|

市場調查報告書

商品編碼

1911308

印度工業自動化:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031)India Industrial Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

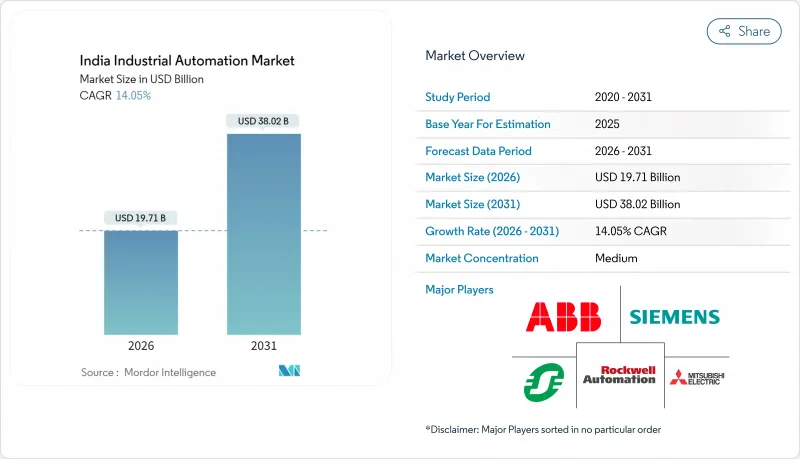

2025年印度工業自動化市場價值為172.8億美元,預計到2031年將達到380.2億美元,而2026年為197.1億美元。

預測期(2026-2031 年)的複合年成長率預計為 14.05%。

持續的政策支援、老舊工廠的快速現代化改造以及感測器價格的下降共同支撐了兩位數的成長。生產連結獎勵計畫計劃,促進了外國直接投資,並引發了現有設施維修的蓬勃發展,從而提高了生產力和出口競爭力。跨國公司擴大了其本地生產基地,以縮短供應鏈並規避進口關稅,而中型企業則採用了基於雲端的執行軟體來克服資金限制。同時,私營部門主導的5G試點計畫和邊緣運算平台緩解了延遲問題,並促進了流程工廠預測性維護的實施。儘管網路安全措施和熟練勞動力的供應仍然是關鍵問題,但政策主導的升級週期已使需求保持了穩健的成長動能。 [1]

印度工業自動化市場趨勢與洞察

加速「印度製造」製造業投資,推動自動化普及

自2024年以來,外國直接投資(FDI)流入擴大了工廠自動化的整體預算。西門子投資100億印度盧比(約1.205億美元)用於擴大驅動器和控制器的生產,三菱電機投資22億印度盧比(約2,650萬美元)用於建造本地組裝。這些對現有設施的升級改造專注於擴充性和模組化設備,而不是新的資本投資,從而實現了更快的投資回報和更高的產能運轉率。古吉拉突邦、馬哈拉斯特拉邦和泰米爾納德邦的叢集正在吸引相關供應商,並在整個價值鏈中傳播技術訣竅。出口導向製造商也在整合全球品質標準,從而推動了對先進運動控制、節能驅動器和機器安全系統的需求。

政府的生產連結獎勵計畫機制加速了僑民產業的現代化。

生產連結獎勵計畫計劃 (PLI) 已撥款 1,402 億印度盧比(約 16.9 億美元),用於支持能夠證明其已做好工業 4.0 準備的行業,該計劃將持續到 2025 年。汽車產業的申請者必須證明其生產線已完全連網,並配備 PLC 控制站和即時品質監控系統,才能繼續獲得增量補貼。電子產品製造商則面臨更嚴格的標準,包括預測性維護能力以及對分包商 100% 的可追溯性。這項規則的設計將放大下游需求,因為一級供應商要求三級供應商實施相容的自動化層,使零件、模具和包裝合作夥伴的市場參與度翻倍。

三級供應商對資本支出的高度敏感度限制了自動化技術的採用。

中小型零件供應商的EBITDA獲利率僅為 8-12%,應收帳款週期長達 90-120 天,這限制了其可用於自動化的自由現金流。全面的設備升級需要相當於年銷售額 15-20% 的資金,許多公司如果沒有補貼融資,難以克服這一障礙。雖然信用擔保降低了貸款機構的風險權重,但抵押品要求和核准延遲仍然阻礙了自動化技術的快速普及。這可能導致生態系統兩極化,一級和二級供應商快速數位化,而三級供應商則落後,破壞了原始設備製造商 (OEM) 所重視的同步生產模式。

