|

市場調查報告書

商品編碼

1911739

精密車削產品製造:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Precision Turned Product Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

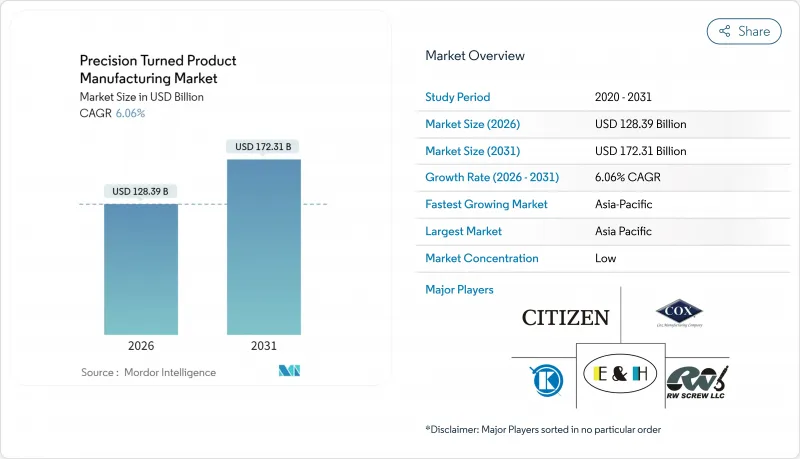

預計精密車削產品製造市場將從 2025 年的 1,210.5 億美元成長到 2026 年的 1,283.9 億美元,到 2031 年將達到 1,723.1 億美元,2026 年至 2031 年的複合年成長率為 6.06%。

這一擴張標誌著製造業正持續從大規模機械加工轉向精密工程零件,從而支持航太業的復甦、電動汽車 (EV) 動力系統日益複雜的需求以及植入式醫療設備的微型化。自動化製造單元也推動了強勁的需求,這些單元需要具有可重複公差的超高精度零件。競爭機會集中在那些將多軸數控加工能力與無人操作相結合的供應商身上,這使他們能夠贏得北美和歐洲的回流業務。隨著鈦和高溫合金在引擎、植入和高溫系統中的佔有率不斷成長,材料策略也在不斷演變,而鋼材仍然是大規模生產的基礎。工具機製造商 (OEM) 的策略性資本投資支援本地化、高利潤的生產線,這些生產線能夠保護智慧財產權並確保供應鏈的穩定性。

全球精密車削產品製造市場趨勢與洞察

精密加工供應鏈回歸日本

為了降低地緣政治和物流風險,北美和歐洲的原始設備製造商(OEM)正在將加工項目遷回國內。美國《晶片製造和整合產品法案》(CHIPS Act)和歐盟主權基金提供的超過1000億美元的激勵措施總合提供了支持。 GKN Aerospace公司對其位於瑞典特羅爾海坦工廠的生產線進行升級,顯示自動化如何在縮短前置作業時間的同時,實現具有成本競爭力的在地化生產。客戶願意為國內供應商支付溢價,因為他們優先考慮的是關鍵零件的可靠供應,而非單純的成本考量。國防合約強制要求從國內或盟國採購,進一步加速了這一趨勢。哈斯自動化公司在內華達州投資3億美元興建的工廠就是一個典型的例子,該工廠透過增加本地主軸生產,避免了運輸延誤對客戶的影響。

電動車傳動系統零件的普及

隨著電動車架構以更少、更精確、熱穩定性更高的零件取代成千上萬的機械零件,精密車削產品製造市場正朝著微米級公差方向發展。比亞迪和蔚來等中國品牌指定使用精密車削的定子殼體和冷卻液接頭,需要多軸瑞士型車削和機上測頭。西方汽車製造商也正在效仿,但兩國對國產化率的限制促使企業增加對本地加工商的投入。隨著全球電動車普及率的提高,市場需求正從單一國家轉向多區域,這為合格供應商的長期訂單保障奠定了基礎。

熟練機械師長期短缺

預計到2030年,美國製造業將面臨210萬名工人的勞動力缺口,其中精密機械加工領域尤其難以招募到合適的人才,因為工具技師需要長達五年的在職培訓。德國和日本的企業也報告了類似的勞動力短缺問題,導致工資上漲和生產力受限。儘管學徒制和高中教育計畫行之有效,但由於人才培育與生產力提升之間存在時間滯後,勞動市場依然緊張。中小企業承受的壓力最大,人才經常流失到能夠提供更高薪資和機器人技術培訓的跨國公司。

