|

市場調查報告書

商品編碼

1910713

聚羥基烷酯(PHA):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Polyhydroxyalkanoate (PHA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

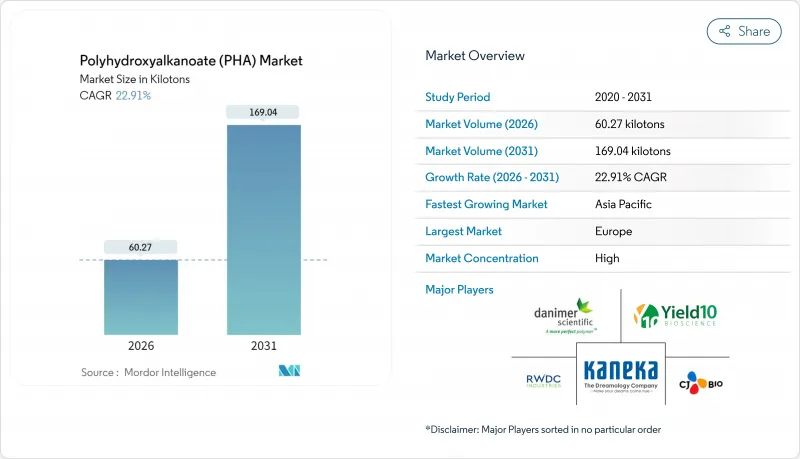

預計聚羥基烷酯市場將從 2025 年的 49.04 千噸成長到 2026 年的 60.27 千噸,到 2031 年將達到 169.04 千噸,2026 年至 2031 年的複合年成長率為 22.91%。

對一次性塑膠製品日益嚴格的監管、大規模產能投資以及材料科學的不斷進步,正推動包裝、醫療保健和農業領域快速實現替代方案。歐洲憑藉嚴格的廢棄物減量指令已確立了先發優勢,而亞太地區的供應鏈正受益於工業成長和豐富的原料供應而迅速擴張。混合微生物培養製程降低了滅菌要求,提高了可靠性,並有可能降低單位成本,提供更多原料選擇。市場競爭依然適中,BASF等老牌化學集團與一些專業製造商和風險投資支持的新創Start-Ups共用市場,這些企業透過原料創新和針對特定應用的樹脂設計實現差異化競爭。

全球聚羥基烷酯(PHA)市場趨勢及展望

一次性塑膠禁令刺激了PHA的需求

日益嚴格的國家和地方法規直接體現在可堆肥材料的採購目標上。加州參議院第54號法案設立了生產者延伸責任制,強制要求所有涵蓋的材料在2032年前必須可回收或可堆肥,並明確將聚羥基脂肪酸酯(PHA)納入受回收和減量目標約束的塑膠定義中。儘管在分類上存在爭議,但歐盟的《一次性塑膠指令》施加了類似的壓力,促使餐飲服務品牌迅速重新設計。夏威夷逐步淘汰不可生物分解包裝的禁令也支持了這一趨勢。目前,大型消費品製造商正在試驗使用PHA基吸管、刀叉餐具和蓋子,以避免受到處罰,這些試點項目已為樹脂供應商贏得了初步的批量合約。

對永續聚合物的需求日益成長

企業脫碳目標和更新的生態設計標準正迫使加工商轉向可在土壤和水環境中分解的材料。聚羥基脂肪酸酯(PHAs)符合此要求,因為它們無需專門的工業堆肥即可礦化,這使其區別於澱粉基混合物和聚乳酸。生命週期研究表明,使用廢棄物衍生碳源的PHAs可將環境影響降低高達50%。包裝、農業薄膜、家電機殼和醫療拋棄式產品市場正在不斷成長,尤其是在新型相容劑技術提高了拉伸強度和阻隔性能之後。

與傳統聚合物相比,價格更高

雖然一般塑膠的交易價格約為每公斤1.00-1.30美元,但商用PHA的價格卻高達每磅2.25-2.75美元,這限制了其在低利潤包裝應用中的廣泛應用。儘管製程最佳化研究預測,改用食品廢棄物作為原料可節省30-40%的成本,但在短期內實現價格競爭力仍面臨挑戰。因此,在產量增加並實現規模經濟之前,終端用戶優先考慮高附加價值應用和受監管主導的細分市場。

