|

市場調查報告書

商品編碼

1934755

東南亞工業與服務機器人:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Southeast Asia Industrial And Service Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

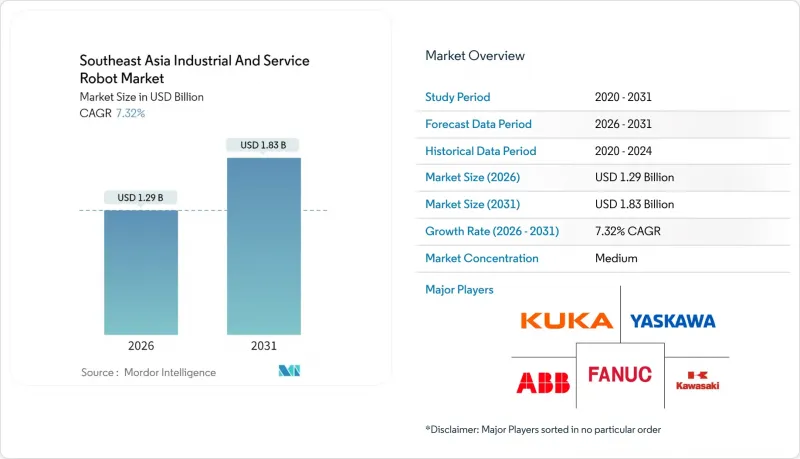

預計東南亞工業和服務機器人市場將從 2025 年的 12 億美元成長到 2026 年的 12.9 億美元,並預計到 2031 年將達到 18.3 億美元,2026 年至 2031 年的複合年成長率為 7.32%。

成熟製造地勞動力短缺日益加劇、積極的「中國+1」戰略推動供應鏈重組,以及政府對工業4.0的大力支持,共同加速了工業機器人和服務機器人的應用。泰國憑藉著東部經濟走廊(EEC)的優惠政策,目前正引領市場需求;而越南則憑藉其快速發展的電子產業,正轉型成為區域自動化中心。協作機器人(cobot)因其靈活、面積的解決方案,在中小型企業中越來越受歡迎;而重型關節機器人仍然是汽車和電子產品生產線的核心。對於尋求地理多元化和成本競爭力的全球製造商而言,東南亞的工業和服務機器人市場正成為其近岸外包策略的關鍵驅動力。

東南亞工業與服務機器人市場趨勢及洞察

東協工業4.0補助計畫加速機器人應用

東協內部的大規模財政獎勵正在降低製造商試點和擴大自動化規模的資本門檻。泰國東部經濟走廊(EEC)已撥款450億美元用於升級其高科技產業,其中機器人技術是重點發展領域。自2016年以來,新加坡已投資6,000萬新元用於40多個機器人計劃,協助Lionsbot等Start-Ups擴大自主清潔設備的生產規模。泰國投資促進委員會也正在支持價值150億泰銖的機器人計劃,目標是每年部署1萬套新系統。這些項目包括培訓津貼和測試平台,旨在彌合技能差距,並建立一個能夠支持從中小企業到跨國公司等各類企業的自我強化型生態系統。馬來西亞的「工業4.0」(Industry4WRD)和印尼的「印尼4.0」(Making Indonesia 4.0)計畫也在推行類似的政策,補貼範圍已擴展至整個東南亞的工業和服務機器人市場。

新加坡和泰國勞動力短缺加劇,推動自動化投資獲得回報

新加坡減少外籍勞工配額以及泰國人口結構的變化正在推動薪資上漲,縮小機器人與人力成本之間的差距。由於企業面臨人才短缺的困境,新加坡政府已撥款4.5億新元(約3.5336億美元),分三年推動職場自動化。在醫療保健領域,曼谷的蒙庫瓦塔納綜合醫院引入了配藥機器人,以應對護理人員短缺的問題。初步計劃的成功表明,機器人能夠快速獲得投資回報,增強了經營團隊的信心,並促使其在製造業、酒店業和物流業等其他行業中得到更廣泛的應用。

