|

市場調查報告書

商品編碼

1911493

射頻和微波二極體:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)RF And Microwave Diodes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

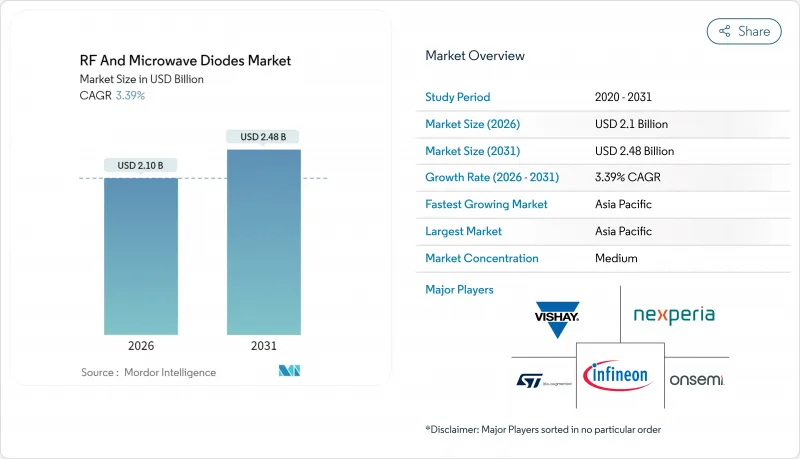

預計射頻和微波二極體市場將從 2025 年的 20.3 億美元成長到 2026 年的 21 億美元,到 2031 年將達到 24.8 億美元,2026 年至 2031 年的複合年成長率為 3.39%。

這一市場成長反映了由5G基地台部署、汽車雷達專案擴展以及低地球軌道衛星星系對航太組件日益成長的需求所推動的穩定勢頭。電信基礎設施升級持續推動大規模採購,而汽車產業正在加速二極體的消耗,以滿足關鍵的高階駕駛輔助系統(ADAS)的需求。氮化鎵材料的替代、日益嚴格的出口管制法規以及主要供應商積極的產能擴張正在塑造當前的競爭格局。

全球射頻及微波二極體市場趨勢及洞察

5G基礎設施的全球普及

大規模MIMO基地台、去程傳輸鏈路和行動電話射頻前端的整合正在推動二極體的需求成長。微波回程傳輸已經支援全球超過一半的行動通訊基地台連接,而5G流量的擴展將需要超過10 Gbps的吞吐量。基於GaN的二極體在N78和N77頻段可實現34%的功率附加效率,但其3.4 V的低供電電壓帶來了顯著的散熱限制。元件製造商正在透過低寄生封裝來應對這項挑戰,以在寬頻寬範圍內保持線性度。頻率調整至26-28 GHz將進一步增加對相位陣列模組所需的毫米波級二極體的需求。

對物聯網和智慧家居設備的需求不斷成長

預計到2025年,全球連網裝置數量將超過250億台,這將持續推動電池供電的穿戴式裝置、智慧電錶和邊緣感測器等應用對小訊號二極體的需求。設計人員需要超低漏電開關和封包追蹤電路來滿足嚴格的功耗預算目標。整合5G、LTE、Wi-Fi 7和低功耗藍牙多重通訊協定的設備正在推動整合二極體陣列的應用,以減少元件數量並縮小裝置尺寸。汽車無線電池管理系統是一個重要的應用案例,它可以透過低功耗藍牙鏈路和低損耗射頻路徑實現即時電壓監測。

原物料價格波動

北京當局對鎵和鍺的許可要求推高了現貨價格,導致氮化鎵外延片的成本上漲了三位數。美國95%的鎵都來自中國,這給高電子移動性電晶體(HEMT)片(許多微波二極體的基礎材料)的供應帶來了風險。製造商已採取措施應對,例如增加雙重採購、廢料回收和簽訂長期契約,但短期價格波動仍對毛利率構成壓力。

細分市場分析

到2025年,PIN二極體將佔據射頻和微波二極體市場28.75%的佔有率,這主要得益於其在射頻開關矩陣和可變衰減器中的應用。通訊設備製造商看重其強大的功率處理能力和寬動態範圍線性度,這對於基地台升級至關重要。國防雷達維修和衛星轉發器等長生命週期設計方案的成功應用也穩定了其量產需求。蕭特基二極體的射頻和微波二極體市場規模預計將以5.12%的複合年成長率成長,這反映了毫米波電路的發展趨勢,毫米波電路需要低正向電壓和快速恢復特性。新興的60-90 GHz汽車成像雷達和77 GHz短程模組不斷取代檢測器鏈中的PIN解決方案,進一步增強了蕭特基二極體的發展動能。

