|

市場調查報告書

商品編碼

1910926

歐洲大樓自動化系統市場-佔有率分析、產業趨勢、統計數據和成長預測(2026-2031年)Europe Building Automation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

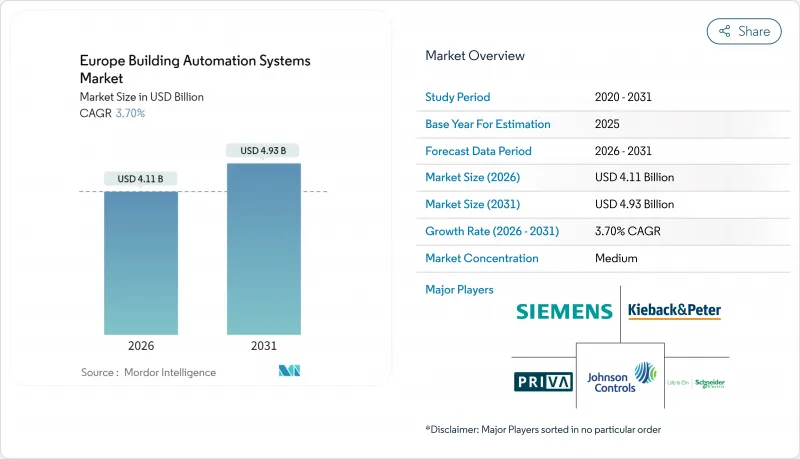

預計到 2025 年,歐洲大樓自動化系統市場規模將達到 39.6 億美元,到 2026 年將成長至 41.1 億美元,到 2031 年將成長至 49.3 億美元,預測期(2026-2031 年)的複合年成長率為 3.70%。

修訂後的《建築能源性能指令》提高了合規要求,電費上漲,以及企業淨零排放目標,正在推動大部分投資決策。該地區四分之三的建築建於1990年以前,因此維修需求佔據主導地位,而創新則集中在雲端分析、無線感測器和人工智慧驅動的最佳化方面。硬體仍然是收入的基礎,但軟體即服務 (SaaS) 可以提供持續的收入來源,並加快中型房地產投資組合的投資回收期。競爭程度適中:雖然少數全球製造商提供核心控制器和現場設備,但數百家區域整合商決定交付時間、計劃成本和使用者培訓效果。持續的勞動力短缺和網路安全風險在短期內會阻礙計劃進展,但產品標準化和生態系統夥伴關係正在逐步降低風險認知。

歐洲大樓自動化系統市場趨勢與洞察

根據EPBD修正案,BACS是強制性的

修訂後的《能源性能指令》(EPBD)將於2025年生效,屆時,暖氣負載超過290千瓦的非住宅建築必須採用可互通的自動化和控制系統。德國和法國已採用更嚴格的標準,這刺激了政府機關、學校和醫療機構的競標活動。 BACnet和KNX等開放通訊協定解決方案受到補貼計畫的青睞,鼓勵建築業主在計畫維修更換專有網路。合規期限集中在2027年左右,這將導致工程需求出現顯著高峰,並刺激專業培訓舉措。雖然各成員國的執行力度有所不同,但總體而言,該指令已為歐洲大樓自動化系統市場的監管時間表預留了成長空間。擁有本地安裝合作夥伴和多語言試運行軟體的供應商具有明顯的競爭優勢。

無線感測器價格暴跌

2023年至2025年間,多技術佔用、溫度和光照感測器的平均售價下降了約30%。這主要歸功於東亞地區200毫米晶圓產量的增加以及向系統晶片(SoC)架構的轉變。北歐的業主率先採用者,利用電池供電的感測器在漫長的供暖季期間監控高能耗設施。佈線和天花板鑽孔成本的降低縮短了小規模計劃的投資回收期,並將基本客群擴展到甲級辦公室以外的領域。新晶片內建的邊緣處理功能可降低延遲、篩檢誤報並現場保存敏感的建築佔用數據,有助於符合GDPR的要求。雖然組件價格的波動性低於2021-2022年供應緊張時期,但專用射頻微控制器的間歇性短缺仍導致整合商的前置作業時間週期略有延長。

現有建築存量零散。

巴黎、羅馬和巴塞隆納等城市的歷史悠久的石砌建築通常限制了岩芯鑽探和大規模管道安裝,這使得感測器安裝和佈線變得複雜。不同時期的機械設備,從散熱器到可變風量箱,都需要精心設計的介面,從而增加了設計時間和應急預算。業主有時會將先進的自動化系統推遲到租戶發生大規模變更時才進行,這使得決策週期超出了傳統的財政年度。當地工匠協會對保護標準的嚴格執行限制了侵入式維修。因此,系統整合商投資於符合歷史建築規範的無線、無電池致動器和可逆安裝套件。然而,這些專用組件價格昂貴,並且會縮短投資回報期。

