|

市場調查報告書

商品編碼

1934744

汽車引擎活塞環:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Engine Piston Rings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

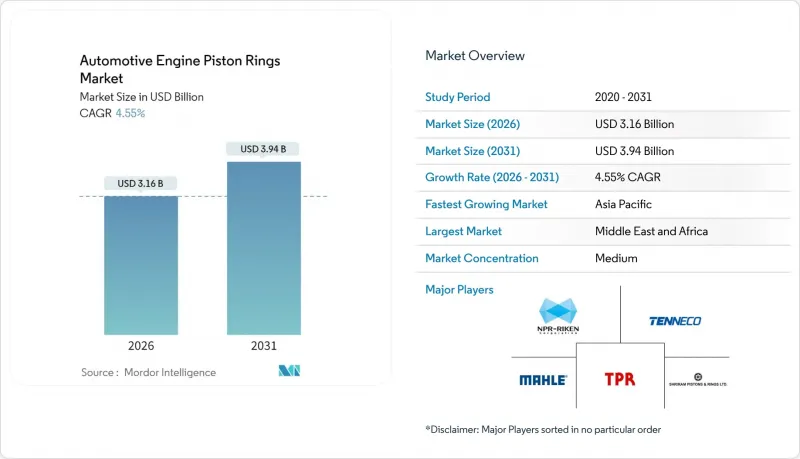

2025年汽車引擎活塞環市值為30.2億美元,預計2031年將達到39.4億美元,高於2026年的31.6億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.55%。

儘管由於內燃機監管壓力不斷加大,電氣化進程加速,但市場需求依然強勁。汽車製造商正優先考慮提高氣密性、降低摩擦並採用輕量化材料,以滿足美國環保署 (EPA) 2032 年二氧化碳排放低於 85 克/英里的目標以及歐盟即將實施的歐 7 排放標準。原始設備製造商 (OEM) 也將關鍵金屬供應鏈遷回國內,並擴大在表面處理技術領域的夥伴關係,以確保下一代活塞環的產能。目前,亞太地區憑藉其高汽車產量和具有成本競爭力的製造基地,在活塞環產量方面佔據主導地位。同時,由於新建組裝廠和不斷擴展的公路網路,中東和非洲地區的複合年成長率 (CAGR) 最高。擁有成熟的摩擦學研究和多層塗層技術的供應商正在贏得長期契約,因為引擎製造商正在尋求能夠減少竄氣和降低機油消耗的承包解決方案。

全球汽車引擎活塞環市場趨勢及洞察

嚴格的排放氣體和燃油經濟性法規推動了創新。

全球廢氣和蒸發排放法規迫使汽車製造商重新設計密封零件,以將竄氣量降至接近零的水平。美國環保署 (EPA) 的多污染物排放法規將在 2027 年至 2032 年間將輕型車輛的二氧化碳排放配額減少近一半,而歐盟 7 排放標準將擴大非廢氣排放的限制。能夠提供微米級公差和奈米級表面處理的供應商正被選中,以幫助汽車製造商在無需進行高成本的引擎重新設計的情況下達到車隊平均排放目標。

新興國家內燃機汽車產量的增加將支撐市場需求。

在印度等國家,儘管電動車數量激增,但對內燃機汽車的需求依然強勁,這主要是由於人們對新能源汽車優勢的認知不足以及缺乏高效的公共充電基礎設施。這些地區注重成本的買家更傾向於選擇耐用型輪圈而非高階塗層,確保了到2030年傳統材料的基本需求。

電動車普及加速威脅傳統需求。

電池式電動車(BEV) 的活動部件約有 20 個,而內燃機汽車的活動部件則約有 2000 個,因此無需活塞環。預計到 2024 會計年度,印度電動車銷量將年增 158%,即使在傳統上對成本非常敏感的市場,也面臨許多挑戰。供應商需要透過進入氫燃料內燃機汽車和燃料無關型零件的細分市場來規避風險。

細分市場分析

到2025年,乘用車將佔據汽車引擎活塞環市場52.74%的佔有率,這主要得益於渦輪增壓3缸和4缸引擎的持續普及,這些引擎需要能夠承受20-30巴峰值壓力的、高度可靠的壓縮環。輕型商用車也構成了一個強勁的細分市場,因為最後一公里運輸車輛優先考慮燃油效率和快速維護週期。

二輪車是成長最快的品類,年複合成長率高達 8.32%,這主要得益於印度、印尼和越南Scooter和摩托車產量的激增。小排氣量引擎更適合採用 DLC 塗層的低張力活塞環,這種活塞環能顯著降低都市區密集使用循環中的摩擦。由於延長換油週期會增加清漆的風險,因此,提供硬鉻刮油環和精密回油槽的供應商正在這個以銷售主導的細分市場中佔據越來越大的佔有率。

截至2025年,灰鑄鐵在汽車引擎活塞環市場仍佔47.12%的佔有率。成熟的供應鏈和良好的加工性能降低了成本,尤其對於大規模生產的乘用車更是如此。添加可控制磷石墨的合金化灰鑄鐵提高了耐磨性,而減少截面厚度則可使每個活塞環減重15-20克。

不銹鋼和鉻鋼的成長速度最快,複合年成長率達9.12%,這主要得益於原始設備製造商(OEM)對小型渦輪增壓引擎基材的需求,他們需要兼具耐腐蝕性和高強度的材料。這些材料的強度重量比提高了30%,並且能夠在不犧牲耐久性的前提下實現0.8毫米的活塞環槽高度。隨著活塞環市場佔有率向高階材料轉移以滿足歐7和Tier 4最終排放標準,擁有真空脫氣和精密拉拔生產線的供應商正在贏得更多項目。

區域分析

亞太地區將主導汽車引擎活塞環市場,預計2025年將佔據52.68%的市場。中國一體化鑄造廠的規模經濟以及印度零件叢集的繁榮發展,鞏固了該地區的主導地位。各國政府正透過提供與生產連結獎勵計畫、加速環境核准、縮短工廠建設週期等方式,鼓勵跨國公司在地採購。

中東和非洲地區成長最快,複合年成長率達6.92%。沙烏地阿拉伯和阿拉伯聯合大公國正積極推進合資組裝廠的建設,以回應「2030願景」多元化發展計劃。非洲聯盟基礎設施走廊的建設帶動了輕型卡車的銷售,進而刺激了對適用於多塵高溫等嚴苛運作況的重型灰鑄鐵環的需求。

北美和歐洲在技術方面仍然是標竿地區。儘管內燃機(ICE)的絕對產量已趨於穩定,但日益嚴格的排放氣體法規支撐了對優質塗層活塞環和混合動力原型的需求。總部位於該地區的供應商在摩擦學研究方面處於領先地位,並透過授權協議向亞洲出口製程技術。而參與企業市場的企業則遵循著不同的發展軌跡:都市區電動車(BEV)的快速普及,以及農村和商用車隊對內燃機(ICE)的穩定需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 嚴格的排放氣體和燃油經濟法規

- 新興國家內燃機汽車產量不斷成長

- 原始設備製造商正在向低摩擦、輕量化鋼環過渡

- 採用渦輪增壓汽油引擎需要更嚴格的活塞環公差。

- 氫內燃機試驗計畫。

- 內建配戴感應器的智慧戒指

- 市場限制

- 加速電動車的普及

- 鋼鐵和鉬價格波動

- 超低張力環的過早磨損問題

- 精密研磨工程師短缺

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 摩托車

- 非公路(建築、農業)

- 依材料類型

- 灰鑄鐵

- 球墨鑄鐵/合金鑄鐵

- 碳鋼

- 不銹鋼/鉻鋼

- 先進複合材料和陶瓷

- 按環型

- 壓縮環

- 刮油環

- 油控環

- 透過塗層技術

- 鍍鉻

- 鉬/鉬噴霧劑

- DLC &ta-C

- 陶瓷和混合奈米塗層

- 按燃料類型

- 汽油

- 柴油引擎

- 替代燃料(壓縮天然氣/液化石油氣、生質燃料)

- 氫內燃機

- 按銷售管道

- OEM

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 泰國

- 亞太其他地區

- 中東和非洲

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NPR Riken Corporation

- Tenneco Inc.(Federal-Mogul)

- MAHLE GmbH

- TPR Co., Ltd.

- Shriram Pistons & Rings Ltd.

- Asimco Technologies

- IP Rings Ltd.

- SAM Pistons & Rings

- Grover Corporation

- Abilities India Piston & Rings

- Hastings Manufacturing(Hastings Manufacturing Company, LLC)

- Atrac Engineering

- Ks Kolbenschmidt GmbH(Rheinmetall Automotive)

- Wossner Pistons USA

- Quintess International

- Garima Global Pvt. Ltd.

第7章 市場機會與未來展望

The automotive engine piston rings market was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.16 billion in 2026 to reach USD 3.94 billion by 2031, at a CAGR of 4.55% during the forecast period (2026-2031).

Growing regulatory pressure on internal-combustion engines (ICEs) keeps demand resilient even as electrification accelerates. Automakers prioritize tighter sealing, lower friction, and lighter materials to comply with the U.S. Environmental Protection Agency's 85 g/mi CO2 target by 2032 and the European Union's forthcoming Euro 7 limits. OEMs are also reshoring critical metal supply chains and expanding surface-engineering partnerships to secure capacity for next-generation piston rings. Asia-Pacific dominates current volumes due to high vehicle output and cost-competitive manufacturing. At the same time, the Middle East and Africa present the fastest CAGR due to green-field assembly plants and expanding road networks. Suppliers with proven tribology research and multilayer coating expertise are gaining long-term contracts as engine builders seek turnkey solutions that cut blow-by and oil consumption.

