|

市場調查報告書

商品編碼

1910904

北美貨櫃型資料中心市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Containerized Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

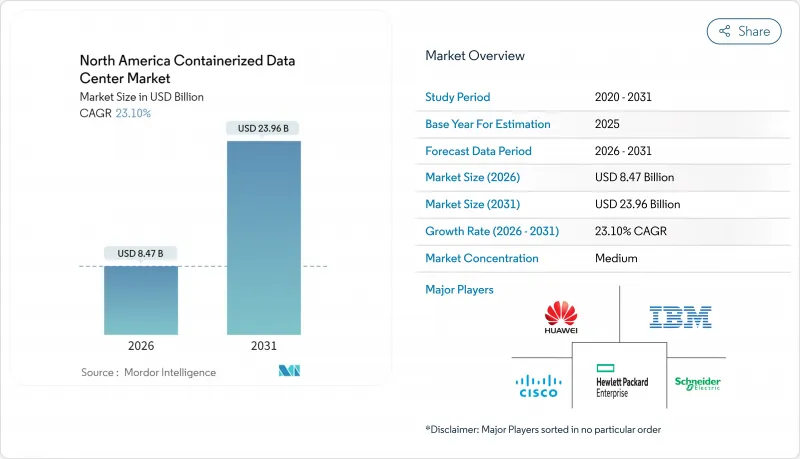

預計到 2025 年,北美貨櫃型資料中心市場價值將達到 68.8 億美元,到 2026 年將成長至 84.7 億美元,到 2031 年將成長至 239.6 億美元,在預測期(2026-2031 年)內複合年成長率為 23.10%。

5G 的推出和人工智慧工作負載的激增正在加速企業採用 5G 技術,因為企業需要將運算資源部署得更靠近使用者。

面對電網限制,超大規模資料中心業者正在對其設施進行改造,採用模組化單元,這些單元可在 12-14 週內運作,而傳統建設方式則需要 18-24 個月。相關的宏觀因素包括:試驗計畫將小型模組化反應器與預製艙結合,以提高離網運作的可靠性;以及國防領域對戰場人工智慧能力日益成長的需求。隨著機架密度超過 40kW,掌握液冷技術和預製電源模組的供應商有望抓住下一波成長。

北美貨櫃型資料中心市場趨勢與洞察

快速部署和擴充性的需求

隨著數位轉型週期的縮短,企業優先考慮可在 12 至 14 週內部署的解決方案,遠比新建資料中心所需的時間短得多。 IBM 的可攜式模組化資料中心展示了承包機櫃如何滿足偏遠內陸地區(施工人員和核准流程往往是瓶頸)的擴展需求。電信業者在網路邊緣也採用了類似的策略,使用標準化模組建構區域 5G 樞紐,從而避免因長期租賃而佔用大量資金。伊頓等供應商正在銷售具有整合電源和行內冷卻的預製機架,從而縮短中端市場買家的安裝週期。這種速度優勢對於需要滿足人工智慧推理需求不可預測激增的雲端服務供應商同樣至關重要。總而言之,快速部署的趨勢正在放大先發優勢,並取代速度較慢、更為傳統的建設方案。

節能型資料中心的需求日益成長

到2024年,冷卻將占美國資料中心電力消耗量的約40%,這將導致營運成本上升,並引發對永續性的更多關注。貨櫃式架構透過整合緊密耦合的氣流路徑和工廠預裝的直接作用於晶片表面的液冷系統,減輕了這一負擔。微軟在模組化機櫃中試點應用了直接作用於晶片的冷卻迴路,與傳統設施相比,實現了更高的機架密度和更低的PUE指標。分散式部署使營運商能夠將資料中心單元部署在再生能源來源附近,從而降低碳排放強度。 GE Vernova的RESTORE直流模組電池系統符合相同的ISO標準,可實現混合儲能,以緩解可再生能源的波動性。不斷上漲的電費和日益嚴格的ESG(環境、社會和治理)要求正在推動對設計中就具備高效性的模組化平台的需求。

