|

市場調查報告書

商品編碼

1934711

硫酸軟骨素:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Chondroitin Sulfate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

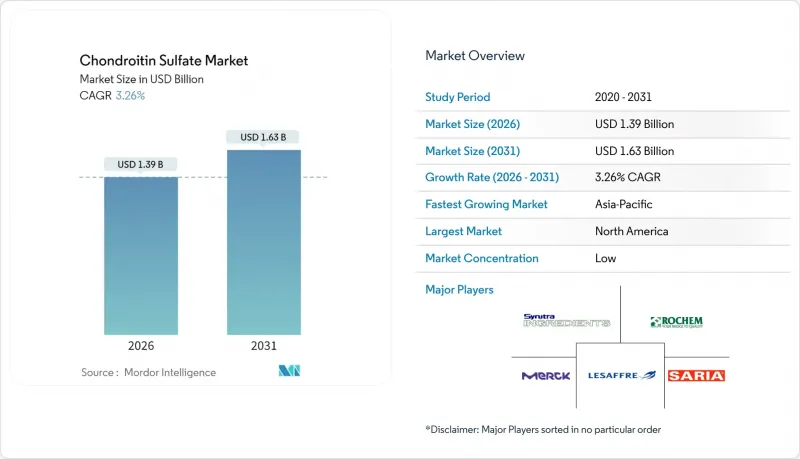

2025年硫酸軟骨素市值為13.5億美元,預計到2031年將達到16.3億美元,高於2026年的13.9億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.26%。

這一穩定成長的趨勢主要受以下因素驅動:45歲以上成年人骨關節炎發病率的急劇上升,導致動物源性成分面臨越來越大的壓力;以及臨床療效的不斷提升,使得藥用級成分成為行業標準。合成和發酵生產技術的加速創新為長期供應安全提供了保障,而與膠原蛋白、透明質酸或乳香等成分的複配製劑則拓展了其應用範圍。競爭策略日益強調垂直整合,以品管並利用有利於高品質產品的監管差異。同時,亞太地區的生產能力也帶來了成長機遇,這有助於支持出口市場並緩解原料價格波動對全球供應造成的周期性壓力。

全球硫酸軟骨素市場趨勢及洞察

45歲及以上人群中骨關節炎的盛行率不斷上升

預期壽命的延長和45歲以上人口的成長推動了對藥用級硫酸軟骨素的持續需求。骨關節炎影響美國3,250萬成年人,而諸如MOVES試驗等大型臨床試驗表明,經過六個月的治療,其療效與塞來昔布相當。亞太地區也呈現類似的人口結構變化,加速了對膳食補充劑的需求。最近一項以卷尾蟲為模型的研究表明,內源性硫酸軟骨素水平翻倍與壽命延長30.6%相關,進一步檢驗了其作為預防藥物的作用。隨著肌肉骨骼疾病在全球致殘原因排名中不斷上升,醫療保健系統正在將硫酸軟骨素納入複雜的治療管理中,這正逐漸成為長期治療的基礎。

膳食補充劑對關節健康越來越受歡迎

預防性自我護理的趨勢已將醫藥領域的研究成果轉化為非處方產品,推動全球關節保健品市場規模超過1,000億美元。在亞太地區,中產階級消費者經常服用硫酸軟骨素粉末、顆粒和咀嚼片,並青睞將其與膠原蛋白和乳香萃取物結合的複合產品,這些產品可在短短五天內緩解疼痛。儘管醫藥級和食品級之間的標準化差距依然存在,但高階營養補充劑正在彌合這一差距,一些品牌聲稱其產品純度達到美國藥典(USP)級別,以此來支撐更高的價格。

動物性原料供應波動

牲畜疾病週期、肉類停工以及《瀕危野生動植物種國際貿易公約》(CITES)對鯊魚軟骨的限制,都會週期性地限制原料供應並推高成本。製造商透過採購多種原料並建立庫存來規避風險,但這會增加營運資金需求,並加大終端用戶的價格壓力。合成路線和發酵技術可以降低這種風險,從而推動可控生物加工的策略性資本投資。

