|

市場調查報告書

商品編碼

1934590

數位資產管理(DAM):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)Digital Asset Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

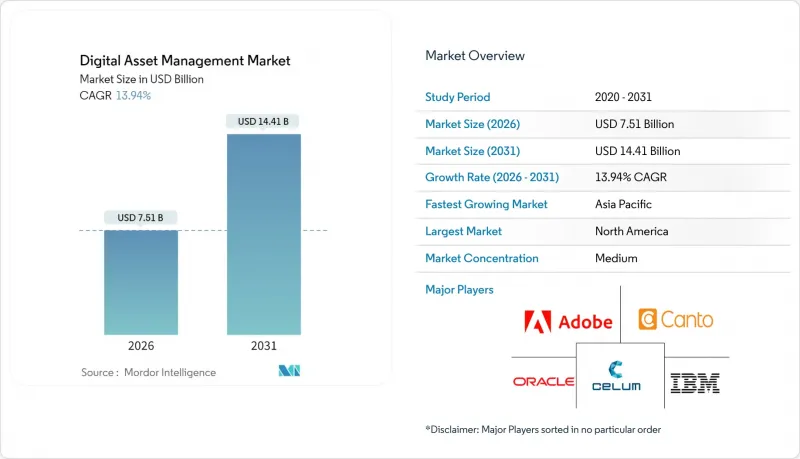

數位資產管理 (DAM) 市場預計到 2025 年將達到 65.9 億美元,預計到 2031 年將達到 144.1 億美元,高於 2026 年的 75.1 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 13.94%。

隨著企業將數位資產管理 (DAM) 從成本中心轉變為全通路內容策略的核心支柱,市場需求正在加速成長。解決方案供應商正在將人工智慧 (AI) 應用於自動標記、版權管理和動態交付,幫助品牌將資產搜尋時間縮短高達 40%。 66% 的大型企業已在試行使用生成式 AI 來大規模個人化。監管變化也是推動成長的催化劑。將於 2025 年 6 月生效的《歐洲無障礙法案》強制要求更豐富的元資料和替代文本,促使企業更新舊有系統。雖然北美在雲端原生架構的採用方面主導,但亞太地區正經歷著最快的成長,這主要得益於行動影片串流媒體的激增。同時,高昂的總體擁有成本和更嚴格的資料主權法規正在阻礙小型企業和受高度監管行業的企業。

全球數位資產管理 (DAM) 市場趨勢與洞察

全通路商務中富媒體資產的數量和速度不斷成長

市場部門目前將39%的預算用於內容製作,其中大部分是短影片和互動形式,這些都需要高階元元資料管理、版權追蹤和渲染管理。整合產品資訊管理 (PIM) 和數位資產管理 (DAM) 的企業可以在實體店、社交電商和市場平台之間重複利用資源,從而在保護品牌價值的同時最大化投資回報率。可口可樂正在將 SKU 層級的數據與創新文件整合,以實現其電商網站的即時個人化。缺乏強大 DAM 系統的公司常常面臨重複製作和訊息不一致的問題,導致宣傳活動效果不佳。

北美正快速向雲端原生、人工智慧增強型數位資產管理平台轉型。

像T-Mobile這樣的公司在從本地資源庫遷移到Adobe Experience Manager Assets後,顯著縮短了創新週期。該平台提供AI驅動的批量標記和渲染生成功能。其SaaS模式免去了高成本的升級費用,並為需要即時存取的分散式團隊提供了強大支援。早期採用者報告稱,營運成本降低,宣傳活動推出速度加快,而競爭對手也在加速遷移。

企業級數位資產管理套件對中小企業而言整體擁有成本過高

授權成本、整合工作以及對數位資產管理 (DAM) 專家的需求,阻礙了許多中小企業採用企業級平台。每個部門通常部署各自的輕量級工具,造成資訊孤島,增加支援成本並使整合工作更加複雜。服務供應商現在提供已打包的變更管理研討會和遷移協助工具,以克服這些採用障礙。