細分市場分析

到2025年,硬體將佔總收入的65.58%,可靠的控制器、致動器和多標準閘道將支援歐洲大樓自動化系統市場的所有功能層。控制器通常需要管理數千個I/O點,這迫使供應商在即時處理和增強網路安全方面不斷進步。同時,感測器正在向超低功耗無線晶片遷移,擴大了1910年以前建造的、電纜配線架稀少的建築的維修可能性。

基於雲端的分析服務和遠端韌體更新推動了SaaS訂閱市場6.02%的複合年成長率。建築業主優先考慮營運支出而非資本支出,並定期購買基於人工智慧的最佳化功能。可預測的收費結構有助於預算規劃,並鼓勵持續的功能增強。一旦建築的暖通空調系統上線,照明、安防和電動車充電模組也會迅速跟進。供應商正在將邊緣人工智慧推理功能整合到房間控制器中,從而減輕超大規模資料中心的運算負載,並確保符合當地的資料主權法律。

到2025年,在強制性能源審核和激烈競爭的推動下,商業建築將佔歐洲大樓自動化系統市場的44.92%。設施管理人員正優先考慮熱舒適度和室內空氣品質儀表板,以吸引混合辦公環境中的員工;醫院正在升級關鍵區域以實現負壓控制;零售業正在部署基於人工智慧的製冷監控系統以減少食物浪費。

到2031年,受智慧電錶安裝補貼和國家電氣化推廣措施的推動,住宅需求將以5.59%的複合年成長率成長。多用戶住宅將採用集中式系統控制系統來精準分配水電費,而語音控制場景和需量反應Widgets將在獨棟住宅中普及。雖然每戶的安裝點數量較少,但家庭整體安裝規模與小規模商業設施相當,這促使家電製造商與傳統建築自動化系統(BAS)供應商合作。

歐洲大樓自動化系統報告按組件(硬體:控制器和現場設備、SaaS 軟體)、最終用戶(住宅、商業、工業)、建築生命週期(新建、維修)、通訊協定(BACnet、KNX Classic 和 IoT、Modbus/LonWorks)以及地區進行細分。市場預測以美元 (USD) 為以金額為準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 根據修訂後的能源性能指令(EPBD),BACS成為強制性要求。

- 無線感測器價格大幅下降

- 企業淨零排放目標

- 邊緣人工智慧分析對降低營運成本的影響

- 智慧家庭維修的興起

- 與環境、社會及公司治理(ESG)相關的金融獎勵

- 市場限制

- 分散的現有建築存量

- 網路安全責任問題

- 由於供應商特定通訊協定而導致的鎖定

- 技術純熟勞工短缺

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 控制器

- 現場設備

- 軟體即服務 (SaaS)

- 硬體

- 最終用戶

- 住宅

- 商業的

- 工業的

- 透過建構生命週期

- 新建工程

- 維修

- 透過通訊協定

- BACnet

- KNX(經典版和物聯網版)

- Modbus/LonWorks

- 按地區

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 比利時

- 瑞典

- 芬蘭

- 丹麥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens AG

- Johnson Controls International plc

- Schneider Electric SE

- Honeywell International Inc.

- ABB Ltd

- Robert Bosch GmbH

- Trane Technologies plc

- Kieback and Peter GmbH and Co. KG

- Priva Holding BV

- Belimo Holding AG

- Fr. Sauter AG

- Lynxspring Inc.

- Delta Controls Inc.

- Legrand SA

- Distech Controls Inc.

- Regin AB

- Danfoss A/S

- Beckhoff Automation GmbH and Co. KG

- Somfy SA

- Crestron Electronics Inc.

第7章 市場機會與未來展望

The Europe Building Automation Systems market was valued at USD 3.96 billion in 2025 and estimated to grow from USD 4.11 billion in 2026 to reach USD 4.93 billion by 2031, at a CAGR of 3.70% during the forecast period (2026-2031).

