|

市場調查報告書

商品編碼

1910827

駕駛模擬器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Driving Simulator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

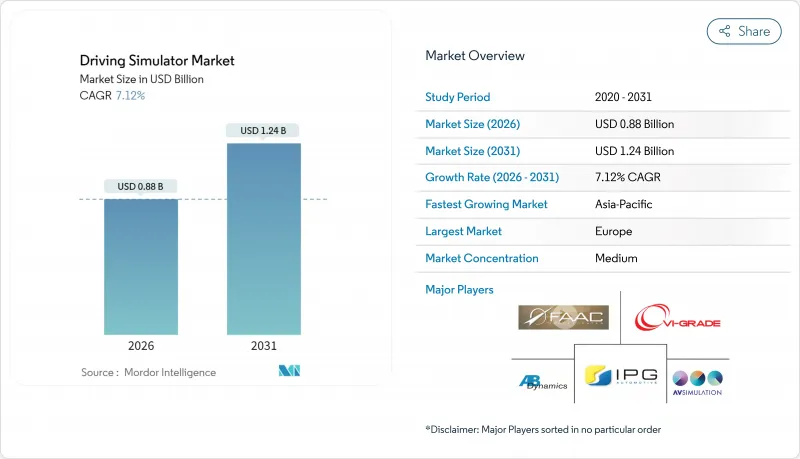

預計到 2025 年,駕駛模擬器市值將達到 8.2 億美元,從 2026 年的 8.8 億美元成長到 2031 年的 12.4 億美元,在預測期(2026-2031 年)內,複合年成長率將達到 7.12%。

這種穩定成長源自於監管機構對更安全駕駛員認證的壓力、降低原型測試成本的需求,以及自動駕駛汽車藍圖與虛擬檢驗要求的契合。商業車隊正在採用先進的模擬器來縮短採用週期,汽車製造商則將研發預算轉向軟體在環測試設備,以補充實際道路測試。訂閱式雲端平台正在擴大成本敏感地區的存取範圍,並培育新的用戶群。歐洲憑藉其成熟的汽車生態系統保持主導地位,而亞太地區則憑藉中國和印度物流網路的擴張,推動了最大的收入成長。如今,競爭優勢正向那些能夠結合數位雙胞胎地圖、空中軟體檢驗和獨立於硬體的運動提示技術的供應商轉移。然而,高昂的初始投資、暈動症風險以及日益成長的網路安全警報正在阻礙小規模採用者。

全球駕駛模擬器市場趨勢與洞察

ADAS/AV檢驗需求快速成長

更嚴格的認證規則要求在自動駕駛功能正式上路前,必須進行數十億英里的虛擬測試。將於2024年發布的Euro NCAP和NHTSA通訊協定,將真實道路測試與仿真相結合,並將高保真測試設備視為符合性認證的關鍵。 IEEE預測,到2030年,自動駕駛模擬市場規模將達到10億美元,凸顯了汽車製造商對數位雙胞胎技術的依賴,他們利用數位孿生技術來探索那些無法在公共道路上檢驗的極端情況。將真實感測器日誌與可擴展場景引擎整合的平台,能夠幫助工程師縮短迭代周期,並減少原型車隊的數量。隨著軟體更新逐漸普及,虛擬回歸測試變得必不可少,這也支撐了駕駛模擬器市場的穩定需求。目前,能夠將場景庫、實體引擎和資料融合介面整合到單一技術堆疊中的供應商,正收到更多來自一級供應商的詢價請求(RFQ)。

電子商務的快速成長正在駕駛人。

線上零售的擴張導致小包裹量激增,貨運能力面臨壓力。 UPS和Fremont Contract Carriers等運輸公司正在教室部署基於動作的模擬器,並報告稱事故減少,新司機入職速度加快。內布拉斯加州卡車運輸協會提供的行動培訓單位透過向偏遠地區的大學提供培訓,緩解了農村地區的人才短缺問題。可重現的危險場景使運輸公司能夠滿足保險審核,並在幾週內完成新司機認證,推動了模擬器的普及。這種商業需求抵消了消費者駕駛員教育計畫成長緩慢的影響,使駕駛模擬器市場在短期內保持兩位數左右的成長。

