|

市場調查報告書

商品編碼

1911811

歐洲滾筒式乾衣機:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Europe Tumble Dryers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

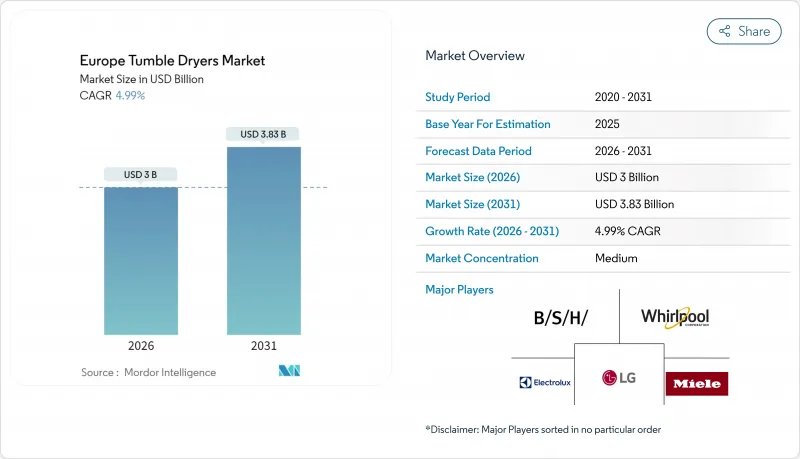

2025年歐洲滾筒式乾衣機市值28.6億美元,預計2031年將達到38.3億美元,高於2026年的30億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.99%。

從絕對值來看,歐洲滾筒式乾衣機市場正從成熟的、更換主導的家電品類向技術主導的升級週期轉型,這一轉型是由歐盟生態設計指令(該指令自2025年7月起禁止使用排氣式和入門級冷凝式乾衣機)引發的。熱泵技術的創新、不斷上漲的家庭能源成本以及後疫情時代對永續性的關注,共同支撐著在持續的宏觀經濟波動中保持強勁的需求勢頭。目前的競爭策略著重於合規性、高階定位和快速的產品線更新。區域差異顯而易見,德國在普及率方面保持領先,而西班牙的成長速度最快。儘管東歐和南歐部分地區對價格的敏感度抑制了熱泵的即時普及,但扶持性的融資方案和社會住宅的大量採購計畫正在擴大目標客戶群。同時,全通路分銷,尤其是透過線上市場,正在重塑客戶獲取的經濟模式,並使擁有直接面對消費者能力的品牌更具優勢。與 R290 冷媒相關的供應鏈摩擦和持續的消防安全監控凸顯了市場的營運風險,而物聯網賦能的模式和公共產業需量反應試點項目則表明,在預測期內,相鄰的收入來源將會成熟。

歐洲滾筒式乾衣機市場趨勢與洞察

歐盟節能法規加速了熱泵的普及

將於2025年7月生效的生態設計法規將強制製造商從其歐洲產品線中淘汰非熱泵技術,從而將歐洲滾筒式乾衣機市場轉變為單一技術競爭格局。僅此一項法規預計到2040年即可減少15兆瓦時(TWh)的電力消耗和二氧化碳當量(CO2-eq)排放,累積消費者節省28億美元。目前,A級能效等級僅授予熱泵機型,這意味著排氣式或基本冷凝式乾衣機實際上不符合標準。像Miele這樣的高階品牌迅速做出反應,推出了配備InfinityCare滾筒和專用羊毛洗滌程序的T2 Nova Edition,強調其在節能之外的纖維保護優勢。 BSH則利用過渡期調整了生產方向,轉向熱泵技術,在維持合規性的同時維持了利潤率。該法規還引入了雙層定價結構,使高階製造商能夠在保持產品價值的同時,對低成本廠商施加壓力。基於 ISO 14001永續性認證的符合性審核正逐漸成為採購的先決條件,這進一步增加了那些行動遲緩的公司所面臨的競爭障礙。

