|

市場調查報告書

商品編碼

1911819

印度防水解決方案市場:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)India Waterproofing Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

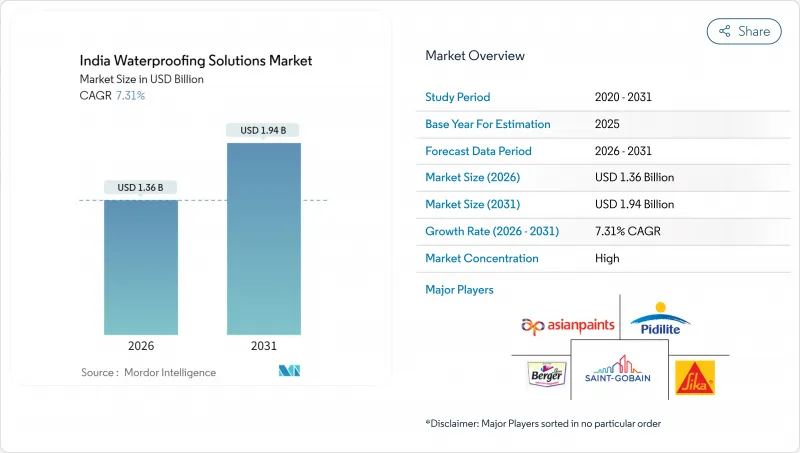

印度防水解決方案市場預計將從 2025 年的 12.7 億美元成長到 2026 年的 13.6 億美元,預計到 2031 年將達到 19.4 億美元,2026 年至 2031 年的複合年成長率為 7.31%。

國家基礎設施計畫下的強勁公共支出、日益嚴格的建築規範(尤其注重氣候適應性)以及客戶對預防性維護的明顯重視,共同支撐了印度防水解決方案市場在原料成本波動的情況下保持穩定成長。防水卷材仍然是領先技術,它不僅在惡劣的季風條件下擁有卓越的性能,還能提供開發商和富裕住宅所追求的長期質保。住宅推動了優質化,而商業、工業和基礎設施計劃則為隔熱反射混合防水卷材等先進系統帶來了規模化應用。隨著多元化塗料巨頭和特種化學品供應商競相加大研發投入、擴大安裝網路並遵守修訂後的印度標準局 (BIS) 防水規範,市場競爭日益激烈。

印度防水解決方案市場趨勢與洞察

快速都市化與經濟適用住宅政策

印度的城市人口每年成長超過1000萬,僅總理住房計劃(PMAY)一項就計劃在2025年提供2000萬套新的經濟適用住宅。由於維修可能高達新建成本的五倍,開發商擴大在設計階段就指定採用預防性防水措施。 2024-2025財政年度累計1,440億美元用於氣候適應型基礎建設,並將資金與符合印度標準局(BIS)標準的防水材料直接掛鉤。 100個城市的智慧城市計畫正在推動地鐵站、多層停車場和綜合用途塔樓等地下結構防水膜的需求。在人口密集的城市中心進行垂直建設時,冷浸式防水膜更受歡迎,因為它可以無縫適應複雜的幾何形狀,並降低因不均勻沉降造成的損壞風險。

採用具有熱反射性能的混合型液態防水薄膜

這種兼具防水和近紅外線反射特性的混合型液體防水膜,在夏季高峰期可將屋頂溫度降低高達15°C。這不僅能減少空調能耗,還有助於獲得印度綠色建築委員會 (IGBC) 和 LEED(環境設計美國)認證積分。亞洲塗料和西卡公司正在加強聚合物研發力度,以解決印度紫外線強度高的氣候條件下該材料的耐久性和色牢度問題。早期應用案例包括資料中心和製造工廠,在這些場所,大面積面積的節能效益可以迅速累積。這項技術也開始應用於高層住宅計劃,對於中高階買家的開發商而言,降低屋頂熱量吸收是一項重要的市場賣點。透過在地化原料採購和提高產量來降低產品成本,是實現長期應用的關鍵。

建築公司分散化導致施工品質下降

在全國範圍內,約80%的防水系統由缺乏正規訓練的小規模承包商安裝,導致安裝品質參差不齊,並容易過早失效。儘管都市區開發商越來越傾向於強制使用OEM認證的安裝人員,但打入印度龐大的建築市場仍然是一項挑戰。雖然製造商資助區域培訓中心,但由於工人經常在短期計劃之間流動,技術純熟勞工的留存率仍然很低。短期來看,糟糕的安裝正在削弱終端用戶的信心,並阻礙向需要精準安裝的高階防水捲材的過渡。

細分市場分析

至2025年,防水卷材將佔據印度防水解決方案市場65.62%的佔有率,並在2031年之前保持7.46%的複合年成長率,鞏固其在嚴苛應用領域作為性能標竿的地位。冷粘捲材因其能在複雜的屋頂幾何形狀上形成無縫屏障且無需火炬固化,從而提高施工現場的安全性,而備受住宅建築商的青睞。全黏結捲材系統廣泛應用於大型商業屋頂和裙樓板,在這些專案中,長達20年的現場性能至關重要。熱粘卷材主要面向化工廠和煉油廠,而預製卷材則透過預製化工藝,為快速基礎設施計劃提供支援。