細分市場分析

到2025年,工業控制系統將佔據印度工業自動化市場佔有率的37.15%,這主要得益於汽車行業對PLC的強勁需求以及化學工業對DCS的廣泛應用。同時,隨著雲端製造執行系統(MES)訂閱模式的普及降低了進入門檻,軟體收入預計將以15.05%的複合年成長率成長。預計到2031年,印度工業自動化市場軟體解決方案的規模將翻倍,這主要得益於中型企業將ERP、MES和品質分析整合到單一系統中。現場設備的成長得益於價格適中的感測器的普及以及鋼鐵廠和食品加工廠對預測性維護的日益重視。此外,由於混合架構需要持續的網路修補程式和模型重新訓練,業務收益也在不斷成長。

為了應對保險公司日益嚴格的審查,大多數控制系統升級方案都內建了增強型網路安全模組和基於角色的存取控制。同時,隨著監管審核追蹤要求對設計修訂進行數位簽章簽名,產品生命週期管理軟體在汽車和航太領域正贏得訂單。人機介面已採用平板電腦式觸控屏,將操作員訓練時間縮短至三天以內。這些變化共同推動收入來源向持續的軟體訂閱和管理服務轉移,而硬體仍然是基礎。

到2025年,可程式自動化將佔收入的41.45%,這主要得益於需要快速更改配方的混合型組裝。然而,隨著工廠將人工智慧、機器視覺和邊緣分析技術整合到封閉回路型最佳化系統中,整合式超自動化正以16.35%的複合年成長率快速成長。像塔塔鋼鐵這樣的早期採用者,在現有SCADA系統上疊加人工智慧預測模型後,計劃外停機時間減少了20%。如果目前的普及速度持續下去,到2031年,印度與超自動化相關的工業自動化市場規模可能達到123.5億美元。

統一的資料層對於向超自動化轉型至關重要,供應商已將MQTT仲介和OPC-UA閘道器與控制器升級捆綁在一起。到2025年,勞動力再培訓預算將增加25%,用於增加對多技能培訓計畫的投入,以使操作人員能夠勝任人工智慧輔助的工作流程。監管審核現在建議採用能夠記錄所有程式參數以實現可追溯性的自動化系統,這進一步加速了向整合式堆疊的轉型。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速「印度製造」製造業投資

- 政府生產關聯激勵計劃對各行業的激勵措施

- 微型、微企業(MSMEs)現有設施數位化維修的快速擴展

- 工業感測器成本正在大幅下降

- 顯著趨勢:Start-Ups主導中型工廠對人工智慧驅動的預測性維護的需求

- 一個鮮為人知的趨勢:與排碳權掛鉤的能源密集型金屬產業自動化

- 市場限制

- 三級供應商對資本支出(CAPEX)高度敏感

- 系統整合商生態系統分散,存在品質差距

- 一個鮮為人知的趨勢:OT網路的網路安全保險費不斷上漲

- 一個被忽略的趨勢:技術工人從產業叢集外流

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 透過解決方案

- 工業控制系統

- 分散式控制系統(DCS)

- 監控與數據採集(SCADA)

- 可程式邏輯控制器(PLC)

- 人機介面(HMI)

- 其他控制系統

- 現場設備

- 感測器和發射器

- 閥門和致動器

- 馬達和驅動器

- 機器人技術

- 其他現場設備

- 軟體

- 產品生命週期管理(PLM)

- 企業資源規劃(ERP)

- 製造執行系統(MES)

- 其他軟體

- 服務

- 一體化

- 維護和培訓

- 工業控制系統

- 按自動化類型

- 固定自動化

- 可程式自動化

- 靈活或模組化自動化

- 整合式或高度自動化

- 按最終用戶行業分類

- 汽車/運輸設備

- 石油和天然氣

- 食品/飲料

- 製藥和生命科學

- 電力/公共產業

- 電子和半導體

- 化工/石油化工

- 金屬和採礦

- 消費品(快速消費品)

- 包裝

- 其他

- 透過部署模式

- 本地部署

- 雲

- 混合

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens Limited

- ABB India Limited

- Yokogawa India Ltd.

