|

市場調查報告書

商品編碼

1910709

熱塑性澱粉(TPS):市佔率分析、產業趨勢與統計、成長預測(2026-2031)Thermoplastic Starch (TPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

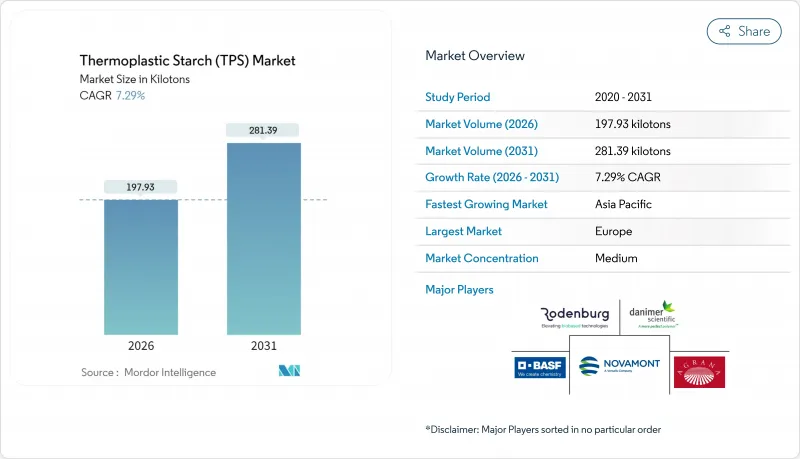

熱塑性澱粉市場規模預計到 2026 年將達到 197.93 千噸,高於 2025 年的 184.49 千噸,預計到 2031 年將達到 281.39 千噸。

預計2026年至2031年年複合成長率(CAGR)為7.29%。

熱塑性澱粉的防潮性能持續提升,加上相容劑和奈米複合材料技術帶來的機械強度增強,長期以來存在的性能瓶頸正在被打破。歐洲優先考慮可堆肥性的法規、北美電子商務的需求以及亞太地區政府對生物基材料的支持,共同推動了熱塑性澱粉市場規模的擴大。玉米和馬鈴薯澱粉原料價格的波動加劇了供應鏈風險,但木薯和農業殘渣等非食品替代原料的同步發展則有助於降低成本風險。市場競爭依然激烈,但格局正趨於多元化:老牌化工巨頭利用其規模優勢,而專業製造商則拓展產品系列,以滿足醫療、3D列印和高階包裝等細分應用領域的需求。

全球熱塑性澱粉(TPS)市場趨勢及洞察

對可生物分解包裝材料的需求不斷成長

將於2025年2月生效的歐盟新包裝及包裝廢棄物法規將強制要求包裝可回收利用,同時鼓勵使用工業和家庭可堆肥基材,這將立即擴大熱塑性澱粉市場。同時,環氧大豆油塑化劑的技術創新已將水性降低了28.6%,且未影響其光學透明度。跨國品牌擁有者現在將可堆肥包裝定位為高階差異化優勢,已開發經濟體中73%的消費者願意為經認證的永續解決方案支付溢價。加工商和澱粉加工商之間建立的合作夥伴關係,剔除了中間環節,鞏固了長期合約並支持了產能擴張。監管需求和商業性需求之間的協同作用正在加速食品、飲料和個人護理行業的規範核准,進一步鞏固了熱塑性澱粉市場的成長勢頭。

主要經濟體禁止使用一次性塑膠製品

到2024年,已有超過67個國家實施了一次性塑膠法規,結束了現有石油基產品的合規期。中國的「竹子取代塑膠」政策和財政獎勵正在推動國內對生物基材料的需求。歐盟的《一次性塑膠指令》要求大型速食連鎖店使用可生物分解的刀叉餐具。同時,澳洲正日益嚴格地執行純度標準,包括各州禁止使用澱粉-聚丙烯複合材料。監管的碎片化正在為符合嚴格生物分解標準的純熱塑性澱粉化合物創造一個高階利基市場。監管實施的加速表明,人們正在持續地從石油基塑膠轉向其他材料,這將推動熱塑性澱粉市場的成長。

水分敏感度會限制保存期限

澱粉的親水性使其水蒸氣透過率比低密度聚乙烯(LDPE)高出五倍,這限制了其在熱帶地區的應用。奈米晶纖維素的增強作用可降低40%的吸濕性,但會使生產成本增加25-35%,這給價格敏感型市場帶來了挑戰。保存期限12個月的食品,如果僅使用熱塑性澱粉薄膜包裝,通常會在30-60天內劣化。在潮濕的市場,溫控物流可能會使分銷成本增加高達15%。預計這些技術和物流方面的限制將暫時限制熱塑性澱粉的市場滲透,直到新一代阻隔材料實現規模化商業化。