細分市場分析

憑藉成熟的供應鏈和具有競爭力的價格,豬軟骨預計到2025年將佔銷售額的25.12%。同時,合成軟骨產品雖然目前佔比仍不足10%,但正以5.81%的複合年成長率快速成長。採用基因改造大腸桿菌的發酵系統可在48小時內達到99%的純度。此製程可產生符合藥典測試標準的均勻硫酸化模式,並顯著降低內毒素風險。這項轉變符合生態標章、猶太潔食/清真食品需求以及純素相容性要求,使領先採用者獲得聲譽優勢。牛軟骨仍然重要,但必須透過認證採購來應對瘋牛症(牛腦病變)的擔憂。由於《瀕危野生動植物種國際貿易公約》(CITES)法規的不斷擴展,鯊魚軟骨的需求持續下降,而禽類軟骨則在滿足宗教要求的配方中保持著一定的市場地位。

價格趨勢顯示存在權衡取捨:目前合成乳的每公斤成本高於牛基準值,但較低的精煉損耗和環境溢價正在縮小兩者之間的差距。在發酵槽產能擴張帶來的規模經濟效益的推動下,預計到2031年,合成乳的市佔率將接近15.3%,從而緩解原物料價格上漲對利潤率的擠壓。

到2025年,藥用級產品將佔市場佔有率的49.62%,隨著臨床證據的不斷增強和醫保覆蓋範圍的擴大,其價格也將水漲船高。 MOVES試驗的結果表明,其療效與塞羅昔布相當,且無胃腸道疾病等副作用。食品級配方推動的硫酸軟骨素市場規模預計將以5.18%的複合年成長率成長,反映出消費者願意為預防性關節護理付費。目前化妝品級產品仍佔市佔率小規模,主要用於抗老精華液以發揮保濕功效。

製藥公司擁有完全符合ICH標準的品管系統、批次放行分析和可追溯的供應鏈——這些要素通常是小規模的食品級供應商所缺乏的。然而,膳食補充劑品牌如果能夠透過USP認證的產品線彌補這一差距,就能提升產品吸引力,並使其更高的價格更具合理性,尤其是在強調透明度的電商管道中。因此,監管逐步實施並非一道難以逾越的障礙,反而為有能力的食品級企業進入製劑市場提供了一條途徑——前提是他們願意投入資源進行檢驗。

區域分析

預計到2025年,北美地區將佔總收入的38.62%,這主要得益於處方箋硫酸軟骨素的健保覆蓋、大規模的骨關節炎患者群體以及成熟的膳食補充劑零售管道。食品用途的GRAS(公認安全)認證和FDA純度標準指南增強了消費者的信心,而訴訟風險則促使製造商繼續投資於精確分析。該地區2.78%的複合年成長率雖然穩健,但也反映了其市場的成熟度。

亞太地區是成長最快的地區,複合年成長率達6.54%,中國和印度產能的擴張支撐了國內和出口需求。人口老化以及人們對傳統醫學的接受度正在加速顆粒狀硫酸軟骨素速溶袋和氣泡式飲料的普及。日本對治療腰椎間盤突出症的藥物Chondriaze的臨床認可進一步推動了治療方法的多樣化。

在歐洲,已有13個國家核准了處方藥,醫生開始使用藥用級硫酸軟骨素取代非類固醇抗發炎藥物來降低心血管風險。南歐的膳食補充劑消費者更傾向於含有地中海植物成分的複雜配方。南美洲以及中東和非洲地區雖然發展落後,但隨著當地經銷商與歐洲藥品供應商達成許可協議,並將銷售管道拓展至私人診所和高階藥房,其複合年成長率也保持在個位數水平。標籤法規和清真認證的區域差異仍然會影響產品的上市時間。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 45歲及以上人群中骨關節炎的盛行率不斷上升

- 關節保健品中膳食補充劑的採用率不斷提高

- 歐盟和美國不斷加強監管,鼓勵使用藥用級CS。

- 擴大中國和印度的牛軟骨加工能力

- 注射用黏彈性補充劑的研究與開發進展(未報告)

- 再生醫學領域對低分子量硫酸軟骨素的需求不斷成長(未報告)

- 市場限制

- 動物性原料供應波動

- 食品級CS的品質與詐欺問題

- 加強《瀕危野生動植物種國際貿易公約》(CITES)關於鯊魚軟骨取得的規定(未報告)

- 植物來源的Glico類似物正變得越來越受歡迎(未報導)

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按來源

- 牛軟骨

- 豬軟骨

- 鯊魚軟骨

- 鳥類軟骨

- 合成

- 其他資訊來源

- 按年級

- 醫藥級

- 食品級

- 化妝品級

- 按形式

- 粉末

- 顆粒

- 片劑和膠囊

- 注射液/溶液

- 透過使用

- 處方藥和非處方藥

- 營養補充品

- 化妝品和個人護理

- 動物醫藥

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Bioiberica SAU

- Changzhou Qianhong Bio-pharma Co., Ltd.