西歐可支配所得成長與更換週期加快

宏觀環境的改善和通膨的溫和正在提振消費者的自由裁量權支配支出。歐盟耐久財銷售額預計將從2023年的2.90%下降反彈至2025年的2.80%成長。平均更換週期為8-10年,不斷上漲的電費促使家庭優先考慮生命週期成本而非購買價格。這推動了消費者對熱泵解決方案的偏好,儘管其初始成本高出兩到三倍。雖然現金回饋計劃正在推動德國和荷蘭的普及,但南歐市場的價格敏感度仍然很高。預計到2027年,歐洲家用電器市場將從384.8億美元成長至424億美元,其中智慧家電預計將成長26%,因為消費者追求能源效率和便利性。調查數據顯示,80%的英國受訪者擔心能源帳單,促使他們願意投資購買高效能烘乾機。知名品牌正在利用其忠誠度優勢,35%的全球消費者表示品牌聲譽是決定性因素。總體而言,收入的成長加上更換的緊迫性,推動歐洲滾筒式乾衣機市場以 1.2 個百分點的複合年成長率成長。

熱泵機型初始價格溢價較高

熱泵式乾衣機的零售價通常超過1,000歐元(1,090美元),而排氣式乾衣機的價格僅為300-400歐元(327-436美元),這構成了較高的市場准入門檻。雖然終身節能效益可超過500美元,但較長的投資回收期阻礙了東歐低收入家庭的普及。儘管融資和政府補貼可以部分抵銷成本,但只有規模經濟效應降低單位成本後,熱泵式乾衣機的普及率才會提高。三星和LG正在試行推出入門級機型,這些機型具備人工智慧最佳化功能,售價低於800歐元(872美元),有望改變市場格局。歐洲現有製造商必須在保護利潤率和以犧牲平均售價(ASP)為代價加速轉型之間做出選擇,無論哪種方式都會影響品牌價值和現有用戶群的經濟效益。短期來看,價格障礙將使歐洲乾衣機市場的複合年成長率(CAGR)下降約1.4個百分點。

細分市場分析

到2025年,熱泵式乾衣機將佔據歐洲乾衣機市場35.44%的佔有率,年複合成長率(CAGR)為13.10%,這主要得益於2025年中期即將實施的排氣式和基本冷凝式乾衣機禁令。冷凝式乾衣機曾是主流產品,到2025年仍將佔據歐洲市場佔有率的50.92%,但隨著市場需求轉向符合新規的替代品,其市場地位正逐漸被淘汰。高階產品定位仰賴降低70%的消費量和更卓越的衣物保護,這使得製造商即使在入門級產品出現的情況下也能維持價格優勢。三星的「Bespoke AI Laundry Combo」融合了大容量設計和基於機器學習的循環最佳化技術。 LG則以其全熱泵「Signature」系列產品與之抗衡,該產品將能耗降低至570瓦,展現了不同的技術概念。在預測期內,產品差異化將越來越依賴連接性、環保認證和售後服務,而不僅僅是機械性能。

歐洲滾筒式乾衣機市場也正經歷排氣式乾衣機逐漸微的趨勢。這種乾衣機在英國曾因其便於獨立住宅外排而廣受歡迎。然而,屋主的房屋維修和建築法規的變更正推動著乾衣機安裝轉向閉式冷凝器或熱泵式乾衣機。製造商們正在積極應對,例如博世家電(BSH)已將生產線重新分配至利潤更高的熱泵系列產品。零件供應商也透過逐步淘汰電阻加熱器並擴大R290壓縮機的生產來應對這一變化。大量不合規庫存迫使零售商透過降價清倉,暫時扭曲了平均售價。然而,從2025年起,隨著歐洲乾衣機市場全面轉向熱泵機型,並透過配套服務合約來保障利潤,預計該品類的獲利能力將出現復甦。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟能源效率法規加速了熱泵的普及應用。