先進的彈性體化學技術使膜材能夠跨越寬達2毫米的裂縫,這在高層建築中尤其重要,因為高層建築的位移現象十分普遍。高階住宅市場的保固期已延長至12年,數位化檢測工具使製造商能夠在保固期內進行安裝審核。雖然化學產品在局部修補和特殊基材方面仍然很重要,但隨著規模的擴大,平方公尺成本降低,膜材市場持續成長。主要供應商對原料的策略性後向整合進一步保護了膜材價格免受油價波動的影響。

《印度防水解決方案報告》按子產品(化學品和防水布)和最終用途(商業、工業和公共、基礎設施和住宅)進行細分。市場預測以以金額為準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速的都市化與經濟適用住宅政策的推廣

- 採用具有增強的熱反射率的混合液體膜

- 季風強度加大,需制定氣候智慧型建築規範。

- 住宅偏好高階產品並要求10年保固

- 向低VOC奈米滲透技術過渡

- 市場限制

- 施工缺陷是由於施工承包商基地分散造成的。

- 與原油價格相關的原料價格波動將影響聚氨酯(PU)和瀝青。

- 都市區地區對預防性防水的認知有限

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按子產品

- 化學品

- 環氧樹脂基

- 聚氨酯基

- 水溶液

- 其他技術

- 防水膜

- 冷液應用

- 全黏性片材

- 熱液應用

- 鬆散鋪放的床單

- 化學品

- 按最終用途面積

- 商業的

- 工業和公共設施

- 基礎設施

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Ardex Group

- Asian Paints

- Berger Paints India Limited

- Bostik(Arkema)

- Choksey FixGuruu

- CICO Group

- Kryton International Inc.

- MAPEI SpA

- MC-Bauchemie

- Pidilite Industries Ltd.

- Saint-Gobain

- Sika AG

- Soprema Group

- STP Limited, India

- Ultratech Cement Ltd.

- Xypex Chemical Corporation

第7章 市場機會與未來展望

The India Waterproofing Solutions Market is expected to grow from USD 1.27 billion in 2025 to USD 1.36 billion in 2026 and is forecast to reach USD 1.94 billion by 2031 at 7.31% CAGR over 2026-2031.

Robust public spending under the National Infrastructure Pipeline, stricter building codes focused on climate resilience, and a clear customer pivot toward preventive maintenance keep the India Waterproofing Solutions market on a stable growth path despite raw-material cost swings. Membranes remain the favored technology because they combine proven performance in aggressive monsoon conditions with the extended warranties demanded by developers and affluent homeowners. Residential construction drives premiumization, while commercial, industrial, and infrastructure projects create scale for advanced systems such as heat-reflective hybrid membranes. Competitive intensity is high as diversified paint majors and specialized chemical suppliers race to improve reseaarch and development, strengthen applicator networks, and comply with the Bureau of Indian Standards' upgraded waterproofing specifications.

India Waterproofing Solutions Market Trends and Insights

Rapid Urbanization and Affordable-Housing Stimulus

India adds more than 10 million urban residents each year, and the Pradhan Mantri Awas Yojana alone targets 20 million new affordable units by 2025. Developers increasingly specify preventive waterproofing at the design stage because retrofits cost up to five times more than original installation. Budget 2024-25 earmarked USD 144 billion for climate-resilient infrastructure, a move that directly links funding to BIS-compliant waterproofing. Smart-City projects in 100 municipalities have elevated demand for membranes that perform in underground metro stations, multilevel parking structures, and mixed-use towers. Vertical construction in dense urban cores favors cold liquid applied membranes, which adapt to complex geometries without joints that could fail under differential settlement.

Adoption of Hybrid Liquid Membranes with Heat-Reflectivity

Hybrid liquid membranes that combine waterproofing with near-infrared reflectance reduce rooftop temperatures by as much as 15 °C during peak summer, lowering HVAC energy loads and helping buildings qualify for IGBC and LEED points. Asian Paints and Sika AG have scaled polymer research and development to address durability and color-fastness concerns in India's ultraviolet-intense climate. Early adopters include data centers and manufacturing plants where energy savings compound quickly across large roof areas. The technology has begun penetrating residential high-rise projects, where reduced heat gain adds marketing value for developers targeting mid-premium buyers. Over the long term, broader rollout depends on lowering product cost through local raw-material sourcing and higher manufacturing volumes.

Fragmented Applicator Base Driving Workmanship Failures

Small contractors with limited formal training install about 80% of waterproofing systems nationwide, leading to inconsistent workmanship and premature failures.Urban developers increasingly mandate OEM-certified applicators, yet reaching India's sprawling construction market remains challenging. Manufacturers fund regional training centers, but retention of skilled labor is low because workers migrate between short-term projects. In the immediate term, workmanship failures erode end-user confidence and slow the shift toward premium membranes that require meticulous installation.

