|

市場調查報告書

商品編碼

1910569

現場可程式閘陣列(FPGA)-市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Field Programmable Gate Array (FPGA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

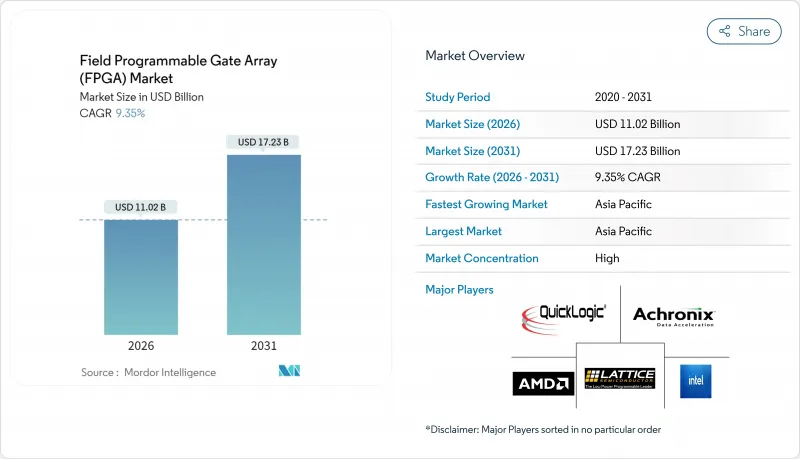

預計到 2025 年,現場可程式閘陣列(FPGA) 市值將達到 100.8 億美元,從 2026 年的 110.2 億美元成長到 2031 年的 172.3 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 9.35%。

邊緣人工智慧推理在超大規模資料中心的快速普及、向5G開放式無線架構的轉型,以及汽車和航太電子產業對部署後可重構性日益成長的需求,都為市場提供了清晰的成長動力。高階元件維持了其營收基礎,而中低階產品則隨著設計團隊在對成本敏感的工業、物聯網和消費系統中部署FPGA技術而快速成長。亞太地區已成為最大的製造地和成長最快的需求中心,這主要得益於汽車動力系統和新型太空衛星群日益成長的需求。英特爾同意分拆Altera後,競爭加劇,供應商動態也跟著重整。同時,出口限制促使中國國內同步發展。 300毫米晶圓代工廠產能的限制以及向16奈米及以下製程節點的高成本轉型,也迫使供應商優先考慮高收益應用,並與台積電和三星簽訂長期晶圓預訂協議。

全球FPGA(現場可程式閘陣列)市場趨勢與洞察

超大規模資料中心對邊緣AI推理的需求

當延遲和功耗預算開始超過純粹的處理容量要求時,超大規模營運商已採用 FPGA 來加速 AI 推理。 AMD 的第二代 Versal AI Edge 裝置的 TOPS/W 能源效率比第一代產品提高了 3 倍,可在降低營運成本的同時實現即時影像分析。 Achronix 報告稱,在運行大型語言模型時,FPGA 的成本和功耗比 GPU 方案低 200%,凸顯了 FPGA 在記憶體受限工作負載中的效率。這種轉變催生了一種分散式計算模型,該模型將推理處理更靠近資料來源,從而緩解了頻寬限制和資料主權風險。將封裝內 HBM 和強化型 AI 引擎整合到領先的 FPGA 系列中,鞏固了它們在雲端邊緣拓撲結構中的地位。因此,現場可程式閘陣列)市場在超大規模資本支出計畫中找到了永續成長的驅動力。

5G ORAN過渡需要無線電中的可程式設計邏輯。

開放式無線接取網路的願景正迫使通訊業者採用與廠商無關的無線單元,這些單元可以透過軟體升級而非全面更新設備來實現演進。英特爾的 Agilex 產品組合採用 10nm SuperFin 工藝,支援軟體定義無線電,能夠適應新的 5G 版本並降低整體擁有成本。萊迪思半導體 (Lattice Semiconductor) 為此硬體提供了參考協定棧,可為分散式網路提供零信任安全性和即時加密。 AMD 的 Zynq RFSoC DFE 的每瓦效能比之前的裝置提高了一倍,從而能夠在緊湊、功耗受限的射頻單元內實現多頻段運作。靈活的邏輯縮短了部署週期,成為通訊業者整合專用 5G、固定無線存取和毫米波服務的關鍵推動因素。這種柔軟性為通訊基礎設施領域的現場閘陣列 ( FPGA) 市場開闢了新的大規模應用機會。

