|

市場調查報告書

商品編碼

1910686

線上彩票:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Online Lottery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

預計到 2025 年,線上彩券市場價值將達到 115.3 億美元,到 2026 年將成長至 125.8 億美元,到 2031 年將成長至 194.5 億美元,在預測期(2026-2031 年)內複合年成長率為 9.11%。

這一成長得益於行動裝置的普及、便捷的數位支付流程以及不斷完善的監管。行動通路目前佔彩券總銷售額的一半以上,行動商務的普及也簡化了轉換流程。區塊鏈技術等創新技術提高了透明度,行動應用程式、安全付款閘道和人工智慧驅動的用戶帳戶等也提升了玩家的安全性和參與度。社群媒體、導向電子郵件宣傳活動和線上廣告等策略在吸引和留住彩票愛好者方面都卓有成效。訂閱服務和遊戲化體驗等功能不僅提高了玩家留存率,也有助於吸引更年輕的族群。歐洲主導其清晰的許可框架和跨國彩券體系,在市場價值方面處於領先地位,而美國在近期合法化後也不斷擴大其市場規模。年輕族群更傾向於數位化即開型遊戲,而傳統彩券形式由於媒體對獎金池式彩券的關注而依然流行。網路安全和合規自動化投入的增加正在鞏固現有平台提供者的地位。

全球線上彩票市場趨勢與洞察

數位錢包和行動支付整合度不斷提高

數位錢包和行動支付方式使彩票購買變得便捷安全,用戶可以隨時隨地購買彩票。這些進步消除了傳統支付方式的局限性,擴大了基本客群,並促進了彩票銷售。根據中國網際網路資訊中心預測,2024年,中國92.8%的行動網路用戶將使用行動支付。這一成長使得彩券購買更加輕鬆便捷,突破了現金交易和實體店銷售的限制。歐洲中央銀行的數位歐元計畫旨在完善現有支付系統,同時減少對非歐洲平台的依賴,簡化跨境彩券交易。行動支付的整合對於刮刮樂彩券尤其有利,因為刮刮樂彩券既滿足了用戶對即時結果的需求,又兼具數位錢包的便利性。在銷售點基礎設施有限的亞洲新興市場,QR碼支付系統已成為基於NFC解決方案的有力競爭者,為彩票市場成長創造了新的機會。此外,採用儲存支付憑證可以增強安全性,並支援定期訂閱彩票服務,從而有助於實現穩定的產生收入。

合法化和放鬆管制

合法化將透過建立明確的監管規定、許可要求和消費者保護措施,增強人們對線上彩券的信心。這將確保遊戲的公平性和中獎保障,從而提升玩家的信心。 2024年7月,麻薩諸塞州州長莫拉·希利核准了2025年預算,使線上彩券的銷售合法化。麻州彩券公司計劃在16個月內推出數位平台,要求參與者年滿21歲。芬蘭的博彩市場改革提案對體育博彩和線上遊戲營運商實行開放的許可製度,同時維持Veikkaus對彩票的壟斷地位。新加坡博彩管理局根據2022年《博彩監管法》向新加坡博彩公司頒發了有效期至2025年10月的許可證,為亞太地區提供了一種結構化的監管方法。猶他州眾議員凱拉·伯克蘭計劃在2025年重新提出一項憲法修正案,以使州彩票合法化,從而將猶他州居民原本會花在其他州購買的彩票上的2億美元彩票收入引入該州。這些監管舉措將擴大市場機遇,並建立合規框架,使線上彩票業務合法化。巴西第14790/2023號法律強制要求負責任博彩行為,並要求業者實施系統來監控投注者的活動並識別高風險玩家,從而為新興市場樹立監管標準。