全動系統需要高資本投入

八軸運動平台、全景圓頂和專用禮堂對許多職業訓練中心來說價格過高。歐洲斯圖加特的駕駛模擬器清楚地展現了此類設施所需的場地和維護成本。資金籌措障礙會延長投資回收期,尤其是在學費受到管制的地區。新興市場的買家往往會推遲購買或選擇靜態駕駛座,這限制了駕駛模擬器市場中高價硬體的銷售成長。

細分市場分析

乘用車模擬器在新手駕駛訓練和OEM研發領域仍將保持主導地位,預計2025年將佔據駕駛模擬器市場59.88%的佔有率。然而,由於消費者駕照考試機構對模擬器替代駕駛設備的限制,預計其成長速度將放緩。不同的應用趨勢表明,物流數位化正在重塑模擬器的需求模式。儘管商用車在2025年的收入基數小規模,但它們將成為未來駕駛模擬器市場擴張的主要驅動力,複合年成長率將達到7.14%。車隊管理人員採用模擬器是為了降低每位駕駛員的培訓成本,保持車輛運轉率,並滿足日益嚴格的駕駛時間監管審核。遠端資訊處理技術的整合進一步將車內駕駛行為與課堂複習培訓連結起來。

商用車需求的成長帶動了周邊服務的發展,例如針對危險品運輸路線的客製化場景庫、多語言使用者介面以及遠端指導站。利用模組化駕駛座和雲端渲染技術的供應商正在開拓先前因價格過高而難以企及的中小型車隊市場。同時,乘用車專案專注於測試下一代資訊娛樂系統的人機介面,這是一個利潤豐厚但市場規模有限的細分市場。開發雙用途架構、可互換儀錶板和可適應性強的軟體堆疊的供應商,在駕駛模擬器市場的各個細分領域保持著柔軟性。

截至2025年,在成熟的培訓課程和企業合規要求的推動下,駕駛員培訓領域佔駕駛模擬器市場規模的50.72%。然而,測試和研究領域7.21%的複合年成長率顯示市場結構正在轉變。汽車製造商為了縮短產品發布週期,正將預算轉向軟體主導的檢驗流程,因為虛擬里程比實際行駛里程更具成本效益。監管機構對實驗室在可控、可重複的環境下進行碰撞避免檢驗的需求也是推動市場成長要素。

培訓需求依然強勁,尤其是在道路擁擠和高油價導致在職訓練效果下降的地區。透過虛擬實境頭盔和自適應人工智慧導師提供的個人化模組有助於提高學員的學習保留率。然而,注重預算的教育機構仍在觀望,暫緩全面更換其傳統設備。供應商透過提供混合用途許可證來分散風險,讓他們在測試自動化腳本和課堂內容之間切換,從而提高駕駛模擬器市場的座位運轉率並實現收入多元化。

區域分析

2025年,歐洲在駕駛模擬器市場將維持36.22%的佔有率,主要得益於密集的測試跑道網路、統一的安全標準以及研發稅收優惠政策。德國、法國和瑞典的汽車製造商正在運作整合的模擬流程,以支援監管申報並穩定硬體更新周期。各國運輸部正在試行模擬器許可證制度,儘管私人預算波動,公共採購項目仍在繼續。

亞太地區新增駕駛座最多,複合年成長率達7.17%。中國正將智慧城市預算投入自動駕駛班車試點項目,而印度則在擴建卡車駕駛人培訓學院以緩解長期存在的勞動力短缺問題。雲端渲染解決方案正在繞過基礎設施瓶頸,使教育機構能夠在臨時教室部署筆記型電腦控制的駕駛座。日本成熟的汽車產業正致力於開發能夠重現複雜城市路口的場景庫,從而提振駕駛模擬器市場的上游軟體需求。

北美受益於完善的聯邦商業駕駛員資格認證指南,以及航空和國防領域早期採用模擬器的文化。重型貨運公司正在投資建造連接區域樞紐的連網車隊,並利用集中式內容傳送。拉丁美洲和中東仍然是小規模的消費區域,但沿岸地區石油和天然氣運輸車隊營運商日益成長的興趣預示著未來地域擴張的趨勢。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- ADAS/自動駕駛車輛檢驗需求快速成長

