|

市場調查報告書

商品編碼

1934672

電腦數值控制(CNC):市場佔有率分析、產業趨勢與統計資料、成長預測 (2026-2031)Computer Numerical Controls (CNC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

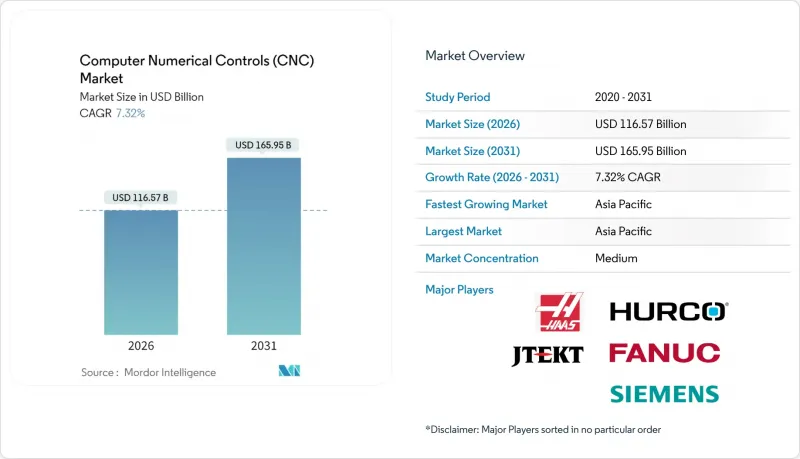

電腦數值控制(CNC) 市場預計到 2026 年價值 1,165.7 億美元,從 2025 年的 1,086.3 億美元成長到 2031 年的 1,659.5 億美元。

預計2026年至2031年年複合成長率(CAGR)為7.32%。

持續的勞動力短缺、生產近岸外包以及工業4.0自動化浪潮的推動,正促使製造商加速投資多軸加工和數位化互聯設備。美國和歐洲的回流政策正將資本從低成本地區轉移到能夠加快生產週轉時間的彈性加工設施。日益增強的互聯性也帶來了網路安全風險,促使供應商在新控制器中融入安全設計特性。同時,持續高企的鋼鋁價格也推動了對能夠最大限度減少廢料的精密加工流程的需求。儘管零件短缺導致短期供應摩擦,但這些因素共同推動了電腦數值控制(CNC) 市場的強勁成長。

全球電腦數值控制(CNC) 市場趨勢與洞察

北美和歐洲因製造業回流而對軟性數控設備的需求主導

2023年,美國從中國進口的成品下降了13%,而由於基礎設施和半導體產業的優惠政策,國內工廠投資大幅成長。由於訂單波動,買家更青睞能夠處理各種零件組合的靈活五軸機床和模組化機器人單元。生產地點越靠近市場,運輸風險越低,交貨時間越短,因此更高的資本支出也越合理。能夠提供快速改造和數位化配置能力的供應商獲得了競爭優勢。這種生產回流的趨勢,將數十年來外包的生產模式轉變為擴大的本地製造能力,從而直接擴大了電腦數值控制(CNC)市場。

引入主導4.0驅動的兼容數位雙胞胎的控制設備

數位雙胞胎技術使程式設計人員能夠虛擬檢驗刀具路徑,從而在西門子Sinumerik 828D硬體上將實體設定時間縮短20%。研究表明,當機器與其虛擬對應物運作封閉回路型協作時,生產率可提高14.53%,能耗可降低13.9%。航太和汽車產業的應用最為廣泛,因為這些產業需要即時補償熱漂移和刀具磨損。控制設備供應商正在整合雲端連接和人工智慧分析技術,將數控市場轉變為以軟體為中心的領域。隨著授權收入的成長,機器製造商越來越重視經常性收入來源,而非一次性硬體利潤。

半導體運動控制晶片短缺限制了供應

精密伺服驅動器依賴專用ASIC晶片,但供不應求持續存在,導致高階機器的前置作業時間長達九個月甚至更久。一些製造商正在利用現有晶片進行設計變更,但這需要昂貴的重新認證。已獲得配額的OEM廠商正在擴大市場佔有率,而後進企業正在失去訂單。儘管訂單充足,但這種瓶頸在短期內限制了CNC市場的規模。