印尼和越南的高資本投資成本和低廉的勞動成本限制了投資報酬率。

廉價的移民勞動成本仍然低於許多重複性工作的機器人每小時成本,這阻礙了勞動力充裕產業的自動化普及。在印尼工廠,人工作業通常能更快收回投資,因此除了品質關鍵型任務外,自動化進程較為緩慢。越南的中小型企業也面臨類似的困境,而電子巨頭們正在實現無塵室生產線的自動化。最低工資的上漲以及像和碩聯合科技(Pegatron)的5G智慧工廠這樣的示範計劃,標誌著一個轉折點的到來:生產力的提升將超過初始資本投資。

細分市場分析

到2025年,工業機器人將佔據東南亞工業和服務機器人市場71.30%的佔有率,這主要得益於電子SMT生產線、汽車焊接單元和通用物料輸送任務的應用。關節型、SCARA型和直角坐標型機器人能夠為注重速度和精確度的終端使用者提供高重複性。同時,協作機器人(cobot)預計將以18.70%的複合年成長率成為成長最快的機器人類型,這主要得益於中小企業採用即插即用的協作機器人進行機器操作和包裝。優傲機器人(Universal Robots)已在全球售出超過10萬台協作機器人,並正在拓展銷售管道,以挖掘尚未開發的市場需求。協作機器人易於改裝到現有設備中,避免了高成本的安全圍欄,縮短了投資回收期,因此在塑膠成型、印刷電路基板組裝和食品加工等領域得到了廣泛應用。在預測期內,將大型工業機械臂與輔助協作機器人結合的混合生產線預計將在越南和泰國的工廠中廣泛應用,東南亞工業和服務機器人市場預計將發展成為一個機器人種類繁多的市場。

第二代Delta和並聯機器人滿足了食品包裝行業對超高速取放的需求,而能夠處理超過1000公斤負載的重型機器人,例如川崎重工的MG系列,則可用於造船和建築工地的貨物搬運。服務機器人雖然目前收入潛力尚小,但在醫療保健、飯店服務和公共場所清潔方面展現出巨大的潛力。這些趨勢表明,東南亞工業和服務機器人市場的硬體多樣化和軟體演進將持續進行。

待開發區工廠佔據了大部分安裝量,跨國公司在越南、馬來西亞和印尼等地建造了最先進的生產線。 AutoStore在泰國新建的模組化機器人工廠就是一個很好的例子,它透過擴大本地產能來滿足全球需求並縮短前置作業時間。東南亞工業和服務機器人市場也出現了維修計劃數量的成長。這代表著一個近期機遇,因為AutoStore 65%的「貨物搬運系統」都安裝在現有設施中(棕地)。不斷成長的維修需求鼓勵中小企業在無需徹底翻新整個工廠的情況下對老舊生產線進行現代化改造。

混合策略允許透過將新的自動化單元與現有的人工工作站結合來實現逐步擴張。轉向基於訂閱的「機器人即服務」模式進一步降低了財務風險,並吸引了新的買家,從而促進了工業和服務機器人在東南亞地區的日益普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 東協「工業4.0」補助計畫加速機器人應用

- 新加坡和泰國日益嚴重的勞動力短缺有助於提高自動化投資收益(ROI)。

- 電子產業向越南和馬來西亞等中國以外地區轉移生產基地,將提振精密組裝的需求。

- 印尼和菲律賓履約的快速成長推動了物流機器人的發展。

- 泰國和新加坡對智慧醫院的投資擴大了服務機器人的應用。

- 區域系統整合商生態系統(PBA、SYS-MAC)的成長降低了中小企業採用新技術的門檻。

- 市場限制

- 在印尼和越南,高昂的資本投資成本抵消了低廉的移民勞動成本,限制了投資收益(ROI)。

- 工廠設施分散以及樓層狀況使得整合變得更加複雜。

- 進口關稅/本地供應基礎薄弱導致機器人零件採購前置作業時間

- 新加坡以外地區熟練機器人技術人員的短缺正在減緩機器人技術的應用和服務交付。

- 價值/供應鏈分析

- 技術展望

- 監理展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按機器人類型

- 工業機器人

- 關節機器人

- SCARA機器人

- 笛卡兒機器人/龍門機器人

- 並聯機器人/ Delta機器人

- 協作機器人(cobots)

- 其他工業機器人類型

- 服務機器人

- 商用服務機器人

- 物流/倉儲業

- 醫療保健

- 農業和農田

- 檢查和維護

- 飯店業

- 家用服務機器人

- 打掃

- 護理和老年護理

- 草坪和游泳池

- 其他家用機器人類型

- 商用服務機器人

- 工業機器人

- 依承載能力(工業用途)

- 體重低於15公斤

- 16~60 kg

- 61-225 kg

- 225公斤或以上

- 按組件

- 硬體

- 機械手臂

- 控制器

- 駕駛

- 感應器

- 末端執行器

- 軟體

- 服務

- 整合與部署

- 培訓和支持

- 維護

- 硬體

- 透過使用

- 物料輸送和取放

- 焊接和釬焊

- 組裝

- 噴塗和分配

- 包裝和托盤堆垛

- 檢驗和品管

- 切割/加工

- 其他用途

- 按最終用戶行業分類

- 車

- 電子和半導體

- 金屬和機械

- 塑膠和化學品

- 食品/飲料

- 物流/倉儲業

- 衛生保健

- 零售和酒店業

- 其他(農業、建築業)

- 按安裝類型

- 新安裝

- 維修和升級

- 按公司規模

- 主要企業

- 小型企業

- 按國家/地區

- 印尼

- 馬來西亞

- 新加坡

- 泰國

- 越南

- 菲律賓

- 東南亞及其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- FANUC Corporation

- Yaskawa Electric Corporation

- ABB Ltd

- KUKA AG

- Mitsubishi Electric Corporation

- Kawasaki Heavy Industries Ltd

- Omron Corporation

- Denso Corporation

- Nachi-Fujikoshi Corp.

- Seiko Epson Corporation

- Universal Robots A/S

- Techman Robot Inc.

- Staubli International AG

- Comau SpA

- Hanwha Robotics

- Delta Electronics Inc.

- Hyundai Robotics

- PBA Robotics(Singapore)Pte Ltd

- Siasun Robot and Automation Co.

- Shibaura Machine Co. Ltd

第7章 市場機會與未來展望

The Southeast Asia industrial and service robot market is expected to grow from USD 1.20 billion in 2025 to USD 1.29 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at 7.32% CAGR over 2026-2031.

Rising labor scarcity in mature manufacturing hubs, aggressive "China-plus-one" supply-chain shifts, and a surge of government Industry 4.0 subsidies combine to accelerate uptake of both industrial and service robots. Thailand leads today's demand thanks to Eastern Economic Corridor incentives, while Vietnam's fast-growing electronics sector turns it into the region's automation hotspot. Collaborative cobots gain traction among SMEs seeking flexible, low-footprint solutions, even as heavy-duty articulated units remain core to automotive and electronics lines. The Southeast Asia industrial and service robot market is becoming a pivotal enabler of near-shoring strategies for global manufacturers that want geographic diversity and cost competitiveness.

Southeast Asia Industrial And Service Robot Market Trends and Insights

ASEAN Industry 4.0 Subsidy Programmes Accelerating Robot Uptake

Massive fiscal incentives across ASEAN are lowering capital hurdles for manufacturers to trial and scale automation. Thailand's Eastern Economic Corridor earmarked USD 45 billion for high-tech industry upgrades, with robotics highlighted as a priority. Singapore has invested SGD 60 million since 2016 into more than 40 robotics projects, enabling startups such as Lionsbot to boost production of autonomous cleaning units. Thailand's Board of Investment further facilitated robotics projects worth 15 billion baht, aiming for 10,000 new systems annually. These programs include training grants and testbeds, closing skill gaps and creating a self-reinforcing ecosystem that supports SMEs as well as multinationals. Malaysia's Industry4WRD and Indonesia's Making Indonesia 4.0 push similar agendas, extending the subsidy tailwind across the entire Southeast Asia industrial and service robot market.

Rising Labor Scarcity in Singapore and Thailand Boosting Automation ROI

Tighter foreign-worker quotas in Singapore and demographic shifts in Thailand are stoking wage inflation that narrows the cost gap between robots and humans. Singapore's government earmarked SGD 450 million (USD 353.36 million) over three years to accelerate workplace automation as companies struggle to hire. In healthcare, Bangkok's Mongkutwattana General Hospital deployed medication-dispensing robots to offset nursing shortages. Successful early projects demonstrate quick payback, reinforcing boardroom confidence and triggering wider adoption across manufacturing, hospitality, and logistics.

High Capex Versus Low Migrant-Labour Costs Limits ROI in Indonesia and Vietnam

Cheap migrant labour still undercuts robot hourly costs for many repetitive tasks, restraining uptake in labour-abundant industries. Indonesian factories often achieve faster payback through manual processes, delaying automation except in quality-critical operations. Vietnamese SMEs confront similar arithmetic even as electronics giants automate clean-room lines. Rising minimum wages and demonstration projects such as Pegatron's 5G-enabled smart factory illustrate the tipping point where premium throughput offsets initial capex.

Other drivers and restraints analyzed in the detailed report include:

- China-Plus-One Electronics Migration to Vietnam/Malaysia Lifting Precision-Assembly Demand

- E-Commerce Fulfilment Boom in Indonesia and Philippines Driving Logistics Robots

- Shortage of Advanced Robotics Talent Outside Singapore Slows Commissioning and Service

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial robots generated 71.30% of the Southeast Asia industrial and service robot market size in 2025, anchored in electronics SMT lines, automotive welding cells, and general material-handling tasks. Articulated, SCARA, and cartesian models deliver high repeatability for end-users that prioritise speed and accuracy. Meanwhile, cobots record the fastest 18.70% CAGR as SMEs adopt plug-and-play units for machine tending and packaging. Universal Robots has shipped more than 100,000 cobots worldwide and enlarged its Philippine channel to tap untapped demand. The retrofit-friendly nature of cobots sidesteps costly safety fencing and shortens payback periods, expanding reach across plastic moulding, PCB assembly, and food processing. Over the forecast horizon, hybrid lines mixing large industrial arms with auxiliary cobots will characterise factories across Vietnam and Thailand, cementing the Southeast Asia industrial and service robot market as a heterogeneous blend of form factors.

Second-generation delta and parallel robots address ultra-high-speed pick-and-place needs in food packaging, while heavy-duty 1,000 kg-plus payload units such as Kawasaki's MG series enable shipbuilding and construction handling. Service robots remain a smaller revenue slice but exhibit strong potential in healthcare, hospitality, and public-space cleaning. Combined, these patterns point to sustained hardware diversification and continual software enhancements that enrich the Southeast Asia industrial and service robot market.

Greenfield factories absorb the bulk of units as multinationals erect state-of-the-art lines in Vietnam, Malaysia, and Indonesia. AutoStore's new modular-robot factory in Thailand exemplifies the build-out of local capacity to meet global demand while cutting lead times. The Southeast Asia industrial and service robot market size for retrofit projects is also rising, representing near-term opportunities because 65% of AutoStore goods-to-person systems have been installed in brownfield sites. Retrofit momentum helps SMEs modernise legacy lines without full plant overhauls.

Hybrid strategies blend new automated cells with existing manual workstations, allowing gradual scaling. The shift towards subscription-based "robots-as-a-service" further reduces financial risk, pulling in first-time buyers and broadening the Southeast Asia industrial and service robot industry's adoption funnel.

Southeast Asia Industrial and Service Robot Market Report is Segmented by Robot Type (Industrial Robots, Service Robots), Payload Capacity (Up To 15 Kg, 16-60 Kg, and More), Component (Hardware, and More), Application (Assembly, and More), End-User Industry (Automotive, and More), Installation Type (New Installations, and More), Enterprise Size (Large Enterprises, Smes). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- FANUC Corporation

- Yaskawa Electric Corporation

- ABB Ltd

- KUKA AG

- Mitsubishi Electric Corporation

- Kawasaki Heavy Industries Ltd

- Omron Corporation

- Denso Corporation

- Nachi-Fujikoshi Corp.

- Seiko Epson Corporation

- Universal Robots A/S

- Techman Robot Inc.

- Staubli International AG

- Comau S.p.A.

- Hanwha Robotics

- Delta Electronics Inc.

- Hyundai Robotics

- PBA Robotics (Singapore) Pte Ltd

- Siasun Robot and Automation Co.

- Shibaura Machine Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ASEAN "Industry 4.0" subsidy programmes accelerating robot uptake

- 4.2.2 Rising labour scarcity in Singapore and Thailand boosting automation ROI

- 4.2.3 China-plus-one electronics migration to Vietnam/Malaysia lifting precision-assembly demand

- 4.2.4 E-commerce fulfilment boom in Indonesia and Philippines driving logistics robots

- 4.2.5 Smart-hospital capex in Thailand and Singapore expanding service-robot adoption

- 4.2.6 Growth of regional system-integrator ecosystem (PBA, SYS-MAC) reducing deployment barriers for SMEs

- 4.3 Market Restraints

- 4.3.1 High capex versus low migrant-labour costs limits ROI in Indonesia and Vietnam

- 4.3.2 Fragmented factory utilities and floor conditions complicate integration

- 4.3.3 Import tariffs/lead-times for robot components due to weak local supply base

- 4.3.4 Shortage of advanced robotics talent outside Singapore slows commissioning and service

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Robot Type

- 5.1.1 Industrial Robots

- 5.1.1.1 Articulated Robots

- 5.1.1.2 SCARA Robots

- 5.1.1.3 Cartesian / Gantry Robots

- 5.1.1.4 Parallel / Delta Robots

- 5.1.1.5 Collaborative Robots (Cobots)

- 5.1.1.6 Other Industrial Robot Types

- 5.1.2 Service Robots

- 5.1.2.1 Professional Service Robots

- 5.1.2.1.1 Logistics and Warehousing

- 5.1.2.1.2 Medical and Healthcare

- 5.1.2.1.3 Agriculture and Field

- 5.1.2.1.4 Inspection and Maintenance

- 5.1.2.1.5 Hospitality

- 5.1.2.2 Domestic Service Robots

- 5.1.2.2.1 Cleaning

- 5.1.2.2.2 Companion and Elder-care

- 5.1.2.2.3 Lawn and Pool

- 5.1.2.2.4 Other Domestic Robot Types

- 5.1.2.1 Professional Service Robots

- 5.1.1 Industrial Robots

- 5.2 By Payload Capacity (Industrial)