細分市場分析

預計到2025年,CNC加工將佔精密車削產品製造市場65.98%的佔有率,到2031年將以8.41%的複合年成長率成長,在此期間新增市場規模約為422億美元。自動化托盤池、刀具預調器和機上測量等技術正在將單一主軸轉變為無人化生產單元,從而緩解技術純熟勞工短缺的問題。發那科(FANUC)已展示了一個可全天候運作的無人化生產單元,其主軸運轉率超過90%,單位工時減少了一半。雖然手排車床仍用於原型製作和小批量傳統零件生產,但隨著多軸數控工具工具機取代順序裝夾進行連續加工,其市場佔有率正在逐年下降。

如今,機械分析平台能夠為預測性維修儀錶板提供資訊,在主軸軸承磨損或滾珠螺桿間隙等問題出現尺寸偏差之前,及時向工程師發出警報。早期採用者報告稱,在不增加檢驗人員的情況下,廢品率降低了 20%。系統整合商正在將機器人和視覺系統結合,以實現二次去毛邊和清潔流程的自動化,從而將單次裝夾的優勢擴展到下游工序。這種端到端的自動化支援可追溯性的另一個飛躍,使數位化數控生產線成為航太、電動車和醫療專案的核心生產模式。

預計到2025年,瑞士型車床將佔據精密車削產品製造市場36.20%的佔有率,並預計在2031年之前保持9.92%的複合年成長率,這主要得益於伺服新型伺服架構的五軸和七軸聯動加工技術的發展。津上(Tsugami)的SS207-II-5AX整合了B軸交叉鑽孔模組,只需一次裝夾即可完成骨螺絲和導管零件的加工。西鐵城(Citizen)的LFV切削功能將伺服驅動的振動與主軸旋轉同步,從而在加工黏性合金時有效破碎切屑,將刀具壽命延長高達30%,並顯著減少加工特殊金屬時的停機時間。

雖然傳統的凸輪式螺紋加工中心仍然適用於通用軸和配件的加工,但價格壓力和更嚴格的表面光潔度要求正迫使加工商轉向數控機床。混合式車銑複合加工中心透過將反向旋轉主軸和Y軸銑床在水平平台上,模糊了工具機類別的界限,在不增加占地面積的情況下有效地提高了零件的複雜性。先進的加工車間在評估工具機採購時,不僅考慮加工週期,還考慮支援MTConnect的資料互通性,從而實現封閉回路型品管。

區域分析

預計亞太地區將在2025年以38.60%的市佔率引領精密車削產品製造市場,並在2031年之前以7.33%的複合年成長率持續成長。這主要得益於中國無與倫比的電動車生產規模以及印度的「印度製造」激勵政策。比亞迪等中國整車製造商正向國內加工廠提供滾動預測,用於生產馬達外殼和冷媒閥體,從而保持遠高於競爭對手的主軸運轉率。印度透過對新工具機資本投資提供15年免稅期來吸引外資,而Endo公司位於印多爾的工廠獲得FDA已通過核准,也凸顯了印度在受目標產品領域的崛起。日本作為高精度工具機的發源地,正專注於為衛星、手術機器人和微流體設備等應用領域生產高附加價值、小批量零件。東南亞國家正在吸引中型外包商,生產對成本敏感的零件,例如壓縮機接頭和遊戲機軸,從而使該地區的生產結構多樣化。

在北美,由於航太業的復甦和聯邦政府對製造業回流的支持,需求正在加速成長。波音公司嚴格的交付目標促使其向華盛頓州、德克薩斯州和安大略省的合規車削零件供應商下了更多批量訂單。哈斯自動化公司位於內華達州的主軸工廠正在縮短美國國內加工廠向高規格CNC工具機轉型過程中的前置作業時間。墨西哥正在根據美國墨加協定(USMCA)擴大其大陸網路,提供經濟高效的組裝和優惠的關稅結構,使得複雜零件能夠在距離美國最終組裝地點兩到三天的時間內送達。

歐洲正利用嚴格的機械和醫療法規來取得競爭優勢。一家德國中型企業(Mittelstand)專門從事豪華汽車銑削原型機的製造,而瑞典一家機器人航太部門則實現了鈦合金風扇葉片的無人重複生產。歐盟法規2023/1230強制要求進行風險評估和CE認證,擴大了與進口產品的合格性差距,並引導原始設備製造商(OEM)選擇經過審核的歐洲供應商。永續性目標正促使工廠進行二氧化碳排放認證,而領先先驅者正在整合太陽能冷卻系統和閉合迴路壓塊技術,以在新版「綠色交易」框架下獲得採購積分。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 調查結果