- Rockwell Automation India Pvt. Ltd.

- Schneider Electric India Pvt. Ltd.

- Honeywell Automation India Ltd.

- Emerson Automation Solutions India Pvt. Ltd.

- Mitsubishi Electric India Pvt. Ltd.

- Omron Automation Private Limited

- Bosch Rexroth India Pvt. Ltd.

- B and R Industrial Automation Pvt. Ltd.

- Larsen and Toubro Ltd.

- Fanuc India Pvt. Ltd.

- Delta Electronics India Pvt. Ltd.

- GE Power India Ltd.

- Tata Elxsi Ltd.

- Wipro Enterprises Pvt. Ltd.

- Akyapak India Pvt. Ltd.

- Bajaj Electricals Ltd.

- Bharat Heavy Electricals Ltd.

第7章 市場機會與未來展望

The India industrial automation market was valued at USD 17.28 billion in 2025 and estimated to grow from USD 19.71 billion in 2026 to reach USD 38.02 billion by 2031, at a CAGR of 14.05% during the forecast period (2026-2031).

Ongoing policy support, rapid modernization of legacy plants, and falling sensor prices together sustain double-digit expansion. Foreign direct investment swelled after the Production Linked Incentive program linked cash disbursements to Industry 4.0 readiness, triggering a wave of brownfield retrofits that lift productivity and export competitiveness. Multinationals increased local manufacturing footprints to shorten supply chains and avoid import duties, while mid-tier enterprises adopted cloud-based execution software to overcome capital constraints. Meanwhile, private 5G pilots and edge computing platforms reduced latency concerns and encouraged predictive maintenance rollouts in process plants. Cybersecurity readiness and skilled labour availability remain watchpoints, yet the policy-driven upgrade cycle keeps demand on a strong growth path.[1]

India Industrial Automation Market Trends and Insights

Accelerated Make in India Manufacturing Investments Drive Automation Uptake

Foreign direct investment flowing into the country after 2024 elevated overall factory-automation budgets. Siemens committed INR 10,000 million (USD 120.5 million) to expand production of drives and controllers, while Mitsubishi Electric directed INR 2,200 million (USD 26.5 million) toward local assembly lines. These brownfield upgrades emphasize scalable, modular equipment rather than greenfield capacity, enabling faster returns and higher asset utilization. Clusters in Gujarat, Maharashtra, and Tamil Nadu attract allied suppliers, spreading technical know-how along the value chain. Export-oriented manufacturers also integrate global quality benchmarks, tightening demand for advanced motion control, energy-efficient drives, and machine safety systems.

Government PLI Scheme Incentives Accelerate Discrete Industry Modernization

The Production Linked Incentive program disbursed INR 140,200 million (USD 1.69 billion) by 2025 to discrete industries on the condition of demonstrable Industry 4.0 compliance. Automotive applicants must showcase fully networked production lines with PLC-controlled stations and real-time quality monitoring to keep receiving tranche payments. Electronics manufacturers face even stricter benchmarks such as predictive maintenance capability and 100 percent traceability across subcontractors. This rule design amplifies downstream demand because Tier-1 suppliers press Tier-3 vendors to install compatible automation layers, multiplying market pull across component, tooling, and packaging partners.

High CAPEX Sensitivity Among Tier-3 Suppliers Constrains Automation Adoption

Smaller component vendors often operate on 8-12% EBITDA margins and face 90-120-day receivable cycles, leaving limited free cash for automation. Comprehensive upgrades can require capital equal to 15-20% of annual revenue, a hurdle that many cannot clear without subsidized loans. While the credit guarantee scheme reduces risk weightings for lenders, collateral requirements and approval delays still deter quick uptake. This creates a bifurcated ecosystem where Tier-1 and Tier-2 firms digitize rapidly while Tier-3 lags, potentially undermining the synchronous production models favoured by OEMs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Brownfield Digital Retrofits Across MSMEs

- Sharp Decline in Industrial Sensor Costs Enables Widespread IoT Adoption

- Fragmented System-Integrator Ecosystem Creates Quality Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial control systems retained 37.15% India industrial automation market share in 2025, anchored by robust PLC demand in automotive and DCS rollouts in chemicals. Software revenue, however, is climbing at a 15.05% CAGR as cloud-hosted manufacturing execution suites become subscription-priced, lowering entry hurdles. The India industrial automation market size for software solutions is projected to double between 2026 and 2031 as mid-tier firms integrate ERP, MES, and quality analytics into a single stack. Field devices gained from cheaper sensors, expanding predictive-maintenance deployments in steel mills and food processing plants. Service revenue also rose because hybrid architectures need ongoing cyber-patching and model retraining.