機架密度及GPU工作負載有限

生成式人工智慧訓練叢集通常每個機架需要 40-60kW 的功率,但許多容器化設計卻被限制在 30kW 左右。戴爾科技已獲得 2025 年第一季價值 121 億美元的人工智慧伺服器訂單,凸顯了遠超過當前模組化規格的高運算需求。需要連續 GPU 架構的客戶仍然傾向於選擇配備冷卻風道和母線槽的專用設施來處理高密度負載。 NVIDIA 的 Blackwell 平台基於液冷技術,其散熱能力超出了現有 ISO 標準外殼的承載能力,且無需重新設計,這進一步加劇了這一限制。因此,預計企業將在未來兩年內平衡模組化部署的整體速度,將資源分配到用於邊緣推理的快速部署模組和用於模型訓練的集中式設施之間。

細分市場分析

由於其卓越的運算密度和與國際運輸物流的兼容性,40英尺ISO標準貨櫃預計在2025年將保持51.45%的市場佔有率。其主導地位反映了超超大規模資料中心業者資料中心和大型企業核心資料中心轉型升級的趨勢。同時,隨著通訊業者在基地台園區和都市區屋頂等空間受限的場所部署微型邊緣節點,預計到2031年,20英尺ISO標準的替代方案將以19.12%的複合年成長率成長。隨著通訊業者競相提高5G覆蓋密度,20英尺貨櫃型資料中心市場預計將快速擴張。較小的面積降低了場地準備成本,簡化了核准流程,使通訊業者能夠快速實現服務差異化。此外,40英尺以上的客製化機殼主要面向政府和能源計劃,這些項目需要高功率電源和射頻屏蔽,但運輸限制阻礙了其普及。

需求兩極化的趨勢日益明顯:大型 ISO 標準滿足雲端服務供應商不斷成長的核心到邊緣運算需求,而超緊湊型機箱則支援零售、製造和智慧城市部署中的即時數據管道。日立系統於 2025 年 5 月對其產品線進行了更新,推出了三個標準 SKU,分別涵蓋人工智慧推理、伺服器機房替代和通訊邊緣應用場景。這表明供應商已經意識到「一刀切」的時代已經結束。Delta在 CEATEC 展會上展出的 20 英尺機殼整合了 800G 乙太網路和 1.5MW 液冷技術,證明在更緊湊的空間內也能實現高性能。因此,性價比將取決於供應商如何在符合 ISO 標準的前提下,有效地封裝高密度計算資源。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速部署和擴充性的需求

- 節能型資料中心的需求日益成長

- 邊緣運算和5G流量爆炸

- 超大規模資料中心業者在電力限制下增加容量

- 將小型模組化反應器整合到容器中

- 用於戰場和災難救援的移動式人工智慧艙

- 市場限制

- 機架密度有限與GPU工作負載挑戰

- 緊湊外形規格中的溫度控管挑戰

- 城市規劃法規/消防安全標準對層壓模組的阻礙

- 預製電力模組供應鏈瓶頸

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按容器尺寸

- 20英尺 ISO

- 40英尺 ISO

- 超過 40 英尺的客製化

- 透過配置模組

- IT模組

- 電源

- 冷卻模組

- 監控和管理模組

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 政府/國防

- 醫學與生命科學

- 能源與公共產業

- 其他最終用戶

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市佔率分析

- 公司簡介

- Hewlett Packard Enterprise

- IBM Corporation

- Dell Technologies

- Cisco Systems

- Huawei Technologies

- Schneider Electric(SE+AST Modular)

- Vertiv Group

- Rittal GmbH & Co. KG

- Eaton Corporation

- Delta Electronics

- CommScope

- BMarko Structures

- PCX Corporation

- Compass Quantum

- Vapor IO

- EdgeMicro

- Cannon Technologies

- BladeRoom Group

- ZTE Corporation

- Colt Data Centre Services

- Kstar

- Eltek

- Zella DC

- Stack Infrastructure

第7章 市場機會與未來展望

The North America containerized data center market was valued at USD 6.88 billion in 2025 and estimated to grow from USD 8.47 billion in 2026 to reach USD 23.96 billion by 2031, at a CAGR of 23.10% during the forecast period (2026-2031).

