|

市場調查報告書

商品編碼

1910927

印尼煤炭市場:佔有率分析、產業趨勢、統計和成長預測(2026-2031年)Indonesia Coal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

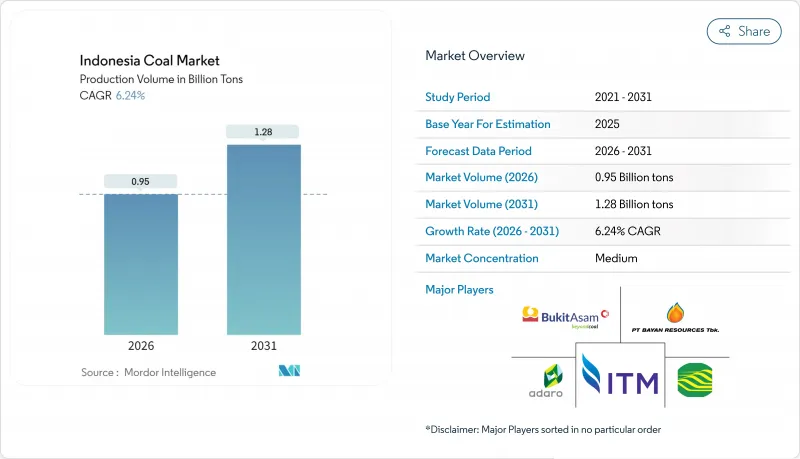

預計印尼煤炭市場將從 2025 年的 8.9 億噸成長到 2026 年的 9.5 億噸,到 2031 年將達到 12.8 億噸,2026 年至 2031 年的複合年成長率為 6.24%。

這一市場規模反映了印尼作為全球最大動力煤出口國的地位及其在該國電力結構中的強勢地位。在脫碳討論活性化的背景下,印尼國家電力公司(PLN)持續的基本負載需求、鎳冶煉業的蓬勃發展以及不斷擴大的“中國+1”戰略,都在支撐著需求成長。綜合礦業公司不斷簽訂長期銷售契約,從而穩定現金流,而戰略儲備的品質也為優質煤炭生產商提供了額外的定價權。同時,促進煤氣化和二甲醚計劃的監管改革正在為低階煤開闢新的國內市場。這些並行的趨勢表明,即使全球煤炭資本成本不斷上升,印尼煤炭市場仍保持強勁勢頭。

印尼煤炭市場趨勢及展望

PLN主導的低熱值煤炭基本負載需求持續存在

由於印尼國家電力公司 (PLN) 快速擴張可再生能源的空間有限,煤炭仍然是印尼電力供應系統的核心。政府對電價的收費系統要求電力公司優先選擇成本最低的發電燃料,而次煙煤仍然是為爪哇-峇裡島負載中心供電最具成本效益的選擇。為了確保電網穩定,需要進一步加強供應優先順序,因為燃煤發電廠提供頻率和電壓調節服務的邊際成本低於電池儲能。從財務角度來看,PLN 的煤炭採購預算可預測,這降低了交易對象的信用風險,並允許礦業公司簽訂固定數量、多年期的銷售合約。因此,即使可再生能源滲透率逐步提高,印尼煤炭市場仍受惠於持續的結構性需求下限。

鎳冶煉廠和電動車電池冶煉廠的燃煤自發電量迅速成長

印尼2020年禁止鎳礦出口的政策促使超過150億美元的資金流入鎳加工廠。這些工廠需要不間斷的電力供應來運作電弧爐。中資冶煉廠通常會自建200至350兆瓦的燃煤發電廠,進而形成一個不受印尼國家電力公司(PLN)輸電優先級影響的專屬市場。這些自建電廠通常簽訂以美元計價的購電協議,使礦商能夠獲得比公用事業公司更高的收益。這種經營模式既能確保高額利潤,又能實現收入來源多元化。隨著下游企業拓展前驅體、正極材料和電池材料業務,需求將進一步成長,看似矛盾地將煤炭的使用與低碳經濟連結起來。預計到2030年,這些趨勢將推動工業用電需求成長超過國內平均消費量。

