|

市場調查報告書

商品編碼

1910888

歐洲印刷基板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Printed Circuit Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

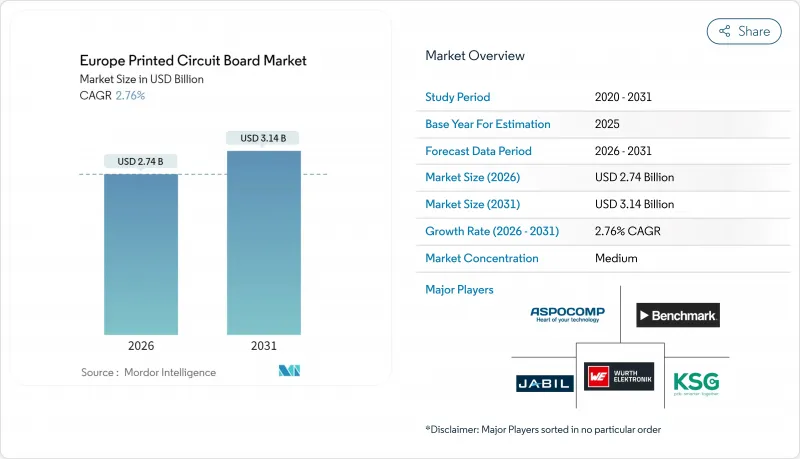

歐洲印刷基板(PCB) 市場規模預計到 2026 年將達到 27.4 億美元,高於 2025 年的 26.7 億美元,預計到 2031 年將達到 31.4 億美元,2026 年至 2031 年的複合年成長率為 2.76%。

這一成長軌跡反映了歐洲PCB市場策略的轉變,即從商品化的大規模生產轉向受監管的高價值細分市場,例如汽車、醫療和工業自動化領域,這些領域支撐著高溢價。歐盟430億歐元(486億美元)的「晶片法案」為歐洲PCB市場提供了經濟獎勵策略,該法案旨在促進對半導體製造廠、先進封裝廠和相關互連供應商的投資。儘管歐洲PCB的產量僅佔全球整體的不到2%,但供應鏈安全、合規性以及與高要求原始設備製造商(OEM)的地理位置接近性仍然是推動區域訂單的主要因素。儘管來自亞洲低成本產品的競爭壓力仍然存在,但歐洲企業正透過其在HDI領域的領先地位、嚴格的品質管理計畫和專業的設計服務來緩解利潤壓力。正如SOMACIS收購醫用級產品以及Cicor創紀錄的訂單訂單所表明的那樣,隨著整合的持續進行,歐洲PCB市場的格局正在日益清晰,剩餘企業正轉向規模化或專業化發展。

歐洲印刷基板市場趨勢與分析

對小型化和高密度互連 (HDI)基板的需求日益成長

對小型化和輕量化的不懈追求迫使原始設備製造商 (OEM) 指定使用 HDI 和 Ultra HDI基板,這使得歐洲 PCB 市場在微孔製造領域佔據了主導地位。目前,區域供應商已具備生產 50微米導體寬度和 75微米以下微孔的資格,從而能夠採用訊號完整性更高的多層堆疊結構來取代傳統的通孔設計。對雷射鑽孔平台、改進的半添加劑處理和 X光檢測的投資為這些能力提供了支持,同時,NCAB 集團和奧地利的專業製造商正在加速推進其工廠運作計劃,目標是在 2025 年前完成。這將使歐洲 PCB 市場透過技術差異化來增強韌性,從而抑制價格競爭。此外,汽車和醫療產業的嚴格標準獎勵那些能夠記錄製程控制和可追溯性的生產商,從而提升 HDI 生產的價值創造。隨著 HDI 技術的應用範圍從德國的汽車產業叢集擴展到荷蘭的工業IoT中心,HDI 需求將繼續成為推動區域收入成長的中期動力。

電動車的快速普及需要先進的汽車印刷電路板

隨著歐洲更嚴格的二氧化碳排放法規將於2025年生效,僅1月份電池式電動車的註冊量就超過25萬輛,年增21%,這推動了每輛車所需複雜多層基板的數量激增。電池管理系統、驅動逆變器和ADAS模組目前均依賴八層或更高層的HDI設計,以滿足IPC-6012汽車標準配件中認證的嚴格振動和熱循環要求。因此,歐洲PCB市場持續收到來自一級供應商的訂單,這些供應商要求在德國、法國和義大利的電動車工廠附近進行在地化生產,以實現即時組裝。電動車細分市場是汽車產業中複合年成長率最高的,預計到2030年仍將是持續的銷售成長推動要素。供應商正利用較長的認證週期和嚴格的缺陷處罰來保護利潤免受進口產品的衝擊,同時也與OEM廠商合作,在有限的電池組尺寸內共同最佳化基板佈局和功率密度。

