surge in EV-Specific Bead Designs for Low Rolling-Resistance Tyres

- Tightening Environmental Rules on Wire-Drawing Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-tensile wire supplied 56.63% of tire bead wire market share in 2025, and this slice will expand at 4.59% CAGR through 2031 as regulators and fleet operators favor longer warranty periods. Process innovation is central: vacuum-degassing cuts hydrogen porosity, while calcium-injection controls sulfide morphology to curb brittle failure. Simulation work shows that reducing TiN inclusions below 0.003% by weight slashes wire-drawing breakage incidents by 24%, lowering scrap rates and improving delivery reliability.

Demand granularity is shifting. Passenger-car tire makers now specify tensile strengths of 2,500 MPa and up to 3,000 MPa for run-flat platforms, while EV manufacturers request slender bead gauges that necessitate even cleaner microstructures. Aerospace tires, though low volume, demand 3,400 MPa wire with crack-propagation resistance exceeding 1 million cycles at 60% load, a specification that only a handful of mills can meet. Regular-tensile grades still occupy cost-sensitive niches such as small two-wheel applications and agricultural equipment but face downward price pressure due to commoditized competitive rivalry.

The Tire Bead Wire Report is Segmented by Grade (High-Tensile Strength and Regular-Tensile Strength), Type (Radial Tyres and Bias Tyres), Application (Passenger Vehicle Tires, Commercial Vehicle Tires, and Other Tires), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific furnished 40.02% of global revenue in 2025 and will accelerate at a 5.41% CAGR to 2031, anchored by China's 24.28% tire-industry revenue leap and its 19.22 million-unit output surge during the first three quarters of 2024. The tire bead wire market benefits from government incentives in India that refund import duties on raw steel under the Production Linked Incentive scheme, further lowering cost barriers for new capacity.

North America, while mature, focuses on premium EV and aerospace lines where bead-wire cleanliness is non-negotiable. ArcelorMittal's Alabama mill will supply both electric-motor laminations and ultra-pure SWRH wire rod, providing local feedstock that mitigates freight risk for Arkansas-based Bekaert, which itself invested in new drawing equipment and 38 additional jobs in 2024.

Europe maintains steady volume mainly in Germany and Poland where premium tire brands operate. Stringent EU Green Deal objectives push bead-wire plants toward renewable-energy electric arc furnaces and force a transition to water-based lubricants that curb volatile-organic-compound emissions. Emerging geographies such as Mexico and Cambodia establish themselves as secondary hubs; Mexico's output will breach 100 million tires post-2026, a shift that diversifies sourcing for U.S. vehicle OEMs.

- Aarti Steel International Limited

- Arcelor Mittal

- Bekaert

- Daye Co., Ltd.

- HBT RUBBER INDUSTRIAL CO.,LTD

- HS HYOSUNG ADVANCED MATERIALS

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Kiswire Ltd.

- Rajratan Global Wire Limited

- Shandong Xinhao Tire Materials Co., Ltd.

- Shanghai Metal Corporation

- SNTAI INDUSTRIAL GROUP LTD.

- TIANJIN BLADDER TECHNOLOGY CO.,LTD

- WireCo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Vehicle Production

- 4.2.2 Expanding Demand from Aviation and Aerospace Tyres

- 4.2.3 Rapid Penetration of Radial Tyres in Developing Economies

- 4.2.4 Surge in EV-Specific Bead Designs for Low Rolling-Resistance Tyres

- 4.2.5 Development of High-Modulus Hybrid Bead Reinforcements

- 4.3 Market Restraints

- 4.3.1 Volatile Steel and Copper Prices

- 4.3.2 Tightening Environmental Rules on Wire-Drawing Emissions

- 4.3.3 Concentration Risk in High-Carbon Steel Rod Supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 High-Tensile Strength

- 5.1.2 Regular-Tensile Strength

- 5.2 By Type

- 5.2.1 Radial Tyres

- 5.2.2 Bias Tyres

- 5.3 By Application

- 5.3.1 Passenger Vehicle Tires

- 5.3.2 Commercial Vehicle Tires

- 5.3.3 Other Tires

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level overview, market level overview, core segments, financials as available, strategic information, market rank/share, products and services, recent developments)

- 6.4.1 Aarti Steel International Limited

- 6.4.2 Arcelor Mittal

- 6.4.3 Bekaert

- 6.4.4 Daye Co., Ltd.

- 6.4.5 HBT RUBBER INDUSTRIAL CO.,LTD

- 6.4.6 HS HYOSUNG ADVANCED MATERIALS

- 6.4.7 Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- 6.4.8 Kiswire Ltd.

- 6.4.9 Rajratan Global Wire Limited

- 6.4.10 Shandong Xinhao Tire Materials Co., Ltd.

- 6.4.11 Shanghai Metal Corporation

- 6.4.12 SNTAI INDUSTRIAL GROUP LTD.

- 6.4.13 TIANJIN BLADDER TECHNOLOGY CO.,LTD

- 6.4.14 WireCo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment