|

市場調查報告書

商品編碼

1913366

皮革化學品市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)Leather Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

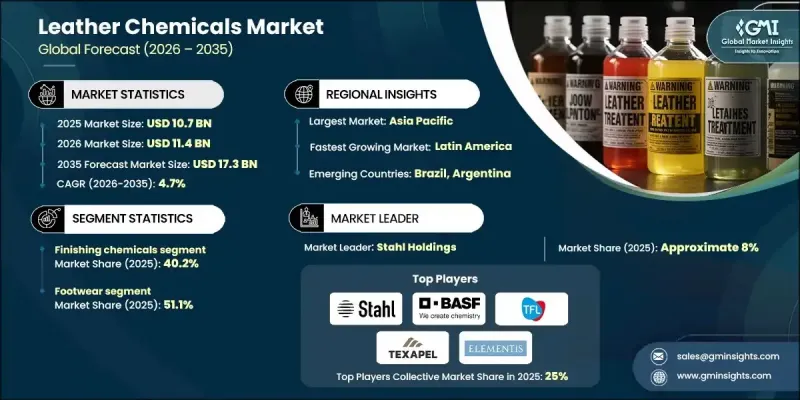

全球皮革化學品市場預計到 2025 年將達到 107 億美元,到 2035 年將達到 173 億美元,年複合成長率為 4.7%。

市場成長與汽車內裝、豪華家具和高階時尚領域對優質皮革的需求不斷成長密切相關。消費者對精緻紋理、耐用性和視覺吸引力的需求日益成長,促使化學品製造商開發先進的配方技術,以上游工程提升皮革品質。汽車產業仍然是關鍵的成長引擎,推動著高性能內裝皮革的持續需求,因為製造商不斷優先考慮輕質、優質的內裝內部裝潢建材。同時,由於日益嚴格的環境法規,皮革化學產業正經歷結構性轉型。向替代鞣製系統和環保加工方法的轉變正在加速,尤其是在已開發地區。化學品供應商正在重新設計其產品以滿足不斷變化的合規標準,促使環保助劑、先進染料和酵素解決方案得到更廣泛的應用。這些趨勢正在重塑全球皮革生產方式,同時保持終端用戶產業所需的性能、均勻性和美觀性。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 107億美元 |

| 市場規模預測 | 173億美元 |

| 複合年成長率 | 4.7% |

2025年,皮革整理化學品市佔率佔比達40.2%,預計到2035年將以4.4%的複合年成長率成長。該細分市場保持主導地位,主要得益於其在提升成品皮革表面外觀、耐用性和功能性能方面發揮的關鍵作用。皮革整理化學品的強勁貢獻也體現在其能夠顯著提高皮革產品的商業性價值,使其成為價值鏈中不可或缺的一部分。

2025年,鞋類市佔率佔比達51.1%,預計2026年至2035年將以4.7%的複合年成長率成長。全球大規模鞋類生產以及對符合嚴格物理、視覺和性能標準的皮革的需求是推動這一成長的主要因素。消費者對優質耐用鞋履日益成長的偏好,促使他們更加依賴特種鞣劑、先進的後整理解決方案和性能增強型化學體系,其中亞太地區、拉丁美洲和歐洲部分地區的成長尤為顯著。

預計到2025年,北美皮革化學品市佔率將達到5%。該地區的需求主要受汽車價值鏈以及室內裝潢和高檔鞋履市場偏好變化的驅動。美國正逐步轉向高品質且永續的皮革解決方案,而加拿大對法規遵循和永續採購的重視,則推動了對先進整理系統和替代鞣革化學品的需求。

目錄

第1章:分析方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要企業的競爭分析

- 競爭定位矩陣

- 主要趨勢

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 按類型分類的市場估算與預測(2022-2035 年)

- 預處理化學品

- 浸沒

- 石灰處理

- 脫鈣和拍打

- 曬黑

- 鉻

- 非鉻

- 染色

- 水溶性

- 不溶於水

- 表面處理化學品

- 聚氨酯

- 丙烯酸纖維

- 矽酮

- 其他

- 其他

第6章 按應用領域分類的市場估算與預測(2022-2035 年)