Global Automotive Engine Piston Rings Market Trends and Insights

Strict Emissions and Fuel-Economy Regulations Drive Innovation

Global tailpipe and evaporative standards compel OEMs to redesign sealing components for near-zero blow-by. The EPA's multi-pollutant rule cuts allowed CO2 nearly in half for 2027-2032 light-duty vehicles, while Euro 7 extends limits to non-tailpipe emissions. Suppliers who deliver micron-level tolerances and nano-scale surface treatments win sourcing awards because they help automakers meet fleet-average targets without costly engine redesigns.

Rising ICE Vehicle Production in Emerging Economies Sustains Demand

Demand for ICE-vehicles in countries such as India, especially due to low awareness of the benefits of new-energy vehicles and a lack of efficient public charging infrastructure, is keeping conventional powertrains relevant even as EV volumes soar. Cost-focused buyers in these regions value durable rings over premium coatings, ensuring baseline demand for legacy materials through 2030.

Accelerating BEV Penetration Threatens Traditional Demand

Battery-electric vehicles contain roughly 20 moving parts versus 2,000 for ICEs, eliminating piston rings. EV sales in India jumped 158% year-on-year in FY24, illustrating the headwind even in traditionally cost-sensitive markets. Suppliers must hedge by entering hydrogen-ICE and fuel-agnostic component niches.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift to Low-Friction, Lightweight Steel Rings Transforms Materials

- Turbo-Gasoline Adoption Demands Tighter Ring Tolerances

- Volatile Steel & Molybdenum Prices Compress Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars controlled 52.74% of the automotive engine piston rings market share in 2025, underpinned by the continual adoption of turbocharged three-and four-cylinder engines that require high-integrity compression rings capable of sealing 20-30 bar peak pressures. Light commercial vans form a resilient sub-pocket as last-mile fleets emphasize fuel efficiency and quick maintenance cycles.

Two-wheelers represent the fastest-growing category, climbing at an 8.32% CAGR due to surging scooter and motorcycle production in India, Indonesia, and Vietnam. Their small-bore engines favor low-tension rings with DLC top layers that slash friction during dense urban duty cycles. Extended drain intervals intensify varnish risks, so suppliers offering hard-chrome scraper rings and precise oil-return slots gain share in this volume-driven niche.

Gray cast iron retained a 47.12% market share in the automotive engine piston rings market in 2025, with established supply chains and forgiving machinability keeping costs low, particularly for high-volume passenger vehicles. Alloyed variants with phosphorus-controlled graphite improve abrasion resistance, enabling thinner cross-sections that save 15-20 g per ring.

Stainless and chromium steels post the quickest growth at 9.12% CAGR as OEMs demand corrosion-resistant, high-strength substrates for downsized turbo engines. These materials boost strength-to-weight by 30%, allowing 0.8 mm ring land heights without compromising durability. Vendors equipped with vacuum degassing and precision wire-drawing lines capture programs where piston rings market share shifts toward premium materials for Euro 7 and Tier 4-final compliance.

The Automotive Engine Piston Rings Market Report is Segmented by Vehicle Type (Passenger Cars, Medium and Heavy Commercial Vehicles, and More), Material Type (Grey Cast Iron and More), Ring Type (Compression Rings and More), Coating Technology (Chrome Plating and More), Fuel Type (Gasoline and More), Sales Channel (OEM and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific dominates the automotive engine piston rings market, holding 52.68% of 2025 revenue. This is owing to China's integrated casting houses and India's component clusters, which ensure economies of scale that underpin the region's leadership. Governments provide production-linked incentives and fast-track environmental approvals that compress factory build-out times, persuading multinationals to source high-volume piston ring programs locally.

The Middle East and Africa are the fastest-growing territories, with a 6.92% CAGR. Saudi Arabia and the United Arab Emirates nurture joint-venture assembly plants aligned with Vision-2030 diversification blueprints. African Union infrastructure corridors stimulate light-truck sales, spurring demand for robust gray iron rings suited to dusty, high-temperature duty cycles.

North America and Europe remain technology bellwethers. Although absolute ICE volumes plateau, stringent emissions timetables support premium coated rings and hybrid-fuel prototypes. Suppliers headquartered here lead in tribology research and exporting process know-how to Asia under licensing agreements. Market participants navigate divergent trajectories: rapid BEV uptake in urban centers versus steady ICE demand in rural and vocational fleets.

- NPR Riken Corporation

- Tenneco Inc. (Federal-Mogul)

- MAHLE GmbH

- TPR Co., Ltd.

- Shriram Pistons & Rings Ltd.