由於其超陡峭的結區輪廓能夠實現超過 8:1 的調諧比,設計人員仍然在 VCO 的頻率合成中使用變容二極體。耿氏二極體和隧道二極體雖然應用領域有限,但專用的高功率測量設備和超低相位雜訊振盪器支撐著其穩定的市場需求。齊納穩壓二極體在高功率 GaN MMIC 的偏壓網路中正逐漸佔據越來越重要的地位,尤其是在需要精確過壓保護的場合。

2025年,3-8 GHz頻段的營收將維持31.85%的成長,主要得益於雷達高度計、衛星下行鏈路和5 GHz Wi-Fi網路基地台。民用航空和海事雷達的龐大安裝基礎延長了產品壽命,並支撐了售後市場二極體的銷售。然而,隨著通訊業者將固定無線接入商業化,以及汽車製造商從傳統的24 GHz雷達向77 GHz雷達平台遷移,40 GHz以上的毫米波需求預計將以5.42%的複合年成長率成長。由於低地球軌道(LEO)饋線鏈路和機載衛星通訊系統的引入(這些系統需要窄波束天線),Ka/V頻段(20-40 GHz)對射頻和微波二極體市場規模的貢獻正在增加。 3 GHz以下的設備將繼續為物聯網模組提供大量產品,在這些應用中,成本比效能更為重要。 12-18 GHz Ku/K 波段二極體的需求將保持穩定,這得益於國防探求者的升級以及廣播衛星通訊地面終端的適度成長。

本《射頻與微波二極體市場報告》依產品類型(例如,PIN二極體、蕭特基二極體)、頻寬(例如,3 GHz以下、3-8 GHz C/ X波段)、材料技術(例如,矽、砷化鎵)、南美洲用戶產業(例如,汽車、家用電子電器)和地區(例如,北美地區、歐洲終端、亞太地區)和地區(例如,北美地區)、歐洲終端產業(例如,汽車、消費)和地區(例如,北美地區)、歐洲終端產業。市場預測以美元計價。

區域分析

預計到2025年,亞太地區將佔全球營收的44.25%,並在2031年之前維持4.51%的複合年成長率。這主要得益於中國2,950億美元的國內半導體產業振興舉措和日本3.9兆日圓(約260億美元)的重建計劃,後者正為下一代晶圓產能奠定基礎。政府激勵措施正在加速外延生長、晶圓層次電子構裝和射頻前端模組組裝等領域的產能擴張。台灣和韓國蓬勃發展的契約製造基地進一步鞏固了其規模優勢,使其在該地區的主導地位得以維持。

北美將受惠於總額達390億美元的《晶片技術創新法案》(CHIPS Act),該法案為新建專用於射頻功率裝置和類比裝置的200毫米/300毫米晶圓廠提供補貼。 MACOM在麻薩諸塞州和北卡羅來納州的無塵室擴建將增強美國國內氮化鎵(GaN-on-SiC)的供應基礎,並降低地緣政治帶來的供應風險。由於更嚴格的出口管制限制了高頻元件的轉讓,預計政府和國防需求將集中在美國供應商。加拿大和墨西哥擁有獨特的組裝和測試能力,並利用美墨加協定(USMCA)的原產地規則為汽車客戶提供服務。

由於汽車雷達強制要求和工業4.0工廠升級,歐洲的二極體消費量趨於穩定。德國一級汽車製造商正在高階和量產車型中採用77GHz雷達,推動了歐洲的需求。法國和英國正在支援航太和衛星項目,這些項目需要使用抗輻射二極體。同時,中東和非洲的業者正在服務不足的農村地區部署5G固定無線接入,但宏觀經濟逆風導致近期銷售成長有限。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G基礎設施在全球的普及

- 對物聯網和智慧家居設備的需求不斷成長

- 汽車雷達和ADAS技術的日益普及

- 低地球軌道衛星星系的成長

- 毫米波雷達在工業無人機和機器人的應用

- 向寬能能隙(GaN/SiC)二極體技術過渡

- 市場限制

- 原料價格波動(鎵、矽、碳化矽、磷化銦)