對中國(美國/歐盟)高效能FPGA出口的限制

美國工業與安全局 (BIS) 的新規將於 2023 年底取消對中國出口的先進 FPGA 的民用豁免,限制適用於人工智慧和軍事應用的裝置出口。這項變更導致 AMD-Xilinx 和 Intel-Altera 暫停或授權大量訂單,造成短期出貨量下降。高文電子和盤古電子等中國供應商試圖填補供應缺口,但由於在取得設計工具、智慧財產權和先進製程方面存在障礙,即時難以實現替代。跨國客戶將敏感生產線遷出中國,或重新設計系統以適應非美國製造的裝置,擾亂了傳統的全球供應鏈。由此產生的不不確定性對現場閘陣列 ( FPGA) 市場造成了沉重打擊,直到新的貿易規則穩定下來。

細分市場分析

截至2025年,高階FPGA元件佔據了FPGA市場佔有率的65.80%,這反映了它們在資料中心加速和5G基礎設施中的核心作用。這些平台擁有超過100萬個邏輯單元,儘管價格分佈,卻能提供GPU無法企及的確定性延遲,從而維持了對安全至關重要的航太和金融科技工作負載的需求。中低階FPGA裝置到2031年的複合年成長率(CAGR)為10.85%,這得益於像Lattice這樣的製造商推出了成本最佳化的裝置,這些裝置配備了預硬體AI引擎,符合邊緣運算的預算要求。設計工具也變得更加直覺,使得不具備硬體專業知識的嵌入式工程師也能採用可配置邏輯。

AMD推出Spartan UltraScale+後,其價值提案發生了轉變。 Spartan UltraScale+功耗降低30%,I/O數量更是無與倫比,並將產品線從高階市場拓展到中階市場。同時,模組廠商透過提供預先檢驗電路板、簡化引腳規劃和PCB佈局,縮短了設計週期。這些變化有望縮小不同層級產品之間的價格差距,但隨著新的AI和網路標準的出現,以及這些標準僅由最高節點的晶片支持,高階元件仍將佔據現場可編程閘陣列)市場的大部分佔有率。

憑藉無限次重編程循環和強大的軟體生態系統,基於 SRAM 的解決方案預計到 2025 年將佔據 54.85% 的市場佔有率,複合年成長率 (CAGR) 為 11.45%。同時,基於快閃記憶體的方案在穿戴式裝置和車用通訊系統處理領域也日益受到認可,因為這些領域對即時啟動的要求極高。 Microchip 的 RT PolarFire 達到了 MIL-STD-883 B 級標準,在提供 100 krad 抗輻射能力的同時,功耗比同類 SRAM 裝置降低了 50%。耐熔熔絲平台在國防航空電子設備領域佔有一席之地,其一次性可程式性消除了篡改風險。

軟體可移植性的提升降低了傳統壁壘,使設計人員能夠根據功耗和安全性而非工具熟悉程度進行選擇。新興的異質架構將SRAM結構與片上非揮發性區域整合在一起,兼具兩者的優勢。雖然SRAM元件仍將繼續推動FPGA市場收入成長,但快閃記憶體和耐熔熔絲產品將在低功耗、嚴苛環境應用中佔據更大的佔有率。

現場可程式閘陣列依配置(高階 FPGA、中階/低階 FPGA)、架構(基於 SRAM 的 FPGA、基於快閃記憶體的 FPGA 等)、技術節點(90nm 及以上、20-90nm、16nm 及以下)、南美洲市場(資料中心/雲端運算、電信/5G 基礎設施、汽車細分)及以下)、北美地區市場(資料中心/雲端運算、電信/5G 基礎設施、汽車細分)及

