|

市場調查報告書

商品編碼

1910671

油壓設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hydraulic Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

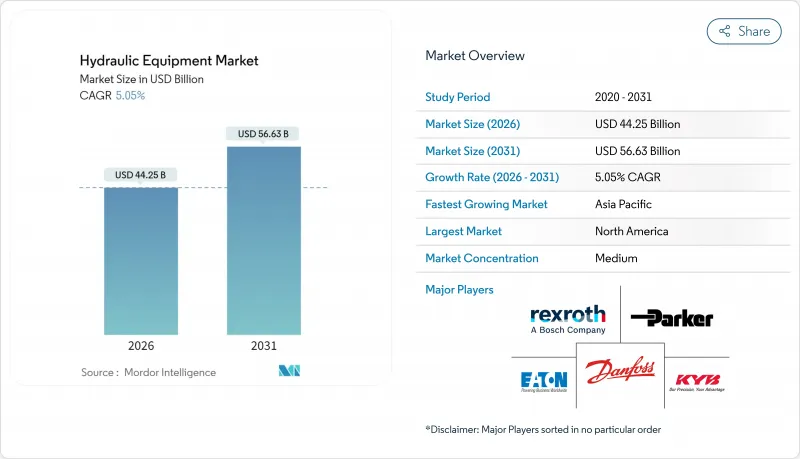

2025年油壓設備市場價值為421.1億美元,預計到2031年將達到566.3億美元,高於2026年的442.5億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.05%。

這一穩定成長展現了該產業在面對週期性放緩、原物料價格波動以及電氣化壓力日益增大等挑戰時的韌性。美國和中國強勁的公共基礎設施投資、全球電子商務中倉庫自動化程度的提高以及精密農業的擴張都支撐了市場需求。同時,設備製造商正在加速轉型為節能型電油壓混合動力技術。以應用工業技術公司(Applied Industrial Technologies)收購海德拉迪恩公司(Hydradyne)為例,產業整合加速,顯示供應商正在積極應對利潤率下降以及對數位化、高功率密度解決方案的需求。北美仍然是最大的區域市場,這得益於前所未有的水利基礎設施預算;而亞太地區則經歷了最快的成長,這主要得益於中國和印度向交通和城市服務獎勵策略注入了數兆美元。

全球油壓設備市場趨勢及展望

加速電子商務物流倉儲履約

為了因應電商訂單量的爆炸性成長,配銷中心正擴大部署自動堆高機、穿梭車系統和產品搬運機器人。這些機器依靠微型伺服油壓缸來實現毫米級的精度。亞馬遜的移動機器人網路表明,全天候運作需要配備感測器且無洩漏的液壓系統,同時還需要預測性維護來預先發現故障並最大限度地減少停機時間。倉庫營運商通常報告生產效率提高了 40%,這使得零件供應商能夠為超可靠、受污染控制的組件收取更高的價格。

政府主導的大型基礎建設項目

從1.2兆美元的美國基礎設施投資和就業創造法案到1.4兆美元的中國地方政府債務計劃,這些多年期公共工程項目對挖掘機、混凝土泵和大口徑油缸的需求預測不斷成長。長期計劃計劃使原始設備製造商(OEM)能夠獲得長期契約,擴大區域服務基地,並就橋樑、港口和可再生能源建設等特定應用領域的液壓系統展開合作。

鋼鐵和稀土等原物料價格波動加劇

預計到2024年,鋼鐵價格將出現40%的波動,而中國在稀土元素加工領域的主導地位將使磁鐵和電機供應鏈面臨地緣政治風險。對中國製造的液壓元件徵收44%至54%的關稅進一步擠壓了利潤空間,迫使供應商進行大宗商品套期保值、改變設計以減少材料用量,或透過併購擴張。

細分市場分析

2025年,泵浦作為建築、農業和工業機械的重要動力來源,將佔油壓設備市場27.85%的佔有率。可變排氣量和負載感應式泵浦可降低油耗,幫助原始設備製造商(OEM)實現效率目標,並促進售後市場改造銷售。預計到2031年,泵浦的油壓設備市場規模將隨著基礎設施投資週期的推進而成長。過濾器和蓄能器預計將以6.18%的複合年成長率實現最快成長,因為更嚴格的ISO 4406清潔度標準使得污染控制成為保固談判中的決定性因素。對高流量、低壓差過濾介質的需求提高了利潤率,而充氮囊可在混合動力迴路中儲存再生能源,從而擴大了該細分市場在行動應用領域的油壓設備市場佔有率。