- 半導體產能限制與供應鏈風險

- 40 GHz 以上的溫度控管挑戰

- 高頻裝置出口管制條例

- 價值鏈分析

- 技術展望

- 監管環境

- 投資分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按類型

- PIN二極體

- 肖特基二極體

- 勢壘(調諧)二極體

- 耿氏二極體

- 隧道二極體

- 齊納二極體

- 其他二極體

- 按頻段

- 低於 3GHz

- 3-8 GHz(C/X波段)

- 8-20 GHz(Ku-/K-Band)

- 20-40 GHz(Ka-/V-Band)

- 40 GHz 以上(毫米波)

- 透過材料技術

- 矽(Si)

- 砷化鎵(GaAs)

- 氮化鎵(GaN)

- 碳化矽(SiC)

- 其他成分

- 按最終用戶行業分類

- 車

- 家用電子電器

- 電訊和網路

- 工業製造與自動化

- 醫療保健

- 航太/國防

- 能源與公共產業

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microchip Technology Inc.

- Infineon Technologies AG

- Diodes Incorporated

- MACOM Technology Solutions Holdings, Inc.

- Nexperia BV(Wingtech Technology Co., Ltd.)

- onsemi(Semiconductor Components Industries, LLC)

- ROHM Co., Ltd.

- Vishay Intertechnology, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Renesas Electronics Corporation

- STMicroelectronics NV

- PANJIT International Inc.

- Suzhou Good-Ark Electronics Co., Ltd.

- Skyworks Solutions, Inc.

- Qorvo, Inc.

- Broadcom Inc.(Avago Technologies)

- Excelitas Technologies Corp.

- SemiGen, Inc.

- Richardson Electronics, Ltd.

- Central Semiconductor Corp.

第7章 市場機會與未來展望

The RF and microwave diodes market is expected to grow from USD 2.03 billion in 2025 to USD 2.1 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 3.39% CAGR over 2026-2031.

This market size growth reflects steady momentum from 5G base-station roll-outs, expanding automotive radar programs, and heightened demand for space-qualified components in LEO satellite constellations. Telecommunications infrastructure upgrades continue to drive bulk procurement, while the automotive sector accelerates diode consumption for mandatory advanced driver-assistance systems. Material substitution toward gallium nitride, tighter export-control enforcement, and proactive capacity additions by leading suppliers shape competitive positioning in the current period.

Global RF And Microwave Diodes Market Trends and Insights

Proliferation of Global 5G Infrastructure

Massive MIMO base-stations, fronthaul links, and handset RF front-ends collectively lift diode demand. Microwave backhaul already supports more than half of worldwide cell-site connections and requires throughput upgrades above 10 Gbps as 5G traffic scales. GaN-based diodes deliver 34% power-added efficiency in N78 and N77 bands, yet thermal constraints intensify at reduced 3.4 V supply rails. Component makers are responding with low-parasitic packaging that maintains linearity across wide bandwidths. Spectrum re-farming toward 26-28 GHz further increases the volume of mmWave-class diodes needed in phased-array modules.

Rising IoT and Smart-Consumer Electronics Demand

Global connected-device counts are set to exceed 25 billion by 2025, feeding sustained orders for small-signal diodes in battery-powered wearables, smart meters, and edge sensors. Designers require ultra-low-leakage switches and envelope-tracking circuits to meet stringent power-budget targets. Multi-protocol devices combining 5G, LTE, Wi-Fi 7, and Bluetooth Low Energy have spurred the adoption of integrated diode arrays that consolidate bill-of-materials while shrinking form factors. Automotive wireless battery-management systems provide a visible use case where low-loss RF paths enable real-time voltage monitoring over BLE links.

Volatile Raw-Material Prices

Beijing's export-licensing requirements on gallium and germanium lifted spot prices, pushing GaN epi-wafer costs upward by triple digits. The United States sources 95% of gallium from China, creating procurement risk for high-electron-mobility transistor wafers that underpin many microwave diodes. Manufacturers react by dual-sourcing, recycling scrap, and increasing long-term contracts, yet near-term volatility still compresses gross margins.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Automotive Radar and ADAS Adoption

- Growth of LEO Satellite Constellations

- Semiconductor Capacity Constraints and Supply-Chain Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PIN variants accounted for 28.75% of the RF and microwave diodes market share in 2025, anchored by their role in RF switching matrices and variable attenuators. Telecommunications OEMs value their robust power-handling capability and wide dynamic-range linearity, attributes critical for base-station upgrades. Defense radar retrofits and satellite transponders also lock in long-lifecycle design wins that stabilize volume demand. The RF and microwave diodes market size for Schottky devices is projected to expand at 5.12% CAGR, reflecting mmWave circuit migration that favors their low forward voltage and fast recovery properties. Emerging 60-90 GHz automotive imaging radar and 77 GHz short-range modules continue to displace PIN solutions in detector chains, reinforcing Schottky-unit momentum.