- 西歐可支配所得成長與更換週期加快

- MDA採購中電子商務管道的成長

- 社會住宅維修計畫指定使用熱泵烘乾機

- 飯店業的ESG目標推動設施升級,以提高效率。

- 物聯網賦能的烘乾機用於公用事業需量反應試點項目

- 市場限制

- 熱泵機型的初始成本較高

- 歐盟五大主要國家住宅市場飽和

- 消防安全召回事件損害消費者信心

- R290冷媒供應鏈的變異性

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭強度

第5章 市場規模與成長預測

- 依產品類型

- 熱泵式滾筒烘乾機

- 冷凝式滾筒乾衣機

- 滾筒式烘乾機排氣

- 最終用戶

- 住宅

- 商業

- 透過分銷管道

- 離線

- 線上

- 按國家/地區

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 比利時

- 荷蘭

- 盧森堡

- 北歐國家

- 丹麥

- 芬蘭

- 冰島

- 挪威

- 瑞典

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BSH Hausgerate GmbH(Bosch/Siemens)

- Whirlpool Corp.

- Electrolux AB

- Miele & Cie. KG

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Candy Hoover Group(Haier Europe)

- Gorenje(Hisense Europe)

- Indesit

- Beko

- Hotpoint

- AEG

- Zanussi

- Teka Group

- Blomberg

- Asko Appliances

- Smeg SpA

- Vestel

- Sharp Corp.

- Grundig

第7章 市場機會與未來展望

The European tumble dryer market was valued at USD 2.86 billion in 2025 and estimated to grow from USD 3.00 billion in 2026 to reach USD 3.83 billion by 2031, at a CAGR of 4.99% during the forecast period (2026-2031).

In absolute terms, the European tumble dryer market is evolving from a mature replacement-driven appliance category to a technology-led upgrade cycle triggered by the European Union's ecodesign mandate that bans vented and entry-level condenser units from July 2025. . Heat-pump innovation, the rising cost of household energy, and a post-pandemic focus on sustainability jointly underpin healthy demand momentum despite lingering macro volatility. Competitive strategies now hinge on regulatory compliance, premium positioning, and rapid portfolio renewal, while regional disparities remain pronounced as Germany maintains a lead in unit penetration but Spain posts the fastest incremental growth. Price sensitivity in Eastern and parts of Southern Europe tempers immediate heat-pump uptake, yet supportive financing schemes and bulk-procurement programs in social housing are widening the addressable base. Simultaneously, omnichannel distribution, especially via online marketplaces, is remolding customer acquisition economics and favoring brands with direct-to-consumer capabilities. Supply chain friction linked to R290 refrigerant and continued fire-safety scrutiny highlight the market's operational risks, but IoT-ready models and utility demand-response pilots represent adjacent revenue pools that will mature during the outlook period.

Europe Tumble Dryers Market Trends and Insights

EU Energy-Efficiency Mandates Accelerating Heat-Pump Adoption

The July 2025 ecodesign regulation compels manufacturers to eliminate non-heat-pump technology from their European portfolios, instantly transforming the Europe tumble dryer market into a single-technology contest. This rule alone is expected to save 15 TWh of electricity and 1.7 Mt CO2-equivalent by 2040, generating USD 2.8 billion in cumulative consumer savings. A-class ratings now appear exclusively on heat-pump models, effectively relegating vented or basic condenser dryers to non-compliant status. Premium brands such as Miele responded early, unveiling the T2 Nova Edition with InfinityCare drums and wool-specific cycles that showcase fabric-care benefits beyond raw energy efficiency. BSH capitalized on the transition by re-balancing production toward heat-pump units, thereby sustaining profit margins while meeting compliance. The regulation simultaneously introduces a two-tier pricing environment in which premium manufacturers can defend value, whereas value-oriented firms face intense margin pressure. Compliance audits based on ISO 14001 sustainability credentials are becoming procurement prerequisites, further raising competitive barriers for late adopters.