細分市場分析

預計到2025年,擠出成型將佔據熱塑性澱粉市場57.72%的佔有率,這主要得益於連續加工的經濟性和其對高產能軟性薄膜生產線的適用性。此製程單位成本低,加之在線連續添加塑化劑和快速換料,已成功獲得休閒食品和農產品包裝袋加工商的訂單。射出成型雖然規模較小,但預計其複合年成長率將達到7.73%,因為品牌商對尺寸公差較小的精密零件(例如藥蓋和化妝品罐)的需求日益成長。往復式螺桿設計的不斷改進已將停留時間劣化降低了20%,提高了機械完整性,並拓展了薄壁產品的應用範圍。

為了因應需求波動,製造商正在跨平台進行多元化發展。擠出系統仍然是通用薄膜的核心技術,但產能擴張的重點在於能夠切換片材、吹膜和型材擠出的多功能生產線,從而最大限度地提高資產利用率。射出成型機製造商正在採用伺服馬達驅動,以提高能源效率並縮小與液壓機的成本差距。設備價格的下降吸引了更多中小企業,加劇了區域競爭,並加速了新興經濟體熱塑性澱粉市場的深化。

熱塑性澱粉市場報告按生產類型(擠出成型和射出成型)、應用領域(包裝袋、薄膜、3D列印及其他應用)、終端用戶行業(包裝、農業園藝、消費品及其他)以及地區(亞太、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以千噸為單位。

區域分析

預計到2025年,歐洲將佔據熱塑性澱粉市場39.32%的佔有率,這主要得益於清晰的法律體制、成熟的堆肥系統以及消費者的高度接受度。成員國的廢棄物分類目標鼓勵市政當局投資有機物收集,從而確保真正的循環經濟,並支撐對澱粉基材料的需求。然而,玉米價格的急劇上漲導致原物料採購壓力增大,AGRANA公司計劃在2024年將其玉米加工量減少26%,凸顯了供應鏈風險。

亞太地區預計將成為成長最快的地區,到2031年年均成長率將達到8.22%,主要得益於中國的生物材料補貼和印度不斷擴大的生物聚合物產能。該地區的優勢包括豐富的農業殘餘物以及國內對永續和軟性包裝材料日益成長的需求。當地加工商正利用政府補貼增設反應擠出生產線,加速市場進入並加劇競爭。這正使熱塑性澱粉市場從出口導向型轉變為擁有廣泛區域生產基地的市場。

在北美,電子商務的興起和零售商日益提高的永續性標準正在推動成長。加州和華盛頓州的市政有機物處理計畫為可堆肥廢棄物創造了天然的出口管道,從而增強了直接面對消費者的品牌的需求。南美洲豐富的澱粉資源使其成為原料出口地區,但下游加工能力的不足正在減緩國內消費的成長。中東和非洲地區仍處於低度開發狀態,其推廣應用取決於未來的廢棄物基礎設施現代化和農業節水項目,這些項目有望推動可生物分解地膜的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 可生物分解包裝的需求不斷成長

- 主要經濟體禁止使用一次性塑膠製品

- 品牌所有者的永續性超越了監管義務。

- 改用可堆肥的電商信封

- 使用TPS複合材料測試替代藥品泡殼包裝

- 市場限制

- 水分敏感度會限制保存期限

- 與石油基塑膠相比,機械強度較差

- 圍繞澱粉成分的食品與食材之爭

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按生產類型

- 擠出成型

- 射出成型

- 透過使用

- 包包

- 電影

- 3D列印

- 其他用途

- 按最終用戶行業分類

- 包裝

- 農業和園藝

- 消費品

- 醫療和藥品

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AGRANA

- BASF

- BioLogiQ Inc.

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Danimer Scientific

- Great Wrap

- Grupa Azoty

- Kuraray Co., Ltd

- Novamont SpA(Versalis SpA)

- Rodenburg Biopolymers

第7章 市場機會與未來展望

Thermoplastic Starch market size in 2026 is estimated at 197.93 kilotons, growing from 2025 value of 184.49 kilotons with 2031 projections showing 281.39 kilotons, growing at 7.29% CAGR over 2026-2031.

Continuous improvements in moisture-barrier performance, coupled with mechanical-strength gains achieved through compatibilizer and nanocomposite technologies, are removing long-standing functional barriers. European legislation that prioritizes compostability, North American e-commerce fulfillment demands, and Asia-Pacific government stimulus for bio-based materials are jointly expanding the thermoplastic starch market's addressable applications. Price volatility in corn and potato starch feedstocks has raised supply-chain risk, yet parallel progress in non-food alternatives such as cassava and agricultural residues is buffering cost exposure. Competition remains intense but fragmented, with established chemical majors leveraging scale while specialists round out product portfolios for niche medical, 3-D printing, and premium packaging uses.