Growing compliance obligations under the revised Energy Performance of Buildings Directive, rising electricity prices, and corporate net-zero targets guide most investment decisions. Retrofit opportunities dominate because three-quarters of the region's building stock predates 1990, yet innovation centers on cloud-enabled analytics, wireless sensors, and AI-driven optimization. Hardware remains the revenue anchor while Software-as-a-Service introduces recurring income streams and shortens payback periods for mid-sized property portfolios. Competition is moderate: a handful of global manufacturers supply core controllers and field devices, but hundreds of regional integrators shape delivery schedules, project costs, and user training outcomes. Persistent labour bottlenecks and cybersecurity liabilities act as near-term brakes on project velocity, although product standardization and ecosystem partnerships are gradually reducing risk perceptions.

Europe Building Automation Systems Market Trends and Insights

Mandatory BACS in EPBD revision

The 2025 enforcement of the revised Energy Performance of Buildings Directive obliges non-residential facilities above 290 kW heating load to deploy interoperable automation and control systems. Germany and France adopted even stricter thresholds, accelerating tender activity across public offices, schools, and healthcare sites. Open-protocol solutions such as BACnet and KNX receive preferential treatment in grant programs, prompting building owners to replace proprietary networks during planned renovations. Compliance deadlines cluster around 2027, creating pronounced peaks in engineering demand and sparking specialized training initiatives. Enforcement rigor differs by member state, yet the overall mandate locks Europe Building Automation Systems market growth into regulatory timetables. Vendors with local installation partners and multilingual commissioning software gain a visible competitive edge.

Rapid fall in wireless sensor prices

Average selling prices of multi-technology occupancy, temperature, and light sensors dropped by nearly 30% between 2023 and 2025, mainly because of higher 200 mm wafer output in East Asia and a transition to system-on-chip architectures. Nordic property owners were early adopters, using battery-powered sensors to monitor energy-intensive facilities during prolonged heating seasons. Reduced wiring and ceiling core-drilling costs shorten payback periods on small projects, broadening the customer base beyond A-grade office towers. Edge-processing features embedded inside new chips lower latency, screen false positives, and retain sensitive building usage data inside the premises, supporting GDPR compliance. Although component prices are now less volatile than during the 2021-2022 supply crunch, occasional shortages of specialized RF microcontrollers still trigger modest lead-time spikes for integrators.

Fragmented legacy building stock

Historic masonry structures in Paris, Rome, and Barcelona often prohibit core drilling or heavy conduit runs, complicating sensor placement and cabling. Mixed-era mechanical plant - from radiators to variable-air-volume boxes - requires meticulous interface mapping, elevating engineering hours and contingency budgets. Owners sometimes postpone deep automation until major tenancy turnovers, prolonging decision cycles beyond conventional fiscal years. Regional craft guilds enforce preservation norms, curbing invasive retrofits. Consequently, integrators invest in wireless, battery-free actuators and reversible mounting kits that comply with heritage guidelines, yet these specialized components carry price premiums that shrink return-on-investment windows.

Other drivers and restraints analyzed in the detailed report include:

- Corporate net-zero commitments

- Edge-AI analytics boosting OPEX savings

- Cyber-security liability concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 65.58% of 2025 revenue as reliable controllers, actuators, and multi-standard gateways underpin every functional layer of the Europe Building Automation Systems market size. Controllers routinely manage thousands of I/O points, pushing suppliers to refine real-time processing and cyber-hardening. In parallel, sensors migrate to ultra-low-power wireless chips, broadening retrofit feasibility inside pre-1910 buildings where cable trays are scarce.

Cloud-hosted analytics and remote firmware updates explain the 6.02% CAGR in SaaS subscriptions. Building owners favour operating expenses over capital outlays, purchasing AI-based optimization features on rolling contracts. Predictable billing eases budget planning and encourages continuous scope expansion, once a building's HVAC loops are online, lighting, security, and EV-charger modules follow swiftly. Vendors integrate edge-AI inference capabilities into room controllers, shifting computation away from hyperscale data centers and satisfying regional data-sovereignty laws.

Commercial premises held 44.92% of Europe Building Automation Systems market share in 2025, spurred by mandatory energy audits and competitive tenant landscapes. Facility managers prioritize thermal comfort and indoor-air-quality dashboards to attract occupants in hybrid-work environments. Hospitals upgrade critical zones for negative pressure control, whereas the retail sector deploys AI-based refrigeration monitoring to reduce spoilage.

Residential demand grows at a 5.59% CAGR through 2031, catalysed by smart-meter rebates and national electrification incentives. Multi-family dwellings adopt centralized plant control to allocate utility costs precisely, while detached homes lean toward voice-activated scenes and utility-driven demand-response widgets. Despite fewer per-unit points, aggregate household volumes rival small commercial footprints, prompting consumer-electronics brands to forge alliances with traditional BAS suppliers.