細分市場分析

到2025年,CNC車床將佔據CNC工具機市場22.95%的佔有率,是加工軸和輪轂等圓形零件的關鍵設備。隨著電動車(EV)動力傳動系統的發展,公差要求日益嚴格,許多加工廠正在對傳統車削中心進行改造,加裝動力刀具和Y軸功能。銑床將成為CNC工具機市場中第二大佔有率的工具機,主要負責加工航太零件和醫療植入所需的複雜模腔。電池機殼鈑金設計的增加將推動對雷射切割機和電漿切割機的需求,而電火花加工(EDM)在加工硬化工具鋼方面繼續發揮關鍵作用。由於單次裝夾功能顯著縮短了夾具使用時間並消除了重新裝夾誤差,預計五軸平台數控工具機的市場規模將以10.35%的複合年成長率成長。研磨和焊接機則為細分市場增添了深度:摩擦攪拌焊接無需填充材即可連接電池外殼,而研磨則可在渦輪盤上實現鏡面拋光效果。

5軸及以上加工中心類別充分說明了價值正從單純的主軸功率轉向柔軟性。整合式刀庫可在單一加工週期內管理數百種不同的刀具,加工鋁、鈦和複合材料。利用探針程序進行現場幾何檢驗,雖然會增加材料成本,但可以減少廢棄物。早期採用者發現,一旦操作員掌握了同步軸控制,生產效率就能提高18%。這促使零件供應商將多軸加工定位為應對勞動力風險的策略手段,從而推動數控市場朝著更高複雜度的方向發展,而這與車間規模無關。

三軸機床仍佔總裝機量的45.35%,鞏固了其作為簡單加工經濟高效成本績效的地位。然而,對於涉及倒扣或螺旋槽的零件加工,則需要加裝旋轉工作台或引入完整的五軸工具機。五軸及以上工具機市場正以10.35%的複合年成長率成長,這主要得益於銑削和車削加工的整合,使得無需重新裝夾即可進行全方位加工。 CAM軟體的改進和培訓補貼的增加正在促進中端市場對技術的接受,進一步推動高軸數數控工具機市場的擴張。

安裝在四軸系統上的旋轉傾斜工作台為定位加工提供了一種經濟實惠的入門途徑,填補了技術空白。然而,領先的航太製造商越來越需要只有真正的五軸機床才能提供的同步運動能力。 FANUC的500i-A 控制器可將 CPU 效能提升 2.7 倍,並針對複雜的刀具路徑最佳化軸間插補。隨著 OEM 廠商展示其縮短的加工週期和更佳的表面光潔度,即使是較保守的機械加工廠也在重新考慮其設備採購計畫。這一趨勢確保了 CNC 市場在傳統模式之外的穩定擴張。

區域分析

亞太地區以51.40%的營收佔有率領先數控工具機市場,這主要得益於中國龐大的供應商生態系統和日本領先的多軸技術。北京的「雙循環」政策促進了國產化,主導了對國產主軸和回饋編碼器的需求。東京透過投資鎂合金加工技術(用於航太運載火箭),進一步鞏固了主導在輕量材料領域的領先地位。韓國政府主導的驅動系統研發正在減少對進口伺服的依賴,並推動全部區域的自主化策略。東南亞國協正受益於供應鏈多元化,吸引需要入門級但可升級設備的工廠。

根據《基礎設施投資與就業法案》和《晶片製造與生產法案》(CHIPS Act),北美地區的製造業回流項目正在蓬勃發展。西門子正投資超過100億美元,擴建其在美國的電氣化硬體生產線,並新增900個技術崗位。FANUC在密西根州投資1.1億美元的園區每年培訓數千名工程師,緩解了勞動力短缺問題。加拿大魁北克的航太叢集正在引進高速鈦合金刀具,而墨西哥的汽車產業基地則在投資軟性加工技術,以滿足電動車組裝的需求。這些政策和私人投資的共同作用,正推動數控(電腦數值控制)市場的發展。