Global Thermoplastic Starch (TPS) Market Trends and Insights

Rising Demand for Biodegradable Packaging

New EU Packaging and Packaging Waste Regulation rules, effective February 2025, legally require recyclability while encouraging industrial and home-compostable substrates, instantly enlarging the thermoplastic starch market. Parallel breakthroughs in epoxidized soybean-oil plasticizers have lowered water sensitivity by 28.6% without losing optical clarity. Multinational brand owners now treat compostable packaging as a premium differentiator, and 73% of consumers in developed economies are willing to pay higher prices for verified sustainable solutions. Converter-starch-processor partnerships that cut intermediaries are cementing long-term contracts, thereby supporting capacity expansions. The combined regulatory and commercial pull is translating into faster specification approvals across food, beverage, and personal-care verticals, further solidifying thermoplastic starch market growth trajectories.

Ban on Single-Use Plastics in Major Economies

More than 67 nations enforced single-use plastic restrictions by 2024, closing the compliance window for incumbent petro-based products. China's bamboo-as-plastic-substitute policy and financial incentives have catalyzed domestic demand for bio-materials. The EU Single-Use Plastics Directive has pushed major quick-service restaurants to require biodegradable utensils, while Australia's state-level bans on starch-polypropylene blends illustrate tightening purity thresholds. Regulatory fragmentation creates a premium niche for pure thermoplastic starch formulations meeting strict biodegradability standards. The accelerated enforcement pace points to an enduring, structural shift away from petroleum plastics, thus feeding the thermoplastic starch market.

Moisture Sensitivity Limiting Shelf-Life

The hydrophilic nature of starch results in water-vapor transmission rates up to 5 times higher than LDPE, curbing adoption in tropical zones. Nanocrystalline-cellulose reinforcement can slash moisture uptake by 40%, yet production costs jump 25-35%, challenging price-sensitive segments. Food products that require 12-month shelf lives typically experience quality degradation in 30-60 days when packaged purely in thermoplastic starch films. Climate-controlled logistics add as much as 15% to distribution costs in humid markets. These technical and logistical penalties temporarily limit the thermoplastic starch market's penetration rate until next-generation barrier chemistries become commercial at scale.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Sustainability Pledges Beyond Regulatory Mandates

- Pharma Blister-Pack Replacement Trials with TPS Composites

- Inferior Mechanical Strength Vs. Petro-Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusion molding delivered 57.72% of the thermoplastic starch market share in 2025, buoyed by its continuous processing economics and adaptability to high-volume flexible-film lines. The process allows inline plasticizer dosing and rapid order changeovers, keeping per-unit costs low and securing orders from snack-food and produce-bag converters. Injection molding, although smaller, is forecast at a 7.73% CAGR as brand owners pursue precision components such as pharmaceutical caps and cosmetic jars that demand tighter dimensional tolerances. Continuous enhancements in reciprocating-screw designs now reduce residence-time degradation by 20%, lifting mechanical integrity and widening the addressable range of thin-wall items.

Manufacturers diversify across both platforms to hedge demand swings. Extrusion systems remain the backbone for commodity films, but capacity additions tilt toward multi-purpose lines that switch between sheet, blown film, and profile extrusion to maximize asset utilization. Injection equipment suppliers embed servo-electric drives to enhance energy efficiency, narrowing the cost gap with hydraulic machines. As equipment prices fall, small and medium enterprises gain entry, expanding regional competition and deepening the thermoplastic starch market across emerging economies.

The Thermoplastic Starch Report is Segmented by Manufacturing Type (Extrusion Molding and Injection Molding), Application (Bags, Films, 3-D Printing, and Other Applications), End-User Industry (Packaging, Agriculture and Horticulture, Consumer Goods, and More), and Geography ( Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Geography Analysis

Europe's 39.32% share of the thermoplastic starch market in 2025 is rooted in clear legislative frameworks, mature composting systems, and strong consumer acceptance. Member-state waste-sorting targets incentivize municipal investments in organics collection, ensuring true circularity and validating demand for starch-based materials. Feedstock pressure, however, surfaced when corn prices spiked and AGRANA reported a 26% drop in corn processing volumes in 2024, highlighting supply-chain risk.

Asia-Pacific is forecast to deliver the fastest 8.22% CAGR through 2031, anchored by China's bio-material subsidies and India's widening biopolymer capacity. Regional advantages include abundant agricultural residues and growing domestic demand for sustainable, flexible packaging. Local processors leverage government grants to add reactive-extrusion lines, thereby accelerating market entry and intensifying competition. The thermoplastic starch market thus transitions from export-oriented pockets to a broad regional production base.