銅材和層壓板價格的波動給利潤率帶來了壓力。

2024年5月,銅價突破每噸11,000美元,但同年稍後跌破9,000美元。研究預測,在電氣化需求的推動下,銅價將在2025年底回升至每噸1萬美元以上。銅佔原料成本的40%,而原料成本約佔總成本的40%。價格波動直接影響歐洲晶圓廠的息稅折舊攤提前利潤(EBITDA),這些晶圓廠本來就面臨高昂的人事費用和能源成本。在2024年的供應緊張時期,基板供應商還加收了兩位數的附加費,迫使許多基板製造商重新談判年度價格或實施季度調整條款。因此,歐洲PCB市場面臨利潤率波動,這對沒有避險計畫或長期供應協議的中小型企業尤其嚴重。一些公司透過專注於 HDI 原型來降低風險,因為 HDI 原型的材料成本與銷售比率較低;而其他公司則實施動態報價軟體,即時重新計算銅和層壓板指數。

細分市場分析

截至2025年, 基板和基板將佔據歐洲PCB市場佔有率的30.88%,這標誌著汽車ECU和工業控制設備對複雜互連解決方案的需求正在成長。隨著OEM廠商從傳統的通孔設計轉向多層微孔結構,從而縮小晶片面積並提升訊號性能,歐洲HDI應用PCB市場規模將持續穩定成長。軟硬複合基板雖然目前在銷售上佔比不高,但預計到2031年將實現3.13%的複合年成長率,這主要得益於微型醫療設備和汽車雷達線束中對剛性區域間軟性連接的需求。

標準多層基板在對成本高度敏感的工業模組領域仍佔據重要地位,但價格壓力正推動大宗商品生產轉移到亞洲。軟性電路應用於需要生物相容性和滅菌性能的植入式和穿戴式生物感測器,而歐洲的製造地受益於ISO 13485認證。由於低利潤產品的退出,剛性單面或雙面基板的市佔率正在萎縮。整體而言,歐洲PCB市場展現出韌性,這主要得益於對高密度互連(HDI)和軟硬複合的需求,這些需求優先考慮的是接近性、專業化和文件記錄,而非最低成本。

到2025年,汽車產業將佔據歐洲PCB市場佔有率的26.12%,這主要得益於電動車平台的發展,預計到2031年,電動車平台的複合年成長率將達到3.08%。隨著電池管理系統、車載充電器和ADAS單元的整合度不斷提高,並採用耐熱增強型基板,歐洲汽車電子PCB市場規模持續擴大。工業自動化和工業4.0計劃透過在智慧工廠中整合高密度感測器控制器基板,保持適度的個位數成長。

通訊基礎設施的擴張,特別是5G和邊緣資料中心的建設,將推動對多層基板的需求;而航太和國防領域仍將是小規模但價值極高的細分市場,需要嚴格的認證流程。醫療電子領域將受益於基於生物相容性軟式電路板的植入式刺激器和穿戴式診斷設備而成長。家用電子電器仍將是成長最弱的板塊,因為歐洲製造商正逐步放棄大批量生產的通用型行動電話和平板電腦,轉而專注於需要監管認證的專業設備。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對小型化和高密度印刷電路基板(PCB)的需求不斷成長