Rising Disposable Income & Replacement Cycles in Western Europe

Improved macro conditions and subdued inflation are rekindling discretionary spending, with EU consumer-durables sales swinging from a 2.90% decline in 2023 to a 2.80% upswing in 2025. Replacement cycles average 8-10 years, and rising electricity tariffs push households to prioritize life-cycle cost over sticker price, favoring heat-pump solutions despite a 2-3X upfront premium. Germany and the Netherlands reinforce adoption via cash-back schemes, while southern markets remain more price sensitive. The European household appliance market is projected to grow from USD 38.48 billion to USD 42.40 billion by 2027, with smart appliances experiencing 26% growth as consumers demand energy efficiency and convenience features. Survey data reveal 80% of UK respondents worried about utility bills, translating into a higher willingness to invest in efficient dryers. Established brands exploit loyalty advantages, as 35% of global consumers list brand reputation as a decisive factor. Altogether, income growth plus replacement urgency contribute a 1.2-percentage-point tailwind to the Europe tumble dryer market CAGR.

High Upfront Price Premium of Heat-Pump Models

Heat-pump dryers often retail for EUR 1,000 (USD 1,090) or more versus EUR 300-400 (USD 327-436) for vented alternatives, creating a steep affordability hurdle. Although lifetime energy savings can exceed USD 500, the payback horizon discourages adoption among lower-income households in Eastern Europe. Financing schemes and government rebates partially bridge the gap, but penetration lags until economies of scale lower unit costs. Samsung and LG are testing entry-level heat-pump SKUs with AI-driven optimization at sub-EUR 800 (USD 872) price points, potentially resetting market expectations. European incumbents must choose between defending margin or sacrificing ASP to accelerate conversion, with each approach influencing brand equity and installed-base economics. In the near term, price barriers shave roughly 1.4 percentage points off the CAGR of the Europe tumble dryer market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-Commerce Channels for MDA Purchases

- Social-Housing Retrofit Programs Specifying Heat-Pump Dryers

- Market Saturation in Core EU-5 Residential Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heat-pump models entered 2025 with a 35.44% contribution to the Europe tumble dryer market size and are advancing at a 13.10% CAGR, bolstered by the regulatory ban on vented and basic condenser units effective mid-2025. Condenser dryers, once dominant, still held 50.92% of Europe tumble dryer market share in 2025, yet they face an unavoidable sunset, funneling demand into compliant alternatives. Premium positioning hinges on 70% lower energy consumption and fabric-care advantages, allowing manufacturers to defend pricing even as entry-level SKUs emerge. Samsung's Bespoke AI Laundry Combo illustrates the convergence of large-capacity engineering and machine-learning-based cycle optimization. LG counters with a fully heat-pump Signature stack that reduces power draw to 570 W, demonstrating differing technological bets. Over the forecast horizon, product differentiation will increasingly rely on connectivity, environmental certifications, and after-sales services rather than core mechanical performance alone.

The Europe tumble dryer market also witnesses a gradual fadeout of vented designs, historically popular in the UK due to easy exterior venting in single-family homes. Landlord refurbishments and changing building codes shift those installations toward closed-cycle condensers or heat-pump units. Manufacturers retool factories accordingly, with BSH reallocating production lines to higher-margin heat-pump families. Component suppliers adapt by phasing out resistive heaters and scaling up R290 compressor output. The impending cliff on non-compliant stock encourages retailers to clear inventories through discounting, temporarily distorting average selling prices. Yet post-2025, category revenues rebound as the Europe tumble dryer market pivots to all-heat-pump portfolios linked with bundled service contracts that protect margins.

The Europe Tumble Dryer Market Report is Segmented by Product Type (Heat Pump Tumble Dryer, Condenser Tumble Dryer, Vented Tumble Dryer), End-User (Residential, Commercial), Distribution Channel (Offline, Online), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- BSH Hausgerate GmbH (Bosch/Siemens)

- Whirlpool Corp.

- Electrolux AB

- Miele & Cie. KG

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Candy Hoover Group (Haier Europe)

- Gorenje (Hisense Europe)

- Indesit

- Beko

- Hotpoint

- AEG

- Zanussi

- Teka Group

- Blomberg

- Asko Appliances

- Smeg S.p.A.

