|

市場調查報告書

商品編碼

1907317

鈮:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Niobium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

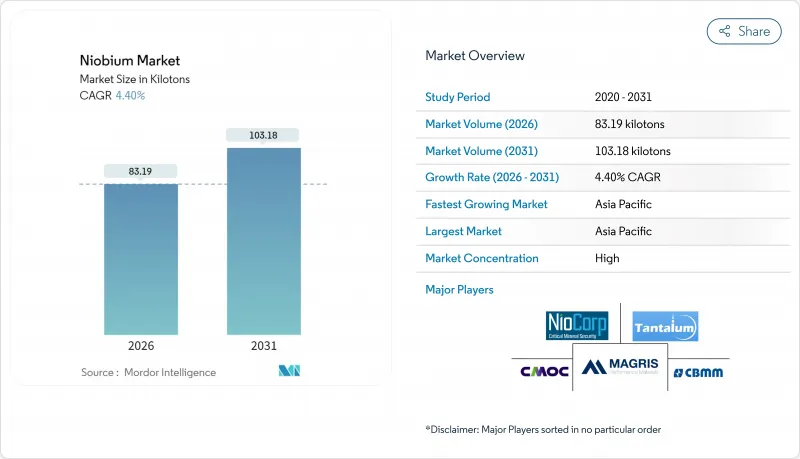

預計鈮市場將從 2025 年的 79.68 千噸成長到 2026 年的 83.19 千噸,到 2031 年將達到 103.18 千噸,2026 年至 2031 年的複合年成長率為 4.4%。

建築和汽車製造業對高強度低合金鋼(HSLA)的持續需求支撐著此擴張,因為添加微量鈮可將抗張強度提高高達30%,同時保持良好的焊接性能。以巴西為中心的集中供應基地將價格穩定在每公斤45至50美元,這有利於簽訂長期供應協議,從而降低大型基礎設施計劃的採購風險。市場對添加鈮的電池負極材料、量子級超導體和耐氫管鋼的興趣日益濃厚,促進了終端市場的多元化,使鈮市場免受鋼鐵週期放緩的影響。加拿大和美國的供應多元化措施旨在降低巴西主導地位帶來的地緣政治風險,並加強國內關鍵礦產戰略。

全球鈮市場趨勢與洞察

建築業中高強度低合金鋼(HSLA鋼)的應用日益廣泛

隨著建築規範的修訂,為提升抗震性能,建築材料對強度重量比提出了更高的要求。含鈮量為0.02%至0.05%的高強度低合金鋼(HSLA)相比傳統鋼材,強度可提高20%至30%,同時還能降低用量。中國2024年抗震規範明確規定高樓必須使用鈮微合金鋼,印尼和墨西哥也考慮類似的修訂。工程公司正將鈮材規範納入其長期基礎設施規劃,因為儘管材料成本會增加5%至8%,但結構鋼的使用量可減少最多20%。隨著亞洲和非洲新一輪都市化進程的加速,建築需求佔鈮總消費量的49%以上,進一步鞏固了鈮市場的穩定基礎。監管力度的加大將使高強度低合金鋼(HSLA)的普及應用在十年內成為不可逆轉的趨勢。

促進汽車和造船產業的輕量化發展

更嚴格的燃油經濟性目標和船舶排放法規正在推動積極的輕量化策略。鈮摻雜的先進高強度鋼目前已應用於超過60%的高階車型,並且隨著原始設備製造商(OEM)在提升碰撞安全性和增加電池重量之間尋求平衡,這種鋼材在量產車型平台上的應用也日益廣泛。在造船領域,添加鈮的低溫高強度低合金鋼(HSLA)能夠滿足液化天然氣(LNG)運輸船在-162°C低溫下的斷裂韌性要求,從而支持韓國和卡達的船隊更新。商用卡車和鐵路車輛製造商也傾向於採用鈮增強樑和底盤零件,在無需進行重大設計改造的情況下提高負載效率。這種跨產業的應用週期使鈮市場能夠充分利用多個產業的協同效應,而不是僅僅依賴單一領域。