在永續性和電氣化進程的推動下,歐洲經濟正穩定成長。法國航太的補助加速了混合增材-減材機床的試點部署,提升了本土原始設備製造商(OEM)的競爭力。一家德國中型企業正在對老舊銑床進行改造,加裝封閉回路型驅動裝置,以降低能耗,符合歐盟綠色交易的目標。發那FANUC)在伊比利亞半島的辦公室擴張表明,西班牙和葡萄牙對機器人加工單元的需求正在成長。東歐國家正在接手西歐工廠的剩餘產能,從而推動了中型三軸加工中心的訂單成長。儘管面臨宏觀經濟逆風,歐洲仍是塑造未來數控(CNC)市場規格的技術試驗場。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 北美和歐洲因企業回流而對軟性數控設備的需求主導

- 引入由工業4.0主導的兼容數位雙胞胎技術的CNC控制器

- 電動動力傳動系統日益複雜,推動了亞洲多軸CNC訂單的成長。

- 政府對航太精密加工的獎勵措施(日本、法國)

- 自動化數控加工單元可解決全球技術純熟勞工短缺問題。

- 高成長醫療設備領域對微型CNC工具機的需求趨勢

- 市場限制

- 半導體運動控制晶片短缺限制了供應。

- 對五軸加工中心及積層製造/減材混合加工中心的高額資本投入

- 網路化數控系統中的網路安全問題

- 鋼鐵和鋁價波動對中小企業投資收益(ROI) 的影響

- 價值/供應鏈分析

- 監理與技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 投資趨勢與資本投資分析

第5章 市場規模與成長預測

- 按模型

- CNC車床

- CNC銑床

- 數控雷射切割機

- 數控等電漿切割機

- CNC電火花加工工具機(EDM)

- CNC研磨

- CNC繞線機

- 數控焊接機

- 其他機器類型

- 按軸類型

- 三軸

- 第四軸

- 5個或更多軸

- 按組件

- CNC控制器

- 伺服馬達驅動裝置

- 感測器和回饋

- 其他

- 透過控制系統

- 開放回路

- 封閉回路型

- 透過部署

- 獨立式CNC工具工具機

- 整合生產單元(CNC工具機+機器人)

- 最終用戶

- 汽車(包括電動車)

- 航太/國防

- 電力和能源

- 工業機械

- 醫療設備

- 電子裝置和半導體

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 中東和非洲

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Fanuc Corporation

- Siemens AG

- DMG Mori Seiki Co., Ltd.

- Haas Automation, Inc.

- Mitsubishi Electric Corporation

- Okuma Corporation

- Yamazaki Mazak Corporation

- Hurco Companies, Inc.

- JTEKT Corporation

- Dr. Johannes Heidenhain GmbH

- Trumpf Group

- Bosch Rexroth AG

- GSK CNC Equipment Co., Ltd.

- Dalian Machine Tool Group

- Makino Milling Machine Co., Ltd.

- Hyundai Wia Corporation

- Fagor Automation

- Brother Industries, Ltd.

- Amera-Seiki, Inc.

- Fair Friend Group(FFG)

- Doosan Machine Tools Co., Ltd.

- Hardinge Inc.

- TAKISAWA Machine Tool Co., Ltd.

- Protomatic Inc.

- Metal Craft AMS

- Micromedical LLC

第7章 市場機會與未來展望

The computer numerical controls market size in 2026 is estimated at USD 116.57 billion, growing from 2025 value of USD 108.63 billion with 2031 projections showing USD 165.95 billion, growing at 7.32% CAGR over 2026-2031.

Persistently tight labor markets, near-shoring of production, and the push for Industry 4.0 automation are converging, prompting manufacturers to accelerate investments in multi-axis and digitally connected equipment. Reshoring legislation in the United States and Europe is shifting capital away from low-cost regions toward flexible machining assets that support short lead times in production. Cybersecurity risk is rising in parallel with connectivity, motivating vendors to embed security-by-design features in new controllers. At the same time, sustained high steel and aluminum prices are driving demand for precision processes that minimize scrap. Together, these forces keep the computer numerical controls (CNC) market on a solid growth trajectory even as component shortages create near-term supply friction.