Designers maintain varactor adoption for frequency synthesis in VCOs because hyperabrupt junction profiles afford tuning ratios exceeding 8:1. Gunn and tunnel diodes remain niche, yet specialized high-power instrumentation and very-low-phase-noise oscillators preserve consistent demand. Zener regulation diodes capture share in bias networks for high-power GaN MMICs, especially where precise over-voltage protection is mandatory.

The 3-8 GHz class retained 31.85% revenue in 2025, driven by radar altimeters, satellite downlinks, and 5 GHz Wi-Fi access points. Solid installed bases in civil aviation and maritime radar extend product lifetime and underpin after-market diode sales. However, above-40 GHz mmWave demand grows at a 5.42% CAGR as operators commercialize fixed-wireless access and automotive OEMs transition from traditional 24 GHz to 77 GHz radar platforms. The RF and microwave diodes market size contribution from the Ka/V-band (20-40 GHz) segment rises with LEO feeder-links and airborne satcom installations that require narrow beamwidth antennas. Up-to-3 GHz devices keep supplying high-volume IoT modules where cost outweighs performance. Ku/K-band diodes slated for 12-18 GHz remain steady, buoyed by defense seeker upgrades and moderate growth in broadcast satcom ground terminals.

The RF and Microwave Diodes Report is Segmented by Product Type (PIN Diodes, Schottky Diodes, and More), Frequency Band (Up To 3 GHz, 3-8 GHz C-/X-Band, and More), Material Technology (Silicon, Gallium Arsenide, and More), End-User Industry (Automotive, Consumer Electronics, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.25% of 2025 revenue and is projected to grow at 4.51% CAGR to 2031, supported by China's USD 295 billion domestic semiconductor initiative and Japan's JPY 3.9 trillion (USD 26 billion) revival program that anchors next-generation wafer capacity. Government incentives accelerate build-outs in epi-growth, wafer-level packaging, and RF front-end module assembly. The vibrant contract-manufacturing base in Taiwan and South Korea augments scale advantages that sustain regional leadership.

North America benefits from the USD 39 billion CHIPS Act, which subsidizes new 200 mm and 300 mm fabs dedicated to RF power and analog devices. Clean-room expansions by MACOM in Massachusetts and North Carolina will reinforce domestic GaN-on-SiC supply and mitigate geopolitical supply risk. Export-control tightening restricts high-frequency device transfers, channeling government and defense demand toward U.S. suppliers. Canada and Mexico contribute niche assembly and test capacity, leveraging USMCA rules of origin to serve automotive clients.

Europe enjoys steady diode consumption through automotive radar mandates and Industry 4.0 factory upgrades. Germany's tier-1 OEMs employ 77 GHz radar in premium and mass-market models, propelling continental demand. France and the United Kingdom support aerospace and satellite programs that specify radiation-hardened diodes. Meanwhile, Middle East and African operators deploy 5G fixed-wireless access in underserved rural areas, but macroeconomic headwinds keep near-term volumes modest.

- Microchip Technology Inc.

- Infineon Technologies AG

- Diodes Incorporated

- MACOM Technology Solutions Holdings, Inc.

- Nexperia B.V. (Wingtech Technology Co., Ltd.)

- onsemi (Semiconductor Components Industries, LLC)

- ROHM Co., Ltd.

- Vishay Intertechnology, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- PANJIT International Inc.

- Suzhou Good-Ark Electronics Co., Ltd.

- Skyworks Solutions, Inc.

- Qorvo, Inc.

- Broadcom Inc. (Avago Technologies)

- Excelitas Technologies Corp.

- SemiGen, Inc.

- Richardson Electronics, Ltd.