監管和法律挑戰

全球監管標準的零碎化導致許可、課稅和消費者保護方面出現混亂。這些不一致之處不僅存在於國界之間,也存在於各州內部,使得彩券業者的市場准入和營運更加複雜。 2025年4月,德克薩斯州彩券委員會一致投票透過禁止宅配,理由是先前與這些服務相關的爭議性中獎事件引發了人們對合法性和誠信的擔憂。德克薩斯州參議院通過了第28號參議院法案,將透過宅配銷售線上彩券的行為定為犯罪,凸顯了法規環境的不穩定性。在香港,《博彩條例》實施了嚴格的監管,並賦予香港賽馬會博彩活動和六彩運營的壟斷權,限制了國際運營商的市場准入。同樣,西澳大利亞州2024年的《博彩法修正案》透過提高違規處罰力度和要求彩票牌照提供銀行擔保,加強了對互動博彩服務的監管。這種監管碎片化增加了合規的複雜性和營運成本,有利於擁有更強監管專業知識的成熟企業,而對小規模的企業造成不成比例的影響。

細分市場分析

行動平台將在2025年佔據55.72%的市場佔有率,並展現出最快的成長勢頭,到2031年複合年成長率將達到11.08%。這一成長主要得益於智慧型手機的普及和行動支付系統的整合。桌面平台對於需要精細介面的複雜彩票遊戲仍然至關重要,但隨著行動裝置最佳化程度的提高,用戶參與度一直在下降。行動優先策略支援定位服務、彩票結果推播通知以及無縫的社交共用,從而突破傳統桌面平台的局限,提升玩家參與度。

Pollard Banknote與愛爾蘭Premier Lotteries於2024年12月合作推出行動應用程式和電子即開型彩票遊戲組合,體現了業界對行動裝置體驗的重視。該平台包含玩家註冊、遊戲購買和彩票掃描等功能。行動平台受益於應用程式商店的分發管道,但同時也必須應對監管方面的挑戰,例如地理位置限制和年齡驗證。將行動遊戲的美學元素與傳統彩票機制結合,打造出既能吸引年輕用戶群又能符合監管標準的混合體驗。此外,跨平台同步功能可讓玩家在行動裝置上發起交易,並在桌面平台上完成交易,從而提升整個使用者體驗流程的轉換率。

到2025年,抽獎式彩券遊戲將佔據32.10%的市場佔有率,凸顯了消費者對定期開獎、獎金豐厚的傳統彩券遊戲的強烈偏好。這類遊戲,例如歐洲百萬彩票,利用跨境獎池,創造出任何單一司法管轄區都無法企及的巨額獎金。即時彩票遊戲預計將快速成長,到2031年複合年成長率將達到10.12%,這主要得益於即時滿足感和行動遊戲功能對數位原住民的吸引力。此外,體育博彩和其他新興遊戲類型融合了傳統彩票機制和現代娛樂形式,但不同地區的法規結構差異顯著。

即時遊戲利用科技創新,提供媲美行動遊戲的先進圖形、動畫和互動體驗,同時符合彩票合規標準。此外,區塊鏈技術在彩票營運中的應用,透過為彩票遊戲和即時遊戲提供透明、防篡改的記錄,正在改變整個行業。這項創新有助於防止欺詐,並促進智慧合約的自動化。遊戲類型的多樣化體現了營運商為滿足不同玩家的偏好所做的努力,從追求改變人生巨額獎金的玩家到喜歡快速贏取小額獎金的休閒玩家,都能找到適合自己的遊戲。

區域分析

2025年,歐洲維持了45.20%的市場佔有率,這主要得益於成熟的跨境彩票營運模式,例如歐洲百萬彩票(EuroMillions)。歐洲百萬彩券在九個國家運營,採用標準化的獎金結構和收益分成機制。英國經歷了重大轉型,Allwin Entertainment成為其第四家獲得許可的營運商。此次轉型涉及3.5億英鎊的投資、30多個新系統的實施以及複雜的資料遷移,旨在使公共產業的收益翻倍。德國繼續根據《州際博彩公約》調整法規結構,該公約確立了線上博彩法規,並解決了近期社群媒體調查中提出的污名化問題。北歐國家取得了顯著進展,芬蘭計劃進行全面的博彩市場改革,將於2027年1月前為商業運營商引入開放式許可製度。此外,歐洲中央銀行的數位歐元計畫正在創建一個統一的支付基礎設施,這有望簡化跨境彩票交易,並減少對非歐洲支付提供者的依賴。