區域分析

預計亞太地區將在2025年引領FPGA市場,營收佔比將達到39.10%,並在2031年之前維持16.20%的複合年成長率。中國在電動車驅動裝置和衛星有效載荷等領域的創新推動了半導體自主化進程,從而帶動了對FPGA的大規模需求。台灣和韓國擁有先進的製造技術,而日本則專注於汽車模組和工廠自動化子系統。萊迪思在印度浦那設立研發中心,促進了印度設計服務產業的發展,並擴大了工程人才儲備。

北美在資料中心基礎設施、高可靠性航太和EDA軟體領域保持主導。超大規模資料中心業者資料中心營運商為自適應加速器投入巨額資本預算,以控制人工智慧服務成本,從而在該地區佔據了強大的市場佔有率。出口許可證審查影響了出貨模式,但也推動了國內對先進封裝技術和OSAT(外包組裝和測試)能力的投資,以支持FPGA市場。

歐洲依賴德國汽車供應鏈和北歐電信設備供應商。 ISO 26262合規性推動了汽車應用的發展,而能源轉型計劃則催生了對低損耗功率轉換器的需求。歐盟「數位十年」政策鼓勵發展自主邊緣運算平台,並強調其可重構性。南美洲和中東及非洲目前市場佔有率較小,但5G基礎設施和工業現代化帶來的成長潛力預計將在預測期內提升其市場佔有率。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 超大規模資料中心對邊緣AI推理的需求

- 隨著我們向 5G ORAN 過渡,無線設備中對可程式設計邏輯的需求日益成長。

- ASIC/SoC 製程微縮週期(≤7 nm)中快速原型製作的需求

- 符合汽車產業功能安全標準(ISO 26262)

- 新型太空衛星群的抗輻射設計

- 中國電動車動力傳動系統OEM廠商採用eFPGA進行馬達控制

- 市場限制

- 美國和歐盟對高效能FPGA出口中國實施限制

- 300mm晶圓代工廠產能分配的波動性

- 與專用ASIC相比,靜態功耗增加

- 價值鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟趨勢對FPGA產業的影響

第5章 市場規模與成長預測

- 成分

- 高階FPGA

- 中低階FPGA

- 建築設計

- 基於SRAM的FPGA

- 基於快閃記憶體的FPGA

- 反熔絲FPGA

- 依技術節點

- 90奈米或以上

- 20~90 nm

- 16奈米或更小

- 按終端市場

- 資料中心和雲端運算

- 電訊和5G基礎設施

- 汽車(ADAS、電氣化)

- 工業自動化與機器人

- 航太與國防(航空電子設備、衛星通訊)

- 家用電子電器和穿戴式裝置

- 測試、測量和醫療設備

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家(瑞典、挪威、芬蘭、丹麥)

- 其他歐洲

- 亞太地區

- 中國

- 台灣

- 日本

- 韓國

- 印度

- ASEAN

- 亞太其他地區

- 南美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Advanced Micro Devices Inc.(Xilinx)

- Intel Corporation

- Lattice Semiconductor Corp.

- Microchip Technology Inc.(Microsemi)

- Achronix Semiconductor Corp.

- QuickLogic Corporation

- Efinix Inc.

- GOWIN Semiconductor Corp.

- Flex Logix Technologies Inc.

- NanoXplore SAS

- Anlogic Infotech Co. Ltd.

- Pango Microsystems Inc.

- Shenzhen S2C Ltd.

- BittWare(Molex Company)

- Digilent Inc.

- AlphaData Parallel Systems Ltd.

- Colfax International

- Reflex Ces SAS

- Aldec Inc.

- Beijing Tsinghua Tongfang Co. Ltd.

第7章 市場機會與未來展望

The field programmable gate array market was valued at USD 10.08 billion in 2025 and estimated to grow from USD 11.02 billion in 2026 to reach USD 17.23 billion by 2031, at a CAGR of 9.35% during the forecast period (2026-2031).

