|

市場調查報告書

商品編碼

1910442

皮革化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Leather Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

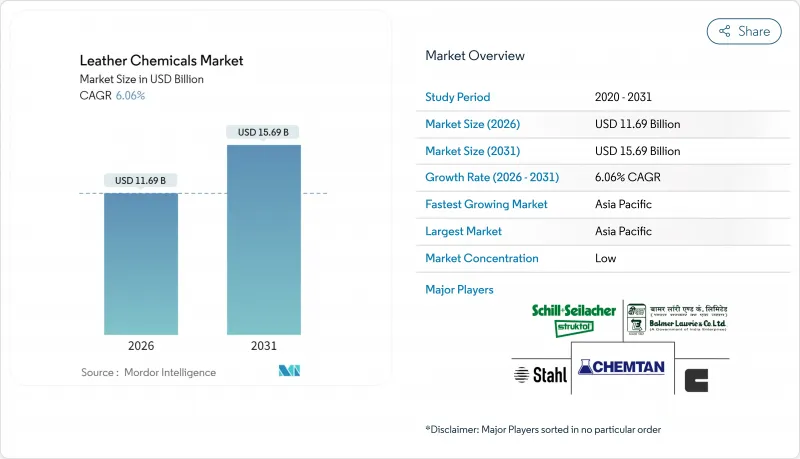

預計皮革化學品市場將從 2025 年的 110.2 億美元成長到 2026 年的 116.9 億美元,到 2031 年將達到 156.9 億美元,2026 年至 2031 年的複合年成長率為 6.06%。

這一上升趨勢主要受以下因素驅動:鉻鞣製程的穩定替代、高階鞋履和汽車內部裝潢建材需求的成長,以及生物基助劑的日益普及。無鉻鞣劑已在全球市場佔據主導地位,而由於產品性能要求日益嚴格,整理加工劑配方也備受關注。亞太地區在產量和創新方面均處於領先地位,儘管近期主導了一些旨在兼顧規模和永續性的整合舉措,但競爭格局依然分散。

全球皮革化學品市場趨勢與洞察

無鉻和無金屬鞣革技術的蓬勃發展

監管機構正在製定更嚴格的鉻含量標準,加速製造商向有機和無礦物鞣劑的轉型。加州2023年《鍍鉻替代技術標準》(ATCM)禁止新建六價鉻設施,並逐步淘汰裝飾性鍍鉻,進一步推動了無鉻化進程。像Gruppo Mastrotto這樣的生產商正在投資植物來源方法,以提高生物分解性並減少碳足跡。實驗室研究證實,生質能衍生的鞣劑比鉻鹽具有更高的分解速率,從而緩解了廢棄物處理的難題。 Stahl公司的Granofin Easy F-90 Liq展示了其獨特的配方如何在節約水和能源的同時消除六價鉻殘留。

鞋業和紡織業的快速成長

在拉里奧哈進行的試驗證實鞋內化合物具有有效的殺菌效果後,抗菌功能現已成為標準配置。中國當地每年加工約40億平方英尺的皮革,是皮革化學品市場中浸灰間和後整理化學品的最大單一客戶。紡織業在混紡鞋面上使用類似的整理加工劑,也創造了第二個需求來源。隨著中國對汽車皮革的需求激增,巴西供應商迅速做出反應,擴大了製革廠對華出口。

嚴格的六價鉻排放和廢水標準

歐洲化學品管理局 (ECHA) 計劃每年阻止 17 噸六價鉻 (Cr(VI)) 進入生態系統,這將迫使企業進行合規投資,從而擠壓制革廠的利潤空間。加州 65 號提案要求到 2025 年 12 月,所有皮革必須 100% 使用經認證的無鉻皮革,這迫使品牌商對其上游供應鏈進行審核。德國聯邦風險評估研究所的一份報告發現,超過一半的受檢皮革產品超過了 REACH 法規規定的 3 毫克/公斤基準值,這會帶來召回和法律風險。採用電化學氧化或芬頓製程升級廢水處理設施可以顯著減少廢水排放量,但這需要數百萬美元的資本投資。無法承擔這些成本或實施無鉻技術的中小型企業將面臨生存危機。

細分市場分析

從2026年到2031年,塗料整理劑將以6.72%的複合年成長率成長,成為成長最快的產業;而鞣革和染色劑的市佔率在2025年將維持在44.78%。製造商正在採用多功能面漆,這種面漆無需使用含氟添加劑即可賦予塗料耐磨性和抗菌性。活性絲素蛋白L1展現了生物基聚合物替代的潛力,同時實現了與溶劑型漆相媲美的光澤度。