- 電動車的快速普及需要先進的汽車印刷電路基板

- 歐洲基板製造廠研發投入不斷成長

- 政府對國內半導體和封裝產能的補貼

- 推廣符合REACH標準的無鹵層壓板

- 生物相容性軟性印刷電路板在植入式醫療器材的應用日益廣泛。

- 市場限制

- 銅材和基板價格的波動給利潤率帶來了壓力。

- 下一代HDI生產線資本密集度高

- 由於層壓基板供應集中在亞洲,前置作業時間較長。

- 在整個價值鏈中逐步淘汰 PFAS 的成本

- 宏觀經濟因素的影響

- 產業生態系分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類別

- 標準多層印刷電路基板

- 剛性單面或雙面印刷基板

- HDI/微孔/堆積

- 軟式電路板

- 軟硬複合基板

- 其他類別

- 終端用戶產業

- 工業電子

- 航太與國防

- 家用電子電器

- 溝通

- 車

- 醫療保健

- 其他終端使用者區域

- 按基板

- FR-4

- 金屬核

- 聚醯亞胺

- 陶瓷製品

- 其他印刷基板基板

- 按層數

- 1-2層

- 4-6層

- 8-10層

- 10層或更多層

- 透過組裝方法

- 表面黏著技術

- 通孔技術

- 混合實施

- 按國家/地區

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AT&S Austria Technologie und Systemtechnik AG

- Wurth Elektronik Group

- KSG GmbH

- NCAB Group AB

- Aspocomp Group Plc

- Jabil Inc.

- TTM Technologies Inc.

- Benchmark Electronics Inc.

- ICAPE Group

- Schweizer Electronic AG

- LeitOn GmbH

- MicroCirtec Micro Circuit Technology GmbH

- Becker and Muller Schaltungsdruck GmbH

- Elvia PCB Group

- Cicor Group AG

- Multek Corporation

- MEKTEC Europe GmbH(Nippon Mektron Ltd.)

- Fujikura Ltd.

- Lab Circuits SA

- Exception PCB Ltd.

第7章 市場機會與未來展望

Europe PCB market size in 2026 is estimated at USD 2.74 billion, growing from 2025 value of USD 2.67 billion with 2031 projections showing USD 3.14 billion, growing at 2.76% CAGR over 2026-2031.

This trajectory reflects a strategic pivot away from commoditized volumes toward regulated high-value niches in automotive, medical, and industrial automation that support premium pricing. The Europe PCB market benefits from the European Union's EUR 43 billion (USD 48.6 billion) Chips Act stimulus, which channels investment into semiconductor fabs, advanced packaging hubs, and supporting interconnect suppliers. Supply-chain security, regulatory conformity, and proximity to demanding OEMs continue to reinforce regional orders, even as production represents less than 2% of global output. Competitive stress from low-cost Asian imports persists, yet European companies mitigate margin pressure through HDI leadership, rigorous quality programs, and specialized design services. Consolidation further defines the Europe PCB market, as illustrated by SOMACIS's medical-grade acquisition and Cicor's record intake, signaling a flight to scale or specialization among remaining players.

Europe Printed Circuit Board Market Trends and Insights

Growing Demand for Miniaturisation and High-Density Interconnect PCBs

The relentless push toward smaller, lighter electronic assemblies compels OEMs to specify HDI and ultra-HDI boards, elevating the Europe PCB market to a leadership role in microvia fabrication. Regional suppliers now qualify 50 micrometer conductor widths and microvias below 75 micrometers, enabling multilayer stack-ups that replace older through-hole designs with improved signal integrity. Investments in laser-drilling platforms, modified semi-additive processes, and X-ray inspection underpin these capabilities, with NCAB Group and Austrian specialists accelerating factory-readiness programs throughout 2025. The Europe PCB market thereby gains resilience through technical differentiation that deters price-based competition. In addition, stringent automotive and medical standards reward producers that document process control and traceability, reinforcing value extraction from HDI production. As adoption scales from German automotive clusters to Dutch industrial IoT hubs, HDI demand sustains a mid-term lift on regional revenue growth

Rapid Proliferation of Electric Vehicles Requiring Advanced Automotive PCBs

Tighter 2025 European CO2 thresholds ignited a 21% year-over-year spike in battery-electric vehicle registrations to more than 250,000 units in January alone, translating to a sharp uptick in complex multilayer board content per vehicle. Battery-management systems, traction inverters, and ADAS modules now rely on eight-plus-layer HDI designs with stringent vibration and thermal cycling prescriptions certified under IPC-6012 automotive addenda. Consequently, the Europe PCB market secures recurring orders from tier-one suppliers that mandate regional production for just-in-time assembly near German, French, and Italian EV plants. The electric-vehicle subsegment posts the fastest CAGR within automotive, ensuring a durable volume driver through 2030. Suppliers leverage long qualification cycles and punitive defect penalties to defend margins against imports, while collaborating with OEMs to co-optimize board layout and power-density within constrained pack footprints.