- Focus Chem Biotech(Nantong Furuida)

- Gnosis by Lesaffre

- IBSA Institut Biochimique SA

- Jiaxing Hengtai Pharma Co., Ltd.

- Kraeber & Co. GmbH

- Pacific Rainbow International Inc.

- Qingdao WanTuMing Biological Co., Ltd.

- Seikagaku Corporation

- Shandong Dongcheng Pharmaceutical Co., Ltd.

- Summit Nutritionals International

- Synutra Ingredients

- Tidal Vision Products

- TSI Group Ltd.

- Zhaoqing Konson Nutraceutical Co., Ltd.

- Focus Chem Biotech

第7章 市場機會與未來展望

The chondroitin sulfate market was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 3.26% during the forecast period (2026-2031).

This steady trajectory is shaped by the rapid rise in osteoarthritis among adults over 45, mounting pressure on animal-derived sources, and growing clinical validation that positions pharmaceutical-grade material as the industry benchmark. Intensifying innovation around synthetic and fermentation-based production underpins long-term supply security, while combination formulations with collagen, hyaluronic acid or Boswellia serrata broaden application breadth. Competitive strategies increasingly emphasize vertical integration to control raw-material quality and leverage regulatory differentiation that rewards higher-grade offerings. Parallel growth opportunities lie in Asia-Pacific manufacturing capacity, which supports export markets and mitigates raw-material price swings that periodically tighten global supply.

Global Chondroitin Sulfate Market Trends and Insights

Intensifying Osteoarthritis Prevalence Among 45+ Population

Rising life expectancy and a larger cohort of adults over 45 sustain demand for pharmaceutical-grade chondroitin sulfate, with osteoarthritis affecting 32.5 million U.S. adults. Large-scale trials such as MOVES confirmed efficacy comparable to celecoxib over six-month regimens. Asia-Pacific mirrors this demographic wave, magnifying nutraceutical uptake. Recent C. elegans work showing 30.6% lifespan extension when endogenous chondroitin doubled adds mechanistic validation that resonates with preventive-care positioning. With musculoskeletal disorders climbing the global disability chart, healthcare systems adopt chondroitin sulfate in multi-modal management, embedding this driver as a long-term pillar.

Rising Nutraceutical Adoption in Joint-Health Supplements

Preventive self-care trends convert pharmaceutical insights into over-the-counter formats, propelling joint-health supplements past USD 100 billion globally. In Asia-Pacific, middle-class consumers integrate chondroitin sulfate powders, granules and chewables into daily routines, attracted by combination formats that cut pain in as few as five days when paired with collagen and Boswellia serrata. Standardization gaps still differentiate pharmaceutical-grade from food-grade, but premium nutraceuticals bridge this divide as brands tout USP-level purity to justify higher price points.

Volatility in Animal-Derived Raw-Material Supply

Livestock disease cycles, slaughterhouse shutdowns and CITES constraints on shark cartilage periodically curtail raw-material flows and elevate costs. Manufacturers hedge through multi-species sourcing and higher inventories, which lift working-capital requirements and price tags for end users. Synthetic pathways and fermentation reduce this exposure, encouraging strategic capex toward controlled bioprocessing.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Upgrades Endorsing Pharmaceutical-Grade CS in EU & US

- Expansion of Bovine Cartilage Processing Capacity in China & India

- Quality & Adulteration Concerns in Food-Grade CS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

2025 revenue shows swine cartilage at 25.12%, supported by mature supply chains and competitive pricing. Yet synthetic output, still below 10% share, races ahead at a 5.81% CAGR. Fermentation systems using engineered E. coli achieve 99% purity in 48 hours. This process yields consistent sulfation patterns that satisfy pharmacopoeia tests and greatly reduce endotoxin risk. The pivot aligns with eco-labeling, kosher/halal demand and vegan positioning, granting first movers a reputational moat. Bovine cartilage remains relevant but must manage BSE perception through certified sourcing. Shark cartilage continues to fall as CITES listings expand, and avian cartilage holds niche status for religious-compliance formulations.