細分市場分析

解決方案垂直領域佔據了 71.90% 的市場佔有率,為企業採用奠定了基礎。該平台現已整合了 AI 轉錄、色彩校正和版權授權功能,使數位資產管理市場成為更廣泛的數位體驗基礎設施不可或缺的一部分。知名品牌正在利用編配規則自動建立宣傳活動工具包,確保創建符合規範的內容集。

同時,業務收益預計將以17.35%的複合年成長率成長,超過軟體收入,因為企業依賴合作夥伴進行分類系統設計、分散式檔案庫遷移以及使用者培訓。包含管治儀錶板和KPI追蹤的託管服務協議正逐漸成為常態。專家實施協助透過提高搜尋速度和降低合規成本,可帶來196%的投資報酬率。

到2025年,雲端部署將佔總收入的63.40%,因為更新可以無縫交付,自動擴展的儲存層級降低了每項資產的總成本。客戶將透過SaaS API全面整合AI視訊智慧,從而在零停機時間內將他們的數位業務擴展到新的管道。

儘管國防、政府和醫療保健產業仍在繼續採用本地部署,但混合模式正變得越來越普遍,敏感的主文件儲存在防火牆後,而衍生文件則從區域雲端串流傳輸。雲端模式繼續佔據主導地位,推動其以 15.53% 的複合年成長率成長,這主要得益於語義搜尋等功能的持續推出。數位資產管理市場進一步鞏固了其在現代技術棧中的主導地位。

區域分析

到2025年,北美將以37.70%的市場佔有率領跑,這主要得益於企業對人工智慧雲端套件的廣泛採用以及超大規模雲端服務供應商不斷提升的合規認證。 DeFi Technologies預計其基於Solana的產品將帶來2.0107億美元的收入,展現了其在代幣化資產管理領域深厚的區域專業知識。此外,該地區成熟的廣告科技廣告科技系統正在推動用戶內容支出的增加,進一步鞏固主導地位。

預計到2031年,亞太地區的複合年成長率將達到17.02%。 2025年雪梨數位資產管理大會(DAM Sydney 2025)重點關注了日常消費品(FMCG)、醫療保健和政府計畫對多語言資產編配日益成長的需求。智慧型手機普及率的提高和社交電商的興起正在推動大規模即時影片個人化應用。政府主導的智慧城市計畫也在推動整合內容中心的發展,以支援公共服務應用程式。

歐洲的成長得益於無障礙存取要求和嚴格的隱私法規。隨著企業對現有資料集進行改造,添加替代文字和詳細的用戶許可追蹤,合規解決方案的數位資產管理市場正在不斷擴大。供應商正透過先進的元元資料管理、版本控制和匿名化功能來滿足 GDPR 和區域本地化法律的要求,從而實現差異化競爭。奧斯本克拉克律師事務所建議,儘早遵守歐洲無障礙存取法律有助於提升品牌聲譽並降低法律風險。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全通路商務中富媒體資產的數量和速度不斷成長

- 北美正快速向雲端原生、人工智慧增強型數位資產管理平台轉型。

- 亞洲對個人化影片串流資產的需求激增

- 整合數位資產管理 (DAM) 和無頭內容管理系統 (CMS) 以實現即時內容傳送

- 在歐洲推廣無障礙法規(WCAG-2.2)並改善元資料標準

- 由生成式人工智慧驅動的自動化標籤技術的出現,正在縮短品牌上市時間(TTM)。

- 市場限制

- 對於中小企業而言,企業級數位資產管理套件的總擁有成本過高

- 資料主權和居住要求限制了跨境資產儲存。

- 碎片化的遺留儲存庫阻礙了無縫遷移

- 缺乏具備人工智慧元元資料管治技能的人員

- 技術展望

- 評估宏觀經濟因素的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析(資金籌措、併購、創業投資活動)