Volatile Copper and Laminate Prices Squeezing Margins

Copper traded above USD 11,000 per metric ton in May 2024 before retreating below USD 9,000 later that year, and research anticipates a rebound past USD 10,000 by late 2025 on electrification demand. Because copper forms 40% of raw-material spend and materials consume about 40% of total cost, swings directly compress EBITDA for European fabs already grappling with elevated labor and energy overheads. Laminate suppliers likewise pushed double-digit surcharges during the 2024 squeeze, compelling many board houses to renegotiate annual pricing or pass through quarterly adjustment clauses. The Europe PCB market therefore confronts margin volatility that disproportionately hurts smaller firms lacking hedging programs or long-term supply contracts. Some mitigate exposure by specializing in HDI prototypes where material share of selling price is lower, while others adopt dynamic quoting software that recalculates copper and laminate indices in real time.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies for On-Shore Semiconductor and Packaging Capacity

- Increasing R and D Investment in European PCB Fabs

- High Capital Intensity of Next-Gen HDI Production Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HDI and micro-via boards accounted for 30.88% of the Europe PCB market share in 2025, underscoring the region's pivot to complex interconnect solutions for automotive ECUs and industrial controls. The Europe PCB market size for HDI applications continues to expand steadily as OEMs convert legacy through-hole designs to multilayer micro-via architectures that shrink footprint and enhance signal performance. Rigid-Flex formats, while only a fraction of volume, achieve a 3.13% CAGR to 2031 as medical device miniaturization and automotive radar harness bendable linkages between rigid zones.

Standard multilayer boards retain relevance in cost-sensitive industrial modules, though price pressure pushes commodity production toward Asia. Flexible circuits serve implantables and wearable biosensors that demand biocompatibility and sterilization compliance, domains where European fabs leverage ISO 13485 accreditation. Rigid 1-2-sided boards erode as producers exit low-margin runs. Overall, the Europe PCB market derives resilience from HDI and Rigid-Flex demand that values proximity, expertise, and documentation over lowest cost.

Automotive accounted for 26.12% of the Europe PCB market share in 2025, buoyed by surging electric-vehicle platforms that register a 3.08% CAGR through 2031. The Europe PCB market size for automotive electronics grows as battery-management systems, on-board chargers, and ADAS units integrate higher layer counts and thermal-enhanced substrates. Industrial automation and Industry 4.0 initiatives sustain mid-single-digit growth by embedding sensor-dense controller boards across smart factories.

Communications build-out, notably 5G and edge-data centers, uplifts multilayer demand, whereas aerospace and defense persist as small yet premium niches with rigorous qualification cycles. Medical electronics expand on the back of implantable stimulators and diagnostic wearables that rely on biocompatible flex boards. Consumer electronics remains the weakest cohort as European players relinquish high-volume commodity handsets and tablets, instead concentrating on specialized equipment demanding regulatory assurance.

The Europe PCB Market Report is Segmented by Category (Standard Multilayer PCBs, Rigid 1-2-Sided PCBs, and More), End-User Vertical (Industrial Electronics, Consumer Electronics, and More), PCB Substrate (FR-4, Metal Core, Polyimide, and More), Layer Count (1-2 Layers, 4-6 Layers, 8-10 Layers, and More), Assembly Type (Surface-Mount Technology, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AT&S Austria Technologie und Systemtechnik AG

- Wurth Elektronik Group

- KSG GmbH

- NCAB Group AB

- Aspocomp Group Plc

- Jabil Inc.

- TTM Technologies Inc.

- Benchmark Electronics Inc.

- ICAPE Group

- Schweizer Electronic AG

- LeitOn GmbH

- MicroCirtec Micro Circuit Technology GmbH

- Becker and Muller Schaltungsdruck GmbH

- Elvia PCB Group

- Cicor Group AG

- Multek Corporation

- MEKTEC Europe GmbH (Nippon Mektron Ltd.)

- Fujikura Ltd.

- Lab Circuits S.A.