細分市場分析

在聚羥基烷酯(PHA)市場,共聚物預計到2025年將達到25.21千噸,佔51.40%的市佔率。 PHBV等共聚物具有柔軟性與氧氣阻隔性能,能夠滿足冷藏食品包裝標準。近期研究表明,50% PHBV與Polybutylene Adipate Terephthalate( PBA)的混合物具有更高的斷裂伸長率和更低的水蒸氣滲透性,使其適用於肉類和起司包裝的熱成型托盤。此外,產品開發人員也十分看重其易於在傳統擠出生產線上進行下游加工,降低了資本投入。

儘管三元共聚物目前的產量相對較低,但其複合年成長率高達23.70%,遠超其他樹脂系列,凸顯了其在專用醫療設備和電子機殼的重要性。生產過程的創新將4-羥基丁酸酯(4HB)含量提高到50%以上,從而改善了其彈性和緩釋性能,使其適用於可吸收藥物遞送薄膜。隨著生產規模的擴大,三元共聚物的生產將開啟一個差異化的細分市場,滿足先前由石油基彈性體主導的機械性能需求,從而推動整個聚羥基烷酯市場的發展。

預計到2025年,醣類和糖蜜將佔聚羥基烷酯)市場佔有率的56.60%,這得益於其可預測的產量和完善的物流網路。巴西和泰國與甘蔗和甜菜供應相關的發酵平台已形成綜合性農業產業中心,確保了原料的自給自足。然而,原料成本仍然是商業化工廠最大的支出項目。乙醇和食品市場中蔗糖競爭的加劇促使企業策略性地轉向使用廢油和甘油作為原料。預計此原料來源將以23.95%的複合年成長率成長。

廢油利用途徑可降低碳排放強度,並節省高達 40% 的成本。測試表明,利用粗甘油培養的巨型普氏菌(Priestia megaterium)可獲得 42% 的細胞內聚羥基脂肪酸酯(PHA)含量。農業廢棄物也備受關注,例如,韓國利用泡菜生產過程中產生的白菜碎屑作為概念驗證生物反應器的原料,展現了本地循環經濟的協同效益。雖然甲烷和二氧化碳的直接利用仍處於起步階段,但日益成熟的光養混合培養系統可望實現真正的碳負排放特性。

區域分析

歐洲保持主導地位,預計2025年將佔據43.80%的市場。這主要得益於生態設計法規、掩埋稅以及消費者偏好等因素的共同推動,加速了塑膠製品的普及。一次性塑膠指令要求迅速減少石油基刀叉餐具的使用,促使德國、法國和北歐國家的零售連鎖店擴大使用PHA(聚羥基烷酯)製作蒸餾袋蓋和水果網。諸如COM4PHA聯盟等研發舉措,結合公共津貼和私人技術,透過促進PHBV(聚羥基乙烯醇)化合物的大規模生產,進一步增強了區域專業實力,這些化合物可用於化妝品容器和農業用繩。

亞太地區是成長最快的市場,預計到2031年將以24.10%的複合年成長率成長。中國正主導這項轉型,透過將PHA生產能力整合到現有的糖和棕櫚油加工廠中,來規避供應風險。道達爾能源與布魯法之間的合作,便是跨國公司和本土企業整合資本和下游管道的典範。日本持續突破性能極限,KANEKA工廠的擴建使其年產量超過2萬噸,同時也率先開發了可生物分解的漁具等級。在韓國,世界泡菜研究所的「廢棄物製PHA」示範計劃展示了原料創新如何解決廢棄物處理難題並擴大聚合物產量。

北美地區正經歷強勁成長,主要得益於監管措施和創業投資資金。加州、紐約州和沿海城市的生產者延伸責任制(EPR)費用有效地補貼了可堆肥材料。 Danimer Scientific在喬治亞的擴張將提高當地產量,並縮短品牌所有者的供應鏈。加拿大計劃訂定的一次性用品法規以及墨西哥城市層面的泡沫塑膠發泡將進一步推動推動要素。區域性學術機構正在培養人才,以支持持續的製程最佳化。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對一次性塑膠的監管禁令將推動對聚羥基脂肪酸酯(PHAs)的需求。