- Asimco Technologies

- IP Rings Ltd.

- SAM Pistons & Rings

- Grover Corporation

- Abilities India Piston & Rings

- Hastings Manufacturing (Hastings Manufacturing Company, LLC)

- Atrac Engineering

- Ks Kolbenschmidt GmbH (Rheinmetall Automotive)

- Wossner Pistons USA

- Quintess International

- Garima Global Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict emissions & fuel-economy regulations

- 4.2.2 Rising ICE vehicle production in emerging economies

- 4.2.3 OEM shift to low-friction, lightweight steel rings

- 4.2.4 Turbo-gasoline adoption demanding tighter ring tolerances

- 4.2.5 Hydrogen-ICE pilot programs needing compatible rings

- 4.2.6 Smart rings with embedded wear sensors

- 4.3 Market Restraints

- 4.3.1 Accelerating BEV penetration

- 4.3.2 Volatile steel & molybdenum prices

- 4.3.3 Premature wear issues with ultra-low-tension rings

- 4.3.4 Precision-grinding talent shortage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.1.5 Off-Highway (Construction, Agricultural)

- 5.2 By Material Type

- 5.2.1 Gray Cast Iron

- 5.2.2 Ductile / Alloyed Cast Iron

- 5.2.3 Carbon Steel

- 5.2.4 Stainless / Chromium Steel

- 5.2.5 Advanced Composites & Ceramics

- 5.3 By Ring Type

- 5.3.1 Compression Rings

- 5.3.2 Wiper / Scraper Rings

- 5.3.3 Oil Control Rings

- 5.4 By Coating Technology

- 5.4.1 Chrome Plating

- 5.4.2 Molybdenum / Mo-Spray

- 5.4.3 DLC & ta-C

- 5.4.4 Ceramic & Hybrid Nano-Coatings

- 5.5 By Fuel Type

- 5.5.1 Gasoline

- 5.5.2 Diesel

- 5.5.3 Alternative Fuels (CNG/LPG, Biofuels)

- 5.5.4 Hydrogen ICE

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Indonesia

- 5.7.4.6 Thailand

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Turkey

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 United Arab Emirates

- 5.7.5.4 South Africa

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 NPR Riken Corporation

- 6.4.2 Tenneco Inc. (Federal-Mogul)

- 6.4.3 MAHLE GmbH

- 6.4.4 TPR Co., Ltd.

- 6.4.5 Shriram Pistons & Rings Ltd.

- 6.4.6 Asimco Technologies

- 6.4.7 IP Rings Ltd.

- 6.4.8 SAM Pistons & Rings

- 6.4.9 Grover Corporation

- 6.4.10 Abilities India Piston & Rings

- 6.4.11 Hastings Manufacturing (Hastings Manufacturing Company, LLC)

- 6.4.12 Atrac Engineering

- 6.4.13 Ks Kolbenschmidt GmbH (Rheinmetall Automotive)

- 6.4.14 Wossner Pistons USA

- 6.4.15 Quintess International

- 6.4.16 Garima Global Pvt. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

汽車引擎市場:依汽缸數、燃料類型、排氣量範圍及車輛類型分類-2026-2032年全球市場預測汽車承油盤市場:按材料、引擎類型、應用和車輛類型分類-2026-2032年全球市場預測氫燃料內燃機市場:2026-2032年全球市場預測(依車輛類型、終端用戶產業、功率範圍、燃燒技術及燃料混合比分類)

汽車引擎市場:依汽缸數、燃料類型、排氣量範圍及車輛類型分類-2026-2032年全球市場預測汽車承油盤市場:按材料、引擎類型、應用和車輛類型分類-2026-2032年全球市場預測氫燃料內燃機市場:2026-2032年全球市場預測(依車輛類型、終端用戶產業、功率範圍、燃燒技術及燃料混合比分類) 2026年全球汽車性能調校與引擎重映射服務市場報告汽車進氣壓力感知器市場:依引擎類型、感知器類型、技術、壓力範圍、車輛類型和銷售管道分類-2026-2032年全球市場預測2026年全球引擎調校市場報告2026年史特靈引擎全球市場報告

2026年全球汽車性能調校與引擎重映射服務市場報告汽車進氣壓力感知器市場:依引擎類型、感知器類型、技術、壓力範圍、車輛類型和銷售管道分類-2026-2032年全球市場預測2026年全球引擎調校市場報告2026年史特靈引擎全球市場報告 先進觸媒技術市場分析及預測(至2035年):類型、產品、技術、應用、材料類型、最終用戶、製程、組件、安裝類型

先進觸媒技術市場分析及預測(至2035年):類型、產品、技術、應用、材料類型、最終用戶、製程、組件、安裝類型 全球同步環市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球鋁活塞市場報告

全球同步環市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球鋁活塞市場報告