|

市場調查報告書

商品編碼

1911446

編碼和標記解決方案:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Coding And Marking Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

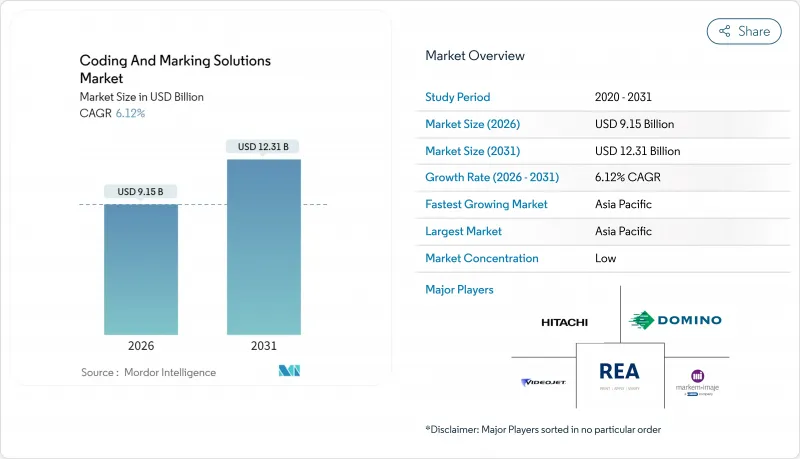

預計到 2026 年,編碼和標記解決方案市場價值將達到 91.5 億美元,從 2025 年的 86.2 億美元成長到 2031 年的 123.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.12%。

對唯一產品識別碼、端到端可追溯性和製造過程中更高監管合規性的強勁需求,正推動著這項擴張。日益嚴格的環境法規加速了從溶劑型油墨轉向光纖雷射系統的轉變,而支援遠端分析和預測性維護的軟體平台則重新定義了客戶價值提案。藥品序列化監管期限、2D條碼的廣泛應用以及GS1數位連結標準的實施,將推動2030年的關鍵投資。同時,半導體短缺正在推動印表機控制設備和耗材的重新設計,這加劇了成本壓力,同時也為供應商多元化採購開闢了新的市場機會。亞太地區的製造業規模和政策協調使其始終處於產能擴張和升級的前沿,鞏固了主導地位。

全球編碼和標誌解決方案市場趨勢與洞察

生產和包裝產業的擴張

新興市場產能的不斷提升,持續推動對整合識別系統的訂單。軟性包裝的快速普及和產品生命週期的縮短,迫使製造商轉向能夠適應不同基材和SKU變更且無需停機的印表機。可口可樂的瓶裝飲料補充裝項目採用GS1數位連結QR碼,在部分拉丁美洲市場,補充裝飲料的銷售額佔比超過50%。為了實現這些目標,該公司越來越依賴高通量連續噴墨設備和堅固耐用的雷射編碼器,以確保在曲面和可回收表面上的清晰可辨。隨著永續性準則的日益普及,注重可重複使用的包裝推動了日期、批號和押金退款資訊的印刷量增加。

端到端可追溯性的需求

藥品序列化已成為食品、飲料和化妝品製造商降低召回風險和驗證產品真偽的典範。 Woolworths在實施GS1 DataMatrix編碼後,食品浪費減少了40%。詳細的庫存可視性已被證明能夠提高營運效率。一個將包裝標識符與分散式帳本連接起來的區塊鏈試點專案已開始提供即時儲存記錄,使品牌所有者能夠透過可追溯性資訊服務獲利。為此,供應商正在將雲端連接器和開放API整合到其編碼設備中,從而從獨立的設備供應商轉型為資料利用支援公司。

高昂的初始投資和營運成本

光纖雷射印表機的價格從1萬美元到10萬美元以上不等,而連續噴墨印表機則需要不斷補充墨水,從而推高了總擁有成本。小規模的合約包裝商不願投資利潤率低的領域,通常會等到監管機構實施新的標籤規定後再升級。管理服務協議和租賃模式正日益普及,因為它們可以將投資從資本支出轉移到可預測的營運成本,但微企業採用這些模式的比例仍然有限。