Global Computer Numerical Controls (CNC) Market Trends and Insights

Reshoring-led Demand for Flexible CNC Equipment in North America and Europe

U.S. imports of finished goods from China fell 13% in 2023 while domestic factory investment rose sharply after infrastructure and semiconductor incentives. Incoming work is highly variable, so buyers prefer adaptable 5-axis machines and modular robot cells that handle diverse part families. Near-market production justifies higher capital outlays because freight risks fall and delivery speed improves. Vendors that offer rapid re-tooling and digital setup features gain a competitive edge. This reshoring vector directly enlarges the computer numerical controls market by converting decades of outsourced volumes into local capacity growth.

Industry 4.0-Driven Adoption of Digital-Twin-Enabled CNC Controllers

Digital twins let programmers validate tool paths virtually, cutting physical setup time by 20% with Siemens Sinumerik 828D hardware. Studies show 14.53% productivity gains and 13.9% lower energy use when machines run in closed-loop coordination with their virtual counterparts. Adoption is strongest in aerospace and automotive sectors that need real-time compensation for thermal drift and tool wear. Controller suppliers embed cloud connectivity and AI analytics, turning the computer numerical controls market into a software-centric arena. As license revenues grow, machine builders look to recurring income rather than one-time hardware margin.

Semiconductor Motion-Control Chip Shortages Constraining Supply

Precision servo drives rely on specialty ASICs that remain in short supply, stretching lead times for premium machines to more than nine months. Some builders redesign around available chips, but that demands costly re-qualification. OEMs with secured allocations win share while latecomers lose backlog. The bottleneck suppresses the near-term computer numerical controls market volume despite solid order books.

Other drivers and restraints analyzed in the detailed report include:

- EV Power-train Complexity Boosting Multi-Axis CNC Orders in Asia

- Government Incentives for Aerospace Precision Machining (Japan, France)

- High CAPEX of 5-Axis and Hybrid Additive-Subtractive Machines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC lathes held 22.95% of the computer numerical controls market share in 2025 and remain indispensable for round parts such as shafts and hubs. Continuing EV power-train development raises tolerance demands, so many shops retrofit live tooling and Y-axis capability to conventional turning centers. Milling machines form the next largest slice of the CNC machine market, serving complex mold cavities for aerospace and medical implants. Laser and plasma cutters grow as sheet-metal designs multiply in battery enclosures, and EDM stays relevant for hardened tool steels. The CNC machine market size for 5-axis platforms is poised to grow 10.35% CAGR because single-setup capability slashes fixture time and eliminates reposting errors. Grinding and welding machines add niche depth: friction-stir welding joins battery shells without filler metal, while grinding delivers mirror finishes on turbine discs.

The 5-axis and above category illustrates why value is shifting toward flexibility rather than raw spindle horsepower. Integrated tool changers allow several hundred cutters that handle aluminum, titanium, and composites in one cycle. Probing routines verify geometry in situ, reducing scrap despite high material costs. Early adopters report 18% throughput gains once operators master simultaneous axis commands. Component suppliers therefore treat multi-axis as a strategic hedge against labor risk, pushing the computer numerical controls market toward higher complexity tiers regardless of plant size.

Three-axis units still anchor the installed base with a 45.35% share and attractive price-performance ratios for simple work. Yet part programs with undercuts and helical flutes drive shops to add rotary tables or invest in full five-axis machines. The 5-axis and above segment posts a 10.35% CAGR because it merges milling and turning, enabling machining from all directions without reclamping. Improved CAM software plus training subsidies make the technology accessible to mid-market buyers, widening the computer numerical controls market size for advanced axis counts.

Rotary-tilt tables on 4-axis systems bridge the gap and allow affordable entry into positional machining. However, aerospace primes increasingly require simultaneous motion capability that only true 5-axis delivers. FANUC's 500i-A controller, with 2.7 times CPU power, optimizes axis interpolation for complex tool paths. As OEMs validate shorter cycle times and better surface finishes, even conservative job shops reconsider equipment roadmaps. This dynamic ensures a steady migration that enlarges the computer numerical controls market beyond conventional formats.