閥門供應商將滿足遠端和自主任務對精確流量控制的需求。隨著電子商務倉儲機器人的普及,氣缸將受益於其對可重複、高循環線性運動的需求。馬達和變速器將服務於扭矩密度和過載能力至關重要的專用移動設備。由於整合式動力單元的普及簡化了OEM組裝並縮短了產品上市時間,輔助組件(儲液罐、歧管、冷卻器)的需求也將增加。

2025年,受全球公共工程項目和商業房地產建設項目開工量的推動,建築業將佔油壓設備市場收入的31.05%。車隊營運商正在採用電液油壓混合動力,以滿足日益嚴格的現場排放法規,同時維持較高的運轉率和零件消耗量。由於橋樑、港口和鐵路計劃在未來幾年內需要大量長行程致動器和重型泵,預計建築油壓設備市場規模將以中等個位數的成長率穩步成長。同時,受民用窄體飛機產量擴張和國防機構機身現代化改造的推動,航太和國防領域將呈現最快的成長軌跡,複合年成長率將達到6.35%。用於飛行控制和起落架的輕量化高壓致動器價格分佈,這使得航太供應商能夠佔據更大的油壓設備市場佔有率。

得益於精密農業中採用GPS引導液壓系統實現厘米級播種技術的應用,農業部門維持穩定成長。物料輸送產業因全通路零售物流的擴張而蓬勃發展,石油和天然氣產業的需求保持穩定,尤其是在海上結構物建造和管道維護方面。工具機、塑膠和汽車產業的趨勢雖然與全球製造業週期密切相關,但它們仍然是密封件、閥門和小直徑汽缸的重要批量生產基地。

區域分析

到2025年,北美將佔全球收入的37.65%,這得益於688億美元的水利基礎建設資金和8.5億美元的土地復墾計劃資金。強勁的倉儲自動化投資和老舊設備更新換代的需求將推動氣缸、比例閥和過濾套件的銷售。然而,運輸設備產業需求疲軟構成不利因素,供應商正專注於售後服務合約數位化維護服務。

預計到2031年,亞太地區將以8.07%的複合年成長率實現最高增速,其中中國1.4兆美元的信貸計劃以及印度的城市軌道交通和供水計劃將推動國內需求在經濟週期之外持續保持高峰。本地整車製造商正與零件專家合作以滿足Tier 4f排放標準,而關稅爭端則促使跨國供應商將其組裝基地多元化轉移至東南亞。高壓微型幫浦和防污閥在韓國和日本的精密製造群中得到越來越廣泛的應用。

歐洲前景喜憂參半。預計到2024年,德國流體動力訂單將下降8%,但法國的「大巴黎快線」項目和義大利的風電場建設計劃正在推動高壓油缸這一細分市場的需求。更嚴格的PFAS法規正在加速向生物基密封件的轉型,並推動油壓設備市場進行大規模的研發投資。歐盟再生能源計畫(REPowerEU)為可再生能源基礎設施撥款3,000億歐元(3,390億美元),預計提振離岸風力發電船舶用伸縮油缸的需求,從而緩解宏觀經濟疲軟的影響。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 產業供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 市場促進因素

- 加速電子商務物流倉儲履約

- 大型政府資助的基礎建設項目

- 轉向節能型電油壓混合動力

- 非公路領域電氣化程度的提高推動了緊湊型、高功率密度油壓設備的發展。

- 擴大精密農業機械的引進

- 經合組織國家老舊工業機械的更新週期

- 市場限制

- 在輕載範圍內,其總擁有成本(TCO)高於電動驅動系統。

- 鋼鐵和稀土元素等原物料價格波動加劇

- 增強型ESG監測液壓油洩漏

- 維修維修工作缺乏技術純熟勞工

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 透過裝置

- 泵浦

- 閥門

- 圓柱

- 馬達

- 過濾器和蓄能器

- 傳播

- 其他

- 按最終用戶行業分類

- 建造

- 農業

- 物料輸送

- 航太/國防

- 工具機

- 石油和天然氣

- 油壓機

- 塑膠

- 車

- 其他最終用戶

- 透過使用

- 移動液壓

- 工業固定式液壓系統

- 按工作壓力範圍

- 低壓(低於150巴)

