|

市場調查報告書

商品編碼

1934608

汽車自動變速箱:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Automotive Automatic Transmission - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

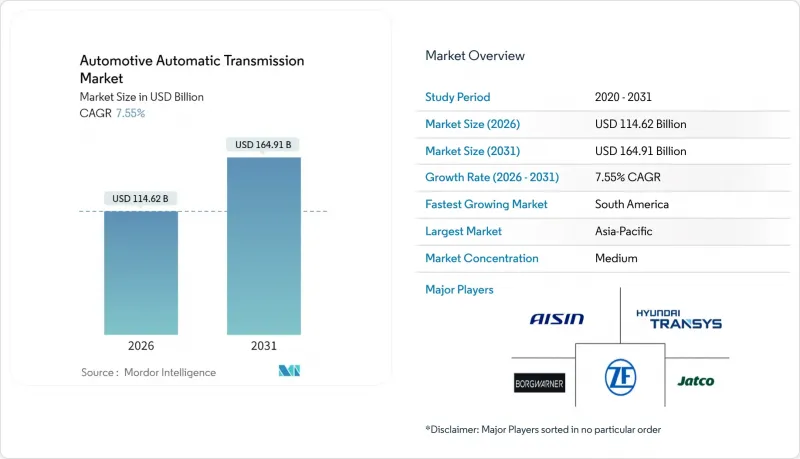

汽車自排變速箱市場預計將從 2025 年的 1,065.7 億美元成長到 2026 年的 1,146.2 億美元,預計到 2031 年將達到 1,649.1 億美元,2026 年至 2031 年的複合年成長率為 7.55%。

日益嚴格的溫室氣體排放法規、快速的電氣化以及消費者對無縫駕駛體驗的需求,持續重塑汽車變速箱市場的技術投資重點。關鍵的監管目標——尤其是美國環保署 (EPA) 提出的在 2027-2032 年款車型中將車輛平均二氧化碳排放降低 50% 的目標——正推動著汽車製造商 (OEM) 向高效自動變速箱、無段變速箱(CVT) 和雙離合器變速箱 (DCT) 轉型。電氣化動力總成正在加速這項變革。專用混合動力變速箱、多段電力驅動橋和軟體定義控制模組是車型更新周期中的核心。競爭優勢取決於人工智慧賦能的換檔策略和空中升級架構的整合,這將有助於降低合規成本、創造業務收益並降低汽車變速箱市場的保固風險。

全球汽車自動變速箱市場趨勢與洞察

加強全球二氧化碳排放法規

美國環保署 (EPA) 設定了到 2032 年年輕型車輛平均燃油經濟性達到 85 克/英里的目標,因此提高變速箱效率對於實現這一目標至關重要。雖然乘用車和輕型卡車每年 2% 的企業平均燃油經濟性 (CAFE) 提升目標日益緊迫,但重型皮卡則面臨著更嚴格的每年 10% 的增幅。在模擬測試中,預測性人工智慧換檔策略已將油耗降低了 10.42%。在充電基礎設施不完善的地區,汽車製造商正將變速箱升級定位為更快、更經濟的減排方式,這使得汽車變速箱市場成為推動監管的關鍵因素。

轉向緩解都市區的堵塞

儘管在印度,自動變速箱的價格比手排變速箱高出約6109美元,但孟買和雅加達等主要城市的走走停停的交通狀況仍然推動了對自動變速箱的需求。印度政府的「印度製造」計畫和東協的混合動力汽車稅收優惠等本土化方案正在縮小這一價格差距。更年輕、更精通技術的消費者越來越傾向於將自動變速箱與減少駕駛疲勞和提高實際燃油經濟性聯繫起來,加速了自動變速箱在汽車變速箱市場的普及。

高成本且複雜

自動變速箱價格溢價顯著,61%的印度買家選擇手排變速箱。 8速和10速等多速變速箱增加了電子控制閥體和複雜的液壓系統,這限制了研討會的數量,並增加了總擁有成本(TCO)。雖然愛信等供應商的本地化努力降低了進口關稅,但無法完全消除材料成本差距,這限制了它們在汽車變速箱市場的普及。

細分市場分析

到2025年,自動變速箱將佔汽車變速箱市場45.60%的佔有率。高性能雙離合器變速箱目前正以3.63%的複合年成長率快速成長,吸引了新興市場從豪華轎車到緊湊型轎車等各類車型的需求,從而支撐了該細分市場的強勁勢頭。在日益嚴格的燃油經濟性法規下,人工智慧驅動的換檔邏輯、快速換檔功能和鎖定式液壓變速箱等技術也推動了這一成長。