細分市場分析

預計到2025年,設備收入將佔總收入的大部分,這主要得益於工廠持續的多條生產線安裝。硬體編碼和標記解決方案市場預計將達到49.9億美元,而服務和軟體市場將以6.78%的複合年成長率成長,到2031年將超過21.8億美元,這主要得益於分析訂閱和遠端監控儀表板的普及。 VideojetConnect中嵌入的預測性維護模組可通知操作員液位、溫度偏差和噴嘴狀態,從而減少高達20%的停機時間。備件和耗材採用年度收入模式,色帶和墨水的銷售額與整體列印量的成長密切相關,從而保障了供應商的盈利。

向基於雲端的編碼管理套件的轉變反映了SKU日益成長的複雜性以及對分散工廠的列印規則進行集中管理的需求。開放的API架構能夠與ERP和MES平台無縫整合,簡化審核期間的合規性報告。隨著工業5.0討論的不斷深入,供應商正將編碼設備定位為「融合人工監督和人工智慧輔助決策的協作資產」。

2025年,連續噴墨列印仍佔出貨量的43.78%,證實了其在高速瓶裝和罐裝生產線上的多功能性。隨著品牌商採用耐磨損、防潮的無溶劑永久性標記,雷射打碼機的市佔率不斷擴大。 Markem-Imaje公司的SmartLase F500每分鐘可對多達2000個鋁罐進行打碼,這項性能標準降低了飲料製造商採用雷射技術的門檻。光纖雷射打碼機無需耗材,並減少了VOC排放,從而鞏固了其在環境法規嚴格的地區的地位。

熱感噴墨和按需噴墨系統對於在瓦楞紙箱等多孔材料上進行列印仍然至關重要,而熱感印表機則適用於需要以中等速度列印清晰、可變影像的軟包裝。為了滿足預期的需求激增,Epson等組件製造商正在將其印表機頭產能提高四倍。該公司在日本新建的工廠是一項價值51億美元的策略性投資。

區域分析

預計到2025年,亞太地區將佔全球營收的33.55%,並繼續以6.45%的複合年成長率推動成長。中國的大型快速消費品工廠正在大量安裝高速連續噴墨設備,而印度的藥品出口商正在維修其生產線以滿足印度藥品供應鏈安全局(DSCSA)的進口要求。像DKSH這樣的本地分銷商正在結合其區域市場知識和Koenig & Bauer的噴碼硬體,以加強其在東南亞的售後市場地位。政府為促進智慧工廠而採取的支持措施正在進一步加速硬體和軟體的普及應用,並推動噴碼單元整合到電子和汽車產業叢集的自動化檢測單元中。

北美地區擁有穩定的法規環境,這得益於《藥品安全追蹤法案》(DSCSA) 和美國食品藥物管理局(FDA) 的食品安全法規。隨著零售通路全面過渡到2D條碼(預計在 2027 年完成),能夠以每分鐘 1000 個單元以上的速度進行 300 dpi 圖形顯示的印表機的早期應用正在加速。墨西哥憑藉在美國墨加協定 (USMCA) 下的地理優勢,吸引了許多電子產品和白色家電的組裝基地。美國零售商對包裝薄膜按需噴碼機的應用也在穩定成長。

儘管歐洲的雷射噴碼機裝置量已相當成熟,但其更新換代需求依然強勁,尤其對符合循環經濟目標、旨在減少溶劑排放的雷射噴碼機的需求更為旺盛。德國原始設備製造商 (OEM) 正在指定使用支援 OPC UA 的噴碼機,以便更輕鬆地整合到現有的 PLC 架構中。英國脫歐後,合規要求保持不變,基於 EN 標準的法規仍然有效,這為倉庫自動化列印貼標系統的持續投資提供了支援。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 生產和包裝產業的擴張

- 端到端可追溯性的需求

- 批次編碼的監理要求

- 面向工業4.0的預測性維護

- 朝向無溶劑光纖雷射塗層的轉變

- 市場限制

- 高昂的資本和營運成本

- 預印包裝替代品的成長

- 印表機控制設備半導體短缺

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 投資分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 透過解決方案

- 裝置

- 流體和帶狀物

- 備用零件

- 服務和軟體

- 透過設備技術

- 連續噴墨(CIJ)

- 熱感噴墨(TIJ)

- 雷射打碼機

- 按需滴注和閥門噴射系統

- 熱感

- 透過使用

- 組件識別

- 品牌意識與行銷

- 可追溯性和防偽措施

- 合規性和監理編碼

- 按最終用戶行業分類

- 食品/飲料

- 製藥

- 化妝品和個人護理

- 建築與工業

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Videojet Technologies Inc.