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 透過部署模式

- 本地部署

- 雲(SaaS)

- 按公司規模

- 小型企業

- 主要企業

- 透過使用

- 銷售和行銷支持

- 廣播和出版工作流程

- 產品與電子商務管理

- 照片、圖形和設計資料庫

- 文件和知識管理

- 按最終用戶行業分類

- 媒體與娛樂

- BFSI

- 政府和公共部門

- 醫療保健和生命科學

- 零售與消費品包裝 (CPG)

- 製造業

- 資訊科技和電信

- 其他(教育機構、非營利組織)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- Strategic Developments

- Vendor Positioning Analysis

- 公司簡介

- Adobe Inc.

- OpenText Corp.

- Bynder BV

- Aprimo LLC

- Oracle Corp.

- Cloudinary Ltd.

- IBM Corp.

- Canto Inc.

- Widen Enterprises(Acquia)

- CELUM GmbH

- MediaBeacon Inc.

- Nuxeo(Hyland)

- Extensis

- Digizuite A/S

- MediaValet Inc.

- Brandfolder(Smartsheet)

- Sitecore

- Northplains Systems

- Tenovos

- Amplifi.io

第7章 市場機會與未來展望

The Digital Asset Management market was valued at USD 6.59 billion in 2025 and estimated to grow from USD 7.51 billion in 2026 to reach USD 14.41 billion by 2031, at a CAGR of 13.94% during the forecast period (2026-2031).

Demand is accelerating as enterprises reposition DAM from a cost center to a core pillar of omnichannel content strategy. Solution providers now embed AI for auto-tagging, rights management, and dynamic delivery, helping brands reduce asset search time by up to 40%. Generative AI pilots are already underway at 66% of large organizations, boosting personalization at scale. Regulatory change is another growth catalyst. Europe's Accessibility Act, effective June 2025, requires richer metadata and alt-text, pushing companies to upgrade legacy systems. North America leads the adoption of cloud-native architectures, while the Asia-Pacific region is experiencing the fastest expansion, driven by the surge in mobile video streaming. At the same time, the high total cost of ownership and tightening data-sovereignty rules restrain smaller firms and heavily regulated sectors.

Global Digital Asset Management Market Trends and Insights

Growing Volume and Velocity of Rich Media Assets in Omnichannel Commerce

Marketing teams now devote 39% of budgets to content creation, much of it short-form video and interactive formats that require sophisticated metadata, rights tracking, and rendition management. Organizations that integrate Product Information Management with DAM repurpose assets across storefronts, social commerce, and marketplaces, maximizing ROI while protecting brand integrity. Coca-Cola links SKU-level data with creative files to drive real-time personalization across e-commerce sites. Companies without a robust DAM struggle with duplicate production and inconsistent messaging, eroding campaign effectiveness.

Rapid Shift to Cloud-Native AI-Enhanced DAM Platforms in North America

Enterprises such as T-Mobile decreased creative cycle times after moving from on-premise repositories to Adobe Experience Manager Assets, which uses AI for bulk tagging and rendition generation. SaaS delivery eliminates costly upgrades and supports distributed teams that need instant access. Early adopters report measurable OPEX savings and faster campaign launches, prompting competitors to accelerate migrations.

High Total Cost of Ownership for Enterprise-Grade DAM Suites in SMEs

Licensing fees, integration work, and the need for DAM specialists deter many smaller firms from enterprise platforms. Departments often adopt lightweight tools, creating silos that inflate support overhead and complicate consolidation efforts. Service providers now bundle change-management workshops and migration accelerators to close this adoption gap.