The Europe Building Automation Systems Report is Segmented by Component (Hardware - Controllers and Field Devices, Software-As-A-Service), End User (Residential, Commercial, Industrial), Building Life-Cycle (New-Build, Retrofit), Communication Protocol (BACnet, KNX Classic and IoT, Modbus/LonWorks), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens AG

- Johnson Controls International plc

- Schneider Electric SE

- Honeywell International Inc.

- ABB Ltd

- Robert Bosch GmbH

- Trane Technologies plc

- Kieback and Peter GmbH and Co. KG

- Priva Holding B.V.

- Belimo Holding AG

- Fr. Sauter AG

- Lynxspring Inc.

- Delta Controls Inc.

- Legrand SA

- Distech Controls Inc.

- Regin AB

- Danfoss A/S

- Beckhoff Automation GmbH and Co. KG

- Somfy SA

- Crestron Electronics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory BACS in EPBD revision

- 4.2.2 Rapid fall in wireless sensor prices

- 4.2.3 Corporate net-zero commitments

- 4.2.4 Edge-AI analytics boosting OPEX savings

- 4.2.5 Increasing smart-home retrofits

- 4.2.6 ESG-linked financing incentives

- 4.3 Market Restraints

- 4.3.1 Fragmented legacy building stock

- 4.3.2 Cyber-security liability concerns

- 4.3.3 Vendor-specific protocol lock-in

- 4.3.4 Skilled-labour bottlenecks

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Controllers

- 5.1.1.2 Field Devices

- 5.1.2 Software-as-a-Service

- 5.1.1 Hardware

- 5.2 By End User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.3 By Building Life-Cycle

- 5.3.1 New-build

- 5.3.2 Retrofit

- 5.4 By Communication Protocol

- 5.4.1 BACnet

- 5.4.2 KNX (Classic and IoT)

- 5.4.3 Modbus / LonWorks

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 Netherlands

- 5.5.7 Belgium

- 5.5.8 Sweden

- 5.5.9 Finland

- 5.5.10 Denmark

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Johnson Controls International plc

- 6.4.3 Schneider Electric SE

- 6.4.4 Honeywell International Inc.

- 6.4.5 ABB Ltd

- 6.4.6 Robert Bosch GmbH

- 6.4.7 Trane Technologies plc

- 6.4.8 Kieback and Peter GmbH and Co. KG

- 6.4.9 Priva Holding B.V.

- 6.4.10 Belimo Holding AG

- 6.4.11 Fr. Sauter AG

- 6.4.12 Lynxspring Inc.

- 6.4.13 Delta Controls Inc.

- 6.4.14 Legrand SA

- 6.4.15 Distech Controls Inc.

- 6.4.16 Regin AB

- 6.4.17 Danfoss A/S

- 6.4.18 Beckhoff Automation GmbH and Co. KG

- 6.4.19 Somfy SA

- 6.4.20 Crestron Electronics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球商業建築市場報告2026年全球大樓自動化系統市場報告2026年全球建築自動化與控制系統市場報告

2026年全球商業建築市場報告2026年全球大樓自動化系統市場報告2026年全球建築自動化與控制系統市場報告 大樓自動化系統市場:按組件、系統類型、技術、解決方案類型、部署模式、建築類型和最終用途分類-2026-2032年全球市場預測商業建築市場:2026-2032年全球市場預測(依類型、建築風格、建築系統、建築規模及所有權狀況分類)

大樓自動化系統市場:按組件、系統類型、技術、解決方案類型、部署模式、建築類型和最終用途分類-2026-2032年全球市場預測商業建築市場:2026-2032年全球市場預測(依類型、建築風格、建築系統、建築規模及所有權狀況分類) KNX產品全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)建築自動化軟體市場:按組件類型、最終用戶類型、應用和部署模式分類-2026-2032年全球市場預測智慧建築自動化技術市場:按組件、連接方式、應用和最終用戶分類-2026-2032年全球預測2026年全球智慧建築自動化技術市場報告

KNX產品全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)建築自動化軟體市場:按組件類型、最終用戶類型、應用和部署模式分類-2026-2032年全球市場預測智慧建築自動化技術市場:按組件、連接方式、應用和最終用戶分類-2026-2032年全球預測2026年全球智慧建築自動化技術市場報告 2026-2030年全球建築自動化與控制系統市場

2026-2030年全球建築自動化與控制系統市場