預計北美將經歷最快的成長,到2031年將以10.44%的複合年成長率成長。這一成長主要得益於各州層級的合法化努力和對技術基礎設施的投資,從而擴大了潛在市場。 2024年7月,馬薩諸塞州核准了線上彩票銷售,並將收入分配給幼兒教育計畫。維吉尼亞將其與NeoPollard Interactive的線上彩票合約延長至2028年,延續了夥伴關係創下的收入紀錄。在加拿大,亞伯達推出了線上彩票,這是北美首個整合式彩票遊戲。這展現了各州在數位彩券產品方面的創新。然而,監管的碎片化,例如德克薩斯州禁止第三方宅配服務,構成了一項挑戰。與此同時,其他一些州正在推動數位彩票的擴張。儘管先進的行動支付系統和智慧型手機的高普及率正在推動地方彩票的數位化,但聯邦博彩法規給跨州彩票營運帶來了合規方面的挑戰。

亞太地區及其他全球市場蘊藏著多元化的成長機遇,但這些機會受到監管方式和文化對博彩態度差異的限制。新加坡博彩管理局已根據《2022年博彩管制法》向新加坡博彩公司(Singapore Pools)頒發許可證,使其成為包括公共彩票在內的在線非賭場博彩服務的獨家運營商,這體現了發達亞洲市場結構化的法規結構。澳洲的監管環境也在不斷發展,推出了國家消費者保護框架和BetStop自我排除登記系統,並對與外國兼容的彩票和線上基諾服務進行了審查。在南美洲,巴西的第14790/2023號法律強調負責任博彩措施並強制要求建立營運商監控系統,為該地區的新興市場樹立了監管先例。隨著新興經濟體數位基礎設施的持續發展,高所得收入國家和低收入國家之間的網路普及率差距蘊藏著巨大的成長潛力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 數位錢包普及率不斷提高,行動支付整合度不斷提升

- 合法化和放鬆管制

- 全球網路普及率不斷提高

- 跨境累積獎金池增加獎金金額

- 數位科技的進步

- 利用微型網紅聯盟行銷降低客戶獲取成本

- 市場限制

- 監管和法律挑戰

- 加強對應用程式商店中真錢賭博的監管

- 網路安全威脅與詐欺風險

- 負面的社會看法和污名

- 消費行為分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依平台類型

- 桌面

- 移動的

- 按遊戲類型

- 抽籤

- 即時彩券

- 現場彩券

- 其他

- 按年齡層

- 25歲以下

- 25至40歲

- 40至55歲

- 55歲或以上

- 最終用戶

- 男性

- 女士

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 英國

- 德國

- 瑞典

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 大洋洲國家

- 亞太其他地區

- 其他地區

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Allwyn Entertainment

- PlayHugeLottos

- Francaise des Jeux

- ZEAL Network SE

- Lotto Direct Ltd

- Lottoland

- Lotto Agent

- LottoKings

- WinTrillions

- Lotto247

- Annexio Ltd.

- China Welfare Lottery

- Intralot

- Sisal

- The Lottery Corporation

- International Game Technology(IGT)

- Flutter Entertainment(The Lotteries Pilot)

- NeoGames

- Pollard Banknote

- Jumbo Interactive

第7章 市場機會與未來展望

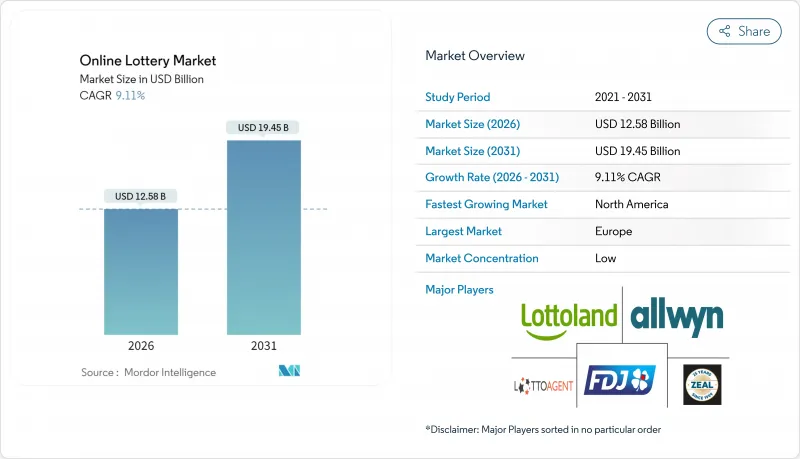

The online lottery market was valued at USD 11.53 billion in 2025 and estimated to grow from USD 12.58 billion in 2026 to reach USD 19.45 billion by 2031, at a CAGR of 9.11% during the forecast period (2026-2031).