- 鞋類

- 休閒鞋和時尚鞋

- 運動鞋

- 安全鞋和工業鞋

- 靴子

- 家具

- 住宅裝飾

- 辦公家具

- 飯店家具

- 豪華真皮座椅

- 車

- 汽車座椅和內裝

- 方向盤和變速桿蓋

- 門板

- 摩托車座椅

- 衣服

- 皮夾克

- 褲子和裙子

- 腰帶

- 外套和外衣

- 手套

- 工業和安全手套

- 時尚手套

- 運動手套

- 戰術/軍用手套

- 其他

- 包包

- 皮夾和小飾品

- 馬具

- 體育用品

第7章 各地區市場估算與預測(2022-2035 年)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第8章 公司簡介

- ATC Tannery Chemicals

- Balmer Lawrie &Co. Ltd.

- BASF SE

- Clariant International Ltd.

- DyStar Group

- Elementis plc

- FGL International SpA

- Industrias Quimicas Iris, SA

- Kolon Industries, Inc.

- PIOVAN Leather Chemicals

- Schill+Seilacher GmbH

- Sisecam Chemicals

- Stahl Holdings

- Syntans &Colloids

- Texal

- Texapel

- TFL Ledertechnik GmbH

- Trumpler GmbH &Co. KG

- Zschimmer &Schwarz GmbH &Co KG

- Others

The Global Leather Chemicals Market was valued at USD 10.7 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 17.3 billion by 2035.

Market growth is closely linked to rising consumption of premium leather across automotive interiors, luxury furniture, and high-end fashion segments. Increasing demand for refined texture, durability, and visual appeal has encouraged chemical producers to innovate advanced formulations that enhance leather quality during upstream processing. The automotive sector remains a significant growth engine, as manufacturers continue to prioritize lightweight and premium interior materials, leading to sustained demand for high-performance upholstery and interior leather. At the same time, the leather chemicals industry is undergoing a structural transformation driven by tightening environmental regulations. The shift toward alternative tanning systems and environmentally responsible processing methods is accelerating, particularly across developed regions. Chemical suppliers are responding by reformulating products to meet evolving compliance standards, resulting in higher adoption of eco-friendly auxiliaries, advanced dyes, and enzyme-driven solutions. These developments are reshaping leather production practices globally while maintaining performance, consistency, and aesthetic value across end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.7 Billion |

| Forecast Value | $17.3 Billion |

| CAGR | 4.7% |

The finishing chemicals segment accounted for 40.2% share in 2025 and is projected to grow at a CAGR of 4.4% through 2035. This segment maintains leadership due to its critical role in enhancing surface appearance, durability, and functional performance of finished leather. The strong contribution of finishing chemicals is also supported by their ability to significantly increase the commercial value of leather products, making them indispensable within the production chain.

The footwear segment held 51.1% share in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. Demand is driven by large-scale global footwear manufacturing and the need for leather that meets strict physical, visual, and performance standards. Rising preference for premium and durable footwear has increased reliance on specialized tanning agents, advanced finishing solutions, and performance-enhancing chemical systems, with notable growth observed across Asia-Pacific, Latin America, and parts of Europe.

North America Leather Chemicals Market accounted for 5% share in 2025. Regional demand is primarily supported by the automotive value chain and evolving preferences in upholstery and premium footwear. The United States continues to witness gradual shifts toward higher-quality and sustainable leather solutions, while Canada's emphasis on regulatory compliance and sustainable sourcing has strengthened demand for advanced finishing systems and alternative tanning chemistries.

Key companies active in the Global Leather Chemicals Market include BASF SE, Stahl Holdings, Clariant International Ltd., TFL Ledertechnik GmbH, DyStar Group, Zschimmer & Schwarz GmbH & Co KG, Trumpler GmbH & Co. KG, Balmer Lawrie & Co. Ltd., Schill + Seilacher GmbH, ATC Tannery Chemicals, Texapel, Texal, Sisecam Chemicals, Elementis plc, Kolon Industries, Inc., PIOVAN Leather Chemicals, Industrias Quimicas Iris, S.A., FGL International S.p.A., and Syntans & Colloids. Companies operating in the Global Leather Chemicals Market are strengthening their competitive position through product innovation, sustainability-focused reformulation, and geographic expansion. Key strategies include developing compliant and environmentally responsible chemical solutions that align with evolving regulatory frameworks. Firms are investing in research to improve leather performance while reducing environmental impact. Strategic partnerships with tanneries and OEMs are helping suppliers secure long-term contracts and enhance market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Beamhouse Chemicals