Rapid adoption of edge-AI inference in hyperscale data centers, the migration to 5G open radio architectures, and the rising need for post-deployment reconfigurability in automotive and aerospace electronics gave the market clear momentum. High-end devices continued to anchor revenues, yet mid-range and low-end products climbed quickly as design teams pushed FPGA technology into cost-sensitive industrial, IoT, and consumer systems. Asia-Pacific emerged as both the largest manufacturing base and the fastest-growing demand center, benefiting from electric-vehicle powertrains and new-space constellations. Competitive intensity increased after Intel agreed to carve out Altera, reshaping supplier dynamics while export controls spurred parallel domestic development in China. Tighter 300 mm foundry capacity and the costly transition to <=16 nm nodes also forced vendors to prioritize high-margin applications and long-term wafer reservations with TSMC and Samsung.

Global Field Programmable Gate Array (FPGA) Market Trends and Insights

Edge-AI inference demand in hyperscale data centers

Hyperscale operators deployed FPGAs to accelerate AI inference once latency and power budgets began outweighing raw throughput requirements. AMD's Versal AI Edge Gen 2 devices delivered up to 3 X higher TOPS-per-watt than first-generation parts, enabling real-time vision analytics while containing operating expenses. Achronix reported 200 % cost and power advantages versus GPU alternatives when running large language models, underscoring FPGA efficiency in memory-bound workloads. This shift unlocked a distributed compute model where inference processing moved closer to data sources, easing bandwidth constraints and data-sovereignty risks. Integration of on-package HBM and hardened AI engines within leading FPGA families strengthened their position in cloud-edge topologies. Consequently, the field programmable gate array market found a durable growth pillar in hyperscale capital expenditure plans.

5G ORAN shift requiring re-programmable logic in radios

Open radio access network initiatives pushed carriers to adopt vendor-agnostic radio units that could evolve with software upgrades rather than forklift replacements. Intel's Agilex portfolio used 10 nm SuperFin technology to deliver software-defined radios that adapt to new 5G releases at a lower total cost of ownership. Lattice Semiconductor complemented that hardware with a reference stack providing zero-trust security and real-time encryption for disaggregated networks. AMD's Zynq RFSoC DFE doubled performance per watt versus prior devices, letting operators support multi-band operation inside compact, power-constrained radio heads. Flexible logic shortened rollout cycles, a critical factor as carriers blended private-5G, fixed-wireless access, and mmWave services. That flexibility secured a new volume opportunity for the field programmable gate array market across telecom infrastructure.

US-EU export controls on high-performance FPGAs to China

New Bureau of Industry and Security rules removed civilian exemptions for advanced FPGA shipments to China in late 2023, restricting devices suited for AI or military use. The shift forced AMD-Xilinx and Intel-Altera to halt or license-screen many orders, reducing near-term unit volumes. Chinese suppliers such as GOWIN and Pango sought to close the gap, yet hurdles in design tools, IP, and advanced process access limited immediate substitution. Multinational customers moved sensitive production away from China or redesigned systems to qualify non-US devices, fracturing previously global supply chains. The resulting uncertainty weighed on the field programmable gate array market until new trade norms stabilized.

Other drivers and restraints analyzed in the detailed report include:

- Rapid prototyping needs for ASIC/SoC shrink cycles (<=7 nm)

- Functional safety compliance in automotive (ISO 26262)

- Volatility in 300 mm foundry capacity allocation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-end devices held 65.80% of the field programmable gate array market share in 2025, reflecting their central role in data-center acceleration and 5G infrastructure. These platforms, often exceeding 1 million logic cells, carried premium ASPs yet delivered deterministic latency unavailable in GPUs, preserving their appeal for safety-critical aerospace and fintech workloads. Mid-range and low-end devices exhibited an 10.85% CAGR to 2031 as manufacturers like Lattice shipped cost-optimized parts with hardened AI engines that met edge-compute budgets. Design tools have grown more intuitive, letting embedded engineers adopt configurable logic without hardware backgrounds.

The value proposition evolved as AMD introduced Spartan UltraScale+ with 30% lower power and unrivaled I/O count, attacking the mid-range from above. Simultaneously, module vendors supplied pre-validated boards that abstracted pin-planning and PCB layout, trimming design cycles. These shifts are expected to compress the pricing gap between tiers, although high-end devices still command a majority of the field programmable gate array market size when new AI or networking standards emerge that only top-node silicon can satisfy.