Enhanced cybersecurity modules and role-based access controls now come bundled inside most control-system upgrades, addressing rising insurance scrutiny. Meanwhile, product lifecycle management software wins orders in automotive and aerospace because regulatory audit trails demand digitally signed design revisions. Human-machine interfaces adopt tablet-style touchscreens, shortening operator training to under three days. Collectively, these shifts pivot revenue toward recurring software subscriptions and managed services, though hardware remains foundational.

Programmable automation accounted for 41.45% revenue in 2025, favoured for mixed-model assembly lines that need rapid recipe changes. Yet integrated hyper-automation is expanding at a 16.35% CAGR as plants converge AI, machine vision, and edge analytics into closed-loop optimization. Early adopters like Tata Steel logged a 20% cut in unplanned downtime after overlaying AI predictive models on legacy SCADA. The India industrial automation market size tied to hyper-automation could reach USD 12.35 billion by 2031 if current adoption curves hold.

Transitioning to hyper-automation requires unified data layers, so vendors bundle MQTT brokers and OPC-UA gateways with controller upgrades. Workforce retraining budgets rose 25% in 2025 as firms invest in multi-skilling programs to align operators with AI-assisted workflows. Regulatory audits now prefer automation systems that log every process parameter for traceability, further reinforcing the move toward integrated stacks.

The India Industrial Automation Market Report is Segmented by Solution (Industrial Control Systems, Field Devices, Software, and Services), Automation Type (Fixed, Programmable, Flexible, and Integrated), End-User Industry (Automotive, Oil and Gas, Food and Beverage, Pharmaceuticals, Power, Electronics, and More), and Deployment Mode (On-Premise, Cloud, and Hybrid). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens Limited

- ABB India Limited

- Yokogawa India Ltd.

- Rockwell Automation India Pvt. Ltd.

- Schneider Electric India Pvt. Ltd.

- Honeywell Automation India Ltd.

- Emerson Automation Solutions India Pvt. Ltd.

- Mitsubishi Electric India Pvt. Ltd.

- Omron Automation Private Limited

- Bosch Rexroth India Pvt. Ltd.

- B and R Industrial Automation Pvt. Ltd.

- Larsen and Toubro Ltd.

- Fanuc India Pvt. Ltd.

- Delta Electronics India Pvt. Ltd.

- GE Power India Ltd.

- Tata Elxsi Ltd.

- Wipro Enterprises Pvt. Ltd.

- Akyapak India Pvt. Ltd.

- Bajaj Electricals Ltd.

- Bharat Heavy Electricals Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated "Make in India" manufacturing investments

- 4.2.2 Government PLI scheme incentives for discrete industries

- 4.2.3 Rapid expansion of brownfield digital retrofits across MSMEs

- 4.2.4 Sharp decline in industrial sensor costs

- 4.2.5 Under-the-radar: Start-up led AI-driven predictive maintenance demand from mid-tier plants

- 4.2.6 Under-the-radar: Carbon-credit linked automation for energy-intensive metals vertical

- 4.3 Market Restraints

- 4.3.1 High CAPEX sensitivity among Tier-3 suppliers

- 4.3.2 Fragmented system-integrator ecosystem quality gaps

- 4.3.3 Under-the-radar: Cyber-insurance premium escalation for OT networks

- 4.3.4 Under-the-radar: Skilled labour flight from industrial clusters

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Solution

- 5.1.1 Industrial Control Systems

- 5.1.1.1 Distributed Control System (DCS)

- 5.1.1.2 Supervisory Control and Data Acquisition (SCADA)

- 5.1.1.3 Programmable Logic Controller (PLC)

- 5.1.1.4 Human Machine Interface (HMI)