Pricing dynamics illustrate the trade-off: synthetic costs per kilogram currently exceed bovine benchmarks, yet lower purification losses and environmental premiums narrow the gap. As expanded fermenter capacity drives economies of scale, synthetic share is projected to approach 15.3% by 2031, moderating raw-material price spikes that historically pinched margins.

Pharmaceutical-grade products contributed 49.62% of 2025 value and command a widening premium amid stronger clinical evidence and reimbursement recognition. MOVES trial outcomes showed equivalence to celecoxib without gastrointestinal side effects. The chondroitin sulfate market size attributable to food-grade formulations climbs at 5.18% CAGR, reflecting consumer willingness to pay for proactive joint care. Cosmetics-grade remains a micro-segment, integrated in anti-aging serums for moisture retention.

Pharmaceutical manufacturers showcase full ICH-compliant quality systems, batch-release analytics and traceable supply chains that smaller food-grade suppliers often lack. However, nutraceutical brands closing this gap with USP-verified product lines improve shelf appeal and justify higher price points, especially through e-commerce channels emphasizing transparency. The regulatory gradient therefore acts less as an impermeable wall and more as a pathway for capable food-grade players to ascend into prescription markets, provided they allocate resources to validation.

The Chondroitin Sulfate Market Report is Segmented by Source (Bovine Cartilage, Porcine Cartilage, Shark Cartilage, Avian Cartilage, Synthetic, Other Sources), Grade (Pharmaceutical Grade, Food Grade, Cosmetics Grade), Form (Powder, Granules, and More), Application (Pharmaceuticals & OTC Drugs, Dietary Supplements, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 38.62% of 2025 revenue, anchored by insurance coverage for prescription chondroitin sulfate, a large osteoarthritis patient pool and well-established nutraceutical retail channels. GRAS acceptance for food use and FDA guidance on purity thresholds reinforce consumer trust, though litigation risk keeps manufacturers invested in high-end analytics. The region's stable yet modest 2.78% CAGR reflects maturity.

Asia-Pacific rises fastest at 6.54% CAGR, propelled by capacity buildouts in China and India that feed both domestic and export demand. Aging demographics intersect with traditional medicine openness, accelerating uptake of sachet sticks and effervescent drinks that dissolve granulated chondroitin sulfate. Japanese clinical acceptance of condoliase for lumbar disc herniation further diversifies therapeutic landscapes.

Europe benefits from ethical-drug approvals across 13 countries, with physicians prescribing pharmaceutical-grade chondroitin sulfate in place of NSAIDs to mitigate cardiovascular risk. Southern European nutraceutical consumers favor combination formulas featuring Mediterranean botanicals. South America and Middle East & Africa trail but post mid-single-digit CAGR as local distributors negotiate licensing deals with European API suppliers, extending reach into private clinics and upscale pharmacies. Regional heterogeneity in labeling rules and halal certification continues to affect product-launch timelines.

- Bioiberica

- Changzhou Qianhong Bio-pharma Co., Ltd.

- Focus Chem Biotech (Nantong Furuida)

- Gnosis by Lesaffre

- IBSA Institut Biochimique SA

- Jiaxing Hengtai Pharma Co., Ltd.

- Kraeber & Co. GmbH

- Pacific Rainbow International Inc.

- Qingdao WanTuMing Biological Co., Ltd.

- Seikagaku

- Shandong Dongcheng Pharmaceutical Co., Ltd.

- Summit Nutritionals International

- Synutra Ingredients

- Tidal Vision Products

- TSI Group

- Zhaoqing Konson Nutraceutical Co., Ltd.