- 對永續聚合物的需求日益成長

- 提高快速消費品產業的永續性意識

- 高齡化社會對生物可吸收植入的需求日益成長

- 擴大PHA在農業領域的應用

- 市場限制

- 與傳統聚合物相比,價格更高

- 生產能力和擴充性有限

- 消費者意識和教育的缺乏

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 單體

- 共聚物

- 三元共聚物

- 按原料

- 糖/糖蜜

- 植物油和脂肪酸

- 廢油和甘油

- 甲烷/二氧化碳

- 農業和食品廢棄物

- 透過生產方法

- 細菌發酵

- 混合微生物培養

- 人造植物/藻類

- 按最終用戶行業分類

- 包裝

- 農業

- 生物醫學

- 其他(基礎設施、石油和天然氣等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- BASF

- BIO ON SpA

- Bluepha Co,. Ltd.

- CJ CheilJedang Corp.

- Danimer Scientific

- Genecis Bioindustries Inc.,

- Kaneka Corporation

- Mango Materials

- PolyFerm Canada

- RWDC Industries

- Terraverdae Bioworks Inc.

- Yield10 Bioscience, Inc.

第7章 市場機會與未來展望

The Polyhydroxyalkanoate market is expected to grow from 49.04 kilotons in 2025 to 60.27 kilotons in 2026 and is forecast to reach 169.04 kilotons by 2031 at 22.91% CAGR over 2026-2031.

Regulatory restrictions on single-use plastics, sizeable investments in production capacity and continuing material-science advances are reinforcing a rapid substitution dynamic in packaging, biomedical and agricultural uses. Europe commands early-mover advantage on account of strict waste-reduction directives, while the Asia-Pacific supply base is scaling fast in response to industrial growth and abundant feedstock. Mixed microbial culture processing is gaining credibility by cutting sterilisation demands, potentially lowering unit costs and broadening the feedstock slate. Competitive intensity remains moderate; established chemical groups such as BASF share the stage with specialist producers and venture-backed start-ups that differentiate through feedstock innovation and application-specific resin design.

Global Polyhydroxyalkanoate (PHA) Market Trends and Insights

Regulatory bans on single-use plastics accelerating PHA demand

Mounting national and municipal restrictions are translating directly into procurement targets for compostable materials. California's Senate Bill 54 established an Extended Producer Responsibility program mandating that all covered materials be recyclable or compostable by 2032, explicitly including PHA in its definition of plastics subject to recycling and reduction targets . Despite classification debates, the EU Single-Use Plastics Directive exerts similar pressure, spurring rapid brand reformulations in food service articles. Hawaii's phased bans on non-biodegradable containers reinforce the trend. Major consumer-goods companies now pilot PHA-based straw, cutlery, and lid programmes to pre-empt penalties, thereby anchoring early-volume contracts for resin suppliers.

Growing demand for sustainable polymers

Corporate decarbonisation targets and updated eco-design metrics push converters toward materials that can degrade in soil and aquatic environments. PHAs fulfil this requirement because they mineralise without specialised industrial composting, differentiating them from starch blends and polylactic acid. Life-cycle studies record up to 50% lower environmental footprints when PHAs derive their carbon from waste substrates. Packaging, agricultural films, consumer electronics casings and medical disposables therefore constitute growing addressable volume, especially as recent compatibiliser chemistries boost tensile strength and barrier performance.

Higher price compared to conventional polymers

Commodity plastics trade at roughly USD 1.00-1.30 per kg, whereas commercial PHA grades range from USD 2.25-2.75 per lb, constraining uptake in thin-margined packaging. Process optimisation studies project a possible 30-40% cost reduction when switching to food-waste feedstocks, yet parity remains elusive in the near term. Consequently, end-users prioritise high-value or regulation-driven niches until volumes rise and economies of scale materialise.