This growth is bolstered by a surge in mobile adoption, seamless digital payment processes, and forward-thinking regulations. Currently, mobile channels account for over half of all ticket sales, and the familiarity with m-commerce streamlines the conversion process. Innovations like blockchain for enhanced transparency, mobile applications, secure payment gateways, and AI-driven user accounts are elevating player security and engagement. Strategies such as leveraging social media, targeted email campaigns, and online advertising are proving effective in both attracting and retaining lottery enthusiasts. Features like subscription services and gamified experiences are not only boosting player retention but also drawing in a younger demographic. Europe leads in market value, thanks to its clear licensing frameworks and multi-country draws. Meanwhile, recent legalizations are expanding the market base in the U.S. While younger adults are leaning towards digital-first instant games, traditional draw formats still hold their ground, largely due to the media's focus on pooled jackpots. Increased spending on cybersecurity and automation in compliance are fortifying the position of established platform providers.

Global Online Lottery Market Trends and Insights

Rising penetration of digital wallets and mobile payments integration

Lottery ticket purchases have become seamless and secure with the use of digital wallets and mobile payment options, allowing users to buy tickets anytime and anywhere. This advancement removes the challenges of traditional payment methods, increasing the customer base and driving ticket sales. In 2024, 92.8% of mobile internet users in China utilized mobile payments, according to the China Internet Network Information Center. This growth facilitates hassle-free lottery ticket purchases, bypassing the limitations of cash transactions and physical retail outlets. The European Central Bank's digital euro initiative, currently under preparation, seeks to complement existing payment systems while reducing reliance on non-European platforms, potentially streamlining cross-border lottery transactions. Mobile payment integration is particularly advantageous for instant lottery games, where the demand for immediate results aligns with the convenience of digital wallets. In developing Asian markets with limited point-of-sale infrastructure, QR code-based payment systems are emerging as strong competitors to NFC-based solutions, creating new opportunities for lottery market growth. Additionally, the adoption of stored payment credentials enhances security and supports subscription-based lottery services, fostering consistent revenue generation.

Legalization and regulatory liberalization

Legalization establishes clear regulations, licensing requirements, and consumer protections, enhancing trust in online lotteries. This increases player confidence by ensuring fair games and secure winnings. In July 2024, Massachusetts Governor Maura Healey approved the FY 2025 budget, legalizing online lottery sales. The Massachusetts Lottery plans to launch its digital platform within 16 months, requiring participants to be at least 21 years old. Finland's gaming market reform suggests an open licensing system for commercial operators in sports betting and online gaming while preserving Veikkaus's monopoly over lotteries. Singapore's Gambling Regulatory Authority issued a license to Singapore Pools under the 2022 Gambling Control Act, valid until October 2025, showcasing structured regulatory measures in Asia-Pacific. Utah State Representative Kera Birkeland intends to reintroduce a constitutional amendment in 2025 to legalize the state lottery, aiming to capture the USD 200 million spent by Utah residents on lottery tickets in neighboring states. These regulatory developments expand market opportunities and establish compliance frameworks that legitimize online lottery operations. Brazil's Law 14,790/2023 enforces responsible gambling practices, requiring operators to monitor bettor activity and implement systems to identify at-risk players, setting a regulatory standard for emerging markets.

Regulatory and legal challenges

Fragmented global regulatory standards cause confusion regarding licensing, taxation, and consumer protection. This inconsistency, present across countries and even within states, complicates market entry and operations for lottery operators. In April 2025, the Texas Lottery Commission unanimously decided to ban third-party courier services from purchasing lottery tickets, citing concerns over legality and integrity after controversial jackpot wins linked to these services. Highlighting the volatility of the regulatory environment, the Texas Senate passed Senate Bill 28, criminalizing online lottery ticket sales through couriers. In Hong Kong, the Gambling Ordinance enforces strict regulations, granting the Hong Kong Jockey Club exclusive rights to betting activities and Mark Six Lottery operations, thereby restricting market access for international operators. Similarly, Western Australia's Gambling Legislation Amendment Act 2024 strengthens regulations for interactive gambling services by increasing penalties for noncompliance and requiring operators to provide bank guarantees for lottery permits. This regulatory fragmentation increases compliance complexities and operational costs, disproportionately affecting smaller operators while favoring established players with greater regulatory expertise.