電氣化代表設計上的轉折點,而非生存威脅。例如,伊頓的四速變速箱等商用電動卡車多速變速箱表明,當負載容量和爬坡能力至關重要時,效率的提升足以抵消重量的增加。在汽車變速箱市場,隨著原始設備製造商(OEM)透過機械改進和軟體更新相結合的方式提供售後升級,自動變速箱平台預計將繼續存在。

到2025年,汽油動力系統將佔汽車總銷量的60.95%,而混合動力汽車預計將以12.62%的複合年成長率成長,成為汽車變速箱市場中成長最快的細分市場。泰國和印尼的監管機構已降低了符合條件的混合動力汽車的銷售稅和增值稅稅率,這將加速汽車製造商將專用混合動力變速箱整合到其區域產品陣容中。

雖然電池式電動車主要依賴單速減速器,但研究表明,多級電動驅動裝置有望延長高速公路行駛里程。同時,柴油引擎在重型商用車領域仍然佔據主導地位,因為該領域對扭矩的需求需要堅固耐用的齒輪組。隨著各國充電基礎設施發展不平衡,混合動力系統用汽車變速箱的市場規模將持續擴大。

區域分析

亞太地區仍然是汽車變速箱市場最大的貢獻者,這主要得益於中國龐大的市場規模以及印度在「印度製造」計劃下大力推進的本地化生產。採埃孚在中國擁有超過50家工廠和技術中心,並計劃在2031年將其在該地區的銷售佔有率提升至30%。

到2031年,南美洲將以12.76%的複合年成長率實現最快成長。阿根廷的稅收改革使中檔汽車價格降低了高達20%,提高了汽車的可負擔性,並促進了自動變速箱的普及。哥倫比亞的八家組裝廠和巴西成熟的供應鏈為該地區製造地的擴張提供了支持,儘管貨幣波動和政治風險限制了資本投資決策。

北美和歐洲的汽車產量保持穩定,但技術創新步伐迅速。汽車變速箱市場持續專注於高階升級,美國環保署(EPA)的溫室氣體減排目標和聯合國歐洲經濟委員會(UNECE)R155網路安全法規推動了對新一代控制模組和軟體硬體的需求。中東和非洲地區受都市化和車輛現代化進程的驅動,擁有長期成長潛力,但目前較低的車輛普及率正在減緩近期的成長速度。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 日益嚴格的全球二氧化碳排放標準和CAFE法規正在推動汽車製造商對高效自動變速箱、無段變速箱和雙離合器變速箱(DCT)的需求。

- 都市區擁擠促使新興經濟體的消費者轉向自動駕駛汽車

- 隨著混合動力汽車和XEV的普及,需要專用的電子控制變速箱(ECTV、DHT)。

- 可透過OTA升級的TCMS系統開啟了新的軟體業務收益來源。

- 亞太地區先進自動變速箱製造的生產連結獎勵計畫

- 人工智慧最佳化的換班調度可提高燃油經濟性並延長動力傳動系統壽命

- 市場限制

- 與手排變速箱相比,單位成本更高,維修更複雜。

- 半導體短缺擾亂了傳統中醫藥和機電一體化供應鏈

- 輸電ECU網路安全成本不斷增加(UNECE WP.29)

- 保固問題(例如通用汽車8速變速箱震動)會削弱消費者信心。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按變速器類型

- 自動變速箱(AT)/液力變矩器

- 自動手排變速箱(AMT)

- 無段變速箱(CVT)

- 雙離合器變速箱(DCT)

- 按燃料類型

- 汽油

- 柴油引擎

- 油電混合車

- 電池電動(單速電動驅動)

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 按組件

- 液力變矩器

- 行星齒輪裝置

- 液壓和機電一體化控制

- 變速箱油

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Aisin Seiki Co., Ltd.

- ZF Friedrichshafen AG

- JATCO Ltd.

- Hyundai Transys

- Allison Transmission Holdings

- BorgWarner Inc.

- Magna International Inc.

- Continental AG

- Schaeffler AG

- Eaton Corporation plc

- Valeo SA

- Punch Powertrain NV

- Tremec

- Shaanxi Fast Auto Drive

第7章 市場機會與未來展望

The Automotive Automatic Transmission market is expected to grow from USD 106.57 billion in 2025 to USD 114.62 billion in 2026 and is forecast to reach USD 164.91 billion by 2031 at 7.55% CAGR over 2026-2031.