急性暴露引起的健康與環境問題

鈮礦通常與釷和鈾共生,因此開採過程中需要嚴格的輻射監測。在巴西,監管機構現在要求在許可證續約前進行地下水基準調查和同位素測繪,這使得合規成本增加了15%至25%。圍繞原住民居住地區的爭議進一步延緩了新採礦許可證的核准,加拿大「火環」地區也面臨類似的社區參與挑戰。雖然尚未有工業暴露水準下出現慢性中毒病例的報告,但公眾對風險的認知可能會影響資本投資決策並限制供應彈性。

細分市場分析

碳酸鹽礦床在2025年佔全球鈮供應量的95.85%,預計到2031年將以4.43%的複合年成長率成長,這將支撐鈮市場的成長動能。巴西阿拉沙礦的特點是剝採比低、礦石粗粒燒綠石,且選礦製程簡單,能夠以具競爭力的營運成本生產鈮鐵。

目前,探勘投資主要集中在格陵蘭島和坦尚尼亞探勘的碳酸岩礦床,但尚未發現像阿拉克薩礦場那樣規模的礦藏,延續了現有供應集中的趨勢。可預測的礦物成分和數十年來累積的冶金技術確保了穩定的加工量,為長期供應合約奠定了基礎,並增強了鈮市場的價格穩定性。日本和德國的戰略儲備商繼續優先採購碳酸鹽岩原料,因為其雜質組成穩定,有助於簡化合金廠的品管。

2025年,鈮鐵的出貨量佔比高達92.75%,預計到2031年將以4.35%的複合年成長率成長,與全球粗鋼需求趨勢相符。通常含鈮量為65%的中間合金可無縫整合到鹼性氧氣轉爐熔煉製程中,使熔煉車間技術人員能夠精確控制晶粒尺寸和析出速率。儘管氧化鈮目前市場佔有率較小,但由於電池和介電陶瓷需求的成長,其成長速度正在加快。 CBMM的專用氧化物生產線計畫在2030年實現年產4萬噸的目標。

真空金屬和特殊合金粉末為航太引擎、核磁共振磁鐵和量子裝置提供原料,儘管產量較低,但單價仍然很高。隨著積層製造技術的日益普及,預計對球形C-103粉末的需求將超過板材和棒材,使加工商的收入來源更加多元化。因此,雖然鈮鐵仍將是主要產品,但高純度衍生將推動整個鈮鐵產業的利潤率成長。

本鈮報告依礦床類型(碳酸鹽岩及相關礦床、鈮鉭鐵礦)、產品類型(鈮鐵、氧化鈮等)、應用(鈮鐵、超導磁體和電容器等)、終端用戶產業(建築、汽車和南美、航太和國防等)以及北美地區(亞太地區、北美地區、歐洲地區、中東地區和國防等)。

區域分析

預計亞太地區將繼續佔據鈮市場最大的區域佔有率,到 2025 年將佔全球產量的 60.10%,到 2031 年將以 4.71% 的複合年成長率成長。中國龐大的鋼鐵產量和不斷發展的抗震標準將支撐巨大的需求,而探索鈮矽合金的航太計畫正在擴大其在下一代推進系統中的應用。

北美地區的成長取決於兩大主題:交通工具的脫碳以及國防主導的高超音速技術發展。美國環保署(EPA)更嚴格的燃油經濟性法規和各州零排放強制令正促使汽車製造商(OEM)採用鈮強化鋼來減輕車輛重量,並平衡日益成長的電池系統重量。儘管加拿大尼奧貝克礦的產量約佔全球總產量的8%至10%,美國決策者仍將透過埃爾克溪礦實現供應來源多元化視為一項戰略重點,以減少對巴西進口的依賴。

在歐洲,氫氣管道的擴建(需要鈮微合金化的API X70級鋼材)正在推動淨零排放目標的實現。在汽車產業,嚴格的二氧化碳排放法規促使高抗張強度鋼在沖壓領域廣泛應用。在德國的汽車產業叢集中,鈮鐵的添加使得輕量化素車組裝成為可能。同時,挪威的礦產策略將鈮列為國內探勘的優先資源,並修訂了相關許可法規。該地區也支持為歐洲核子研究中心(CERN)加速器升級而進行的鈮超導體基礎研究,從而在更廣泛的鈮市場中保持著以研究為導向的鈮超導體基礎研究,從而在更廣泛的鈮市場中保持著以研究主導的鈮產業地位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 建築業中高強度低合金鋼(HSLA鋼)的應用日益廣泛