制革產業持續轉向植物和合成有機體系,以緩解六價鉻排放問題並符合標籤認證要求。浸灰間清潔劑正逐步過渡到低pH值下清潔和脫脂的酵素複合物,以符合污水減量目標,從而使後整理化學品供應商獲得更高的附加價值利潤。同時,水場工段企業正透過提供可縮短製程週期的承包環保配方解決方案來豐富產品系列。

真皮化學品報告按產品類型(鞣製和染色化學品、浸灰間化學品、整理化學品)、化學功能(鉻基、無鉻礦物基、合成有機基)、最終用戶行業(鞋類、家具、汽車、紡織和時尚、其他最終用戶行業)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。

區域分析

預計到2025年,亞太地區將佔全球營收的48.37%,並在2026年至2031年間以6.65%的複合年成長率成長。印度預計在2023會計年度將出口價值52.6億美元的皮革製品,並僱用442萬名工人,這將推動對浸灰間輔助劑和整理加工劑的需求。區域成本優勢、一體化的供應鏈以及不斷成長的國內消費意味著亞太地區仍然是新增產能擴張的中心。日本和韓國的買家需要小批量的高純度合成鞣劑和麵漆,並且更傾向於選擇擁有ISO 14001認證工廠和不含揮發性有機化合物(VOC)配方的供應商。

北美和歐洲是成熟市場,價格高昂,合規援助往往超過每公升折扣。在歐洲,成品中的鉻含量限制已收緊至低於3毫克/公斤,這推動了義大利、西班牙和德國對無鉻產品的訂單激增。加州要求在2025年中期,75%的企業必須符合鉻安全標準,這使得上游審核和綠色標籤認證變得更加迫切。這些法規將推動對生物基合成樹脂、低霧鞣革油和短週期回收系統的支出。北美汽車內裝工廠要求使用符合美墨加協定(USMCA)的材料,並優先考慮在當地設有混合站的供應商。這兩個地區共同推動了對永續、高性能化學品的需求。

南美洲是全球生皮供應地,但在地化加工也正在蓬勃發展。匯率波動和歐盟可追溯性法規為成本結構帶來了挑戰,但也推動了對自動化浸灰間線的投資。中東的製革廠正在利用石油化學原料生產特殊單寧,而非洲的新計畫正從濕藍皮出口轉向硬皮和成品革,從而擴大了綜合加工解決方案的基本客群。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 無鉻和無金屬鞣革技術的蓬勃發展

- 鞋類和紡織業的快速成長

- 汽車和飛機內部裝潢建材的需求不斷成長

- 人們對生物基潤滑劑和合成鞣劑的偏好日益成長

- 數位雷射列印化學品的需求不斷成長

- 市場限制

- 對六價鉻排放和污水處理制定嚴格的規定

- 高昂的能源和污水處理成本

- 來自合成皮革和植物皮革化學品的競爭

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 鞣革和染色化學品

- 浸灰間 Chemicals

- 表面處理化學品

- 透過化學功能

- 鉻基

- 無鉻礦物

- 合成有機物

- 按最終用戶行業分類

- 鞋類

- 家具

- 車

- 紡織與時尚

- 其他終端使用者產業(重型工業皮革製品、馬具等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AMIT

- Balmer Lawrie & Co. Ltd.

- Buckman

- Chemtan Company, Inc.

- CLARIANT

- Dyna Glycols

- DyStar Singapore Pte Ltd.

- Fashion Chemicals GmbH & Co. KG

- Indofil Industries Limited.

- SCHILL+SEILACHER GMBH

- Sisecam

- Stahl Holdings BV

- Syn-Bios SpA

- TEXAPEL SA

- TFL

- YILDIRIM Group Of Companies

- Zschimmer & Schwarz Chemie GmbH

第7章 市場機會與未來展望

The Leather Chemicals Market is expected to grow from USD 11.02 billion in 2025 to USD 11.69 billion in 2026 and is forecast to reach USD 15.69 billion by 2031 at 6.06% CAGR over 2026-2031.

The uptrend is driven by the steady replacement of chromium-based tanning, increased demand from premium footwear and automotive interiors, and wider adoption of bio-based auxiliaries. Chrome-free chemical functions already dominate global demand, while finishing formulations are gaining traction thanks to stricter product-performance requirements. Asia-Pacific leads in both output and innovation, and the competitive field remains fragmented despite recent consolidation initiatives that seek to pair scale with sustainability.