Other drivers and restraints analyzed in the detailed report include:

- Surging Demand for Personalised Video Streaming Assets in Asia

- Integration of DAM with Headless CMS for Real-Time Content Syndication

- Data-Sovereignty and Residency Mandates Limiting Cross-Border Asset Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Solutions segment captured a 71.90% share, establishing a baseline for enterprise adoption. Platforms now bundle AI transcription, color correction, and rights clearance, making the Digital Asset Management market an integral part of broader digital-experience stacks. Large brands utilize orchestration rules to automatically assemble campaign kits, ensuring the creation of regulatory-ready content sets.

Meanwhile, Services revenue is forecast to outpace software at a 17.35% CAGR as firms rely on partners for taxonomy design, migration from fragmented archives, and user-training programs. Managed-service engagements that wrap governance dashboards and KPI tracking are becoming standard. Implementations supported by specialists demonstrate a 196% ROI through faster retrieval and compliance savings.

Cloud installations account for 63.40% of 2025 revenue, as updates flow seamlessly and the total cost per asset decreases as storage tiers are automatically scaled. Clients integrate AI Video Intelligence entirely through SaaS APIs, expanding their digital presence across new channels without downtime.

On-premise installations persist in defense, government, and healthcare, but hybrid patterns are gaining traction, where sensitive master files remain behind the firewall while derivatives are streamed from regional clouds. Continuous delivery of features such as semantic search keeps the cloud model ahead, fueling a 15.53% CAGR and reinforcing the primacy of the Digital Asset Management market in modern tech stacks.

The Digital Asset Management Market is Segmented by Component (Solutions, and Services), Deployment (On-Premise, and Cloud), Organization Size (SMEs, and Large Enterprises), Application (Sales and Marketing Enablement, Broadcast and Publishing Workflows, and More), End-User (Media and Entertainment, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with a 37.70% share in 2025, as enterprises adopted AI-rich cloud suites and hyperscale providers enhanced their compliance certifications. DeFi Technologies projected USD 201.07 million in revenue from Solana-based products, illustrating deep regional expertise in tokenized asset management, and the region's mature ad-tech ecosystem drives higher per-user content spend, solidifying its leadership in the Digital Asset Management market. The region's mature ad-tech ecosystem drives higher per-user content spend, solidifying its leadership in the Digital Asset Management market.

Asia-Pacific is forecast to post a 17.02% CAGR through 2031. The DAM Sydney 2025 conference highlighted the growing demand for multilingual asset orchestration across FMCG, healthcare, and government programs. Rising smartphone penetration and social commerce are expanding the use cases for instant video personalization at scale. Government smart-city initiatives also encourage the development of unified content hubs to power public-service apps.

Europe's growth is anchored in accessibility mandates and strict privacy frameworks. The Digital Asset Management market size for compliance-ready solutions is expanding as firms retrofit their heritage collections with alt-text and granular consent tracking. Vendors differentiate on advanced metadata, versioning, and anonymization features to satisfy GDPR and regional localization laws. Osborne Clarke advises that early conformance with the European Accessibility Act enhances brand reputation and mitigates legal risk

- Adobe Inc.

- OpenText Corp.

- Bynder BV

- Aprimo LLC

- Oracle Corp.

- Cloudinary Ltd.

- IBM Corp.

- Canto Inc.

- Widen Enterprises (Acquia)

- CELUM GmbH

- MediaBeacon Inc.

- Nuxeo (Hyland)

- Extensis

- Digizuite A/S

- MediaValet Inc.

- Brandfolder (Smartsheet)

- Sitecore

- Northplains Systems

- Tenovos

- Amplifi.io

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Volume and Velocity of Rich Media Assets in Omnichannel Commerce

- 4.2.2 Rapid Shift to Cloud-Native AI-Enhanced DAM Platforms in North America

- 4.2.3 Surging Demand for Personalised Video Streaming Assets in Asia

- 4.2.4 Integration of DAM with Headless CMS for Real-Time Content Syndication

- 4.2.5 Regulatory Push for Accessibility (WCAG-2.2) Elevating Metadata Standards in Europe