- 5.1.1.5 Other Control Systems

- 5.1.2 Field Devices

- 5.1.2.1 Sensors and Transmitters

- 5.1.2.2 Valves and Actuators

- 5.1.2.3 Motors and Drives

- 5.1.2.4 Robotics

- 5.1.2.5 Other Field Devices

- 5.1.3 Software

- 5.1.3.1 Product Lifecycle Management (PLM)

- 5.1.3.2 Enterprise Resource Planning (ERP)

- 5.1.3.3 Manufacturing Execution System (MES)

- 5.1.3.4 Other Software

- 5.1.4 Services

- 5.1.4.1 Integration

- 5.1.4.2 Maintenance and Training

- 5.1.1 Industrial Control Systems

- 5.2 By Automation Type

- 5.2.1 Fixed Automation

- 5.2.2 Programmable Automation

- 5.2.3 Flexible or Modular Automation

- 5.2.4 Integrated or Hyper-Automation

- 5.3 By End-user Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Oil and Gas

- 5.3.3 Food and Beverage

- 5.3.4 Pharmaceuticals and Life Sciences

- 5.3.5 Power and Utilities

- 5.3.6 Electronics and Semiconductors

- 5.3.7 Chemicals and Petrochemicals

- 5.3.8 Metals and Mining

- 5.3.9 Fast-Moving Consumer Goods (FMCG)

- 5.3.10 Packaging

- 5.3.11 Others

- 5.4 By Deployment Mode

- 5.4.1 On-Premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siemens Limited

- 6.4.2 ABB India Limited

- 6.4.3 Yokogawa India Ltd.

- 6.4.4 Rockwell Automation India Pvt. Ltd.

- 6.4.5 Schneider Electric India Pvt. Ltd.

- 6.4.6 Honeywell Automation India Ltd.

- 6.4.7 Emerson Automation Solutions India Pvt. Ltd.

- 6.4.8 Mitsubishi Electric India Pvt. Ltd.

- 6.4.9 Omron Automation Private Limited

- 6.4.10 Bosch Rexroth India Pvt. Ltd.

- 6.4.11 B and R Industrial Automation Pvt. Ltd.

- 6.4.12 Larsen and Toubro Ltd.

- 6.4.13 Fanuc India Pvt. Ltd.

- 6.4.14 Delta Electronics India Pvt. Ltd.

- 6.4.15 GE Power India Ltd.

- 6.4.16 Tata Elxsi Ltd.

- 6.4.17 Wipro Enterprises Pvt. Ltd.

- 6.4.18 Akyapak India Pvt. Ltd.

- 6.4.19 Bajaj Electricals Ltd.

- 6.4.20 Bharat Heavy Electricals Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球機器人雷射焊接單元市場報告2026年土耳其機器人焊接單元解決方案全球市場報告2026年5G鑽井機器人全球市場報告2026年全球風化層挖掘機器人市場報告

2026年全球機器人雷射焊接單元市場報告2026年土耳其機器人焊接單元解決方案全球市場報告2026年5G鑽井機器人全球市場報告2026年全球風化層挖掘機器人市場報告 工業自動化和設備管理軟體市場:2026-2032年全球市場預測(按設備類型、組織規模、連接方式、部署模式、應用程式和最終用戶產業分類)2026年全球工業自動化市場報告2026年全球自動化與控制市場報告辦公室尋呼系統市場按技術、組件類型、最終用戶和部署模式分類,全球預測(2026-2032年)靜電紡絲噴嘴市場按類型、技術、材料、應用和最終用途分類,全球預測(2026-2032年)全球鑽屑管理系統市場依技術、鑽井液類型、應用、服務模式及最終用途分類,2026-2032年預測

工業自動化和設備管理軟體市場:2026-2032年全球市場預測(按設備類型、組織規模、連接方式、部署模式、應用程式和最終用戶產業分類)2026年全球工業自動化市場報告2026年全球自動化與控制市場報告辦公室尋呼系統市場按技術、組件類型、最終用戶和部署模式分類,全球預測(2026-2032年)靜電紡絲噴嘴市場按類型、技術、材料、應用和最終用途分類,全球預測(2026-2032年)全球鑽屑管理系統市場依技術、鑽井液類型、應用、服務模式及最終用途分類,2026-2032年預測