- 中壓(150-350 巴)

- 高壓(高於 350 巴)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bosch Rexroth AG

- Parker Hannifin Corporation

- HYDAC International GmbH

- Danfoss A/S

- SMC Corporation

- Festo SE and Co. KG

- Norgren Limited(IMI plc)

- Bucher Hydraulics GmbH(Bucher Industries AG)

- HAWE Hydraulik SE

- Linde Hydraulics GmbH and Co. KG

- Caterpillar Inc.

- KYB Corporation

- Eaton Corporation plc

- Kawasaki Heavy Industries Ltd.

- Yuken Kogyo Co., Ltd.

- Daikin Industries, Ltd.

- Komatsu Ltd.

- Sun Hydraulics LLC(Helios Technologies, Inc.)

- Moog Inc.

- Argo-Hytos Group AG

第7章 市場機會與未來展望

The hydraulic equipment market was valued at USD 42.11 billion in 2025 and estimated to grow from USD 44.25 billion in 2026 to reach USD 56.63 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

This steady momentum underscores the sector's resilience in the face of cyclical slowdowns, raw material volatility, and intensifying pressures from electrification. Robust public infrastructure spending in the United States and China, rising warehouse automation in global e-commerce, and expanding precision agriculture underpin demand, even as equipment makers accelerate the shift toward energy-efficient electro-hydraulic hybrids. Heightened consolidation, exemplified by Applied Industrial Technologies' acquisition of Hydradyne, signals how suppliers are responding to margin compression and the need for digital, power-dense solutions. North America remains the largest regional base, supported by unprecedented water infrastructure appropriations, while the Asia-Pacific records the fastest gains as China and India commit multi-trillion-dollar stimulus to transport and urban services.

Global Hydraulic Equipment Market Trends and Insights

Accelerated Warehouse Automation in E-commerce Fulfillment

Explosive e-commerce order volumes compel distribution centers to deploy autonomous forklifts, shuttle systems, and goods-to-person robots that rely on compact servo-hydraulic cylinders for milli-meter accuracy. Amazon's network of mobile robots illustrates how 24/7 operation requires leak-free, sensor-equipped hydraulics offering predictive failure alerts to minimize downtime. Warehouse operators typically report 40% productivity gains, enabling component suppliers to charge premium prices for ultra-reliable, contamination-controlled assemblies.

Government-Funded Mega-Infrastructure Programmes

Multi-year public works-from the USD 1.2 trillion U.S. Infrastructure Investment and Jobs Act to China's USD 1.4 trillion local-government debt plan-create demand visibility for excavators, concrete pumps, and large-bore cylinders. Extended project pipelines allow OEMs to lock-in long-term contracts, expand regional service hubs, and co-develop application-specific hydraulics for bridge, port, and renewable-energy construction.

Intensifying Raw-Material Price Volatility for Steel and Rare Earths

Steel prices swung 40% in 2024, while China's dominance of rare-earth processing exposes magnet-motor supply chains to geopolitical risk. Tariffs of 44-54% on Chinese hydraulic components further compress margins, forcing suppliers to hedge commodities, redesign to reduce material intensity, or pursue scale through mergers.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Energy-Efficient Electro-Hydraulic Hybrids

- Increasing Off-Highway Electrification

- Skilled-Labor Shortage for Maintenance and Retrofits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pumps anchored 27.85% of the hydraulic equipment market in 2025 as the indispensable power-source across construction, agriculture, and industrial machinery. Variable-displacement and load-sensing models cut fuel draw, satisfying OEM efficiency targets and boosting aftermarket retrofit sales. The hydraulic equipment market size for pumps is positioned to advance with infrastructure investment cycles through 2031. Filters and accumulators log the quickest gains at a 6.18% CAGR as stricter ISO 4406 cleanliness codes make contamination control decisive during warranty negotiations. Demand for high-flow, low-delta-pressure filter media elevates margins, while nitrogen-charged bladders store regenerative energy in hybrid circuits, extending the hydraulic equipment market share of this sub-segment across mobile applications.