- 5.2.1 Up to 15 kg

- 5.2.2 16 - 60 kg

- 5.2.3 61 - 225 kg

- 5.2.4 Above 225 kg

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.1.1 Manipulator

- 5.3.1.2 Controller

- 5.3.1.3 Drives

- 5.3.1.4 Sensors

- 5.3.1.5 End-Effectors

- 5.3.2 Software

- 5.3.3 Services

- 5.3.3.1 Integration and Deployment

- 5.3.3.2 Training and Support

- 5.3.3.3 Maintenance

- 5.3.1 Hardware

- 5.4 By Application

- 5.4.1 Material Handling and Pick-and-Place

- 5.4.2 Welding and Soldering

- 5.4.3 Assembly

- 5.4.4 Painting and Dispensing

- 5.4.5 Packaging and Palletising

- 5.4.6 Inspection and Quality Control

- 5.4.7 Cutting and Processing

- 5.4.8 Other Applications

- 5.5 By End-user Industry

- 5.5.1 Automotive

- 5.5.2 Electronics and Semiconductor

- 5.5.3 Metals and Machinery

- 5.5.4 Plastics and Chemicals

- 5.5.5 Food and Beverage

- 5.5.6 Logistics and Warehousing

- 5.5.7 Healthcare

- 5.5.8 Retail and Hospitality

- 5.5.9 Others (Agriculture, Construction)

- 5.6 By Installation Type

- 5.6.1 New Installations

- 5.6.2 Retrofit and Upgrades

- 5.7 By Enterprise Size

- 5.7.1 Large Enterprises

- 5.7.2 Small and Medium Enterprises

- 5.8 By Country

- 5.8.1 Indonesia

- 5.8.2 Malaysia

- 5.8.3 Singapore

- 5.8.4 Thailand

- 5.8.5 Vietnam

- 5.8.6 Philippines

- 5.8.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 FANUC Corporation

- 6.4.2 Yaskawa Electric Corporation

- 6.4.3 ABB Ltd

- 6.4.4 KUKA AG

- 6.4.5 Mitsubishi Electric Corporation

- 6.4.6 Kawasaki Heavy Industries Ltd

- 6.4.7 Omron Corporation

- 6.4.8 Denso Corporation

- 6.4.9 Nachi-Fujikoshi Corp.

- 6.4.10 Seiko Epson Corporation

- 6.4.11 Universal Robots A/S

- 6.4.12 Techman Robot Inc.

- 6.4.13 Staubli International AG

- 6.4.14 Comau S.p.A.

- 6.4.15 Hanwha Robotics

- 6.4.16 Delta Electronics Inc.

- 6.4.17 Hyundai Robotics

- 6.4.18 PBA Robotics (Singapore) Pte Ltd

- 6.4.19 Siasun Robot and Automation Co.

- 6.4.20 Shibaura Machine Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

家用服務機器人市場預測至2034年—按產品類型、組件、技術、應用、最終用戶和地區分類的全球分析

家用服務機器人市場預測至2034年—按產品類型、組件、技術、應用、最終用戶和地區分類的全球分析 服務機器人市場-全球產業規模、佔有率、趨勢、機會和預測:按運行環境、應用、最終用戶、地區和競爭對手分類,2021-2031年

服務機器人市場-全球產業規模、佔有率、趨勢、機會和預測:按運行環境、應用、最終用戶、地區和競爭對手分類,2021-2031年 服務機器人市場:按產品類型、組件類型、運輸方式和最終用戶分類 - 全球市場預測 2026–2032

服務機器人市場:按產品類型、組件類型、運輸方式和最終用戶分類 - 全球市場預測 2026–2032 2026-2034年全球家用機器人市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球家用機器人市場規模、佔有率、趨勢和成長分析報告 2026年航太服務機器人市場報告全球服務機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年航太服務機器人市場報告全球服務機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 服務機器人市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、部署形式、最終用戶、功能2026年全球服務機器人市場報告購物指南機器人市場:依產品類型、支付方式、經營模式、通路和最終用戶分類-2026-2032年全球預測公共間機器人市場:按機器人類型、清潔技術、運作模式、通路、應用程式和終端用戶產業分類,全球預測(2026-2032年)

服務機器人市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、部署形式、最終用戶、功能2026年全球服務機器人市場報告購物指南機器人市場:依產品類型、支付方式、經營模式、通路和最終用戶分類-2026-2032年全球預測公共間機器人市場:按機器人類型、清潔技術、運作模式、通路、應用程式和終端用戶產業分類,全球預測(2026-2032年)