- 調查先決條件

- 調查範圍

第2章調查方法

- 分析和調查方法

- 調查階段

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 政府法規和政策

- 工業技術趨勢

- 價值鏈/供應鏈分析

- 新冠疫情對市場的影響

第5章 市場動態

- 市場促進因素

- 航太業的成長推動了市場發展。

- 汽車產業正在引領市場

- 市場限制

- 技術純熟勞工短缺

- 市場機遇

- 工業4.0將在2025年徹底改變製造業。

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第6章 市場細分

- 透過操作

- 手動操作

- 數控操作

- 按機器類型

- 自動螺絲加工機

- 旋轉式傳輸機

- 電腦數值控制(CNC)

- 車床或車削中心

- 依材料類型

- 塑膠

- 鋼

- 其他材料類型

- 按最終用戶行業分類

- 車

- 電子設備

- 防禦

- 衛生保健

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 孟加拉

- 土耳其

- 韓國

- 澳洲

- 印尼

- 亞太其他地區

- 中東和非洲

- 埃及

- 南非

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 其他

- 北美洲

第7章 競爭情勢

- 市場集中度概覽

- 公司簡介

- Cox Manufacturing Co.

- Citizen FINEDEVICE(Citizen Group)

- Zhejiang Ronnie Precision

- RW Screw Products

- E& H Precision

- KDK Finish-Turning

- Astro Machine Works

- Melling Tool Co.

- EJ Basler Co.

- Hall Industries Incorporated

- Supreme Machined Products Company

- Alpha Grainger Mfg

- C & M Machine Products

- Alger Precision Machining

- Tompkins Products Inc.

- 其他公司

第8章:市場機會與未來趨勢

第9章附錄

The Precision Turned Product Manufacturing market is expected to grow from USD 121.05 billion in 2025 to USD 128.39 billion in 2026 and is forecast to reach USD 172.31 billion by 2031 at 6.06% CAGR over 2026-2031.

The expansion marks an ongoing shift from volume-based machining toward precision-engineered parts that support aerospace recovery, electric-vehicle (EV) drivetrain complexity, and the miniaturization of implantable medical devices. Demand resilience also stems from automated manufacturing cells that require ultra-precise components with repeatable tolerances. Competitive opportunity centers on suppliers that combine multi-axis CNC capability with lights-out operations, allowing them to capture reshored programs in North America and Europe. Material strategy is evolving as titanium and super-alloys gain share in engines, implants, and high-temperature systems, even while steel remains the volume foundation. Strategic capital investments by machine tool builders and OEMs bolster localized, higher-margin production runs that protect intellectual property and ensure supply-chain certainty.

Global Precision Turned Product Manufacturing Market Trends and Insights

Reshoring of Precision-Machining Supply Chains

North American and European OEMs are bringing machining programs home to mitigate geopolitical and logistics risks, backed by more than USD 100 billion in combined incentives under the U.S. CHIPS Act and the EU Sovereignty Fund. GKN Aerospace's upgrade of its Trollhattan, Sweden, cell shows how automation enables cost-competitive local production while shrinking lead times. Customers reward domestic suppliers with price premiums because secure access to mission-critical parts outweighs pure cost concerns. Defense contracts intensify the movement by requiring domestic or allied sourcing. Haas Automation's USD 300 million Nevada plant is a case in point, adding regional spindle production to shield customers from shipping delays.

Proliferation of EV Drivetrain Parts

EV architectures replace thousands of mechanical parts with a smaller set of highly accurate, thermally stable components, pushing the Precision Turned Product Manufacturing market toward micron-level tolerances. Chinese brands such as BYD and NIO specify precision-turned stator housings and coolant junctions that demand multi-axis Swiss-type machining backed by on-machine probing. European and U.S. automakers follow suit, yet domestic-content rules in both regions divert a rising share of the spend to local job shops. As global EV adoption climbs, the market gains a multi-regional demand base rather than a single-country concentration, underwriting long-term order stability for qualified suppliers.