- Central Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of global 5G infrastructure

- 4.2.2 Rising IoT and smart-consumer electronics demand

- 4.2.3 Expansion of automotive radar and ADAS adoption

- 4.2.4 Growth of LEO satellite constellations

- 4.2.5 mmWave radar uptake in industrial drones and robots

- 4.2.6 Shift toward wide-bandgap (GaN/SiC) diode technology

- 4.3 Market Restraints

- 4.3.1 Volatile raw-material prices (Ga, Si, SiC, InP)

- 4.3.2 Semiconductor capacity constraints and supply chain risk

- 4.3.3 Thermal-management challenges at more than 40 GHz

- 4.3.4 Export-control restrictions on high-freq devices

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Investment Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 PIN Diodes

- 5.1.2 Schottky Diodes

- 5.1.3 Varactor (Tuning) Diodes

- 5.1.4 Gunn Diodes

- 5.1.5 Tunnel Diodes

- 5.1.6 Zener Diodes

- 5.1.7 Other Diodes

- 5.2 By Frequency Band

- 5.2.1 Up to 3 GHz

- 5.2.2 3 - 8 GHz (C-/X-Band)

- 5.2.3 8 - 20 GHz (Ku-/K-Band)

- 5.2.4 20 - 40 GHz (Ka-/V-Band)

- 5.2.5 Above 40 GHz (mmWave)

- 5.3 By Material Technology

- 5.3.1 Silicon (Si)

- 5.3.2 Gallium Arsenide (GaAs)

- 5.3.3 Gallium Nitride (GaN)

- 5.3.4 Silicon Carbide (SiC)

- 5.3.5 Other Materials

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Consumer Electronics

- 5.4.3 Telecommunications and Networking

- 5.4.4 Industrial Manufacturing and Automation

- 5.4.5 Medical and Healthcare

- 5.4.6 Aerospace and Defense

- 5.4.7 Energy and Utilities

- 5.4.8 Other Industries

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microchip Technology Inc.

- 6.4.2 Infineon Technologies AG

- 6.4.3 Diodes Incorporated

- 6.4.4 MACOM Technology Solutions Holdings, Inc.

- 6.4.5 Nexperia B.V. (Wingtech Technology Co., Ltd.)

- 6.4.6 onsemi (Semiconductor Components Industries, LLC)

- 6.4.7 ROHM Co., Ltd.

- 6.4.8 Vishay Intertechnology, Inc.

- 6.4.9 Toshiba Electronic Devices & Storage Corporation

- 6.4.10 Renesas Electronics Corporation

- 6.4.11 STMicroelectronics N.V.

- 6.4.12 PANJIT International Inc.

- 6.4.13 Suzhou Good-Ark Electronics Co., Ltd.

- 6.4.14 Skyworks Solutions, Inc.

- 6.4.15 Qorvo, Inc.

- 6.4.16 Broadcom Inc. (Avago Technologies)

- 6.4.17 Excelitas Technologies Corp.

- 6.4.18 SemiGen, Inc.

- 6.4.19 Richardson Electronics, Ltd.

- 6.4.20 Central Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

微波裝置市場:按產品類型、頻段、最終用戶和分銷管道分類的全球市場預測,2026-2032年頻率合成器市場:按類型、技術、頻率範圍、應用和銷售管道分類-2026-2032年全球市場預測

微波裝置市場:按產品類型、頻段、最終用戶和分銷管道分類的全球市場預測,2026-2032年頻率合成器市場:按類型、技術、頻率範圍、應用和銷售管道分類-2026-2032年全球市場預測 微波裝置市場分析及預測(至2035年):依類型、產品、技術、組件、應用、最終用戶、功能、安裝類型及設備分類

微波裝置市場分析及預測(至2035年):依類型、產品、技術、組件、應用、最終用戶、功能、安裝類型及設備分類 2026年全球微波元件市場報告

2026年全球微波元件市場報告 微波裝置市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、頻率、應用、地區及競爭格局分類,2021-2031年)頻率合成器市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、組件、應用、地區和競爭格局分類,2021-2031年全球多功能微波爐市場(按產品類型、技術、功率、最終用戶和分銷管道分類)—2026-2032年預測微波消解萃取系統市場:按產品類型、應用、最終用戶和分銷管道分類 - 全球預測(2026-2032年)

微波裝置市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、頻率、應用、地區及競爭格局分類,2021-2031年)頻率合成器市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、組件、應用、地區和競爭格局分類,2021-2031年全球多功能微波爐市場(按產品類型、技術、功率、最終用戶和分銷管道分類)—2026-2032年預測微波消解萃取系統市場:按產品類型、應用、最終用戶和分銷管道分類 - 全球預測(2026-2032年) 微波設備市場規模、佔有率、趨勢及預測(按產品類型、頻率、應用和地區),2025 年至 2033 年

微波設備市場規模、佔有率、趨勢及預測(按產品類型、頻率、應用和地區),2025 年至 2033 年 全球射頻和微波二極體市場

全球射頻和微波二極體市場