The Computer Numerical Controls Market Report is Segmented by Machine Type (CNC Lathe Machines, CNC Milling Machines, and More), Axis Type (3-Axis, and More), Component (CNC Controller, Servo Motor Drive, and More), Control System (Open-Loop, Closed-Loop), Deployment (Stand-Alone CNC Machines, and More), End User (Automotive, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads the CNC machine market with a 51.40% revenue share, anchored by China's vast supplier ecosystem and Japan's trail-blazing multi-axis technology. Beijing's dual-circulation policy encourages local content, spurring demand for domestic spindle makers and feedback encoders. Tokyo's investment in magnesium alloy machining for space launch widens its leadership in lightweight materials. South Korea's state-funded drive system advances cut reliance on imported servos, underlining a regional strategy toward self-sufficiency. ASEAN countries benefit from supply-chain diversification, attracting greenfield plants that require entry-level yet upgradeable equipment.

North America gains momentum as reshoring projects proliferate under the Infrastructure Investment and Jobs Act and the CHIPS Act. Siemens earmarked over USD 10 billion to expand U.S. production lines for electrification hardware, adding 900 skilled roles. FANUC's USD 110 million campus in Michigan trains thousands of technicians annually, alleviating talent shortages. Canadian aerospace clusters in Quebec adopt high rpm titanium cutters, while Mexican automotive hubs invest in flexible machining to service near-term EV assembly demand. The computer numerical controls market thus benefits from synchronized policy and private investment.

Europe shows steady growth amid sustainability mandates and push for electric mobility. French aerospace subsidies accelerate hybrid additive-subtractive machine trials, boosting local OEM competitiveness. Germany's Mittelstand firms retrofit legacy mills with closed-loop drives to cut energy use, aligning with EU Green Deal goals. FANUC's Iberia office expansion signals rising demand in Spain and Portugal for robotized machining cells. Eastern European countries capture overflow work from Western plants, driving orders for mid-range 3-axis centers. Despite macro headwinds, Europe remains a technology testbed that shapes future computer numerical controls market specifications.

- Fanuc Corporation

- Siemens AG

- DMG Mori Seiki Co., Ltd.

- Haas Automation, Inc.

- Mitsubishi Electric Corporation

- Okuma Corporation

- Yamazaki Mazak Corporation

- Hurco Companies, Inc.

- JTEKT Corporation

- Dr. Johannes Heidenhain GmbH

- Trumpf Group

- Bosch Rexroth AG

- GSK CNC Equipment Co., Ltd.

- Dalian Machine Tool Group

- Makino Milling Machine Co., Ltd.

- Hyundai Wia Corporation

- Fagor Automation

- Brother Industries, Ltd.

- Amera-Seiki, Inc.

- Fair Friend Group (FFG)

- Doosan Machine Tools Co., Ltd.

- Hardinge Inc.

- TAKISAWA Machine Tool Co., Ltd.

- Protomatic Inc.

- Metal Craft AMS

- Micromedical LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reshoring-led Demand for Flexible CNC Equipment in North America and Europe

- 4.2.2 Industry 4.0-Driven Adoption of Digital-Twin-Enabled CNC Controllers

- 4.2.3 EV Power-train Complexity Boosting Multi-Axis CNC Orders in Asia

- 4.2.4 Government Incentives for Aerospace Precision Machining (Japan, France)

- 4.2.5 Automated CNC Cells Addressing Global Skilled-Labor Shortages

- 4.2.6 Micro-CNC Demand from High-Growth Medical Device Segment

- 4.3 Market Restraints

- 4.3.1 Semiconductor Motion-Control Chip Shortages Constraining Supply

- 4.3.2 High CAPEX of 5-Axis and Hybrid Additive-Subtractive Machines

- 4.3.3 Cyber-Security Concerns with Networked CNC Systems

- 4.3.4 Volatile Steel and Aluminum Prices Impacting SME ROI

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Trends and Capital Expenditure Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Machine Type

- 5.1.1 CNC Lathe Machines

- 5.1.2 CNC Milling Machines

- 5.1.3 CNC Laser Cutting Machines

- 5.1.4 CNC Plasma Cutting Machines

- 5.1.5 CNC Electric Discharge Machines (EDM)