Tightening greenhouse-gas rules, rapid electrification, and consumer demand for seamless driving continue to recalibrate technology investment priorities across the automotive transmission market. Regulatory milestones-most notably the Environmental Protection Agency's 50% fleet-average CO2 reduction target for model years 2027-2032-are steering original-equipment manufacturers toward higher-efficiency automatic, continuously variable, and dual-clutch systems. Electrified drivelines amplify this shift: dedicated hybrid transmissions, multi-speed e-axles, and software-defined control modules are now central to model-year refresh cycles. Competitive advantage hinges on integrating AI-enabled shift strategies and over-the-air update architectures, which lower compliance costs, unlock service revenue, and cushion warranty risk in the automotive transmission market.

Global Automotive Automatic Transmission Market Trends and Insights

Tight global CO2 regs

The Environmental Protection Agency now targets an 85 g/mile fleet average for light-duty vehicles by 2032, a mandate that elevates transmission efficiency to compliance linchpin status. Corporate Average Fuel Economy increments of 2% per year for cars and light trucks amplify the urgency, while heavy-duty pickups face a steeper 10% annual climb Predictive AI shift strategies have already cut fuel use by 10.42% in simulation trials. OEMs now treat transmission upgrades as a quicker, lower-cost path to reducing tailpipe emissions where charging infrastructure is immature, positioning the automotive transmission market as a key compliance lever

Urban Congestion Shift

Stop-and-go traffic in megacities such as Mumbai and Jakarta bolsters demand for automated gearboxes, despite price premiums hovering near USD 6,109 over manual variants in India. Government localization schemes under Make-in-India and ASEAN hybrid tax breaks are narrowing that pricing gap. Younger, tech-savvy buyers now associate automatics with lower fatigue and better real-world mileage, accelerating penetration in the automotive transmission market.

High cost & complexity

Automatic gearboxes command notable price premiums that retain 61% of India's buyers in manual segments. Multi-speed 8- and 10-speed designs add electronic valve bodies and complex hydraulics, narrowing the pool of service-ready workshops and heightening total cost of ownership. Localization efforts by suppliers such as Aisin ease import duties but cannot fully erase material cost differentials, restraining adoption in the automotive transmission market

Other drivers and restraints analyzed in the detailed report include:

- Hybrid/xEV e-transmissions

- OTA-ready TCMs

- Semiconductor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic units captured 45.60% of the automotive transmission market share in 2025. Performance-oriented dual-clutch variants, now advancing at 3.63% CAGR, appeal to both premium sedans and emerging-market compacts, reinforcing segment resilience. AI-driven shift logic, gear-jump capability, and lock-up torque converters underpin these gains amid mounting fuel-economy regulations.

E-mobility poses design pivots rather than existential threats. Multi-speed boxes for electric commercial trucks, such as Eaton's 4-speed, show that efficiency gains justify added mass when payload or gradeability is critical. The automotive transmission market size for automatic platforms will therefore persist as OEMs combine mechanical refinement with software updates that unlock post-sale upgrades.

Gasoline powertrains held 60.95% revenue in 2025, yet hybrids are surging with a 12.62% CAGR, the highest within the automotive transmission market. Regulators in Thailand and Indonesia cut excise and VAT rates for qualified hybrids, propelling OEMs to bundle dedicated hybrid transmissions into regional line-ups.

Battery-electric vehicles rely mainly on single-speed reducers, but research suggests multi-speed e-drives could extend highway range. Meanwhile, diesel remains entrenched in heavy-duty fleets where torque demands require robust gearsets. The automotive transmission market size for hybrid systems will keep expanding as charging infrastructure matures unevenly across countries.

The Automotive Automatic Transmission Market Report is Segmented by Transmission Type (Automatic Transmission (AT)/Torque Converter, Automatic Manual (AMT), and More), Fuel Type (Gasoline, Diesel, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Torque Converter, Planetary Gear-Set, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific remains the largest contributor to the automotive transmission market, buoyed by China's scale and India's localisation push under the Make-in-India program. ZF targets raising its regional sales share to 30% by 2031, supported by over 50 plants and technical centres in China .

South America posts the fastest growth at 12.76% CAGR through 2031. Argentina's tax reform slashed mid-range vehicle prices by up to 20%, improving affordability and spurring automatic uptake. Colombia's eight assembly plants and Brazil's established supply base underscore the region's widening manufacturing footprint, even as currency volatility and political risk temper capital-spending decisions.