- 促進汽車和造船產業的輕量化發展

- 氫氣和液化天然氣運輸管道的建設

- 擴大鈮摻雜鋰離子電池的生產規模

- 用於航太工業的積層製造鈮合金

- 市場限制

- 巴西的供應集中度與定價權

- 急性暴露引起的健康與環境問題

- ESG可追溯性成本

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 技術概述/生產分析

- 價格趨勢

第5章 市場規模與成長預測

- 按發生狀態

- 碳酸岩及相關礦物

- 鈮鉭鐵礦

- 按類型

- 鈮鐵

- 氧化鈮市場

- 鈮市場金屬

- 用於真空的鈮合金

- 透過使用

- 鋼

- 超合金

- 超導磁鐵和電容器

- 電池

- 其他用途

- 按最終用戶行業分類

- 建造

- 汽車和造船

- 航太/國防

- 石油和天然氣

- 其他最終用戶

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 俄羅斯

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Admat Inc.

- American Elements

- Australian Strategic Materials Ltd

- CBMM

- Changsha South Tantalum Niobium Co. Ltd

- CMOC

- Grandview Materials

- Magris Performance Materials

- NioCorp Development Ltd

- Titanex GmbH

第7章 市場機會與未來展望

The Niobium market is expected to grow from 79.68 kilotons in 2025 to 83.19 kilotons in 2026 and is forecast to reach 103.18 kilotons by 2031 at 4.4% CAGR over 2026-2031.

Sustained demand for high-strength low-alloy (HSLA) steel in construction and automotive manufacturing anchors this expansion because micro-additions of the element raise tensile strength by up to 30% while preserving weldability. Price stability between USD 45-50 per kilogram, maintained by a concentrated supply base led by Brazil, encourages long-term offtake agreements that lower procurement risk for large infrastructure projects. Rising interest in niobium-doped battery anodes, quantum-grade superconductors, and hydrogen-ready pipeline steels is broadening end-market diversity, cushioning the niobium market against potential slowdowns in the steel cycle. Supply-side diversification efforts in Canada and the United States aim to mitigate geopolitical risk tied to Brazil's dominance and to reinforce domestic critical-minerals strategies.

Global Niobium Market Trends and Insights

Rising HSLA Steel Adoption in Construction

Building-code revisions now mandate higher strength-to-weight ratios for seismic resilience, and HSLA steels containing 0.02-0.05% niobium deliver 20-30% strength gains over conventional grades while cutting tonnage requirements. China's 2024 seismic standards explicitly cite niobium-microalloyed steels for high-rise projects, and similar updates are under review in Indonesia and Mexico. Because material cost premiums remain 5-8% yet structural steel volumes fall by up to 20%, engineering firms are embedding niobium specifications across long-term infrastructure plans. As new urbanization waves in Asia and Africa accelerate, construction demand anchors more than 49% of overall niobium consumption, reinforcing a stable baseline for the niobium market. Regulatory momentum makes HSLA adoption essentially irreversible within a decade horizon.

Lightweighting Push in Automotive and Shipbuilding

Stricter fuel-economy targets and maritime emission limits foster aggressive mass-reduction strategies. Advanced high-strength steels incorporating niobium now appear in over 60% of premium-segment vehicles and are migrating into mass-market platforms as OEMs balance crashworthiness with battery-induced weight penalties. In shipbuilding, cryogenic-grade HSLA plate with niobium additions satisfies LNG-carrier requirements for fracture toughness at -162 °C, supporting fleet renewal across South Korea and Qatar. Commercial trucking and railcar builders likewise gravitate toward niobium-enhanced beam and chassis components, improving payload efficiency without major design overhauls. The cross-modal adoption cycle positions the niobium market for multi-industry synergies rather than single-sector dependency.