- 5.2.1 Soaking

- 5.2.2 Liming

- 5.2.3 Deliming and Bating

- 5.3 Tanning

- 5.3.1 Chrome

- 5.3.2 Non-Chrome

- 5.4 Dyeing

- 5.4.1 Water Soluble

- 5.4.2 Non-water Soluble

- 5.5 Finishing Chemicals

- 5.5.1 Polyurethane

- 5.5.2 Acrylic

- 5.5.3 Silicone

- 5.5.4 Others

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Footwear

- 6.2.1 Casual and Fashion Shoes

- 6.2.2 Sports Shoes

- 6.2.3 Safety/Industrial Footwear

- 6.2.4 Boots

- 6.3 Furniture

- 6.3.1 Residential Upholstery

- 6.3.2 Office Furniture

- 6.3.3 Hospitality Furniture

- 6.3.4 Luxury Leather Seating

- 6.4 Automobile

- 6.4.1 Car Seats & Upholstery

- 6.4.2 Steering Wheel & Gear Covers

- 6.4.3 Door Panels

- 6.4.4 Motorcycle Seats

- 6.5 Garments

- 6.5.1 Leather Jackets

- 6.5.2 Trousers & Skirts

- 6.5.3 Belts

- 6.5.4 Coats & Outerwear

- 6.6 Gloves

- 6.6.1 Industrial/Safety Gloves

- 6.6.2 Fashion Gloves

- 6.6.3 Sports Gloves

- 6.6.4 Tactical/Military Gloves

- 6.7 Others

- 6.7.1 Bags & Luggage

- 6.7.2 Wallets & Small Accessories

- 6.7.3 Saddlery

- 6.7.4 Sporting Goods

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 ATC Tannery Chemicals

- 8.2 Balmer Lawrie & Co. Ltd.

- 8.3 BASF SE

- 8.4 Clariant International Ltd.

- 8.5 DyStar Group

- 8.6 Elementis plc

- 8.7 FGL International S.p.A.

- 8.8 Industrias Quimicas Iris, S.A.

- 8.9 Kolon Industries, Inc.

- 8.10 PIOVAN Leather Chemicals

- 8.11 Schill + Seilacher GmbH

- 8.12 Sisecam Chemicals

- 8.13 Stahl Holdings

- 8.14 Syntans & Colloids

- 8.15 Texal

- 8.16 Texapel

- 8.17 TFL Ledertechnik GmbH

- 8.18 Trumpler GmbH & Co. KG

- 8.19 Zschimmer & Schwarz GmbH & Co KG

- 8.20 Others

日本皮革化學品市場規模、佔有率、趨勢和預測:按產品、工藝、應用和地區分類,2026-2034年

日本皮革化學品市場規模、佔有率、趨勢和預測:按產品、工藝、應用和地區分類,2026-2034年 2026年全球皮革化學品市場報告

2026年全球皮革化學品市場報告 皮革黏合劑市場按應用、產品類型、形式、皮革類型和通路—2026-2032年全球預測

皮革黏合劑市場按應用、產品類型、形式、皮革類型和通路—2026-2032年全球預測 皮革化學品市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,預測(2026-2034年)

皮革化學品市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,預測(2026-2034年) 皮革化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)皮革染料市場規模、佔有率、成長及全球產業分析:按應用和地區劃分的洞察與預測(2026-2034)

皮革化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)皮革染料市場規模、佔有率、成長及全球產業分析:按應用和地區劃分的洞察與預測(2026-2034) 皮革化學品市場規模、佔有率和成長分析(按產品、製程、應用和地區分類)-2026-2033年產業預測皮革化學品市場報告(按化學品類型、產品、最終用戶和地區)2025-2033全球皮革化學品市場:區域、範圍和預測

皮革化學品市場規模、佔有率和成長分析(按產品、製程、應用和地區分類)-2026-2033年產業預測皮革化學品市場報告(按化學品類型、產品、最終用戶和地區)2025-2033全球皮革化學品市場:區域、範圍和預測 皮革化學品市場報告:2030 年趨勢、預測與競爭分析

皮革化學品市場報告:2030 年趨勢、預測與競爭分析