Other drivers and restraints analyzed in the detailed report include:

- Growing awareness over sustainability in FMCG industry

- Rising demand for bio-resorbable implants amid ageing populations

- Limited production capacity and scalability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The polyhydroxyalkanoate market size for co-polymers reached a leading 25.21 kilotons in 2025, translating into 51.40% share. Co-polymer grades such as PHBV deliver flexibility and oxygen barrier performance that meet chilled-food packaging standards. Recent work blending 50% PHBV with polybutylene adipate terephthalate improved elongation at break and cut water-vapour transmission, paving the way for thermoformed trays in meat and cheese packs. Product formulators also value the ease of downstream conversion on conventional extrusion lines, which curtails capital expenditure.

Terpolymers command only a modest volume base today yet outpace all other resin families at a 23.70% CAGR, underscoring their role in specialised biomedical and electronics housings. Production breakthroughs that boost 4HB content above 50% have enhanced elasticity and slow-release characteristics, useful for absorbable drug-delivery films. As scale grows, terpolymer production will lift the overall polyhydroxyalkanoate market by opening differentiated niches where mechanical demands previously favoured petrochemical elastomers.

Sugar and molasses contributed 56.60% of polyhydroxyalkanoate market share in 2025 on the back of predictable yields and established logistics. Fermentation platforms tethered to sugar-cane or beet supply in Brazil and Thailand create integrated agro-industrial hubs with captive raw materials. Nonetheless, feedstock cost remains the single largest expense at commercial plants. Rising competition for sucrose among ethanol and food markets has sparked a strategic pivot toward waste oils and glycerol, a stream forecast to expand volume at 23.95% CAGR.

Waste-oil pathways lower carbon intensity and deliver up to 40% cost relief, according to trials where Priestia megaterium achieved 42% intracellular PHA content from crude glycerol. Agricultural residues are also gaining traction; cabbage trimmings from kimchi production now feed proof-of-concept bioreactors in South Korea, pointing to regional circular-economy synergies. Methane and direct COa utilisation remain embryonic yet could confer true carbon-negative credentials once phototrophic mixed-culture systems mature.

The Polyhydroxyalkanoate Market Report Segments the Industry by Product Type (Monomers, Copolymers, and Terpolymers), Feedstock (Sugar/Molasses, Plant Oils and Fatty Acids, and More), Production Method (Bacterial Fermentation and More), End-User Industry (Packaging, Agriculture, and More) and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Europe retained leadership with 43.80% share in 2025 as eco-design rules, landfill taxes and consumer preference converged to accelerate deployment. The Single-Use Plastics Directive mandates steep reduction of petroleum-based cutlery and plates, prompting retail chains across Germany, France and the Nordics to use PHA for ready-meal lids and fruit nets. R&D initiatives such as the COM4PHA consortium bundle public grants with private know-how to scale PHBV compounds targeting cosmetic jars and agricultural twines, further anchoring regional expertise.

Asia-Pacific is the fastest-growing arena, expanding at 24.10% CAGR to 2031. China champions the transition by integrating PHA capacity into existing sugar and palm-oil processing complexes, thereby hedging against supply risk. TotalEnergies and Bluepha's collaboration exemplifies how multinational and domestic groups pool capital and downstream channels. Japan continues to edge performance thresholds; Kaneka's plant upgrade pushes annual output past 20 kt while pioneering grades tailored for biodegradable fishing gear. South Korea's waste-to-PHA demonstration at the World Institute of Kimchi showcases how feedstock innovation solves disposal headaches and fuels polymer volume.

North America exhibits robust growth supported by regulatory momentum and venture funding. California, New York and several coastal municipalities impose EPR fees that effectively subsidise compostable materials. Danimer Scientific's Georgia expansion will lift local output and offer brand owners shorter supply lines. Canada's forthcoming single-use regulation and Mexico's city-level bans on styrene foams present additional traction points. Regional academics widen the talent pipeline, ensuring sustained process optimisation.

- BASF

- BIO ON SpA

- Bluepha Co,. Ltd.

- CJ CheilJedang Corp.