Acute-exposure Health and Environmental Concerns

Niobium ores often coexist with thorium and uranium, necessitating strict radiological surveillance during mining. Regulatory authorities in Brazil now require groundwater baselines and isotopic mapping before license renewals, adding 15-25% to compliance costs. Indigenous-territory debates further delay greenfield approvals, and similar community-engagement hurdles appear in Canada's Ring of Fire region. While no chronic-toxicity cases have been documented at industrial exposure levels, public perception risks can influence capex decisions, tempering supply-side agility.

Other drivers and restraints analyzed in the detailed report include:

- Pipeline Build-out for Hydrogen and LNG Transmission

- Niobium-doped Li-ion Batteries Scale-up

- ESG Traceability Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbonatite-hosted deposits held 95.85% of the 2025 global supply and are set to expand at a 4.43% CAGR through 2031, underpinning the niobium market size growth trajectory. Brazil's Araxa mine exemplifies low-strip ratios and coarse-grained pyrochlore that simplify beneficiation, yielding ferroniobium at competitive opex levels.

Exploration spending now targets undercover carbonatites in Greenland and Tanzania; however, no discovery approaches Araxa's scale, reinforcing existing supply concentration. Predictable mineralogy and decades of metallurgical know-how translate into steady throughput, anchoring long-term delivery contracts and reinforcing the niobium market's pricing stability. Strategic stockpilers in Japan and Germany continue to favor carbonatite feed due to consistent impurity profiles that streamline alloy-shop quality control.

Ferroniobium accounted for 92.75% of 2025 shipments and is forecast to post a 4.35% CAGR through 2031, mirroring global crude-steel demand patterns. The master alloy, usually containing 65% niobium, integrates seamlessly into basic-oxygen furnace practices, enabling melt-shop engineers to fine-tune grain size and precipitation kinetics. Niobium oxide, while representing a minor share today, is pacing up on the back of battery and dielectric-ceramic uptake; CBMM's dedicated oxide line targets 40,000 tons annual capacity by 2030.

Vacuum-grade metal and specialty alloy powders feed aerospace engines, MRI magnets, and quantum devices, commanding premium unit values in spite of small tonnages. As additive manufacturing spreads, demand for spherical C-103 powder is likely to outpace bulk plate and bar, diversifying revenue streams for converters. Consequently, ferroniobium will remain the volume anchor, but high-purity derivatives will shape margin dynamics across the niobium industry.

The Niobium Report is Segmented by Occurrence (Carbonatites and Associates and Columbite-Tantalite), Type (Ferroniobium, Niobium Oxide, and More), Application (Steel, Super-Alloys, Superconducting Magnets and Capacitors, and More), End-User Industry (Construction, Automotive and Shipbuilding, Aerospace and Defense, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific held 60.10% of 2025 global volume and is forecast to grow at a 4.71% CAGR to 2031, securing the largest regional slice of the niobium market. China's gargantuan steel output and evolving seismic codes sustain bulk demand, while aerospace programs exploring niobium-silicon alloys extend uptake into next-generation propulsion systems.

North America's growth hinges on dual themes: decarbonization of transport fleets and defense-driven hypersonic development. Tightened EPA fuel-economy rules and state-level zero-emission mandates push OEMs toward niobium-enriched steels for chassis mass reduction, counterbalancing heavier battery systems. Canada's Niobec mine supplies roughly 8-10% of global output, but U.S. policymakers continue to view diversification via Elk Creek as a strategic imperative to curb reliance on Brazilian imports.

Europe targets net-zero targets by expanding hydrogen pipelines that demand niobium-microalloyed API X70 grades, and stringent vehicle CO2 limits sustain high-strength steel penetration in automotive stamping. Germany's auto clusters integrate ferroniobium additions to deliver lighter body-in-white assemblies, while Norway's mineral strategy lists niobium as a priority for domestic exploration under revised permitting rules. The region also supports fundamental research into niobium-tin superconductors for CERN's accelerator upgrades, sustaining a research-driven niche inside the broader niobium market.

- Admat Inc.