- 電子商務的快速成長正在推動對卡車駕駛人培訓的需求。

- 道路安全法規與駕駛執照改革

- 利用基於雲端的「模擬器即服務」減少資本投資

- 針對通過模擬器認證的機隊,提供與保險相關的保費折扣

- 用於OTA軟體回歸的數位雙胞胎整合

- 市場限制

- 全動系統需要高資本投入

- 暈動症和保真度限制

- 劇本內容開發人員短缺

- 網路模擬器的網路安全風險

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 按車輛類型

- 搭乘用車

- 商用車輛

- 透過使用

- 訓練

- 測試和調查

- 依模擬器類型

- 緊湊型模擬器

- 全尺寸模擬器

- 高空模擬器

- 最終用戶

- 駕訓班和訓練中心

- 汽車製造商

- 車隊營運商及物流

- 學術和研究機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AB Dynamics plc

- VI-grade GmbH

- IPG Automotive GmbH

- Ansible Motion Ltd

- Cruden BV

- AutoSim AS

- AVSimulation

- Virage Simulation Inc.

- Tecknotrove Simulator Systems Pvt Ltd

- XPI Simulation

- FAAC Incorporated

- Moog Inc.

- Mechanical Simulation Corp.

- CAE Inc.

- Thales Group

- Bosch Rexroth AG

- Dassault Systemes SE

- Applied Intuition Inc.

- Exail Technologies SA

第7章 市場機會與未來展望

The Driving Simulator Market was valued at USD 0.82 billion in 2025 and estimated to grow from USD 0.88 billion in 2026 to reach USD 1.24 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

This steady rise stems from regulatory pressure for safer driver certification, the need to cut prototype testing costs, and the alignment of autonomous-vehicle roadmaps with virtual validation mandates. Commercial fleets turn to advanced simulators to shorten recruitment cycles, while carmakers channel research budgets toward software-in-the-loop test beds that complement physical tracks. Subscription-based, cloud-hosted platforms broaden access in cost-sensitive regions and nurture new user segments. Europe keeps its lead on account of a mature automotive ecosystem, but Asia-Pacific contributes the largest incremental revenue as China and India expand logistics networks. Competitive advantage now flows to providers that fuse digital-twin maps, over-the-air software verification, and hardware-agnostic motion cueing, although high capital outlays, motion-sickness risks, and rising cyber-security alerts hold back smaller adopters.

Global Driving Simulator Market Trends and Insights

ADAS/AV Validation Needs Surge

Tougher homologation rules now insist on billions of virtual test miles before autonomous functions reach public roads. Euro NCAP and NHTSA protocols released in 2024 pair track runs with simulation, turning high-fidelity rigs into compliance gates. The IEEE forecasts over a billion dollar autonomous-driving simulation niche by 2030, underscoring how carmakers rely on digital twins to probe edge cases unreachable on open roads. Platforms integrating real-world sensor logs with scalable scenario engines let engineers shorten iteration loops and trim prototype fleets. As software updates move over the air, virtual regression testing becomes mandatory, anchoring steady demand for the driving simulator market. Vendors that wrap scenario libraries, physics engines, and data-fusion interfaces into one stack now win more RFQs from tier-1 suppliers.

E-Commerce Boom Raising Truck-Driver Training Demand

Online retail pushes parcel volumes upward, straining freight capacity. Carriers such as UPS and Fremont Contract Carriers equip classrooms with motion-based simulators and report accident reductions alongside faster rookie onboarding. The Nebraska Trucking Association's mobile units bring training to remote colleges, easing the rural talent gap. Repeatable hazard scenarios help fleets meet insurance audits and qualify recruits within weeks, boosting uptake. This commercial pull offsets slower growth in consumer driver-ed programs and keeps the driving simulator market momentum above one-tenth in the short term.