Accelerated uptake comes from enterprises that must position computing resources closer to users as 5G rollouts and artificial intelligence workloads surge.

Hyperscalers facing power-grid constraints are supplementing their brick-and-mortar footprints with modular units that can be commissioned in 12-14 weeks instead of the 18-24 months typical of conventional builds. Allied macro factors include pilot programs that pair small modular reactors with prefabricated pods to achieve off-grid resilience, as well as rising defense demand for battlefield AI capability. Vendors that master liquid cooling and prefabricated power modules are positioned to capture the next wave of growth as rack densities push past 40 kW.

North America Containerized Data Center Market Trends and Insights

Need for rapid deployment and scalability

Enterprises confronted by compressed digital-transformation timelines are prioritizing solutions that can be deployed in 12-14 weeks, well inside the window required for green-field facilities. IBM's Portable Modular Data Center illustrates how turnkey enclosures satisfy remote or land-locked expansion scenarios where construction crews and permits create bottlenecks Telecommunications carriers employ similar logic at the network edge, using standardized pods to seed regional 5G hubs without tying up capital in long-term leases. Suppliers such as Eaton now sell off-the-shelf racks with integrated power and in-row cooling, shortening installation cycles for mid-market buyers. The speed advantage is equally important to cloud providers that need to address unpredictable spikes in AI inference demand. Taken together, the rapid-deployment driver amplifies first-mover advantages and displaces slower, stick-built alternatives.

Rising demand for energy-efficient data centers

Cooling consumed close to 40% of U.S. data center electricity in 2024, resulting in elevated operating expenses and sustainability scrutiny. Containerized architectures mitigate the load by integrating tightly coupled airflow channels and factory-installed liquid cooling that reaches chip surfaces directly. Microsoft has piloted direct-to-chip coolant loops inside modular enclosures, achieving higher rack densities at lower PUE metrics than legacy halls . Distributed footprints also allow operators to drop pods alongside renewable sources, improving carbon-intensity scores. GE Vernova's RESTORE DC Block battery system is delivered in the same ISO form factor, enabling hybrid energy storage that smooths renewable intermittency. Rising electricity tariffs and ESG mandates therefore push buyers toward modular platforms that embed efficiency by design.

Limited rack density vs GPU workloads

Generative AI training clusters often demand 40-60 kW per rack, yet many containerized designs cap out at roughly 30 kW. Dell Technologies booked USD 12.1 billion in AI-server orders in Q1 2025, highlighting compute appetites that overshoot current modular envelopes Customers that need contiguous GPU fabrics still gravitate toward purpose-built halls where cooling plenums and busways handle dense loads. Nvidia's Blackwell platform compounds the constraint by specifying liquid-cooling baselines that exceed what most ISO shells can accommodate without redesign. Enterprises therefore split estates between quick-turn pods for edge inference and centralized facilities for model training, moderating overall modular uptake during the next two years.

Other drivers and restraints analyzed in the detailed report include:

- Edge computing and 5G traffic explosion

- Hyperscale capacity additions amid power constraints

- Thermal management challenges in compact form factor

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 40-foot ISO format retained 51.45% of 2025 revenue owing to superior compute density and compatibility with global shipping logistics. Its dominance reflects the core data center conversion trend among hyperscalers and large enterprises. The 20-foot ISO alternative, however, is forecast to register a 19.12% CAGR through 2031 as operators push micro-edge nodes into space-constrained sites such as cell-tower grounds and urban rooftops. The containerized data center market size for 20-foot units is projected to climb sharply as telecoms race to densify 5G coverage. Smaller footprints lower site-prep costs and simplify permitting, giving carriers a fast path to service differentiation. Conversely, custom enclosures exceeding 40 feet cater to government and energy projects where oversized power gear or RF shielding is mandatory, though transport limitations hinder mainstream adoption.