- American Elements

- Australian Strategic Materials Ltd

- CBMM

- Changsha South Tantalum Niobium Co. Ltd

- CMOC

- Grandview Materials

- Magris Performance Materials

- NioCorp Development Ltd

- Titanex GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HSLA Steel Adoption in Construction

- 4.2.2 Lightweighting Push in Automotive and Shipbuilding

- 4.2.3 Pipeline Build-Out for Hydrogen and LNG Transmission

- 4.2.4 Niobium-Doped Li-Ion Batteries Scale-Up

- 4.2.5 Additive-Manufactured Nb Alloys for Aerospace

- 4.3 Market Restraints

- 4.3.1 Supply Concentration in Brazil and Pricing Power

- 4.3.2 Acute-Exposure Health and Environmental Concerns

- 4.3.3 ESG Traceability Compliance Costs

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot/ Production Analysis

- 4.6 Price Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Occurrence

- 5.1.1 Carbonatites and Associates

- 5.1.2 Columbite-Tantalite

- 5.2 By Type

- 5.2.1 Ferroniobium

- 5.2.2 Niobium Oxide

- 5.2.3 Niobium Metal

- 5.2.4 Vacuum-grade Nb Alloys

- 5.3 By Application

- 5.3.1 Steel

- 5.3.2 Super-alloys

- 5.3.3 Superconducting Magnets and Capacitors

- 5.3.4 Batteries

- 5.3.5 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Construction

- 5.4.2 Automotive and Shipbuilding

- 5.4.3 Aerospace and Defense

- 5.4.4 Oil and Gas

- 5.4.5 Other End-users

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Russia

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Admat Inc.

- 6.4.2 American Elements

- 6.4.3 Australian Strategic Materials Ltd

- 6.4.4 CBMM

- 6.4.5 Changsha South Tantalum Niobium Co. Ltd

- 6.4.6 CMOC

- 6.4.7 Grandview Materials

- 6.4.8 Magris Performance Materials

- 6.4.9 NioCorp Development Ltd

- 6.4.10 Titanex GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

五氧化二鈮市場-2026-2032年全球市場預測

五氧化二鈮市場-2026-2032年全球市場預測 鈮棒市場規模、佔有率和成長分析:按產品類型、形狀和規格、應用領域、終端用戶產業和地區分類-2026-2033年產業預測

鈮棒市場規模、佔有率和成長分析:按產品類型、形狀和規格、應用領域、終端用戶產業和地區分類-2026-2033年產業預測 五氧化二鈮:市場佔有率分析、產業趨勢與統計、成長預測(2025-2031)

五氧化二鈮:市場佔有率分析、產業趨勢與統計、成長預測(2025-2031) 四甲基庚二酮鈮市場規模、佔有率和成長分析:按產品等級/純度、應用/製程技術、最終用途、最終用途產業和地區分類 - 產業預測,2026-2033年

四甲基庚二酮鈮市場規模、佔有率和成長分析:按產品等級/純度、應用/製程技術、最終用途、最終用途產業和地區分類 - 產業預測,2026-2033年 2026-2034年全球五氧化二鈮市場規模、佔有率、趨勢和成長分析報告鈮及鈮合金市場按類型、應用、終端用戶產業、形態、等級及生產方法分類-2026-2032年全球預測

2026-2034年全球五氧化二鈮市場規模、佔有率、趨勢和成長分析報告鈮及鈮合金市場按類型、應用、終端用戶產業、形態、等級及生產方法分類-2026-2032年全球預測 五氧化二鈮市場規模、佔有率及成長分析(按等級、應用和地區)-產業預測,2025-2032

五氧化二鈮市場規模、佔有率及成長分析(按等級、應用和地區)-產業預測,2025-2032 全球五氧化二鈮市場

全球五氧化二鈮市場 2032 年鈮市場預測:按類型、純度等級、通路、應用、最終用戶和地區進行的全球分析

2032 年鈮市場預測:按類型、純度等級、通路、應用、最終用戶和地區進行的全球分析 全球鈮市場規模研究,按類型(鈮鐵、鈮氧化物、鈮金屬)、按應用(結構鋼、汽車鋼、管道鋼、不銹鋼等)和區域預測 2022-2032

全球鈮市場規模研究,按類型(鈮鐵、鈮氧化物、鈮金屬)、按應用(結構鋼、汽車鋼、管道鋼、不銹鋼等)和區域預測 2022-2032