High Capex Of Full-Motion Systems

Eight-axis motion bases, panoramic domes, and purpose-built halls push acquisition costs beyond the reach of many vocational centers. Europe's Stuttgart Driving Simulator illustrates the real-estate and maintenance footprint such rigs require. Financing hurdles prolong payback periods, especially where tuition fees are regulated. Emerging-market buyers often defer purchases or settle for static cockpits, tempering volume growth for premium hardware in the driving simulator market.

Other drivers and restraints analyzed in the detailed report include:

- Road-Safety Regulations & Driver-Licensing Reforms

- Digital-Twin Integration For OTA Software Regression

- Motion-Sickness & Fidelity Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger-car simulators still dominate with 59.88% of the driving simulator market share in 2025, serving both novice driver education and OEM R&D, but growth moderates as consumer licensing boards limit simulator substitution. The divergence in uptake illustrates how logistics digitization reshapes simulator demand patterns. Commercial vehicles accounted for a smaller revenue base in 2025, yet their 7.14% CAGR makes them the primary engine of future expansion for the driving simulator market. Fleet managers deploy simulators to cut per-driver training costs, keep rigs on the road, and satisfy stricter hours-of-service audits. Telematics integration further links in-cab behavior with classroom refreshers.

The commercial-vehicle push stimulates peripheral services scenario library customization for hazmat routes, multi-language UI overlays, and remote instructor stations. Vendors leveraging modular cockpits and cloud rendering penetrate small and mid-sized transport operators previously priced out. Meanwhile, passenger-car programs focus on human-machine interface testing for next-gen infotainment, a niche that commands higher margins but fewer seats. Suppliers that craft dual-purpose architectures, swappable dashboards, and adaptable software stacks retain cross-segment flexibility in the driving simulator market.

Training held 50.72% of the driving simulator market size in 2025 due to entrenched driver-ed curricula and corporate compliance needs. Yet the 7.21% CAGR logged by testing and research signals a structural pivot. Automakers wanting to shorten release cycles channel budgets toward software-dominated validation, where virtual miles are cheaper than track miles. Growth also comes from regulatory labs conducting crash-avoidance verification under controlled, repeatable conditions.

Training demand remains resilient, particularly in regions where road congestion and fuel prices make real-world lessons inefficient. Virtual-reality headsets and adaptive AI tutors personalize modules, boosting learner retention. Still, budget-sensitive schools adopt a wait-and-see stance on replacing entire fleets of conventional cars. Providers hedge by offering mixed-use licenses that toggle between test automation scripts and classroom content, increasing seat utilization and diversifying revenue in the driving simulator market.

The Driving Simulator Market Report is Segmented by Vehicle Type (Passenger Car and Commercial Vehicle), Application (Training and Testing & Research), Simulator Type (Compact Simulator and More), End-User (Driving Schools & Training Centers and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe preserved a 36.22% share of the driving simulator market in 2025 on the strength of its dense testing circuits, harmonized safety rules, and R&D tax incentives. Carmakers in Germany, France, and Sweden run integrated simulation pipelines that feed regulatory dossiers, ensuring a steady hardware refresh cycle. National transport ministries pilot simulator-based licensing updates, keeping public procurement programs alive even as private budgets fluctuate.

Asia-Pacific, advancing at a 7.17% CAGR, adds the most new seats. China funnels smart-city budgets into autonomous shuttle pilots, while India scales truck-driver academies to plug chronic labor gaps. Cloud-rendered solutions bypass infrastructure bottlenecks, letting institutes deploy laptop-controlled cockpits in temporary classrooms. Japan's well-established automotive sector focuses on scenario libraries that represent complex urban intersections, reinforcing upstream software demand in the driving simulator market.

North America benefits from structured federal guidelines covering commercial-driver qualifications and an early culture of simulator adoption in aviation and defense. Large freight haulers invest in networked fleets of rigs across regional hubs, leveraging centralized content pushes. Latin America and the Middle East remain smaller consumers, yet oil-and-gas convoy operators in the Gulf show rising interest, signaling wider geographic penetration ahead.

- AB Dynamics plc

- VI-grade GmbH

- IPG Automotive GmbH

- Ansible Motion Ltd

- Cruden BV

- AutoSim AS

- AVSimulation

- Virage Simulation Inc.