Valve suppliers capitalize on precision flow control required by tele-operation and autonomous tasks. Cylinders benefit from e-commerce warehouse robotics that necessitate repeatable, high-cycle linear motion. Motors and transmissions cater to specialty mobile equipment where torque density and overload capacity remain critical. Ancillary components-reservoirs, manifolds, coolers-gain from integrated power-packs that simplify OEM assembly lines and shorten time-to-market.

Construction contributed 31.05% of hydraulic equipment market revenue in 2025, buoyed by global public-works pipelines and commercial real-estate starts. Fleet operators adopt electro-hydraulic hybrids to meet stricter job-site emissions caps, sustaining high utilization and parts consumption. The hydraulic equipment market size for construction is poised for stable mid-single-digit growth as bridge, port, and rail projects consume long-stroke actuators and heavy-duty pumps over multi-year timelines. Aerospace and defense, however, posts the sharpest trajectory at 6.35% CAGR as commercial narrow-body production ramps and defense agencies modernize airframes. High-pressure, weight-optimized actuation for flight-control and landing-gear commands premium pricing, increasing the hydraulic equipment market share captured by aerospace suppliers.

Agriculture maintains steady gains as precision farming embeds GPS-guided hydraulics for centimeter-level seed placement. Material-handling thrives on omnichannel retail logistics, while oil and gas demand stabilizes around offshore construction and pipeline maintenance. Machine-tool, plastics, and automotive segments experience mixed trends tied to global manufacturing cycles yet remain indispensable volume anchors for seal, valve, and small-bore cylinder demand.

The Hydraulic Equipment Market Report is Segmented by Equipment Type (Pumps, Valves, Cylinders, Motors, Filters and Accumulators, Transmissions, and Others), End-User Industry (Construction, Agriculture, Material Handling, and More), Application (Mobile Hydraulics and Industrial Stationary Hydraulics), Operating-Pressure Range (Low, Medium, and High), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.65% of global revenue in 2025, supported by USD 68.8 billion in obligated water-infrastructure funds and USD 850 million dedicated to reclamation projects. Robust warehouse-automation investments and aging fleet replacements underpin sales of cylinders, proportional valves, and filtration kits. Nevertheless, the softness of transport equipment presents a headwind, prompting suppliers to emphasize aftermarket service contracts and digitalized maintenance offers.

The Asia-Pacific region registers the fastest growth, with an 8.07% CAGR through 2031, as China's USD 1.4 trillion credit package and India's urban-rail and water-supply programs sustain demand peaks beyond domestic cycles. Local OEMs partner with component specialists to meet Tier 4f standards, while tariff disputes prompt multinational suppliers to diversify assembly footprints into Southeast Asia. High-pressure micro-pumps and contamination-resistant valves are seeing a rising take-up in Korean and Japanese precision-manufacturing clusters.

Europe presents a mixed outlook: German fluid-power orders fell 8% in 2024, yet projects such as France's Grand Paris Express and Italy's wind-farm builds drive niche high-pressure requirements. PFAS restrictions are accelerating the shift to bio-based seals, prompting significant R&D investment across the hydraulic equipment market. The REPowerEU plan's EUR 300 billion (USD 339 billion) allocation for renewable energy infrastructure multiplies demand for telescopic cylinders in offshore wind installation vessels, cushioning macroeconomic softness.

- Bosch Rexroth AG

- Parker Hannifin Corporation

- HYDAC International GmbH

- Danfoss A/S

- SMC Corporation

- Festo SE and Co. KG

- Norgren Limited (IMI plc)

- Bucher Hydraulics GmbH (Bucher Industries AG)

- HAWE Hydraulik SE

- Linde Hydraulics GmbH and Co. KG

- Caterpillar Inc.

- KYB Corporation

- Eaton Corporation plc

- Kawasaki Heavy Industries Ltd.

- Yuken Kogyo Co., Ltd.

- Daikin Industries, Ltd.

- Komatsu Ltd.

- Sun Hydraulics LLC (Helios Technologies, Inc.)

- Moog Inc.