Global Leather Chemicals Market Trends and Insights

Surge in Chrome-Free and Metal-Free Tanning Technologies

Regulators are setting strict chromium thresholds, spurring manufacturers to shift toward organic and mineral-free tanning agents. California's 2023 Chrome Plating ATCM bans new hexavalent chromium facilities and phases out decorative chrome plating, adding momentum to chrome-free adoption. Producers such as Gruppo Mastrotto have invested in vegetable-based methods, citing better biodegradability and shrinking carbon footprints. Laboratory studies confirm that biomass-based agents deliver higher degradation rates than chromium salts, easing end-of-life treatment challenges. Stahl's Granofin Easy F-90 Liq showcases how proprietary formulations save water and energy while eliminating Cr(VI) residues.

Rapid Growth of Footwear and Textile Industries

Antibacterial performance features are now routine after testing in La Rioja confirmed effective microbe kill rates for in-shoe compounds. Mainland China processes nearly 4 billion ft2 of hides per year, making it the largest single customer of beam-house and finishing chemicals in the leather chemicals market. The textile sector adds a second demand stream by utilizing similar finishing agents on mixed material uppers. Brazil's supply reacted quickly, exporting more tanned hides to China as local auto leather volumes escalated.

Strict Chromium VI Emission and Wastewater Norms

ECHA plans to stop 17 tonnes of Cr(VI) from entering ecosystems each year, imposing compliance investments that strain tanners' margins. California's Proposition 65 requires 100% certified chrome-safe leather by December 2025, forcing brands to audit upstream supply chains. The German Federal Institute for Risk Assessment reported that more than half of the tested leather items exceed the 3 mg/kg REACH limit, sparking recalls and legal exposure. Upgrading effluent plants with electrochemical oxidation or Fenton processes can slash water draw-off, but it involves multimillion-dollar capital outlay. Smaller workshops face existential risks if they cannot absorb these costs or secure chrome-free expertise.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Automotive and Aviation Upholstery

- Rising Preference for Bio-Based Fatliquors and Syntans

- Competition from Synthetic and Vegan Leather Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Finishing chemicals registered the highest 6.72% CAGR between 2026 and 2031, while tanning and dyeing agents retained 44.78% of the 2025 volume. Manufacturers adopt multifunctional topcoats that grant abrasion resistance and antimicrobial traits without fluorinated inputs. Activated Silk L1 demonstrates how bio-based polymers can replace solvent-driven lacquers while matching gloss metrics.

The tanning segment continues to pivot toward vegetable and synthetic organic systems, easing Cr(VI) discharge worries and satisfying label certification schemes. Beam-house detergents have moved toward enzyme complexes that clean and degrease at lower pH, aligning with wastewater reduction goals. Finishing suppliers thus capture premium margins, while wet-end players strengthen portfolios with turnkey eco-recipes that shorten process cycles.

The Leather Chemicals Report is Segmented by Product Type (Tanning and Dyeing Chemicals, Beam-House Chemicals, and Finishing Chemicals), Chemical Function (Chrome-Based, Chrome-Free Mineral, and Synthetic Organic), End-User Industry (Footwear, Furniture, Automotive, Textile and Fashion, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific controlled 48.37% of 2025 revenue and is forecast to grow at a 6.65% CAGR during 2026-2031. India exported USD 5.26 billion worth of leather goods in FY 2023 and employs 4.42 million workers, amplifying demand for beam-house auxiliaries and finishing agents. Regional cost advantages, integrated supply pools, and rising domestic consumption keep APAC at the epicenter of new capacity expansions. Japanese and South Korean buyers, though smaller in volume, demand high-purity syntans and topcoats, favoring suppliers with ISO 14001 plants and VOC-free recipes.

North America and Europe present mature but premium-priced outlets where compliance support often outweighs per-liter discounts. Europe tightened chromium limits to below 3 mg/kg in finished goods, driving chrome-free orders in Italy, Spain, and Germany. California prescribed 75% compliance to chrome-safe standards by mid-2025, adding urgency for upstream audits and green-tag certificates. These rules channel spending into bio-based synthetics, low-fogging fatliquors, and short-cycle recycling systems. North American auto trim plants require USMCA-proven content and favor suppliers offering regional blending stations. Together, the two regions sustain demand for sustainable high-performance chemicals.

South America supplies raw hides globally yet is increasing local finishing. Currency swings and EU traceability rules challenge cost structures but also encourage investments in automated beam-house lines. Middle Eastern tanneries leverage petrochemical feedstocks for specialty syntans, while new African projects look to shift from wet-blue exports to crust or finished leather, widening the client base for comprehensive processing solutions.