- Tecknotrove Simulator Systems Pvt Ltd

- XPI Simulation

- FAAC Incorporated

- Moog Inc.

- Mechanical Simulation Corp.

- CAE Inc.

- Thales Group

- Bosch Rexroth AG

- Dassault Systemes SE

- Applied Intuition Inc.

- Exail Technologies SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ADAS/AV Validation Needs Surge

- 4.2.2 E-Commerce Boom Raising Truck-Driver Training Demand

- 4.2.3 Road-Safety Regulations & Driver-Licensing Reforms

- 4.2.4 Cloud "Simulator-As-A-Service" Lowering Capex

- 4.2.5 Insurance-Linked Premium Discounts For Simulator-Certified Fleets

- 4.2.6 Digital-Twin Integration For OTA Software Regression

- 4.3 Market Restraints

- 4.3.1 High Capex Of Full-Motion Systems

- 4.3.2 Motion-Sickness & Fidelity Limitations

- 4.3.3 Shortage Of Scenario-Content Developers

- 4.3.4 Cyber-Security Risk In Networked Simulators

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Commercial Vehicle

- 5.2 By Application

- 5.2.1 Training

- 5.2.2 Testing & Research

- 5.3 By Simulator Type

- 5.3.1 Compact Simulator

- 5.3.2 Full-Scale Simulator

- 5.3.3 Advanced Simulator

- 5.4 By End-User

- 5.4.1 Driving Schools & Training Centers

- 5.4.2 Automotive OEMs

- 5.4.3 Fleet Operators & Logistics

- 5.4.4 Academic & Research Institutions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 AB Dynamics plc

- 6.4.2 VI-grade GmbH

- 6.4.3 IPG Automotive GmbH

- 6.4.4 Ansible Motion Ltd

- 6.4.5 Cruden BV

- 6.4.6 AutoSim AS

- 6.4.7 AVSimulation

- 6.4.8 Virage Simulation Inc.

- 6.4.9 Tecknotrove Simulator Systems Pvt Ltd

- 6.4.10 XPI Simulation

- 6.4.11 FAAC Incorporated

- 6.4.12 Moog Inc.

- 6.4.13 Mechanical Simulation Corp.

- 6.4.14 CAE Inc.

- 6.4.15 Thales Group

- 6.4.16 Bosch Rexroth AG

- 6.4.17 Dassault Systemes SE

- 6.4.18 Applied Intuition Inc.

- 6.4.19 Exail Technologies SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽車駕駛模擬器市場:按產品類型、應用和地區分類

汽車駕駛模擬器市場:按產品類型、應用和地區分類 全球汽車駕駛模擬器市場

全球汽車駕駛模擬器市場 駕駛模擬器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、應用類型、模擬器類型、地區和競爭格局分類,2021-2031年

駕駛模擬器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、應用類型、模擬器類型、地區和競爭格局分類,2021-2031年 駕駛模擬器市場:2026-2032年全球市場預測(依模擬器類型、車輛類型、應用、最終用戶和部署模式分類)汽車碰撞衝擊模擬器市場:依模擬類型、衝擊類型、目標零件和車輛類型分類-2026-2032年全球市場預測

駕駛模擬器市場:2026-2032年全球市場預測(依模擬器類型、車輛類型、應用、最終用戶和部署模式分類)汽車碰撞衝擊模擬器市場:依模擬類型、衝擊類型、目標零件和車輛類型分類-2026-2032年全球市場預測 2026年全球駕駛模擬器市場報告衝擊式脫殼機市場依產能、應用、最終用途及通路分類,全球預測(2026-2032年)

2026年全球駕駛模擬器市場報告衝擊式脫殼機市場依產能、應用、最終用途及通路分類,全球預測(2026-2032年) 全球駕駛模擬器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球駕駛模擬器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球汽車碰撞衝擊模擬器(ACIS)市場

2026-2030年全球汽車碰撞衝擊模擬器(ACIS)市場 2025-2029年全球汽車駕駛模擬器市場

2025-2029年全球汽車駕駛模擬器市場