- 5.1.6 CNC Grinding Machines

- 5.1.7 CNC Winding Machines

- 5.1.8 CNC Welding Machines

- 5.1.9 Other Machine Types

- 5.2 By Axis Type

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis and Above

- 5.3 By Component

- 5.3.1 CNC Controller

- 5.3.2 Servo Motor Drive

- 5.3.3 Sensors and Feedback

- 5.3.4 Others

- 5.4 By Control System

- 5.4.1 Open-loop

- 5.4.2 Closed-loop

- 5.5 By Deployment

- 5.5.1 Stand-alone CNC Machines

- 5.5.2 Integrated Production Cells (CNC + Robotics)

- 5.6 By End User

- 5.6.1 Automotive (incl. EV)

- 5.6.2 Aerospace and Defense

- 5.6.3 Power and Energy

- 5.6.4 Industrial Machinery

- 5.6.5 Medical Devices

- 5.6.6 Electronics and Semiconductor

- 5.6.7 Other End Users

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 Latin America

- 5.7.2.1 Mexico

- 5.7.2.2 Brazil

- 5.7.2.3 Argentina

- 5.7.2.4 Rest of Latin America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Middle East and Africa

- 5.7.5 Asia-Pacific

- 5.7.5.1 China

- 5.7.5.2 Japan

- 5.7.5.3 South Korea

- 5.7.5.4 India

- 5.7.5.5 Australia

- 5.7.5.6 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Fanuc Corporation

- 6.4.2 Siemens AG

- 6.4.3 DMG Mori Seiki Co., Ltd.

- 6.4.4 Haas Automation, Inc.

- 6.4.5 Mitsubishi Electric Corporation

- 6.4.6 Okuma Corporation

- 6.4.7 Yamazaki Mazak Corporation

- 6.4.8 Hurco Companies, Inc.

- 6.4.9 JTEKT Corporation

- 6.4.10 Dr. Johannes Heidenhain GmbH

- 6.4.11 Trumpf Group

- 6.4.12 Bosch Rexroth AG

- 6.4.13 GSK CNC Equipment Co., Ltd.

- 6.4.14 Dalian Machine Tool Group

- 6.4.15 Makino Milling Machine Co., Ltd.

- 6.4.16 Hyundai Wia Corporation

- 6.4.17 Fagor Automation

- 6.4.18 Brother Industries, Ltd.

- 6.4.19 Amera-Seiki, Inc.

- 6.4.20 Fair Friend Group (FFG)

- 6.4.21 Doosan Machine Tools Co., Ltd.

- 6.4.22 Hardinge Inc.

- 6.4.23 TAKISAWA Machine Tool Co., Ltd.

- 6.4.24 Protomatic Inc.

- 6.4.25 Metal Craft AMS

- 6.4.26 Micromedical LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

精密契約製造市場預測至2034年-按合約類型、服務類型、材料、最終用戶和地區分類的全球分析

精密契約製造市場預測至2034年-按合約類型、服務類型、材料、最終用戶和地區分類的全球分析 全球電腦數值控制(CNC) 工具機市場:機會與策略展望(至 2035 年)

全球電腦數值控制(CNC) 工具機市場:機會與策略展望(至 2035 年) 德國機器人數控車床:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)2026年全球電腦數值控制(CNC) EtherCAT 控制器市場報告

德國機器人數控車床:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)2026年全球電腦數值控制(CNC) EtherCAT 控制器市場報告 電腦數值控制(CNC) 市場報告:按機器類型、最終用途行業和地區分類 (2026–2034)

電腦數值控制(CNC) 市場報告:按機器類型、最終用途行業和地區分類 (2026–2034) 電腦數值控制(CNC)工具機市場:按類型、最終用途和地區分類

電腦數值控制(CNC)工具機市場:按類型、最終用途和地區分類 電腦數值控制(CNC) 機械市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、組件、應用、材質、製程及最終使用者分類

電腦數值控制(CNC) 機械市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、組件、應用、材質、製程及最終使用者分類 全球電腦數值控制(CNC) 市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)2026年全球精密車削產品製造市場報告2026年全球電腦數值控制市場報告

全球電腦數值控制(CNC) 市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)2026年全球精密車削產品製造市場報告2026年全球電腦數值控制市場報告