國內市場義務(DMO)價格上限

印尼的國內煤炭價格管制(DMO)制度要求煤礦企業必須以政府設定的基準價格在國內銷售其年產量的25%。由於在價格高企時期,該基準價格可能比出口價格低至每噸30美元,強制性折扣限制了利潤空間的擴張,並獎勵企業專注於生產高熱值(高CV)煤炭,這些煤炭主要用於出口。金融機構已逐步下調受DMO價格上限影響的蘊藏量估值,導致企業難以取得擴張資金籌措。雖然這項政策保護了國有電力公司PLN和工業用戶免受價格飆升的影響,但也抑制了對新的低階煤計劃的投資,從而限制了印尼煤炭市場的供應成長。

細分市場分析

到2025年,次菸煤將佔印尼煤炭市場46.85%的佔有率,這得益於東加里曼丹和南加里曼丹豐富的煤層資源,可為國內外買家提供具有成本競爭力的燃料。儘管目前次焦結煤的產量將以7.86%的複合年成長率成長,其在印尼煤炭市場的佔有率將從2025年的26.40%成長到2031年的約三分之一。高熱值煤的價格溢價為每噸15-20美元,並符合超超臨界電廠的規格要求,而超超臨界電廠在亞洲正變得越來越普遍。區域高爐對冶金煤的需求將進一步增強擁有優質蘊藏量的生產商的定價權。褐煤的成長預計將保持平穩,這主要受國內氣化先導工廠和老舊、低效鍋爐的影響。生產區域與煤炭等級分佈相符,例如東加里曼丹的Kaltim Prima Coal等業者專注於生產優質煤,而蘇門答臘的礦商則主要向印尼國家電力公司(PLN)供應次煙煤。這種品質細分使企業能夠根據價格差異和物流成本調整不同等級煤炭的混合比例,從而對沖市場波動風險並維持均衡的投資組合。

印尼煤炭市場報告按煤炭類別(褐煤/低階煤、次煙煤、煙煤和煉焦煤)和應用領域(發電、鋼鐵冶金、水泥及其他應用)進行細分。市場規模和預測以產量(噸)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- PLN長期主導的低熱值煤炭基本負載需求

- 鎳冶煉廠和電動車電池冶煉廠的燃煤自發電量迅速成長

- 受「中國+1」策略影響,海運需求轉向印尼。

- 政府對低階煤「氣化和二甲醚」製程的誘因

- CCUS試點計畫實現高熱值煤出口溢價

- 市場限制

- 國內市場義務(DMO)價格上限

- 由JETP資助的燃煤發電廠提前退役

- 州級暫停發放新的採礦許可證(加里曼丹、蘇門答臘)

- 環境、社會及公司治理(ESG)因素推升印尼煤炭貿易融資成本

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 按煤級

- 褐煤/低品位

- 次煙煤

- 煙煤和焦結煤

- 透過使用

- 發電

- 鋼鐵冶金

- 水泥及其他用途

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、聯盟、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- PT Bumi Resources Tbk

- PT Adaro Energy Indonesia Tbk

- PT Bayan Resources Tbk

- PT Bukit Asam Tbk

- PT Indo Tambangraya Megah Tbk

- PT Kaltim Prima Coal

- PT Arutmin Indonesia

- PT Kideco Jaya Agung

- PT Berau Coal Energy Tbk

- PT Indika Energy Tbk

- Golden Energy & Resources Ltd

- BlackGold Natural Resources

- PT Bhakti Energi Persada

- PT Bayan International

- PT Multi Harapan Utama

- Adani Indonesia(Adaro JV)

- Glencore(PT Balangan Coal)

- PT Petrosea Tbk

- PT Delta Dunia Makmur Tbk

- PT Resource Alam Indonesia Tbk

第7章 市場機會與未來展望

The Indonesia Coal market is expected to grow from 0.89 Billion tons in 2025 to 0.95 Billion tons in 2026 and is forecast to reach 1.28 Billion tons by 2031 at 6.24% CAGR over 2026-2031.

The market's scale reflects Indonesia's position as the world's largest thermal-coal exporter and its entrenched role in the country's power mix. Ongoing PLN baseload demand, a nickel smelting boom, and a widening China-plus-One strategy collectively underpin demand growth, despite intensifying decarbonization rhetoric. Integrated miners continue to secure long-term offtake contracts that stabilize cash flows, while strategic reserve quality gives premium-grade producers additional pricing power. At the same time, regulatory reforms encouraging gasification and dimethyl-ether projects are opening new domestic outlets for low-rank coal. These parallel trends signal that the Indonesian coal market will remain resilient even as global capital costs for coal rise.