- Domino Printing Sciences plc

- Markem-Imaje Corporation

- Hitachi, Ltd.

- REA Elektronik GmbH

- Linx Printing Technologies Ltd.

- Matthews International Corporation

- Keyence Corporation

- Paul Leibinger GmbH & Co. KG

- Koenig & Bauer Coding GmbH

- Control Print Limited

- ITW FoxJet

- United Barcode Systems SL

- KGK Jet Group

- ID Technology, LLC(ProMach)

- SATO Holdings Corporation

- Danaher Corporation

- Squid Ink Manufacturing, Inc.

- Guangzhou EC-JET Technology Co., Ltd.

- Diagraph Corporation(ITW)

第7章 市場機會與未來展望

The coding and marking solutions market size in 2026 is estimated at USD 9.15 billion, growing from 2025 value of USD 8.62 billion with 2031 projections showing USD 12.31 billion, growing at 6.12% CAGR over 2026-2031.

Robust demand for unique product identifiers, end-to-end traceability and tighter regulatory compliance across manufacturing industries underpins this expansion. Migrating from solvent-based inks to fiber-laser systems is accelerating as environmental regulations tighten, while software-centric platforms that enable remote analytics and predictive maintenance are redefining customer value propositions. Pharmaceutical serialization deadlines, the proliferation of 2D barcodes and the rollout of GS1 Digital Link standards are creating non-discretionary investments through 2030. Meanwhile, semiconductor shortages have prompted redesigns of printer controls and consumables, added cost pressures yet opening white-space opportunities for suppliers with diversified sourcing. Asia-Pacific's manufacturing scale, coupled with policy harmonization, keeps the region at the forefront of capacity expansions and equipment upgrades, consolidating its lead in the coding and marking solutions market.

Global Coding And Marking Solutions Market Trends and Insights

Expansion of production and packaging industry

Capacity additions across emerging markets generate sustained orders for integrated identification systems. Rapid uptake of flexible packaging, coupled with shorter product life cycles, pushes manufacturers toward printers that adapt to multiple substrates and SKU changes without line stoppages. Coca-Cola's refillable bottle program uses GS1 Digital Link-enabled QR codes, and refillable formats now account for more than 50% of sales in select Latin American markets. These objectives drive greater reliance on high-throughput continuous inkjet units and rugged laser coders that preserve legibility on curved or returnable surfaces. As sustainability guidelines take hold, reuse-focused packaging creates incremental print volumes for date, batch and deposit-refund information.

Demand for end-to-end traceability

Pharmaceutical serialization has become a model for food, beverage and cosmetics producers that seek to mitigate recalls and demonstrate authenticity. Woolworths achieved a 40% reduction in food waste after deploying GS1 DataMatrix codes, illustrating the operational gains from granular inventory visibility. Blockchain pilots that connect on-pack identifiers with distributed ledgers are beginning to offer real-time custody records, allowing brand owners to monetize traceability data services. Solution vendors respond by embedding cloud connectors and open APIs into coding hardware, positioning themselves as data enablers rather than stand-alone machine suppliers.

High capital and running costs

Fiber-laser units range from USD 10,000 to over USD 100,000, while continuous inkjet models require a steady supply of make-up fluids that inflate the total cost of ownership. Smaller contract packers hesitate to commit capital in tight-margin categories and often defer upgrades until regulators enforce new labeling rules. Managed service contracts and leasing schemes are gaining popularity because they shift investments from capital expenditure to predictable operating expenses, yet uptake remains modest among micro-enterprises.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory mandates for batch coding

- Industry 4.0-enabled predictive maintenance

- Semiconductor shortages in printer controls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment generated the bulk of 2025 revenue as factories continued multi-line installations; the coding and marking solutions market size for hardware reached USD 4.99 billion. Services and software, however, posted a 6.78% CAGR and are on track to exceed USD 2.18 billion by 2031 on the back of analytics subscriptions and remote-monitoring dashboards. Predictive-maintenance modules embedded in VideojetConnect alert operators to solvent levels, temperature deviations and nozzle health, cutting downtime by up to 20%. Spares and consumables preserve an annuity-style revenue model, with ribbon and ink sales closely mirroring overall print-volume growth and thereby buttressing vendor profitability.