North America benefits from e-commerce penetration and rising retailer sustainability benchmarks. Municipal organics programs in California and Washington state create a natural outlet for compostable waste streams, reinforcing demand among direct-to-consumer brands. South America's starch abundance positions the region as a feedstock exporter, yet limited downstream processing capacity delays domestic consumption. Middle East and Africa remain nascent, with uptake tied to future waste-infrastructure modernization and agricultural water-conservation programs that could favor biodegradable mulch films.

- AGRANA

- BASF

- BioLogiQ Inc.

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Danimer Scientific

- Great Wrap

- Grupa Azoty

- Kuraray Co., Ltd

- Novamont S.p.A (Versalis S.p.A.)

- Rodenburg Biopolymers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Biodegradable Packaging

- 4.2.2 Ban on Single-Use Plastics in Major Economies

- 4.2.3 Brand-Owner Sustainability Pledges Beyond Regulatory Mandates

- 4.2.4 Shift Toward Home-Compostable E-Commerce Mailers

- 4.2.5 Pharma Blister-Pack Replacement Trials with TPS Composites

- 4.3 Market Restraints

- 4.3.1 Moisture Sensitivity Limiting Shelf-Life

- 4.3.2 Inferior Mechanical Strength Vs. Petro-Plastics

- 4.3.3 Food-Versus-Materials Debate around Starch Feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Manufacturing Type

- 5.1.1 Extrusion Molding

- 5.1.2 Injection Molding

- 5.2 By Application

- 5.2.1 Bags

- 5.2.2 Films

- 5.2.3 3-D Printing

- 5.2.4 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Packaging

- 5.3.2 Agriculture and Horticulture

- 5.3.3 Consumer Goods

- 5.3.4 Medical and Pharmaceuticals

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Nordics

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGRANA

- 6.4.2 BASF

- 6.4.3 BioLogiQ Inc.

- 6.4.4 Biome Bioplastics

- 6.4.5 BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.6 Danimer Scientific

- 6.4.7 Great Wrap

- 6.4.8 Grupa Azoty

- 6.4.9 Kuraray Co., Ltd

- 6.4.10 Novamont S.p.A (Versalis S.p.A.)

- 6.4.11 Rodenburg Biopolymers

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

增強型熱塑性管市場:依材質、壓力等級、管徑、安裝方式及應用分類-2026-2032年全球市場預測熱塑性膠帶市場:2026-2032年全球市場預測(依產品種類、材料種類、黏合劑種類、基材種類、厚度、寬度、最終用途產業及應用分類)介電膠帶市場:黏合劑類型、基材、寬度、厚度、最終用途產業和應用分類-全球預測,2026-2032年

增強型熱塑性管市場:依材質、壓力等級、管徑、安裝方式及應用分類-2026-2032年全球市場預測熱塑性膠帶市場:2026-2032年全球市場預測(依產品種類、材料種類、黏合劑種類、基材種類、厚度、寬度、最終用途產業及應用分類)介電膠帶市場:黏合劑類型、基材、寬度、厚度、最終用途產業和應用分類-全球預測,2026-2032年 2026年全球熱塑性管道市場報告

2026年全球熱塑性管道市場報告 熱塑性塑膠管材市場-全球產業規模、佔有率、趨勢、機會、預測:依聚合物類型、應用、最終用戶、地區和競爭格局分類,2021-2031年高溫熱塑性樹脂市場-全球產業規模、佔有率、趨勢、機會及預測(依樹脂類型、範圍、終端用戶產業、區域及競爭格局分類,2021-2031年)熱塑性層壓板市場:按材料類型、工藝、厚度、應用和最終用途行業分類,全球預測(2026-2032年)熱塑性澱粉合金市場按形態、製造流程、混合類型和應用分類,全球預測(2026-2032年)高性能熱塑性聚氨酯彈性體市場依產品形式、原料類型、加工技術、硬度等級、終端應用產業及通路分類-2026-2032年全球預測

熱塑性塑膠管材市場-全球產業規模、佔有率、趨勢、機會、預測:依聚合物類型、應用、最終用戶、地區和競爭格局分類,2021-2031年高溫熱塑性樹脂市場-全球產業規模、佔有率、趨勢、機會及預測(依樹脂類型、範圍、終端用戶產業、區域及競爭格局分類,2021-2031年)熱塑性層壓板市場:按材料類型、工藝、厚度、應用和最終用途行業分類,全球預測(2026-2032年)熱塑性澱粉合金市場按形態、製造流程、混合類型和應用分類,全球預測(2026-2032年)高性能熱塑性聚氨酯彈性體市場依產品形式、原料類型、加工技術、硬度等級、終端應用產業及通路分類-2026-2032年全球預測 熱塑性管道市場規模、佔有率和成長分析(按管道類型、聚合物類型、安裝位置和地區分類)-2026-2033年產業預測

熱塑性管道市場規模、佔有率和成長分析(按管道類型、聚合物類型、安裝位置和地區分類)-2026-2033年產業預測