Other drivers and restraints analyzed in the detailed report include:

- Intensifying Monsoons Prompting Climate-Resilient Codes

- Shift Toward Low-VOC Nano-Penetrating Technologies

- Limited Tier-3/Rural Awareness for Preventive Waterproofing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Membranes represented 65.62% of the India Waterproofing Solutions market share in 2025 and will maintain a 7.46% CAGR to 2031, reinforcing their status as the functional benchmark for demanding applications. Cold liquid applied membranes attract residential builders because they form seamless barriers over complex roof lines and cure without torches, enhancing job-site safety. Fully adhered sheet systems dominate large-format commercial roofs and podium slabs where proven 20-year field performance matters. Hot liquid variants address chemical plants and refineries, while loose-laid sheets support fast-track infrastructure projects by enabling pre-fabricated installation sequences.

Advanced elastomeric chemistry helps membranes bridge cracks up to 2 mm, a critical advantage in high-rise structures subject to differential movement. Warranties now extend to 12 years in premium residential segments, and digital inspection tools allow manufacturers to audit installations before issuing coverage. While chemicals retain relevance for localized repairs and niche substrates, the India Waterproofing Solutions market size for membranes keeps increasing as cost per square meter falls with scale. Strategic raw-material backward integration by major suppliers further cushions membrane pricing against crude-driven volatility.

The India Waterproofing Solutions Report is Segmented by Sub Product (Chemicals and Membranes), and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ardex Group

- Asian Paints

- Berger Paints India Limited

- Bostik (Arkema)

- Choksey FixGuruu

- CICO Group

- Kryton International Inc.

- MAPEI S.p.A.

- MC-Bauchemie

- Pidilite Industries Ltd.

- Saint-Gobain

- Sika AG

- Soprema Group

- STP Limited, India

- Ultratech Cement Ltd.

- Xypex Chemical Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanization and affordable-housing stimulus

- 4.2.2 Adoption of hybrid liquid membranes that add heat-reflectivity

- 4.2.3 Intensifying monsoons prompting climate-resilient codes

- 4.2.4 Home-owner premiumization and 10-year warranty demand

- 4.2.5 Shift toward low-VOC nano-penetrating technologies

- 4.3 Market Restraints

- 4.3.1 Fragmented applicator base driving workmanship failures

- 4.3.2 Crude-linked raw-material volatility hitting PU and bitumen

- 4.3.3 Limited tier-3 / rural awareness for preventive waterproofing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Sub Product

- 5.1.1 Chemicals

- 5.1.1.1 Epoxy-based

- 5.1.1.2 Polyurethane-based

- 5.1.1.3 Water-based

- 5.1.1.4 Other Technologies

- 5.1.2 Membranes

- 5.1.2.1 Cold Liquid Applied

- 5.1.2.2 Fully Adhered Sheet

- 5.1.2.3 Hot Liquid Applied

- 5.1.2.4 Loose-Laid Sheet

- 5.1.1 Chemicals

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ardex Group

- 6.4.2 Asian Paints

- 6.4.3 Berger Paints India Limited

- 6.4.4 Bostik (Arkema)

- 6.4.5 Choksey FixGuruu

- 6.4.6 CICO Group

- 6.4.7 Kryton International Inc.

- 6.4.8 MAPEI S.p.A.

- 6.4.9 MC-Bauchemie

- 6.4.10 Pidilite Industries Ltd.

- 6.4.11 Saint-Gobain

- 6.4.12 Sika AG

- 6.4.13 Soprema Group

- 6.4.14 STP Limited, India

- 6.4.15 Ultratech Cement Ltd.

- 6.4.16 Xypex Chemical Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球整合防水系統市場報告2026年全球瀝青防水材料市場報告2026年全球防水外加劑市場報告

2026年全球整合防水系統市場報告2026年全球瀝青防水材料市場報告2026年全球防水外加劑市場報告 防水系統市場:全球市場按產品類型、技術、應用、最終用戶和分銷管道分類的預測 - 2026-2032 年

防水系統市場:全球市場按產品類型、技術、應用、最終用戶和分銷管道分類的預測 - 2026-2032 年 東協防水市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東協防水市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球浴室防水解決方案市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球結晶質防水材料市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球防水系統市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球聚乙烯防潮層市場報告

全球浴室防水解決方案市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球結晶質防水材料市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球防水系統市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球聚乙烯防潮層市場報告 全球濕房防水解決方案市場-按類型、原料、地區和競爭格局分類的產業規模、佔有率、趨勢、機會和預測(2021-2031年)

全球濕房防水解決方案市場-按類型、原料、地區和競爭格局分類的產業規模、佔有率、趨勢、機會和預測(2021-2031年)