Persistent Skilled-Machinist Shortage

The U.S. faces a projected 2.1 million manufacturing-role deficit by 2030, and precision machining tops the hard-to-hire list because toolmakers require up to five years of on-the-job mentoring. German and Japanese firms report similar talent gaps that inflate wages and constrain throughput. Apprenticeship programs and high-school outreach help, yet the lag between intake and productivity keeps the labor market tight. Small and medium-sized enterprises (SMEs) feel the squeeze most, often losing workers to large multinationals that can pay premiums and offer robotics training.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization of Medical Implants & Devices

- Aerospace OEM Ramp-ups Post-B737 MAX & A320neo

- Volatility in Specialty Alloy Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC processes own 65.98% of the Precision Turned Product Manufacturing market share in 2025 and are projected to expand at an 8.41% CAGR to 2031, adding roughly USD 42.2 billion in incremental Precision Turned Product Manufacturing market size during the period. Automated pallet pools, tool presetters, and on-machine gauging turn individual spindles into unattended production cells that counterbalance the skilled-labor deficit. FANUC demonstrates 24/7 lights-out cells that log spindle uptimes above 90%, cutting unit labor minutes by half. Manual lathes persist for prototyping and micro-volume heritage parts, yet their share shrinks every year as a series of multi-axis CNC machines replace sequential setups.

Machine analytics platforms now feed predictive maintenance dashboards that alert technicians to spindle bearing wear or ball-screw backlash before dimensional drift occurs. Early adopters report scrap reductions of 20% without adding inspection headcount. Integrators are bundling robots with vision systems to automate secondary deburr and wash cycles, thereby extending the single-setup advantage deeper into the downstream flow. Such end-to-end automation underpins the next leap in traceability, positioning digital CNC lines as the core production model across aerospace, EV, and medical programs.

Swiss-type lathes captured 36.20% of the 2025 Precision Turned Product Manufacturing market size and are pacing a 9.92% CAGR through 2031 as new servo architectures deliver five- and seven-axis simultaneous cutting. Tsugami's SS207-II-5AX integrates a B-axis cross-drill module, allowing complete machining of bone screws and catheter components in one clamp. Citizen's LFV cutting function synchronizes servo-driven oscillation with spindle rotation to break chips in sticky alloys, extending tool life by up to 30% and slashing downtime on exotic metals.

Conventional cam-based screw machines remain relevant for commodity shafts and fittings, yet pricing pressure and tighter surface-finish specs push converters to migrate toward CNC models. Hybrid mill-turn centers blur category lines by integrating opposing spindles and Y-axis milling within a horizontal platform, effectively amplifying part complexity without increasing floor space. Forward-looking shops evaluate machine-tool purchases not only on cycle time but also on MTConnect-enabled data interoperability that powers closed-loop quality controls.

The Precision Turned Product Manufacturing Market Report is Segmented by Operation (Manual Operation, CNC Operation), by Machine Type (Automatic Screw Machines, CNC Swiss-Type and More), by Material Type (Steel, Aluminum and More), by End-User Industry (Automotive & EV, Aerospace & Defense and More), and by Geography (North America, South America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the Precision Turned Product Manufacturing market in 2025 with 38.60% share and a 7.33% CAGR toward 2031, anchored by China's unrivaled EV production scale and India's Make-in-India policy incentives. Chinese OEMs such as BYD place rolling forecasts on domestic machine shops for motor housings and refrigerant valve bodies, keeping spindle utilization high even amid price competition. India lures foreign investment with 15-year tax holidays for green-field machinery assets, and Endo's FDA-approved Indore site validates the country's ascent in regulated products Japan, still the birthplace of high-precision machine tools, focuses on low-volume, high-value components for satellites, surgical robots, and microfluidics. Southeast Asian states attract mid-tier outsourcing for cost-sensitive parts like compressor fittings and gaming-device shafts, diversifying the regional output mix.

North America follows with accelerating demand fueled by aerospace rebound and federal reshoring credits. Boeing's exacting delivery targets translate into expanded blanket orders for compliant turn-part suppliers across Washington, Texas, and Ontario. Haas Automation's Nevada spindle plant shortens lead times for domestic job shops switching to higher-spec CNCs. Mexico amplifies the continental network under USMCA, offering cost-effective assembly and favorable duty structures that keep complex parts within a two-to-three-day logistics radius of U.S. final-assembly centers.

Europe leverages stringent machinery and medical regulations to maintain a competitive moat. Germany's Mittelstand specializes in mill-turn prototyping for luxury vehicles, while Sweden's roboticized aerospace cells showcase lights-out repeatability in titanium fan blades. EU Regulation 2023/1230 mandates risk assessments and CE marking that widen compliance gaps versus imports, steering OEMs toward audited European suppliers. Sustainability targets push plants to certify CO2 footprints, and early adopters integrate solar-powered coolant chillers and closed-loop chip briquetting to score procurement points under new green-deal frameworks.