The shift toward cloud-hosted code-management suites reflects mounting SKU complexity and the need for centralized governance of print rules across dispersed plants. Open API architecture enables seamless exchanges with ERP and MES platforms, simplifying compliance reporting during audits. As Industry 5.0 discussions advance, vendors frame coding devices as collaborative assets that integrate human oversight with AI-assisted decision making.

Continuous inkjet retained 43.78% of 2025 shipments, underscoring its versatility on high-speed bottling and canning lines. The coding and marking solutions market share for laser coders expanded as brands embraced solvent-free, permanent marks that withstand abrasion and moisture. Markem-Imaje's SmartLase F500 engraves up to 2,000 aluminum cans per minute, a performance benchmark that eased laser entry barriers for beverage producers. Fiber-laser coders eliminate consumable costs and reduce VOC emissions, strengthening their position in jurisdictions with rigorous environmental acts.

Thermal inkjet and drop-on-demand systems remain vital in porous applications such as corrugated boxes, while thermal-transfer overprinters cater to flexible packaging that demands crisp variable graphics at moderate speeds. Component makers such as Epson are quadrupling printhead capacity to satisfy anticipated demand spikes; its new plant in Japan embodies USD 5.1 billion in strategic investment.

The Coding and Marking Solutions Market Report is Segmented by Solution (Equipment, Fluids and Ribbons, Spares, Services and Software), Equipment Technology (Continuous Inkjet, Thermal Inkjet and More), Application (Component Identification, Brand Recognition and Marketing, and More), End-User Industry (Food & Beverage, Pharmaceutical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 33.55% of global revenue in 2025 and continues to lead growth with a 6.45% CAGR. China's large-scale FMCG plants consume fleets of high-speed continuous inkjets, while India's pharmaceutical exporters retrofit lines to satisfy DSCSA import requirements. Local distributors such as DKSH pair regional market knowledge with Koenig & Bauer Coding's hardware, improving aftermarket coverage in Southeast Asia. Government incentives that fund smart-factory upgrades further stimulate hardware and software uptake, embedding coding units into automated inspection cells across electronics and automotive clusters.

North America shows high regulatory stability anchored by DSCSA and FDA food-safety statutes. The looming 2027 deadline for full 2D barcode transition across retail channels spurs early adoption of printers capable of 300 dpi graphics at line speeds above 1,000 units per minute. Mexico leverages USMCA proximity to attract electronics and white-goods assembly, resulting in incremental installations of drop-on-demand coders on packaging films destined for U.S. retailers.

Europe maintains a mature installed base yet demonstrates steady replacement demand, particularly for laser coders aligned with circular-economy objectives to cut solvent emissions. Germany's OEMs specify OPC UA-ready coders, easing their integration into existing PLC architecture. Brexit has not altered United Kingdom compliance expectations, keeping EN-aligned regulations intact and supporting ongoing investments in print-and-apply systems for warehouse automation.

- Videojet Technologies Inc.

- Domino Printing Sciences plc

- Markem-Imaje Corporation

- Hitachi, Ltd.

- REA Elektronik GmbH

- Linx Printing Technologies Ltd.

- Matthews International Corporation

- Keyence Corporation

- Paul Leibinger GmbH & Co. KG

- Koenig & Bauer Coding GmbH

- Control Print Limited

- ITW FoxJet

- United Barcode Systems S.L.

- KGK Jet Group

- ID Technology, LLC (ProMach)

- SATO Holdings Corporation

- Danaher Corporation

- Squid Ink Manufacturing, Inc.

- Guangzhou EC-JET Technology Co., Ltd.