- Exception PCB Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Miniaturisation and High-Density Interconnect PCBs

- 4.2.2 Rapid Proliferation of Electric Vehicles Requiring Advanced Automotive PCBs

- 4.2.3 Increasing Research and Development Investment in European PCB Fabs

- 4.2.4 Government Subsidies for On-Shore Semiconductor and Packaging Capacity

- 4.2.5 Regulatory Push For REACH-Compliant Halogen-Free Laminates

- 4.2.6 Surging Adoption of Bio-Compatible Flexible PCBs for Implantable Medical Devices

- 4.3 Market Restraints

- 4.3.1 Volatile Copper and Laminate Prices Squeezing Margins

- 4.3.2 High Capital Intensity of Next-Gen HDI Production Lines

- 4.3.3 Extended Lead Times Due To Asia-Centric Laminate Supply

- 4.3.4 PFAS Phase-Out Compliance Costs Across the Value Chain

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Ecosystem Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Category

- 5.1.1 Standard Multilayer PCBs

- 5.1.2 Rigid 1-2-sided PCBs

- 5.1.3 HDI / Micro-via / Build-up

- 5.1.4 Flexible PCBs

- 5.1.5 Rigid-Flex PCBs

- 5.1.6 Other Categories

- 5.2 By End-User Vertical

- 5.2.1 Industrial Electronics

- 5.2.2 Aerospace and Defense

- 5.2.3 Consumer Electronics

- 5.2.4 Communications

- 5.2.5 Automotive

- 5.2.6 Medical

- 5.2.7 Other End-User Verticals

- 5.3 By PCB Substrate

- 5.3.1 FR-4

- 5.3.2 Metal Core

- 5.3.3 Polyimide

- 5.3.4 Ceramic

- 5.3.5 Other PCB Substrates

- 5.4 By Layer Count

- 5.4.1 1-2 Layers

- 5.4.2 4-6 Layers

- 5.4.3 8-10 Layers

- 5.4.4 more than 10 Layers

- 5.5 By Assembly Type

- 5.5.1 Surface-Mount Technology

- 5.5.2 Through-Hole Technology

- 5.5.3 Mixed Assembly

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AT&S Austria Technologie und Systemtechnik AG

- 6.4.2 Wurth Elektronik Group

- 6.4.3 KSG GmbH

- 6.4.4 NCAB Group AB

- 6.4.5 Aspocomp Group Plc

- 6.4.6 Jabil Inc.

- 6.4.7 TTM Technologies Inc.

- 6.4.8 Benchmark Electronics Inc.

- 6.4.9 ICAPE Group

- 6.4.10 Schweizer Electronic AG

- 6.4.11 LeitOn GmbH

- 6.4.12 MicroCirtec Micro Circuit Technology GmbH

- 6.4.13 Becker and Muller Schaltungsdruck GmbH

- 6.4.14 Elvia PCB Group

- 6.4.15 Cicor Group AG

- 6.4.16 Multek Corporation

- 6.4.17 MEKTEC Europe GmbH (Nippon Mektron Ltd.)

- 6.4.18 Fujikura Ltd.

- 6.4.19 Lab Circuits S.A.

- 6.4.20 Exception PCB Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

類PCB基板:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

類PCB基板:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 印刷基板市場規模、佔有率和成長分析:按產品類型、最終用戶和地區分類-2026-2033年產業預測

印刷基板市場規模、佔有率和成長分析:按產品類型、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球印刷基板(PCB)市場

2026-2030年全球印刷基板(PCB)市場 印刷基板市場:2026-2032年全球市場預測(依類型、基板結構、材料、元件安裝方式、層數、製造流程、應用、終端用戶產業及銷售管道)

印刷基板市場:2026-2032年全球市場預測(依類型、基板結構、材料、元件安裝方式、層數、製造流程、應用、終端用戶產業及銷售管道) AI推理伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年)

AI推理伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年) 印刷基板市場規模、佔有率和趨勢分析報告:按產品類型、基板材料、最終用途、地區和細分市場預測(2026-2033 年)

印刷基板市場規模、佔有率和趨勢分析報告:按產品類型、基板材料、最終用途、地區和細分市場預測(2026-2033 年) 高密度互連(HDI)印刷基板市場:依技術節點、應用與地區分類通用伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年)HDI基板市場:按技術節點、應用和地區分類

高密度互連(HDI)印刷基板市場:依技術節點、應用與地區分類通用伺服器PCB市場報告:趨勢、預測與競爭分析(至2035年)HDI基板市場:按技術節點、應用和地區分類 印刷基板(PCB) 市場預測:至 2034 年-按類型、基板型、應用和地區分類的全球分析

印刷基板(PCB) 市場預測:至 2034 年-按類型、基板型、應用和地區分類的全球分析