- Cox Manufacturing Co.

- Citizen FINEDEVICE (Citizen Group)

- Zhejiang Ronnie Precision

- R W Screw Products

- E&H Precision

- KDK Finish-Turning

- Astro Machine Works

- Melling Tool Co.

- E. J. Basler Co.

- Hall Industries Incorporated

- Supreme Machined Products Company

- Alpha Grainger Mfg

- C & M Machine Products

- Alger Precision Machining

- Tompkins Products Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends in the Industry

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of the Aerospace Industry is Driving the Market

- 5.1.2 Automotive Industry is Driving the Market

- 5.2 Market Restraints

- 5.2.1 Skilled Labor Shortage

- 5.3 Market Opportunities

- 5.3.1 Industry 4.0 Revolutionizing the Manufacturing Industry By 2025

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Operation

- 6.1.1 Manual Operation

- 6.1.2 CNC Operation

- 6.2 By Machine Types

- 6.2.1 Automatic Screw Machines

- 6.2.2 Rotary Transfer Machines

- 6.2.3 Computer Numerically Controlled (CNC)

- 6.2.4 Lathes or Turning centers

- 6.3 By Material Type

- 6.3.1 Plastic

- 6.3.2 Steel

- 6.3.3 Other Material Types

- 6.4 By End-user Industry

- 6.4.1 Automobile

- 6.4.2 Electronics

- 6.4.3 Defense

- 6.4.4 Healthcare

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.1.3 Mexico

- 6.5.2 Europe

- 6.5.2.1 Germany

- 6.5.2.2 France

- 6.5.2.3 United Kingdom

- 6.5.2.4 Italy

- 6.5.2.5 Spain

- 6.5.2.6 Russia

- 6.5.2.7 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Bangladesh

- 6.5.3.5 Turkey

- 6.5.3.6 South Korea

- 6.5.3.7 Australia

- 6.5.3.8 Indonesia

- 6.5.3.9 Rest of Asia-Pacific

- 6.5.4 Middle East and Africa

- 6.5.4.1 Egypt

- 6.5.4.2 South Africa

- 6.5.4.3 Saudi Arabia

- 6.5.4.4 Rest of Middle East and Africa

- 6.5.5 Rest of the World

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Cox Manufacturing Co.

- 7.2.2 Citizen FINEDEVICE (Citizen Group)

- 7.2.3 Zhejiang Ronnie Precision

- 7.2.4 R W Screw Products

- 7.2.5 E&H Precision

- 7.2.6 KDK Finish-Turning

- 7.2.7 Astro Machine Works

- 7.2.8 Melling Tool Co.

- 7.2.9 E. J. Basler Co.

- 7.2.10 Hall Industries Incorporated

- 7.2.11 Supreme Machined Products Company

- 7.2.12 Alpha Grainger Mfg

- 7.2.13 C & M Machine Products

- 7.2.14 Alger Precision Machining

- 7.2.15 Tompkins Products Inc.

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

電腦數值控制(CNC) 機械市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、組件、應用、材質、製程及最終使用者分類

電腦數值控制(CNC) 機械市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、組件、應用、材質、製程及最終使用者分類 電腦數值控制(CNC):市場佔有率分析、產業趨勢與統計資料、成長預測 (2026-2031)

電腦數值控制(CNC):市場佔有率分析、產業趨勢與統計資料、成長預測 (2026-2031) 全球電腦數值控制(CNC) 市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)

全球電腦數值控制(CNC) 市場規模、佔有率、趨勢和成長分析報告(2026-2034 年) 2026年全球精密車削產品製造市場報告2026年全球電腦數值控制市場報告2026年全球電腦數值控制(CNC)機械市場報告2026年全球電腦數值控制(CNC)縫紉機市場報告全球CNC工具機市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034年)

2026年全球精密車削產品製造市場報告2026年全球電腦數值控制市場報告2026年全球電腦數值控制(CNC)機械市場報告2026年全球電腦數值控制(CNC)縫紉機市場報告全球CNC工具機市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034年) 全球電腦數值控制解決方案市場,2026-2030年

全球電腦數值控制解決方案市場,2026-2030年 線切割放電加工市場:按產品類型、機器類型、應用、最終用途和產業細分分類-2026-2032年全球預測

線切割放電加工市場:按產品類型、機器類型、應用、最終用途和產業細分分類-2026-2032年全球預測