Other drivers and restraints analyzed in the detailed report include:

- Increasing global internet penetration

- Cross-border jackpot pooling boosting prize sizes

- App-store policy tightening on real-money gambling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile platforms captured 55.72% market share in 2025 and exhibit the fastest growth trajectory at 11.08% CAGR through 2031. This growth is primarily driven by the widespread use of smartphones and the integration of mobile payment systems. Desktop platforms remain relevant, particularly for complex lottery games requiring detailed interfaces, but they are experiencing a decline in user engagement as mobile optimization continues to improve. The mobile-first approach supports location-based services, push notifications for draw results, and seamless social sharing, enhancing player engagement beyond the limitations of traditional desktop platforms.

Pollard Banknote's partnership with Premier Lotteries Ireland in December 2024, which introduced a mobile app and an eInstant games portfolio, highlights the industry's focus on mobile-centric experiences. This platform includes features such as player registration, game purchases, and ticket scanning. While mobile platforms benefit from app store distribution channels, they must address regulatory challenges, including geo-gating and age verification. The fusion of mobile gaming aesthetics with traditional lottery mechanics creates hybrid experiences that attract younger demographics while adhering to regulatory standards. Additionally, cross-platform synchronization allows players to initiate transactions on mobile devices and complete them on desktop platforms, improving conversion rates across the user journey.

Draw-based lottery games commanded 32.10% market share in 2025, highlighting consumers' strong preference for traditional lotteries with scheduled draws and attractive jackpots. These games, such as EuroMillions, utilize cross-border jackpot pooling to generate prize sizes that individual jurisdictions cannot achieve alone. Instant lottery games are experiencing rapid growth, with a 10.12% CAGR projected through 2031, driven by the appeal of immediate gratification and mobile gaming features that attract digital-native audiences. Additionally, sports lotteries and other emerging game types combine traditional lottery mechanics with modern entertainment formats, though regulatory frameworks differ significantly across regions.

Instant games are leveraging technological advancements to deliver enhanced graphics, animations, and interactive features that mimic mobile gaming experiences while adhering to lottery compliance standards. Furthermore, the adoption of blockchain technology in lottery operations is transforming the industry by providing transparent and immutable records for both draw-based and instant games. This innovation helps reduce fraud and facilitates smart contract automation. The diversification of game types reflects operators' efforts to meet the varied preferences of players, ranging from those seeking life-changing jackpots to casual participants favoring quick, smaller-value wins.

The Online Lottery Market Report is Segmented by Platform Type (Desktop, Mobile), Game Type (Draw-Based Lottery, Instant Lottery, Sports Lottery, Others), Age Group (Below 25 Years, 25-40 Years, 40-55 Years, 55+ Years), End User (Male, Female), and Geography (North America, Europe, Asia-Pacific, Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe maintained a 45.20% market share in 2025, supported by well-established cross-border lottery operations such as EuroMillions. EuroMillions operates across nine countries with standardized prize structures and revenue distribution mechanisms. The UK experienced a major shift as Allwyn Entertainment became the Fourth Licence operator. This transition involved a GBP 350 million investment, introducing over 30 new systems and complex data migrations, with the goal of doubling returns to Good Causes. Germany continues to adapt its regulatory framework under the State Treaty on Gambling, which structured online gambling regulations and addressed stigmatization concerns highlighted in recent social media studies. Nordic countries are making significant progress, with Finland planning a comprehensive gaming market reform to introduce open licensing systems for commercial operators by January 2027. Additionally, the European Central Bank's digital euro initiative is creating a unified payment infrastructure that could streamline cross-border lottery transactions and reduce reliance on non-European payment providers.