- Argo-Hytos Group AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Market Drivers

- 4.6.1 Accelerated warehouse automation in e-commerce fulfilment

- 4.6.2 Government-funded mega infrastructure programmes

- 4.6.3 Shift to energy-efficient electro-hydraulic hybrids

- 4.6.4 Increasing off-highway electrification driving compact power-dense hydraulics

- 4.6.5 Growing adoption of precision agriculture machinery

- 4.6.6 Ageing industrial machinery replacement cycle in OECD

- 4.7 Market Restraints

- 4.7.1 Total cost of ownership (TCO) higher than electric drives in light-duty ranges

- 4.7.2 Intensifying raw-material price volatility for steel and rare earths

- 4.7.3 Rising ESG scrutiny over hydraulic-fluid leakage

- 4.7.4 Skilled-labour shortage for maintenance and retrofits

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Pumps

- 5.1.2 Valves

- 5.1.3 Cylinders

- 5.1.4 Motors

- 5.1.5 Filters and Accumulators

- 5.1.6 Transmissions

- 5.1.7 Others

- 5.2 By End-user Industry

- 5.2.1 Construction

- 5.2.2 Agriculture

- 5.2.3 Material Handling

- 5.2.4 Aerospace and Defence

- 5.2.5 Machine Tools

- 5.2.6 Oil and Gas

- 5.2.7 Hydraulic Press

- 5.2.8 Plastics

- 5.2.9 Automotive

- 5.2.10 Other End-users

- 5.3 By Application

- 5.3.1 Mobile Hydraulics

- 5.3.2 Industrial Stationary Hydraulics

- 5.4 By Operating-Pressure Range

- 5.4.1 Low (Less than 150 bar)

- 5.4.2 Medium (150-350 bar)

- 5.4.3 High (Greater than 350 bar)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bosch Rexroth AG

- 6.4.2 Parker Hannifin Corporation

- 6.4.3 HYDAC International GmbH

- 6.4.4 Danfoss A/S

- 6.4.5 SMC Corporation

- 6.4.6 Festo SE and Co. KG

- 6.4.7 Norgren Limited (IMI plc)

- 6.4.8 Bucher Hydraulics GmbH (Bucher Industries AG)

- 6.4.9 HAWE Hydraulik SE

- 6.4.10 Linde Hydraulics GmbH and Co. KG

- 6.4.11 Caterpillar Inc.

- 6.4.12 KYB Corporation

- 6.4.13 Eaton Corporation plc

- 6.4.14 Kawasaki Heavy Industries Ltd.

- 6.4.15 Yuken Kogyo Co., Ltd.

- 6.4.16 Daikin Industries, Ltd.

- 6.4.17 Komatsu Ltd.

- 6.4.18 Sun Hydraulics LLC (Helios Technologies, Inc.)

- 6.4.19 Moog Inc.

- 6.4.20 Argo-Hytos Group AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球真空鑽井服務市場報告

2026年全球真空鑽井服務市場報告 工業油壓設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

工業油壓設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 油壓設備市場:2026-2032年全球市場預測(依產品類型、動力來源、系統類型、最終用戶產業及通路分類)全球工業油壓設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球液壓輔助設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球拆除機械液壓附件市場報告井口控制面板及系統市場(依控制系統類型、產品類型、井類型、壓力等級、系統材料及最終用戶產業分類),全球預測,2026-2032年井口控制面板和控制系統市場(依控制類型、面板類型、最終用途產業、壓力等級和井口配置分類)-全球預測,2026-2032年

油壓設備市場:2026-2032年全球市場預測(依產品類型、動力來源、系統類型、最終用戶產業及通路分類)全球工業油壓設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球液壓輔助設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球拆除機械液壓附件市場報告井口控制面板及系統市場(依控制系統類型、產品類型、井類型、壓力等級、系統材料及最終用戶產業分類),全球預測,2026-2032年井口控制面板和控制系統市場(依控制類型、面板類型、最終用途產業、壓力等級和井口配置分類)-全球預測,2026-2032年 日本油壓設備市場規模、佔有率、趨勢和預測:按類型、最終用途行業和地區分類,2026-2034年2026年全球油壓設備市場報告

日本油壓設備市場規模、佔有率、趨勢和預測:按類型、最終用途行業和地區分類,2026-2034年2026年全球油壓設備市場報告