SRAM-based solutions owned 54.85% revenue in 2025 and posted an 11.45% CAGR outlook thanks to unlimited reprogram cycles and a deep software ecosystem. Yet flash-based variants gained mindshare in wearables and automotive telematics, where instant-on behavior is vital. Microchip's RT PolarFire achieved MIL-STD-883 Class B, offering 50% lower power than equivalent SRAM parts while tolerating 100 krad radiation. Anti-fuse platforms sustained a niche in defense avionics where one-time programmability eliminates tampering risk.

Software portability is shrinking historical barriers, so designers can now choose based on power and security rather than tool familiarity. Emerging heterogeneous architectures integrate SRAM fabric with on-die non-volatile domains, providing the best-of-both options. While SRAM devices will continue leading the field programmable gate array market revenue, flash and anti-fuse offerings should carve larger shares in low-power and harsh-environment deployments.

Field Programmable Gate Array is Segmented by Configuration (High-End FPGA, and Mid-range/Low-end FPGA), Architecture (SRAM-Based FPGA, Flash-Based FPGA, and More), Technology Node (>=90 Nm, 20-90 Nm, and <=16 Nm), End Market (Data Centre and Cloud Computing, Telecommunications and 5G Infrastructure, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the field programmable gate array market with 39.10% revenue in 2025 and showed a 16.20% CAGR outlook to 2031. China's push for semiconductor self-reliance, highlighted by domestic innovators in electric vehicle drives and satellite payloads, pulled in significant FPGA volumes. Taiwan and South Korea supplied advanced fabrication, while Japan specialized in automotive modules and factory automation subsystems. India's design-service sector advanced after Lattice opened an R&D center in Pune, broadening engineering talent pools.

North America maintained leadership in data-center infrastructure, high-reliability aerospace, and EDA software. Hyperscalers directed large capital budgets toward adaptive accelerators to manage AI service costs, ensuring the region's strong purchase share. Export-license reviews shaped shipment patterns but also prompted domestic investment in advanced packaging and OSAT capacity that supports the field programmable gate array market.

Europe leaned on Germany's automotive supply chain and Nordic telecom equipment providers. ISO 26262 compliance spurred in-vehicle usage, while energy-transition projects created demand for low-loss power converters. EU Digital Decade policies encouraged sovereign edge computing platforms that favor reconfigurability. Although South America and the Middle East, and Africa hold smaller slices today, growth potential in 5G infrastructure and industrial modernization should boost their contribution over the forecast period.

- Advanced Micro Devices Inc. (Xilinx)

- Intel Corporation

- Lattice Semiconductor Corp.

- Microchip Technology Inc. (Microsemi)

- Achronix Semiconductor Corp.

- QuickLogic Corporation

- Efinix Inc.

- GOWIN Semiconductor Corp.

- Flex Logix Technologies Inc.

- NanoXplore SAS

- Anlogic Infotech Co. Ltd.

- Pango Microsystems Inc.

- Shenzhen S2C Ltd.

- BittWare (Molex Company)

- Digilent Inc.

- AlphaData Parallel Systems Ltd.

- Colfax International

- Reflex Ces SAS

- Aldec Inc.

- Beijing Tsinghua Tongfang Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Edge-AI Inference Demand in Hyperscale Data Centres

- 4.2.2 5G ORAN Shift Requiring Re-programmable Logic in Radios

- 4.2.3 Rapid Prototyping Needs for ASIC/SoC Shrink Cycles (<=7 nm)

- 4.2.4 Functional Safety Compliance in Automotive (ISO 26262)

- 4.2.5 Radiation-Tolerant Designs for New-Space Constellations

- 4.2.6 Chinese EV Power-train OEMs Adopting eFPGAs for Motor Control

- 4.3 Market Restraints

- 4.3.1 US-EU Export Controls on High-performance FPGAs to China

- 4.3.2 Volatility in 300 mm Foundry Capacity Allocation

- 4.3.3 Higher Static Power Consumption vs. Dedicated ASIC

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the FPGA Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Configuration