North America and Europe display stable volumes but high technology churn. EPA greenhouse-gas targets and UNECE R155 cybersecurity rules elevate demand for next-generation control modules and software-friendly hardware, keeping the automotive transmission market focused on premium upgrades. The Middle East and Africa offer long-run upside linked to urbanisation and fleet modernisation, though low current motorisation levels delay near-term scale.

- Aisin Seiki Co., Ltd.

- ZF Friedrichshafen AG

- JATCO Ltd.

- Hyundai Transys

- Allison Transmission Holdings

- BorgWarner Inc.

- Magna International Inc.

- Continental AG

- Schaeffler AG

- Eaton Corporation plc

- Valeo SA

- Punch Powertrain NV

- Tremec

- Shaanxi Fast Auto Drive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Global CO2 / CAFE Regulations Spur OEM Demand For High-Efficiency AT, CVT and DCT

- 4.2.2 Urban Congestion Drives Consumer Shift To Automatics in Emerging Economies

- 4.2.3 Hybrid and XEV Proliferation Necessitates Dedicated E-Transmissions (ECTV, DHT)

- 4.2.4 OTA-Upgradeable TCMS Open New Software-Service Revenue Streams

- 4.2.5 Asia-Pacific Production-Linked Incentives for Advanced AT Manufacturing

- 4.2.6 AI-Optimized Shift Scheduling Boosts Fuel Economy and Extends Powertrain Life

- 4.3 Market Restraints

- 4.3.1 High Unit Cost and Repair Complexity Versus Manual Transmissions

- 4.3.2 Semiconductor Shortages Disrupting TCM and Mechatronics Supply Chain

- 4.3.3 Rising Cybersecurity-Compliance Costs for Transmission ECUs (UNECE WP.29)

- 4.3.4 Warranty Issues (E.G., GM 8-Speed Shudder) Dent Consumer Confidence

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD), and Volume (Units))

- 5.1 By Transmission Type

- 5.1.1 Automatic (AT)/Torque-Converter

- 5.1.2 Automated Manual (AMT)

- 5.1.3 Continuously Variable (CVT)

- 5.1.4 Dual-Clutch (DCT)

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Hybrid-Electric

- 5.2.4 Battery-Electric (single-speed e-drive)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Component

- 5.4.1 Torque Converter

- 5.4.2 Planetary Gear-set

- 5.4.3 Hydraulic and Mechatronic Controls

- 5.4.4 Transmission Fluid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Aisin Seiki Co., Ltd.

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 JATCO Ltd.

- 6.4.4 Hyundai Transys

- 6.4.5 Allison Transmission Holdings

- 6.4.6 BorgWarner Inc.

- 6.4.7 Magna International Inc.

- 6.4.8 Continental AG

- 6.4.9 Schaeffler AG

- 6.4.10 Eaton Corporation plc

- 6.4.11 Valeo SA

- 6.4.12 Punch Powertrain NV

- 6.4.13 Tremec

- 6.4.14 Shaanxi Fast Auto Drive

7 Market Opportunities and Future Outlook

2026年全球二合一市場報告

2026年全球二合一市場報告 全球商用車變速箱市場

全球商用車變速箱市場 輕型商用車變速箱市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、燃料類型、齒輪類型、地區和競爭格局分類,2021-2031年

輕型商用車變速箱市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、燃料類型、齒輪類型、地區和競爭格局分類,2021-2031年 汽車變速箱市場:2026-2032年全球市場預測(依變速箱類型、車輛類型、推進系統、傳動系統和銷售管道)自動變速箱市場:按變速箱類型、車輛類型、燃料類型和銷售管道分類-2026-2032年全球市場預測2026年全球汽車自排變速箱市場報告2026年全球汽車變速箱市場報告2026年全球汽車變速箱工程服務外包市場報告

汽車變速箱市場:2026-2032年全球市場預測(依變速箱類型、車輛類型、推進系統、傳動系統和銷售管道)自動變速箱市場:按變速箱類型、車輛類型、燃料類型和銷售管道分類-2026-2032年全球市場預測2026年全球汽車自排變速箱市場報告2026年全球汽車變速箱市場報告2026年全球汽車變速箱工程服務外包市場報告 2026-2034年全球汽車變速箱市場規模、佔有率、趨勢和成長分析報告全球自動變速箱市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球汽車變速箱市場規模、佔有率、趨勢和成長分析報告全球自動變速箱市場規模、佔有率、趨勢和成長分析報告(2026-2034年)