- Diagraph Corporation (ITW)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of production and packaging industry

- 4.2.2 Demand for end-to-end traceability

- 4.2.3 Regulatory mandates for batch coding

- 4.2.4 Industry 4.0-enabled predictive maintenance

- 4.2.5 Shift to solvent-free fiber-laser coding

- 4.3 Market Restraints

- 4.3.1 High capital and running costs

- 4.3.2 Growth of pre-printed packaging alternatives

- 4.3.3 Semiconductor shortages in printer controls

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investments Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Solution

- 5.1.1 Equipment

- 5.1.2 Fluids and Ribbons

- 5.1.3 Spares

- 5.1.4 Services and Software

- 5.2 By Equipment Technology

- 5.2.1 Continuous Inkjet (CIJ)

- 5.2.2 Thermal Inkjet (TIJ)

- 5.2.3 Laser Coders

- 5.2.4 Drop-on-Demand and Valve Jet

- 5.2.5 Thermal Transfer Overprinting

- 5.3 By Application

- 5.3.1 Component Identification

- 5.3.2 Brand Recognition and Marketing

- 5.3.3 Traceability and Anti-counterfeiting

- 5.3.4 Compliance and Regulatory Coding

- 5.4 By End-user Industry

- 5.4.1 Food and Beverages

- 5.4.2 Pharmaceutical

- 5.4.3 Cosmetics and Personal Care

- 5.4.4 Construction and Industrial

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Videojet Technologies Inc.

- 6.4.2 Domino Printing Sciences plc

- 6.4.3 Markem-Imaje Corporation

- 6.4.4 Hitachi, Ltd.

- 6.4.5 REA Elektronik GmbH

- 6.4.6 Linx Printing Technologies Ltd.

- 6.4.7 Matthews International Corporation

- 6.4.8 Keyence Corporation

- 6.4.9 Paul Leibinger GmbH & Co. KG

- 6.4.10 Koenig & Bauer Coding GmbH

- 6.4.11 Control Print Limited

- 6.4.12 ITW FoxJet

- 6.4.13 United Barcode Systems S.L.

- 6.4.14 KGK Jet Group

- 6.4.15 ID Technology, LLC (ProMach)

- 6.4.16 SATO Holdings Corporation

- 6.4.17 Danaher Corporation

- 6.4.18 Squid Ink Manufacturing, Inc.

- 6.4.19 Guangzhou EC-JET Technology Co., Ltd.

- 6.4.20 Diagraph Corporation (ITW)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

2026年全球骨材配料機市場報告

2026年全球骨材配料機市場報告 編碼和標記設備市場:2026-2032年全球市場預測(按技術類型、產品類型、印刷圖案、印刷材料、應用和最終用戶行業分類)編碼與識別市場:2026-2032年全球市場預測(按作業系統、分銷管道、最終用戶和應用分類)攜帶式直接零件標記條碼掃描器市場:按掃描器技術、連接方式、代碼類型和最終用戶產業分類-全球預測,2026-2032年全球直接零件標記解決方案市場(按技術、組件、材料、應用和最終用途行業分類)預測(2026-2032 年)

編碼和標記設備市場:2026-2032年全球市場預測(按技術類型、產品類型、印刷圖案、印刷材料、應用和最終用戶行業分類)編碼與識別市場:2026-2032年全球市場預測(按作業系統、分銷管道、最終用戶和應用分類)攜帶式直接零件標記條碼掃描器市場:按掃描器技術、連接方式、代碼類型和最終用戶產業分類-全球預測,2026-2032年全球直接零件標記解決方案市場(按技術、組件、材料、應用和最終用途行業分類)預測(2026-2032 年) 雷射編碼打標設備:全球市佔率及排名、總收入及需求預測(2025-2031年)

雷射編碼打標設備:全球市佔率及排名、總收入及需求預測(2025-2031年) 工業賦碼與識別解決方案(2025):按需可變資料需求推動轉型

工業賦碼與識別解決方案(2025):按需可變資料需求推動轉型 全球生成人工智慧編碼助理市場

全球生成人工智慧編碼助理市場 全球打碼和標記設備市場(2025-2029)

全球打碼和標記設備市場(2025-2029) 打碼和標記設備市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年

打碼和標記設備市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年