- Vestel

- Sharp Corp.

- Grundig

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU energy-efficiency mandates accelerating heat-pump adoption

- 4.2.2 Rising disposable income & replacement cycles in Western Europe

- 4.2.3 Growth of e-commerce channels for MDA purchases

- 4.2.4 Social-housing retrofit programs specifying heat-pump dryers

- 4.2.5 Hospitality ESG targets driving high-efficiency fleet upgrades

- 4.2.6 IoT-ready dryers for utility demand-response pilots

- 4.3 Market Restraints

- 4.3.1 High upfront price premium of heat-pump models

- 4.3.2 Market saturation in core EU-5 residential segment

- 4.3.3 Fire-safety recall incidents denting consumer trust

- 4.3.4 R290 refrigerant supply-chain volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Heat Pump Tumble Dryer

- 5.1.2 Condenser Tumble Dryer

- 5.1.3 Vented Tumble Dryer

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Distribution Channel

- 5.3.1 Offline

- 5.3.2 Online

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 BENELUX

- 5.4.6.1 Belgium

- 5.4.6.2 Netherlands

- 5.4.6.3 Luxembourg

- 5.4.7 NORDICS

- 5.4.7.1 Denmark

- 5.4.7.2 Finland

- 5.4.7.3 Iceland

- 5.4.7.4 Norway

- 5.4.7.5 Sweden

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BSH Hausgerate GmbH (Bosch/Siemens)

- 6.4.2 Whirlpool Corp.

- 6.4.3 Electrolux AB

- 6.4.4 Miele & Cie. KG

- 6.4.5 LG Electronics Inc.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 Candy Hoover Group (Haier Europe)

- 6.4.8 Gorenje (Hisense Europe)

- 6.4.9 Indesit

- 6.4.10 Beko

- 6.4.11 Hotpoint

- 6.4.12 AEG

- 6.4.13 Zanussi

- 6.4.14 Teka Group

- 6.4.15 Blomberg

- 6.4.16 Asko Appliances

- 6.4.17 Smeg S.p.A.

- 6.4.18 Vestel

- 6.4.19 Sharp Corp.

- 6.4.20 Grundig

7 Market Opportunities & Future Outlook

- 7.1 Demand-response-ready heat-pump dryers integrated into home-energy-management systems

- 7.2 Subscription-based "laundry-appliance-as-a-service" models for urban micro-apartments

2026-2034年全球滾筒式乾衣機市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球滾筒式乾衣機市場規模、佔有率、趨勢和成長分析報告 工業乾燥機市場規模、佔有率和趨勢分析報告:按技術、類型、應用、地區和細分市場分類(2026-2033 年)

工業乾燥機市場規模、佔有率和趨勢分析報告:按技術、類型、應用、地區和細分市場分類(2026-2033 年) 工業乾燥機市場:按產品類型、運行原理、最終用途行業和地區分類

工業乾燥機市場:按產品類型、運行原理、最終用途行業和地區分類 工業乾燥機市場:按產品類型、類別、應用和地區分類(2026-2034 年)

工業乾燥機市場:按產品類型、類別、應用和地區分類(2026-2034 年) 滾筒式乾衣機市場機會、成長要素、產業趨勢分析及2026-2035年預測。工業乾燥機市場機會、成長要素、產業趨勢分析及2026-2035年預測

滾筒式乾衣機市場機會、成長要素、產業趨勢分析及2026-2035年預測。工業乾燥機市場機會、成長要素、產業趨勢分析及2026-2035年預測 工業乾燥機市場:按類型、能源來源、材料、傳熱方式及最終用途產業分類-2026-2032年全球市場預測

工業乾燥機市場:按類型、能源來源、材料、傳熱方式及最終用途產業分類-2026-2032年全球市場預測 全球電動滾筒烘乾機市場

全球電動滾筒烘乾機市場 亞太地區滾筒烘乾機市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美滾筒烘乾機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

亞太地區滾筒烘乾機市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美滾筒烘乾機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)