Indonesia Coal Market Trends and Insights

Prolonged PLN-led Baseload Demand for Low-CV Thermal Coal

PLN's limited headroom for rapid renewable build-out keeps coal in the core of Indonesia's power dispatch stack. Subsidized electricity tariffs require the utility to prioritize the lowest-cost generation fuel, and sub-bituminous coal remains the most cost-effective option delivered to Java-Bali load centers. Grid stability needs further reinforcement of dispatch preference because coal plants provide frequency and voltage services at a lower marginal cost than battery storage. Financially, PLN's budget allocation for coal procurement is predictable, reducing counterparties' credit risk and enabling miners to structure multi-year offtake agreements that lock in volumes. Consequently, the Indonesian coal market benefits from a structural demand floor that persists even as renewable penetration rises incrementally.

Surge in Coal-fired Captive Power for Nickel & EV-battery Smelters

Indonesia's 2020 nickel-ore export ban sparked capital inflows exceeding USD 15 billion into nickel processing complexes that require uninterrupted power for electric-furnace operations. Chinese-backed smelters routinely install on-site coal plants sized at 200-350 MW, providing a dedicated market immune to PLN's dispatch priorities. Captive arrangements typically involve dollar-linked power-purchase agreements, which grant miners higher realizations than utility deliveries. The business model thus secures premium margins while diversifying revenue streams. Demand expands further as downstream players move into precursor-cathode and battery materials, linking coal usage paradoxically to the low-carbon economy. These trends keep industrial offtake growth ahead of national average consumption through 2030.

Mandatory Domestic Market Obligation (DMO) Price Caps

Indonesia's DMO mechanism obliges miners to sell 25% of annual output at a government-set benchmark that trails export parity by up to USD 30 per ton during high-price cycles. This enforced discount compresses margin expansion opportunities and incentivizes firms to skew production toward higher-CV grades, which are earmarked exclusively for export. Financiers increasingly mark down reserve valuations that are exposed to DMO ceilings, complicating debt-raising for expansion. Although the policy shields PLN and industrial buyers from price spikes, it reduces investment appetite in new low-rank coal projects, thereby dampening incremental supply growth in the Indonesian coal market.

Other drivers and restraints analyzed in the detailed report include:

- China-plus-One Strategy Shifting Seaborne Demand to Indonesia

- Government "Gasification & DME" Incentives for Low-rank Coal

- Accelerated Coal-plant Retirement under JETP Funding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sub-bituminous coal accounted for 46.85% of the Indonesian coal market in 2025, leveraging abundant East and South Kalimantan seams that deliver cost-competitive fuel to both domestic and export buyers. Despite this current dominance, bituminous and coking coal output is forecast to grow at an 7.86% CAGR between 2026 and 2031, lifting its share of the Indonesian coal market from 26.40% in 2025 to nearly one-third by 2031. Higher-CV grades unlock premiums of USD 15-20 per ton and align with emerging ultra-supercritical power-plant specifications in Asia. Metallurgical coal demand from regional blast furnaces further reinforces pricing power for producers with suitable reserve quality. Lignite remains oriented toward domestic gasification pilots and legacy low-efficiency boilers, implying flat growth. Production geography mirrors grade distribution; East Kalimantan operators, such as Kaltim Prima Coal, focus on premium grades, whereas Sumatra miners largely supply sub-bituminous coal to PLN. This quality segmentation enables portfolio balancing, as companies hedge against market swings by adjusting blend ratios between grades according to price differentials and logistics economics.

The Indonesia Coal Market Report is Segmented by Coal Grade (Lignite/Low-Rank, Sub-Bituminous, and Bituminous and Coking) and Application (Power Generation, Iron, Steel, and Metallurgy, and Cement and Other Applications). The Market Size and Forecasts are Provided in Terms of Production Volume (Tons).