- AMIT

- Balmer Lawrie & Co. Ltd.

- Buckman

- Chemtan Company, Inc.

- CLARIANT

- Dyna Glycols

- DyStar Singapore Pte Ltd.

- Fashion Chemicals GmbH & Co. KG

- Indofil Industries Limited.

- SCHILL+SEILACHER GMBH

- Sisecam

- Stahl Holdings B.V.

- Syn-Bios S.p.A.

- TEXAPEL S.A.

- TFL

- YILDIRIM Group Of Companies

- Zschimmer & Schwarz Chemie GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Chrome-Free and Metal-Free Tanning Technologies

- 4.2.2 Rapid Growth of Footwear and Textile Industries

- 4.2.3 Increasing Demand for Automotive and Aviation Upholstery

- 4.2.4 Rising Preference for Bio-Based Fatliquors and Syntans

- 4.2.5 Digital Leather Printing Chemicals Gaining Traction

- 4.3 Market Restraints

- 4.3.1 Strict Chromium VI Emission and Wastewater Norms

- 4.3.2 High Energy and Wastewater-Treatment Cost

- 4.3.3 Competition From Synthetic and Vegan Leather Chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tanning and Dyeing Chemicals

- 5.1.2 Beam-house Chemicals

- 5.1.3 Finishing Chemicals

- 5.2 By Chemical Function

- 5.2.1 Chrome-based

- 5.2.2 Chrome-free Mineral

- 5.2.3 Synthetic Organic

- 5.3 By End-user Industry

- 5.3.1 Footwear

- 5.3.2 Furniture

- 5.3.3 Automotive

- 5.3.4 Textile and Fashion

- 5.3.5 Other End-user Industries (Heavy Leather and Saddlery, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMIT

- 6.4.2 Balmer Lawrie & Co. Ltd.

- 6.4.3 Buckman

- 6.4.4 Chemtan Company, Inc.

- 6.4.5 CLARIANT

- 6.4.6 Dyna Glycols

- 6.4.7 DyStar Singapore Pte Ltd.

- 6.4.8 Fashion Chemicals GmbH & Co. KG

- 6.4.9 Indofil Industries Limited.

- 6.4.10 SCHILL+SEILACHER GMBH

- 6.4.11 Sisecam

- 6.4.12 Stahl Holdings B.V.

- 6.4.13 Syn-Bios S.p.A.

- 6.4.14 TEXAPEL S.A.

- 6.4.15 TFL

- 6.4.16 YILDIRIM Group Of Companies

- 6.4.17 Zschimmer & Schwarz Chemie GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

皮革染料市場規模、佔有率和成長分析:按染料類型、應用、最終用途、通路和地區分類-2026-2033年產業預測

皮革染料市場規模、佔有率和成長分析:按染料類型、應用、最終用途、通路和地區分類-2026-2033年產業預測 皮革化學品市場報告:按化學品類型、產品類型、最終用戶和地區分類(2026-2034 年)

皮革化學品市場報告:按化學品類型、產品類型、最終用戶和地區分類(2026-2034 年) 皮革染料市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

皮革染料市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 皮革化學品市場規模、佔有率和趨勢分析報告:按產品、製程、應用、地區和細分市場預測,2026-2033年

皮革化學品市場規模、佔有率和趨勢分析報告:按產品、製程、應用、地區和細分市場預測,2026-2033年 2026-2034年全球皮革化學品市場規模、佔有率、趨勢和成長分析報告日本皮革化學品市場規模、佔有率、趨勢和預測:按產品、工藝、應用和地區分類,2026-2034年

2026-2034年全球皮革化學品市場規模、佔有率、趨勢和成長分析報告日本皮革化學品市場規模、佔有率、趨勢和預測:按產品、工藝、應用和地區分類,2026-2034年 2026年全球皮革化學品市場報告

2026年全球皮革化學品市場報告 皮革黏合劑市場按應用、產品類型、形式、皮革類型和通路—2026-2032年全球預測皮革化學品市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,預測(2026-2034年)皮革染料市場規模、佔有率、成長及全球產業分析:按應用和地區劃分的洞察與預測(2026-2034)

皮革黏合劑市場按應用、產品類型、形式、皮革類型和通路—2026-2032年全球預測皮革化學品市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,預測(2026-2034年)皮革染料市場規模、佔有率、成長及全球產業分析:按應用和地區劃分的洞察與預測(2026-2034)