North America is experiencing the fastest regional growth, with a 10.44% CAGR projected through 2031. This growth is driven by state-level legalization efforts and investments in technological infrastructure, which are expanding the addressable market. In July 2024, Massachusetts approved online lottery sales, allocating funds to early childhood education programs. Virginia extended its iLottery contract with NeoPollard Interactive through 2028, continuing a partnership that has achieved record gross sales. In Canada, Alberta launched online draw-based lottery games, marking the first integration of draw games in North America and showcasing provincial innovation in digital lottery delivery. However, regulatory fragmentation poses challenges, as seen in Texas's ban on third-party courier services, while other states embrace digital lottery expansion. Advanced mobile payment systems and high smartphone penetration rates are driving lottery digitization in the region, though federal gambling regulations create compliance challenges for interstate lottery operations.

Asia-Pacific and other global markets offer diverse growth opportunities, though these are constrained by varying regulatory approaches and cultural attitudes toward gambling. Singapore's Gambling Regulatory Authority, under the 2022 Gambling Control Act, has authorized Singapore Pools as the exclusive operator for online non-casino gambling services, including public lotteries, reflecting structured regulatory frameworks in developed Asian markets. Australia's regulatory landscape is evolving with the implementation of the National Consumer Protection Framework and the BetStop self-exclusion register, alongside reviews of foreign-matched lotteries and online keno services. In South America, Brazil's Law 14,790/2023 emphasizes responsible gambling measures and mandates operator monitoring systems, setting a regulatory precedent for emerging markets in the region. As digital infrastructure continues to develop in emerging economies, disparities in internet penetration between high-income and low-income countries highlight significant growth potential.

- Allwyn Entertainment

- PlayHugeLottos

- Francaise des Jeux

- ZEAL Network SE

- Lotto Direct Ltd

- Lottoland

- Lotto Agent

- LottoKings

- WinTrillions

- Lotto247

- Annexio Ltd.

- China Welfare Lottery

- Intralot

- Sisal

- The Lottery Corporation

- International Game Technology (IGT)

- Flutter Entertainment (The Lotteries Pilot)

- NeoGames

- Pollard Banknote

- Jumbo Interactive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising penetration of digital wallets and mobile payments integration

- 4.2.2 Legalization and regulatory liberalization

- 4.2.3 Increasing global internet penetration

- 4.2.4 Cross-border jackpot pooling boosting prize sizes

- 4.2.5 Advancement of digital technologies

- 4.2.6 Micro-influencer affiliate marketing lowering acquisition costs

- 4.3 Market Restraints

- 4.3.1 Regulatory and legal challenges

- 4.3.2 App-store policy tightening on real-money gambling

- 4.3.3 Cybersecurity threats and fraud risks

- 4.3.4 Negative public perception and stigma

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Platform Type

- 5.1.1 Desktop

- 5.1.2 Mobile

- 5.2 By Game Type

- 5.2.1 Draw-based Lottery

- 5.2.2 Instant Lottery

- 5.2.3 Spots Lottery

- 5.2.4 Others

- 5.3 By Age Group

- 5.3.1 Below 25 Years

- 5.3.2 25-40 Years

- 5.3.3 40-55 Years

- 5.3.4 55+ Years

- 5.4 By End User

- 5.4.1 Male

- 5.4.2 Female

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 Sweden

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Italy

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 Oceanic Countries

- 5.5.3.2 Rest of Asia-Pacific

- 5.5.4 Rest of the Wolrd

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Allwyn Entertainment

- 6.4.2 PlayHugeLottos

- 6.4.3 Francaise des Jeux

- 6.4.4 ZEAL Network SE

- 6.4.5 Lotto Direct Ltd

- 6.4.6 Lottoland

- 6.4.7 Lotto Agent

- 6.4.8 LottoKings

- 6.4.9 WinTrillions

- 6.4.10 Lotto247

- 6.4.11 Annexio Ltd.

- 6.4.12 China Welfare Lottery

- 6.4.13 Intralot

- 6.4.14 Sisal

- 6.4.15 The Lottery Corporation

- 6.4.16 International Game Technology (IGT)

- 6.4.17 Flutter Entertainment (The Lotteries Pilot)

- 6.4.18 NeoGames

- 6.4.19 Pollard Banknote

- 6.4.20 Jumbo Interactive