- 4.2.6 Emergence of Generative-AI-Powered Auto-Tagging Reducing TTM for Brand Launches

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Enterprise-Grade DAM Suites in SMEs

- 4.3.2 Data-Sovereignty and Residency Mandates Limiting Cross-Border Asset Storage

- 4.3.3 Fragmented Legacy Repositories Hindering Seamless Migration

- 4.3.4 Limited Skilled Workforce for AI-based Metadata Governance

- 4.4 Technological Outlook

- 4.5 Macroeconomic Factors Impact Assessment

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis (Funding, M&A, VC Activity)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud (SaaS)

- 5.3 By Organisation Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By Application

- 5.4.1 Sales and Marketing Enablement

- 5.4.2 Broadcast and Publishing Workflows

- 5.4.3 Product and E-commerce Management

- 5.4.4 Photography, Graphics and Design Repositories

- 5.4.5 Document and Knowledge Management

- 5.5 By End-User Industry

- 5.5.1 Media and Entertainment

- 5.5.2 BFSI

- 5.5.3 Government and Public Sector

- 5.5.4 Healthcareand Life Sciences

- 5.5.5 Retail and CPG

- 5.5.6 Manufacturing

- 5.5.7 IT and Telecom

- 5.5.8 Others (Education, Non-Profit)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Kenya

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Adobe Inc.

- 6.3.2 OpenText Corp.

- 6.3.3 Bynder BV

- 6.3.4 Aprimo LLC

- 6.3.5 Oracle Corp.

- 6.3.6 Cloudinary Ltd.

- 6.3.7 IBM Corp.

- 6.3.8 Canto Inc.

- 6.3.9 Widen Enterprises (Acquia)

- 6.3.10 CELUM GmbH

- 6.3.11 MediaBeacon Inc.

- 6.3.12 Nuxeo (Hyland)

- 6.3.13 Extensis

- 6.3.14 Digizuite A/S

- 6.3.15 MediaValet Inc.

- 6.3.16 Brandfolder (Smartsheet)

- 6.3.17 Sitecore

- 6.3.18 Northplains Systems

- 6.3.19 Tenovos

- 6.3.20 Amplifi.io

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球數位資產管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球數位資產管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球影像管理市場報告

2026年全球影像管理市場報告 數位資產管理市場:按組件類型、部署模式、組織規模、應用和產業分類-2026-2032年全球市場預測

數位資產管理市場:按組件類型、部署模式、組織規模、應用和產業分類-2026-2032年全球市場預測 數位資產管理市場規模、佔有率、趨勢和預測:按類型、組件、應用、部署模式、企業規模、最終用戶行業和地區分類,2026-2034 年

數位資產管理市場規模、佔有率、趨勢和預測:按類型、組件、應用、部署模式、企業規模、最終用戶行業和地區分類,2026-2034 年 全球數位資產管理市場(至2031年):依產品(解決方案與服務)、應用(品牌與行銷資產管理、媒體製作與廣播資產管理)、資產類型、組織規模、產業及地區分類2026年全球數位密鑰雲認證管理員市場報告2026年全球數位資產管理市場報告2026年全球數位資產管理(DAM)軟體市場報告

全球數位資產管理市場(至2031年):依產品(解決方案與服務)、應用(品牌與行銷資產管理、媒體製作與廣播資產管理)、資產類型、組織規模、產業及地區分類2026年全球數位密鑰雲認證管理員市場報告2026年全球數位資產管理市場報告2026年全球數位資產管理(DAM)軟體市場報告 數位資產管理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類

數位資產管理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類 數位鑰匙及安全車輛存取系統市場規模、佔有率及預測(依技術、安全協定、智慧型手機整合及OEM廠商採用劃分)-全球預測至2036年

數位鑰匙及安全車輛存取系統市場規模、佔有率及預測(依技術、安全協定、智慧型手機整合及OEM廠商採用劃分)-全球預測至2036年