- Danimer Scientific

- Genecis Bioindustries Inc.,

- Kaneka Corporation

- Mango Materials

- PolyFerm Canada

- RWDC Industries

- Terraverdae Bioworks Inc.

- Yield10 Bioscience, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Bans on Single Use Plastics Accelerating PHA Demand

- 4.2.2 Growing Demand for Sustainable Polymers

- 4.2.3 Growing Awareness over Sustainability in FMCG Industry

- 4.2.4 Rising Demand for Bio Resorbable Implants Amid Ageing Populations

- 4.2.5 Growing Usage of PHA in Agriculture Industry

- 4.3 Market Restraints

- 4.3.1 Higher Price Compared to the Conventional Polymers

- 4.3.2 Limited Production Capacity and Scalability

- 4.3.3 Lack of Consumer Awareness and Education Deficits

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Monomer

- 5.1.2 Copolymer

- 5.1.3 Terpolymer

- 5.2 By Feedstock

- 5.2.1 Sugar / Molasses

- 5.2.2 Plant Oils & Fatty Acids

- 5.2.3 Waste Oils & Glycerol

- 5.2.4 Methane / CO2

- 5.2.5 Agricultural & Food Waste

- 5.3 By Production Method

- 5.3.1 Bacterial Fermentation

- 5.3.2 Mixed Microbial Culture

- 5.3.3 Engineered Plants / Algae

- 5.4 By End-user Industry

- 5.4.1 Packaging

- 5.4.2 Agriculture

- 5.4.3 Biomedical

- 5.4.4 Other (Infrastructure, Oil and Gas, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share(%)/Ranking Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 BASF

- 6.3.2 BIO ON SpA

- 6.3.3 Bluepha Co,. Ltd.

- 6.3.4 CJ CheilJedang Corp.

- 6.3.5 Danimer Scientific

- 6.3.6 Genecis Bioindustries Inc.,

- 6.3.7 Kaneka Corporation

- 6.3.8 Mango Materials

- 6.3.9 PolyFerm Canada

- 6.3.10 RWDC Industries

- 6.3.11 Terraverdae Bioworks Inc.

- 6.3.12 Yield10 Bioscience, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

聚羥基烷酯市場:全球市場按產品類型、製造流程、原料和應用進行預測-2026-2032年

聚羥基烷酯市場:全球市場按產品類型、製造流程、原料和應用進行預測-2026-2032年 聚羥基烷酯市場分析與預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、製程、設備、解決方案、模式

聚羥基烷酯市場分析與預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、製程、設備、解決方案、模式 全球聚羥基烷酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚羥基烷酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 聚羥基烷酯市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

聚羥基烷酯市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) 全球聚羥基烷酯(PHA)市場(至2030年)按類型(短鏈/中鏈)、生產方法(糖發酵/植物油發酵)、應用(包裝和食品服務/生物醫學)和地區分類

全球聚羥基烷酯(PHA)市場(至2030年)按類型(短鏈/中鏈)、生產方法(糖發酵/植物油發酵)、應用(包裝和食品服務/生物醫學)和地區分類 聚羥基脂肪酸酯市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

聚羥基脂肪酸酯市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 聚羥基烷酸酯市場(類型:短鍊和中鏈,最終用途:包裝、油漆塗料、醫療、農業、紡織等)-全球產業分析、規模、佔有率、成長、趨勢及預測,2024-2034

聚羥基烷酸酯市場(類型:短鍊和中鏈,最終用途:包裝、油漆塗料、醫療、農業、紡織等)-全球產業分析、規模、佔有率、成長、趨勢及預測,2024-2034 聚羥基烷酯市場規模、佔有率和趨勢分析報告:按類型、最終用途、按地區、細分市場預測,2024-2030 年聚羥基烷酯(PHA) 市場 - 2024 年至 2029 年預測

聚羥基烷酯市場規模、佔有率和趨勢分析報告:按類型、最終用途、按地區、細分市場預測,2024-2030 年聚羥基烷酯(PHA) 市場 - 2024 年至 2029 年預測 聚羥基鏈烷酸(PHA)的全球市場(2016-2036)

聚羥基鏈烷酸(PHA)的全球市場(2016-2036)