Demand bifurcation is becoming clearer: large ISO formats satisfy core-to-edge spillover for cloud providers, while ultra-compact pods serve real-time data pipelines in retail, manufacturing and smart-city rollouts. Hitachi Systems refreshed its range in May 2025 with three standard SKUs, each covering AI inference, server-room replacement and telco edge use cases, signaling vendor acknowledgment that one size no longer fits all. Delta's 20-foot design shown at CEATEC integrates 800 G Ethernet and 1.5 MW of liquid cooling, proving high performance is achievable even in tighter volumes. Price-performance ratios therefore hinge on how deftly suppliers package dense compute while adhering to ISO standards.

The North America Containerized Data Center Market Report is Segmented by Container Size (20-Foot ISO, 40-Foot ISO, Greater Than 40-Foot Custom), Component Module (IT Module, Power Module, Cooling Module, Monitoring and Management Module), End-User Industry (IT and Telecommunications, BFSI, Government and Defense, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Hewlett Packard Enterprise

- IBM Corporation

- Dell Technologies

- Cisco Systems

- Huawei Technologies

- Schneider Electric (SE + AST Modular)

- Vertiv Group

- Rittal GmbH & Co. KG

- Eaton Corporation

- Delta Electronics

- CommScope

- BMarko Structures

- PCX Corporation

- Compass Quantum

- Vapor IO

- EdgeMicro

- Cannon Technologies

- BladeRoom Group

- ZTE Corporation

- Colt Data Centre Services

- Kstar

- Eltek

- Zella DC

- Stack Infrastructure

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need for rapid deployment and scalability

- 4.2.2 Rising demand for energy-efficient data centers

- 4.2.3 Edge computing and 5G traffic explosion

- 4.2.4 Hyperscaler capacity additions amid power constraints

- 4.2.5 Integration of small modular reactors with containers

- 4.2.6 Battlefield and disaster-relief mobile AI pods

- 4.3 Market Restraints

- 4.3.1 Limited rack density vs GPU workloads

- 4.3.2 Thermal management challenges in compact form factor

- 4.3.3 Urban zoning / fire-code hurdles for stacked modules

- 4.3.4 Prefab power-module supply-chain bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS

- 5.1 By Container Size

- 5.1.1 20-foot ISO

- 5.1.2 40-foot ISO

- 5.1.3 greater than 40-foot Custom

- 5.2 By Component Module

- 5.2.1 IT Module

- 5.2.2 Power Module

- 5.2.3 Cooling Module

- 5.2.4 Monitoring and Management Module

- 5.3 By End-user Industry

- 5.3.1 IT and Telecommunications

- 5.3.2 BFSI

- 5.3.3 Government and Defense

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Energy and Utilities

- 5.3.6 Other End Users

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Hewlett Packard Enterprise

- 6.2.2 IBM Corporation

- 6.2.3 Dell Technologies

- 6.2.4 Cisco Systems

- 6.2.5 Huawei Technologies

- 6.2.6 Schneider Electric (SE + AST Modular)

- 6.2.7 Vertiv Group

- 6.2.8 Rittal GmbH & Co. KG

- 6.2.9 Eaton Corporation

- 6.2.10 Delta Electronics

- 6.2.11 CommScope

- 6.2.12 BMarko Structures

- 6.2.13 PCX Corporation

- 6.2.14 Compass Quantum

- 6.2.15 Vapor IO

- 6.2.16 EdgeMicro

- 6.2.17 Cannon Technologies

- 6.2.18 BladeRoom Group

- 6.2.19 ZTE Corporation

- 6.2.20 Colt Data Centre Services

- 6.2.21 Kstar

- 6.2.22 Eltek

- 6.2.23 Zella DC

- 6.2.24 Stack Infrastructure

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球戶外微型資料中心機櫃市場報告

2026年全球戶外微型資料中心機櫃市場報告 液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)

液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年) 貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告

貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告 貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類

貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類 貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年

貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年 貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) 全球貨櫃型資料中心市場規模、佔有率、趨勢和成長分析報告(2026-2034)貨櫃型資料中心市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

全球貨櫃型資料中心市場規模、佔有率、趨勢和成長分析報告(2026-2034)貨櫃型資料中心市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測