- 5.1.1 High-end FPGA

- 5.1.2 Mid-range/Low-end FPGA

- 5.2 By Architecture

- 5.2.1 SRAM-based FPGA

- 5.2.2 Flash-based FPGA

- 5.2.3 Anti-fuse FPGA

- 5.3 By Technology Node

- 5.3.1 >=90 nm

- 5.3.2 20-90 nm

- 5.3.3 <=16 nm

- 5.4 By End Market

- 5.4.1 Data Centre and Cloud Computing

- 5.4.2 Telecommunications and 5G Infrastructure

- 5.4.3 Automotive (ADAS, Electrification)

- 5.4.4 Industrial Automation and Robotics

- 5.4.5 Aerospace and Defense (Avionics, SATCOM)

- 5.4.6 Consumer Electronics and Wearables

- 5.4.7 Test, Measurement and Medical Devices

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Nordics (Sweden, Norway, Finland, Denmark)

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Taiwan

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 India

- 5.5.3.6 ASEAN

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Mexico

- 5.5.4.2 Brazil

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overview, Core Segments, Financials, Strategy, Rank/Share, Products, Recent Moves)

- 6.4.1 Advanced Micro Devices Inc. (Xilinx)

- 6.4.2 Intel Corporation

- 6.4.3 Lattice Semiconductor Corp.

- 6.4.4 Microchip Technology Inc. (Microsemi)

- 6.4.5 Achronix Semiconductor Corp.

- 6.4.6 QuickLogic Corporation

- 6.4.7 Efinix Inc.

- 6.4.8 GOWIN Semiconductor Corp.

- 6.4.9 Flex Logix Technologies Inc.

- 6.4.10 NanoXplore SAS

- 6.4.11 Anlogic Infotech Co. Ltd.

- 6.4.12 Pango Microsystems Inc.

- 6.4.13 Shenzhen S2C Ltd.

- 6.4.14 BittWare (Molex Company)

- 6.4.15 Digilent Inc.

- 6.4.16 AlphaData Parallel Systems Ltd.

- 6.4.17 Colfax International

- 6.4.18 Reflex Ces SAS

- 6.4.19 Aldec Inc.

- 6.4.20 Beijing Tsinghua Tongfang Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

現場可程式閘陣列 (FPGA) 市場:2026-2032 年全球市場預測(按配置類型、節點尺寸、技術、架構、處理器類型和應用分類)FPGA 安全市場:按技術類型、整合、威脅類型和應用分類 - 2026-2032 年全球市場預測

現場可程式閘陣列 (FPGA) 市場:2026-2032 年全球市場預測(按配置類型、節點尺寸、技術、架構、處理器類型和應用分類)FPGA 安全市場:按技術類型、整合、威脅類型和應用分類 - 2026-2032 年全球市場預測 2026年全球現場可程式閘陣列市場報告

2026年全球現場可程式閘陣列市場報告 全球FPGA(現場可程式閘陣列)市場:按節點尺寸、應用、邏輯密度、裝置類型、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)

全球FPGA(現場可程式閘陣列)市場:按節點尺寸、應用、邏輯密度、裝置類型、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年) FPGA市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形狀、材料類型、最終用戶及部署方式分類

FPGA市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形狀、材料類型、最終用戶及部署方式分類 現場可程式閘陣列(FPGA) 市場機會、成長要素、產業趨勢分析及 2026 年至 2035 年預測2026年嵌入式現場可程式閘陣列(FPGA)全球市場報告

現場可程式閘陣列(FPGA) 市場機會、成長要素、產業趨勢分析及 2026 年至 2035 年預測2026年嵌入式現場可程式閘陣列(FPGA)全球市場報告 現場可程式閘陣列市場 - 全球產業規模、佔有率、趨勢、機會及預測(按技術、應用、配置、垂直產業、地區和競爭格局分類,2021-2031年)

現場可程式閘陣列市場 - 全球產業規模、佔有率、趨勢、機會及預測(按技術、應用、配置、垂直產業、地區和競爭格局分類,2021-2031年) FPGA 安全市場 - 2026-2031 年預測

FPGA 安全市場 - 2026-2031 年預測 FPGA加速市場預測至2032年:全球分析,依架構、結構類型、介面類型、應用、最終用戶及地區分類

FPGA加速市場預測至2032年:全球分析,依架構、結構類型、介面類型、應用、最終用戶及地區分類