- Focus Chem Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying osteoarthritis prevalence among 45 + population

- 4.2.2 Rising nutraceutical adoption in joint-health supplements

- 4.2.3 Regulatory upgrades endorsing pharmaceutical-grade CS in EU & US

- 4.2.4 Expansion of bovine cartilage processing capacity in China & India

- 4.2.5 Growth of injectable viscosupplement R&D (under-reported)

- 4.2.6 Emerging demand for low-molecular-weight CS in regenerative medicine (under-reported)

- 4.3 Market Restraints

- 4.3.1 Volatility in animal-derived raw-material supply

- 4.3.2 Quality & adulteration concerns in food-grade CS

- 4.3.3 Stricter CITES controls on shark cartilage sourcing (under-reported)

- 4.3.4 Plant-based glycosaminoglycan analogues gaining traction (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Source (Value)

- 5.1.1 Bovine Cartilage

- 5.1.2 Porcine Cartilage

- 5.1.3 Shark Cartilage

- 5.1.4 Avian Cartilage

- 5.1.5 Synthetic

- 5.1.6 Other Sources

- 5.2 By Grade (Value)

- 5.2.1 Pharmaceutical Grade

- 5.2.2 Food Grade

- 5.2.3 Cosmetics Grade

- 5.3 By Form (Value)

- 5.3.1 Powder

- 5.3.2 Granules

- 5.3.3 Tablets & Capsules

- 5.3.4 Injectable / Solution

- 5.4 By Application (Value)

- 5.4.1 Pharmaceuticals & OTC Drugs

- 5.4.2 Dietary Supplements

- 5.4.3 Cosmetics & Personal Care

- 5.4.4 Veterinary Medicine

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Bioiberica S.A.U.

- 6.3.2 Changzhou Qianhong Bio-pharma Co., Ltd.

- 6.3.3 Focus Chem Biotech (Nantong Furuida)

- 6.3.4 Gnosis by Lesaffre

- 6.3.5 IBSA Institut Biochimique SA

- 6.3.6 Jiaxing Hengtai Pharma Co., Ltd.

- 6.3.7 Kraeber & Co. GmbH

- 6.3.8 Pacific Rainbow International Inc.

- 6.3.9 Qingdao WanTuMing Biological Co., Ltd.

- 6.3.10 Seikagaku Corporation

- 6.3.11 Shandong Dongcheng Pharmaceutical Co., Ltd.

- 6.3.12 Summit Nutritionals International

- 6.3.13 Synutra Ingredients

- 6.3.14 Tidal Vision Products

- 6.3.15 TSI Group Ltd.

- 6.3.16 Zhaoqing Konson Nutraceutical Co., Ltd.

- 6.3.17 Focus Chem Biotech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球硫酸軟骨素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球硫酸軟骨素市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球硫酸軟骨素市場報告

2026年全球硫酸軟骨素市場報告 硫酸軟骨素市場-全球產業規模、佔有率、趨勢、機會、預測:按原料、應用、區域和競爭對手分類,2021-2031年

硫酸軟骨素市場-全球產業規模、佔有率、趨勢、機會、預測:按原料、應用、區域和競爭對手分類,2021-2031年 犬用葡萄糖胺補充劑市場按劑型、成分類型、配方和分銷管道分類,全球預測(2026-2032年)

犬用葡萄糖胺補充劑市場按劑型、成分類型、配方和分銷管道分類,全球預測(2026-2032年) 硫酸軟骨素市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

硫酸軟骨素市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) 硫酸軟骨素市場規模、佔有率和成長分析(按來源、形態、應用和地區分類)-2026-2033年產業預測

硫酸軟骨素市場規模、佔有率和成長分析(按來源、形態、應用和地區分類)-2026-2033年產業預測 2025-2033年硫酸軟骨素市場報告,依來源(牛、豬、家禽、鯊魚等)、形式(粉末、片劑等)、應用(藥品和保健品、動物飼料、個人護理和化妝品等)和地區分類

2025-2033年硫酸軟骨素市場報告,依來源(牛、豬、家禽、鯊魚等)、形式(粉末、片劑等)、應用(藥品和保健品、動物飼料、個人護理和化妝品等)和地區分類 硫酸軟骨素市場規模、佔有率和趨勢分析報告:按來源、應用、地區和細分市場預測,2025-2033 年

硫酸軟骨素市場規模、佔有率和趨勢分析報告:按來源、應用、地區和細分市場預測,2025-2033 年 硫酸軟骨素市場,規模,佔有率,趨勢,產業分析報告:供給來源,各用途,各地區,2025年~2034年的市場預測

硫酸軟骨素市場,規模,佔有率,趨勢,產業分析報告:供給來源,各用途,各地區,2025年~2034年的市場預測 硫酸軟骨素市場按來源和地區分類

硫酸軟骨素市場按來源和地區分類