List of Companies Covered in this Report:

- PT Bumi Resources Tbk

- PT Adaro Energy Indonesia Tbk

- PT Bayan Resources Tbk

- PT Bukit Asam Tbk

- PT Indo Tambangraya Megah Tbk

- PT Kaltim Prima Coal

- PT Arutmin Indonesia

- PT Kideco Jaya Agung

- PT Berau Coal Energy Tbk

- PT Indika Energy Tbk

- Golden Energy & Resources Ltd

- BlackGold Natural Resources

- PT Bhakti Energi Persada

- PT Bayan International

- PT Multi Harapan Utama

- Adani Indonesia (Adaro JV)

- Glencore (PT Balangan Coal)

- PT Petrosea Tbk

- PT Delta Dunia Makmur Tbk

- PT Resource Alam Indonesia Tbk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prolonged PLN-led baseload demand for low-CV thermal coal

- 4.2.2 Surge in coal-fired captive power for nickel & EV-battery smelters

- 4.2.3 China-plus-One strategy shifting seaborne demand to Indonesia

- 4.2.4 Government "Gasification & DME" incentives for low-rank coal

- 4.2.5 CCUS pilots unlocking high-CV export premiums

- 4.3 Market Restraints

- 4.3.1 Mandatory Domestic Market Obligation (DMO) price caps

- 4.3.2 Accelerated coal-plant retirement under JETP funding

- 4.3.3 Provincial moratoria on new mining permits (Kalimantan, Sumatra)

- 4.3.4 Rising ESG-driven trade financing costs for Indonesian coal

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Coal Grade

- 5.1.1 Lignite/Low-Rank

- 5.1.2 Sub-bituminous

- 5.1.3 Bituminous and Coking

- 5.2 By Application

- 5.2.1 Power Generation

- 5.2.2 Iron, Steel, and Metallurgy

- 5.2.3 Cement and Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PT Bumi Resources Tbk

- 6.4.2 PT Adaro Energy Indonesia Tbk

- 6.4.3 PT Bayan Resources Tbk

- 6.4.4 PT Bukit Asam Tbk

- 6.4.5 PT Indo Tambangraya Megah Tbk

- 6.4.6 PT Kaltim Prima Coal

- 6.4.7 PT Arutmin Indonesia

- 6.4.8 PT Kideco Jaya Agung

- 6.4.9 PT Berau Coal Energy Tbk

- 6.4.10 PT Indika Energy Tbk

- 6.4.11 Golden Energy & Resources Ltd

- 6.4.12 BlackGold Natural Resources

- 6.4.13 PT Bhakti Energi Persada

- 6.4.14 PT Bayan International

- 6.4.15 PT Multi Harapan Utama

- 6.4.16 Adani Indonesia (Adaro JV)

- 6.4.17 Glencore (PT Balangan Coal)

- 6.4.18 PT Petrosea Tbk

- 6.4.19 PT Delta Dunia Makmur Tbk

- 6.4.20 PT Resource Alam Indonesia Tbk

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

煤炭市場:2026-2032年全球市場預測(依煤炭類型、產品類型、品質、採礦技術及最終用途產業分類)煤炭自燃抑制劑市場:依化學類型、形態、應用方法、應用階段和最終用戶分類-全球預測,2026-2032年

煤炭市場:2026-2032年全球市場預測(依煤炭類型、產品類型、品質、採礦技術及最終用途產業分類)煤炭自燃抑制劑市場:依化學類型、形態、應用方法、應用階段和最終用戶分類-全球預測,2026-2032年 動力煤市場規模、佔有率和成長分析:按熱值、揮發分餾、工業應用、區域和產業預測,2026-2033年

動力煤市場規模、佔有率和成長分析:按熱值、揮發分餾、工業應用、區域和產業預測,2026-2033年 2026-2030年全球金屬提煉煉焦市場

2026-2030年全球金屬提煉煉焦市場 煤炭市場分析及預測(至2035年):類型、產品類型、應用、技術、最終用戶、形態、製程、安裝類型、設備、解決方案

煤炭市場分析及預測(至2035年):類型、產品類型、應用、技術、最終用戶、形態、製程、安裝類型、設備、解決方案 2026年全球煤炭、褐煤和無菸煤市場報告2026年全球煤炭市場報告2026年全球白炭市場報告2026年全球冶金煤市場報告煤水煤漿添加劑市場按類型、應用、最終用戶和銷售管道,全球預測(2026-2032年)

2026年全球煤炭、褐煤和無菸煤市場報告2026年全球煤炭市場報告2026年全球白炭市場報告2026年全球冶金煤市場報告煤水煤漿添加劑市場按類型、應用、最終用戶和銷售管道,全球預測(2026-2032年)